andresr

Investment Summary

As we trawl through the small-cap medical technology space here at HBI I’m never ceased to be amazed at the level of innovation within the domain. What’s equally exciting is the prospects for some complex disease segments further down the line. Case in point is DermTech, Inc. (NASDAQ:DMTK) a, relatively new player to the scene after listing in 2017 that has its roots ground in the dermatological diagnostics market. Specifically, melanoma.

The company’s assay menu provides a differentiated offering to examining and diagnosing melanoma, an otherwise complex task. Here, I’ll be discussing our examination findings on the underlying market, the company’s product offerings and what this means for investors looking ahead.

Net-net, we rate DMTK a hold right now, and are acutely aware of the risks in this name [listed below]. Nonetheless, we remain constructive, and I’ve attempted to share where the market opportunity could be in this name looking further down the line.

Before proceeding, investors should have a deep understanding of the risks in investing with DMTK, a small-cap equity:

1. Regulatory Risk: DMTK is subject to regulation by the U.S. Food and Drug Administration (“FDA”). Any changes to the FDA’s regulations or approval process could have a negative impact on DMTK’s revenue and profitability.

2. Market Risk: There are inherent risks in investing in small-cap equities. DMTK stock is subject to market risk, which is the risk of fluctuations in the stock price due to factors such as changes in the overall market, industry trends, and investor sentiment. Moreover, fundamentals can become disconnected from technicals, producing large volatility spikes in the DMTK share price.

3. Competitor Risk: DMTK faces competition from new and established companies in the field of skin diagnostics. If competitors develop products that are more effective or less expensive than DMTK ’s products, it could have a significant impact on the company’s profitability.

5. Financing Risk: Given its small size and relatively small market capitalization, it may not be able to access the capital needed to fund growth initiatives. This could limit the company’s ability to compete in the marketplace.

Investors should understand these risks in full before proceeding any further.

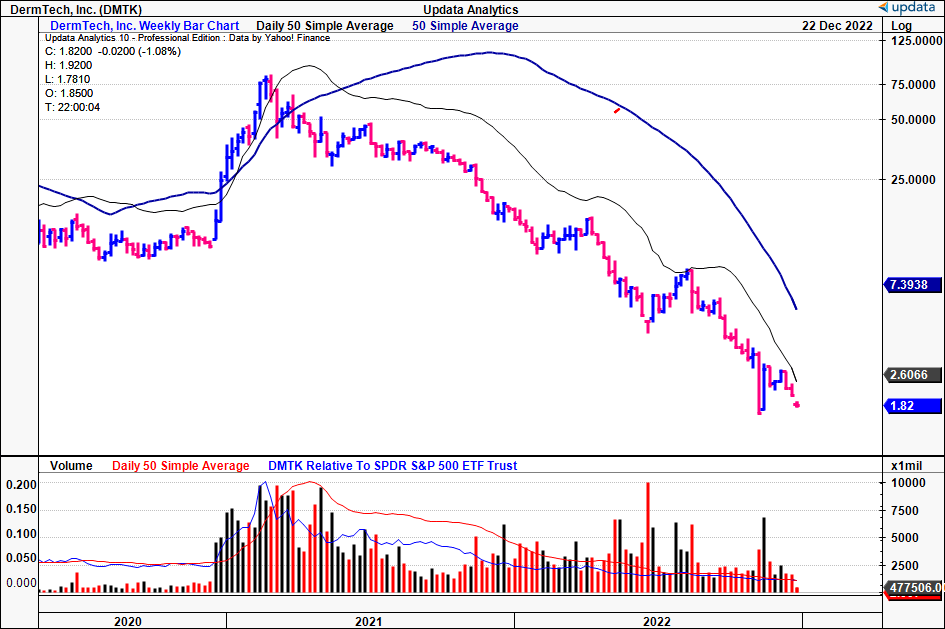

Exhibit 1. DMTK weekly price evolution. The FY22′ year hasn’t been kind to the stock.

Data: Updata

DMTK underlying market opportunity

In order to understand the investment opportunity in DMTK down the line, it’s first important to understand the underpinnings of melanoma and its diagnostics market.

The skin cancer diagnostics market, comprising the development and provision of diagnostic tests and tools for the detection and diagnosis of skin cancer, is expected to reach a value of ~$5.5 Bn by 2028, experiencing a CAGR of ~7.2% over that time. The Asia Pacific (“APAC”) region is anticipated to be the fastest-growing region in the market, with a CAGR of 8.5% from 2021 to 2028.

The melanoma segment is projected to be the fastest-growing segment of the market, with a forecast CAGR of 7.5% during the period. Herein lies the opportunity for DMTK. It is positioned uniquely in the diagnostics portion of the value chain here, and differentiates itself through its PLA division.

Melanoma is a neoplastic disease of the skin that arises from the melanocytes, the pigment-producing cells of the epidermis. Histopathology wise, the condition results from the unrestrained proliferation and division of said melanocytes. It is generally induced by exposure to ultraviolet (“UV”) radiation from the sun or artificial sources, such as tanning beds. Moreover, it is the most aggressive and potentially lethal form of skin cancer.

According to the World Health Organization (“WHO”), melanoma is the fifth most common cancer among males and the seventh most common cancer among females globally. The incidence of melanoma has been on the rise in numerous parts of the world in recent decades. In the U.S., it is estimated that there will be more than 4mm new cases of skin cancer diagnosed in 2022, and over 5mm new cases diagnosed worldwide each year.

Melanoma can occur on any cutaneous site, but it is most commonly found on the trunk and extremities in males and the extremities, face, and neck in females. It can also occur on mucosal surfaces, such as the oral cavity and conjunctiva, as well as the nails. The condition is often characterized by the presence of dark or irregularly shaped moles, or ‘nevi’, on the skin. These nevi may be black, brown, or multicolored and may have an irregular border or be asymmetrical in shape.

The early detection and management of melanoma is crucial for improving patient outcomes. If caught early, the condition can often be treated successfully through the surgical excision of the malignant tissue. More advanced cases may require adjuvant therapies, such as chemotherapy, radiotherapy, or immunotherapy.

Hence, there is an unmet clinical and medical need for a breakthrough in this complex disease segment. DMTK’s penetration of this segment, in our opinion, could open up the floodgates for a fast-growing subset within the broad-based oncology diagnostics market. Hence, it’s unsurprising why we are constructive this early on in this name.

Which brings us to DMTK’s pigmented lesion assay (“PLA”).

DMTK’s clear differentiator within the domain is its PLA division. We believe this is a potential long-term compounder with interesting economics tied into the mix. The PLA is a non-invasive diagnostic technique used to evaluate pigmented lesions (moles) on the skin for the presence of melanoma. It utilizes a small sample of cells collected from a mole using an adhesive patch, which are then analyzed using a proprietary genetic test from DMTK’s clinical laboratory to identify specific genetic markers associated with melanoma.

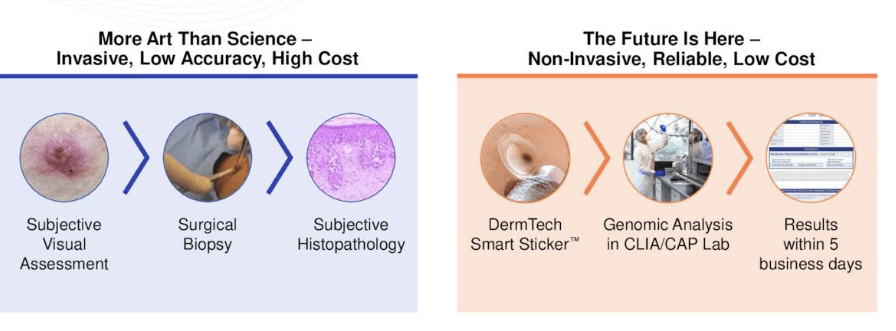

The advantage of the assay is that it enables the early detection and diagnosis of melanoma, which can improve patient outcomes, as mentioned. Melanoma is often challenging to diagnose in its early stages, as it can be mistaken for a benign mole. Traditional diagnostic methods, namely skin biopsy, can be invasive and isn’t suitable for all patients. Not to mention, the initial and downstream costs associated with biopsies.

Underlying challenges with melanoma detection, diagnosis, with PLA’s attempts to address these.

Data: DMTK Q3 FY22 investor presentation, Seeking Alpha.

Conversely, the PLA is non-invasive and can be performed expeditiously and easily in a doctor’s office or other medical setting. Bottom line is that the PLA aligns with the transition to non-invasive, clinically supported diagnostics methods in complex disease areas such as melanoma. On that front, multiple clinical studies have demonstrated the high accuracy and performance of the PLA in detecting melanoma.

A multicenter clinical study conducted in 2018 by Laura et al. evaluated the performance of the pigmented lesion assay in detecting melanoma. The study enrolled 1,000 patients with pigmented lesions and compared the results of the pigmented lesion assay to those of a histopathological examination – the gold standard for melanoma diagnosis. The results of the study showed that the pigmented lesion assay had a sensitivity of 94.4% and a specificity of 96.7% for the detection of melanoma.

Meanwhile, Dinnes & colleagues (2018) compared a meta-analysis of the performance of the pigmented lesion assay to that of visual examination and dermoscopy in detecting melanoma. One study mentioned in the authors’ analysis had enrolled 1,012 patients with pigmented lesions and found that the pigmented lesion assay had a higher sensitivity (87.5%) and specificity (95.7%) for detecting melanoma compared to visual examination (73.3% sensitivity and 79.6% specificity) and dermoscopy (68.8% sensitivity and 87.5% specificity).

From the demonstrated results to date, the data shows the PLA has a >99% negative predicted value (“NPV”) and <1% probability of missing melanoma, at a 91-97% sensitivity level. All of these results were followed up by DMTK in its 2021 TRUST study, where results determined the “longterm repeat-testing study confirmed the NPV of the PLA and found no adverse outcomes related to the test’s routine use.”

In addition, Siegel & co-authors (2022) completed a cost-benefit analysis demonstrating the incorporation of PLA into the visual assessment/histopathology (“VAH”) pathway for assessing melanoma leads to savings for commercial health insurance plans.

The authors used a return on investment model to determine the net savings impact of incorporating PLA into the VAH pathway from a payor perspective. The model was based on claims data from 2019 for patients with lesions suspicious for melanoma (N=239,854) and projected the use of PLA in the VAH pathway over a three-year period. The costs associated with the VAH pathway, including initial visual assessment, surgical procedures, histopathology, and subsequent management, were also analyzed.

The ROI model predicted annual net savings of $0.54 per member per month for commercial health plans with the incorporation of PLA into the VAH pathway. This translates to a total savings of $5.66mm for a plan of 1mm members. The analysis revealed that 95.7% of surgically assessed lesions clinically suspicious for melanoma were diagnosed as benign, with 30.4% of patients with benign lesions undergoing more advanced procedures (e.g., excision) initially or following a biopsy. The melanoma diagnosis rates associated with biopsy only, excision only, and biopsy followed by excision procedures in the VAH pathway were 0.9%, 0.1%, and 17.9%, respectively.

As to how it works, well, just like most advancements in med-tech these past few years, it involves the integration of technology into diagnosis and follows a more convenient route of testing for the patient. DMTK incorporates the PLA into a multi-step tool, consisting of two laboratory tests on a single tissue collection using its tool. Collectively, it calls this the Dermtech Melanoma Test (“DMT”). Whereas the tool, known as the DermTech Smart Sticker, is placed over the suspected lesion, via a see-through ‘label’ that covers the nevi/mole. It’s akin to placing a sticker onto the skin.

The DermTech Smart Sticker

Note: This is not an advertisement for DermTech, or any of its devices. We have no affiliation, and do not own the stock. (Data: DermTech website. )

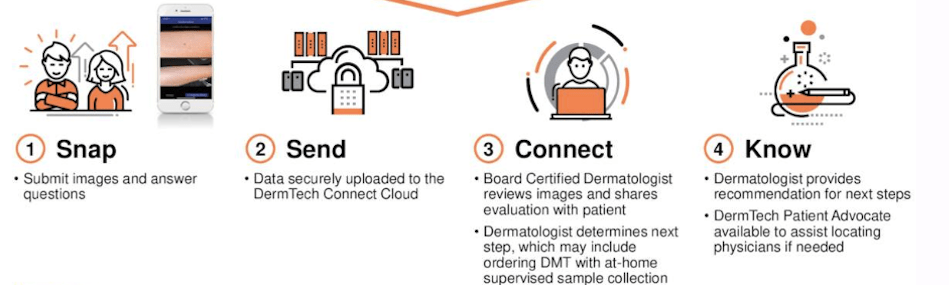

Images are also taken of the lesion, for upload to DMTK’s server through an app. Moreover, when the adhesive is lifted for removal, it collects skin samples of the patient, which are then sent off to DMTK’s gene lab and reviewed by a suite of dermatologists, who examine the image and test, to provide a formal diagnosis. Results are said to be available within 5 business days. You can see the process in the chart below.

Exhibit 2. The DMT flow of steps.

Data: DMTK Q3 FY22 investor presentation, Seeking Alpha.

DMTK early numbers: growth pressured by standard industry forces

It’s worth advising that DMTK isn’t immune to the many hurdles early-stage medtech and biotech companies must endure before successfully commercializing on the grand scale. These were heavily present throughout the company’s last quarter.

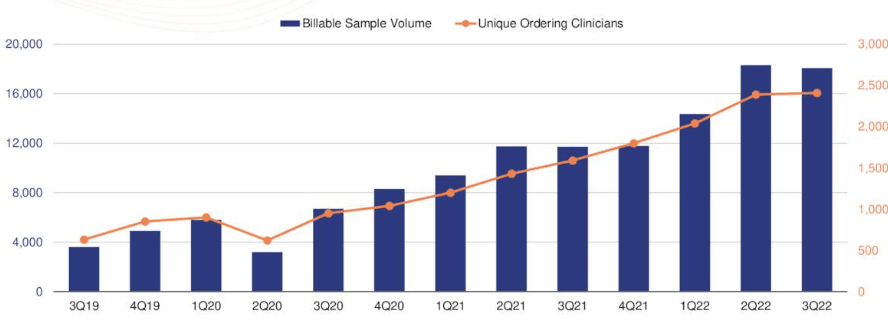

For instance, we’d note that its average selling price (“AS”) of the DMT has remained stagnant, with the exception of prior period adjustments, but has seen a decline when taking those adjustments into consideration. This phenomenon can be attributed to the influence of payers on pricing, per management’s language on the Q3 earnings call. Additionally, the company has encountered some resistance in regards to the expansion of billable samples, as payers have implemented tactics designed to curtail the adoption of the DMT. Sequentially, billable samples growth was flat [Exhibit 3].

We’d advise that these payment pressures are not unique to DMTK and are likely a result of the wider industry’s response to the aftermath of the pandemic.

Exhibit 3. Sequential billable samples growth flat secondary to payor pressures.

Data: DMTK Q3 FY22 investor presentation, Seeking Alpha.

Specifically, some payers have attempted to dissuade customers from utilizing the DMT through the issuance of redirect letters [note, this is common industry practice with accelerated adoption of a new market segment], but the company has effectively countered this through the integration of doctors into the process and advocating for coverage.

To further alleviate these pressures, DMTK is also actively working to expand coverage via its sales-rep footprint. While the tactics implemented by the company to mitigate the efforts of payers are recognized, also recognize that they do require a certain amount of time to take effect. However, we opine this is a good sign when thinking more laterally. We often see within the industry a pushback to adoption momentum when payer’s forecast a new segment will see an accelerated rate of adoption and hence growth. So we believe the resistance from some commercial payers is potentially a net positive.

Switching now to the company’s latest numbers, we saw that assay revenue experienced a 16% YoY increase, totaling $3.4mm, largely due to a 54% YoY surge in billable samples, which reached approximately 18,080. In contrast, contract revenue remained unchanged at $0.1mm during the same period. Looking ahead, we believe that DMTK’s contract research services are expected to continue to demonstrate promise, as we saw the company has signed five contracts in the last six months, following the resurgence of clinical trial activity in the biopharma sector.

Examining the primary drivers of revenue, the ASP per sample was $190 in the third quarter, representing a 25% decrease compared to the previous year and a 16% decrease on a sequential basis. This decrease was partially due to reduced commercial payer payments mentioned, and resulted in a $0.5mm downward adjustment to revenue. Normalizing for these adjustments in both periods, the third quarter’s ASP would have been $217, remaining flat in comparison to the previous quarter.

In terms of unique ordering clinicians, DMTK saw approximately 2,410 in the third quarter, a 1% increase from the 2,390 seen in the second quarter. Over the last 12 months, the company has served approximately 3,910 unique ordering clinicians and has currently penetrated 43% of its target market of 9,000 dermatology clinicians. These are reasonable growth percentages to go by in our estimation and point to the market’s uptake, hence the likely reason behind many commercial payers resistance mentioned earlier.

Moving to Medicare samples, we saw they accounted for ~24% of the company’s billable samples in the third quarter, otherwise unchanged from the previous quarter, but slightly higher than the 22% seen in the previous year. It is worth noting that Medicare represents half of all melanoma biopsies performed each year, and DMTK says it will strive for increase penetration in this market segment.

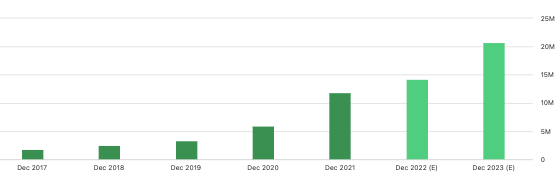

In terms of guidance, management forecast $13mm at the top line in FY22, and this represents sizeable growth on prior annuals. You can see DMTK’s consensus revenue estimates in the image below, noting that FY23′ looks to be a big year for the company.

Exhibit 4. DMTK consensus revenue estimates, FY22–23′, reasonable ramp with FY23 looking to be key inflection point.

Data: Seeking Alpha, DMTK, see: “Earnings Estimates”

In short

As DMTK continues to evolve its market strategy in successfully commercializing its DMT segment we remain constructive on the name. Based on underlying market fundamentals and the differentiated offering of the DMT/PLA in detecting melanoma, if successful, there is potential for the company to create a breakthrough in this diagnostics market. Whilst it’s still very early days, with further adoption and reuptake of its assays, there is reason to keep on top of DMTK’s growth route. For now we rate the stock as a hold, noting the many risks involved with small-cap equities, but I hope that investors were able to gain an understanding of the opportunity downstream from this report nonetheless.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment