Justin Sullivan

Thesis

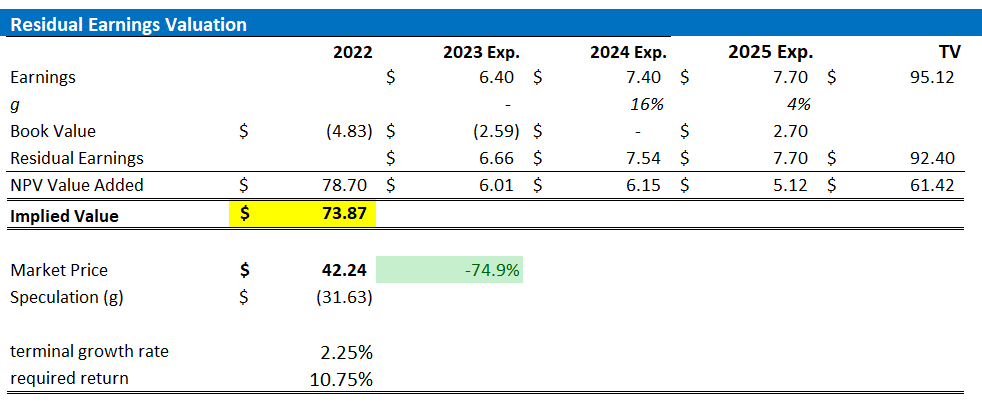

I have previously argued that Dell Technologies (NYSE:DELL) is ‘Buy’. And today I am confident to reiterate the bullish thesis. With focus on innovation and customer satisfaction, Dell Technologies remains, in my opinion, well-positioned to capture attractive financial opportunities, despite the difficult demand environment. Moreover, a stronger focus on OPEX discipline, paired with a recovering demand for PCs, will likely defend an operating profit of between $4 and 4.5 billion for 2023 — which would result in an attractive EV/EBIT of between x11 and x13. Personally, I value Dell stock with a residual earnings model and calculate a fair implied share price of $73.87. ‘Buy’.

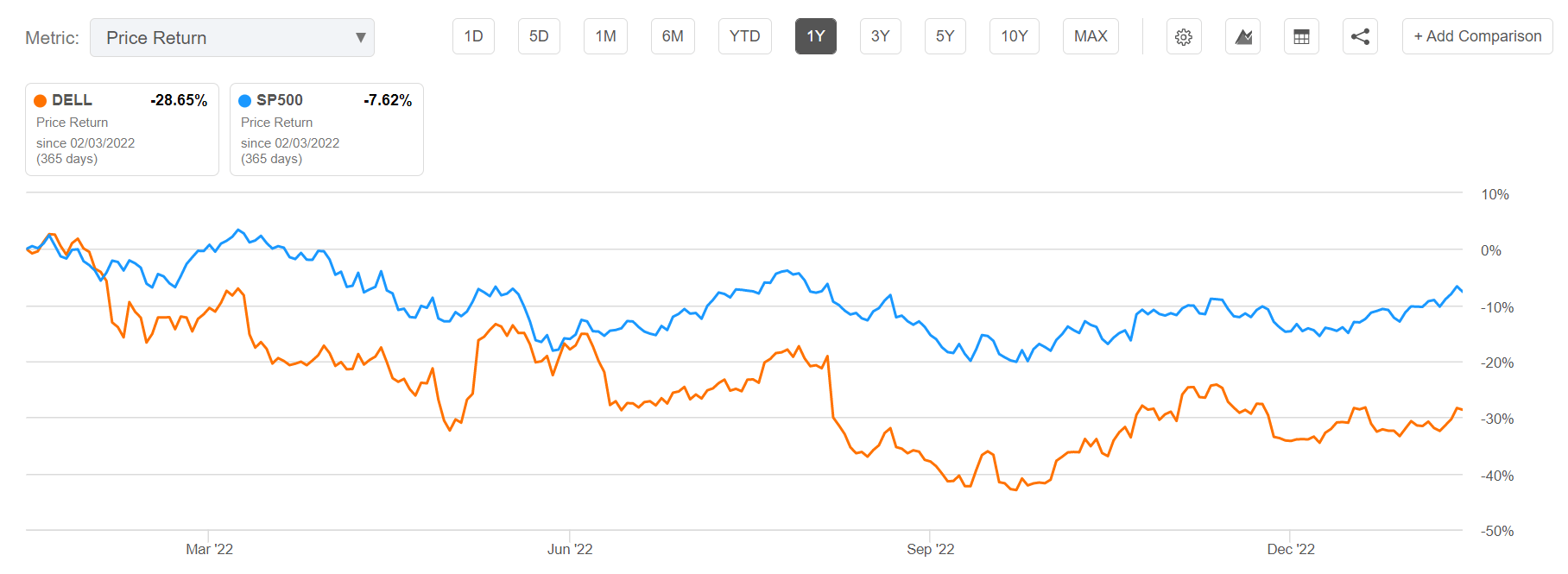

For reference, Dell stock is down approximately 29% for the past twelve months, as compared to a loss of about 8% for the S&P 500 (SPY).

Seeking Alpha

Financials Support Bullish Thesis

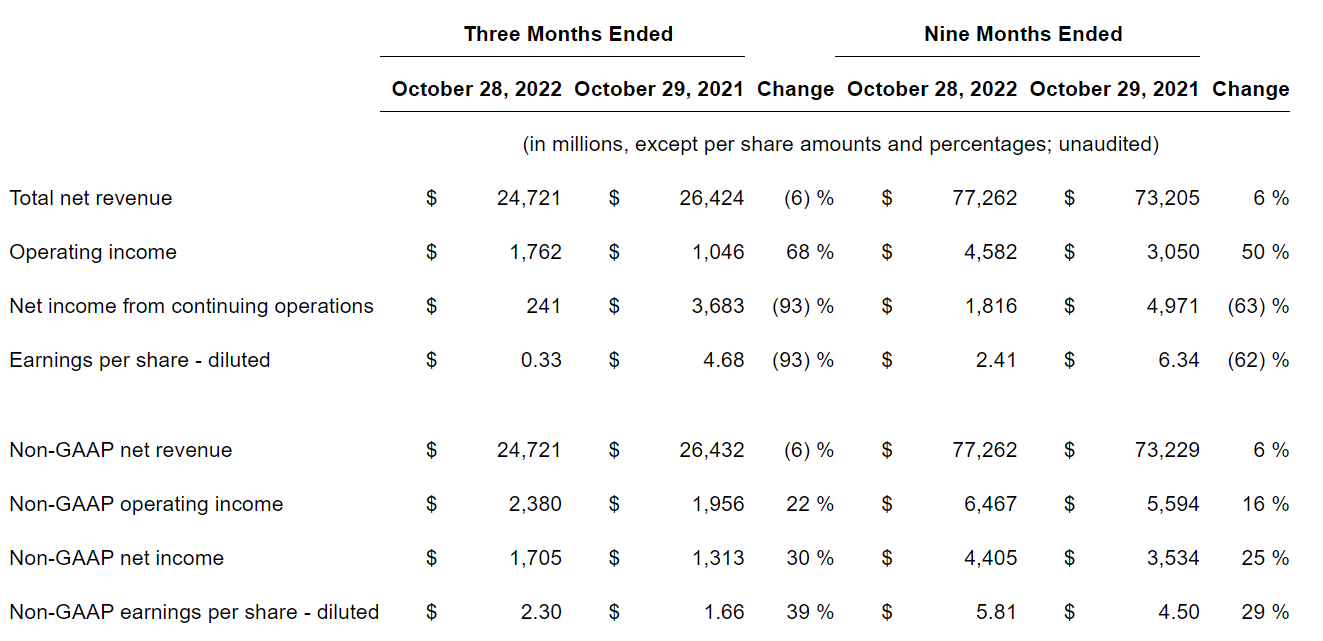

Dell has not yet reported earnings for the December quarter 2022. But the latest results, from the period of July to end of September, support bullish confidence. During Q3 2022, Dell generated total revenues of $24.7 billion. Although topline was down by approximately 6% as compared to the same period in 2021, the company beat analyst consensus estimates by more than $100 million ($24.59 billion estimated). The company’s ISG segment reported $9.6 billion in revenue, up 12% YoY, while CSG was $13.8 billion, down 17%. Recurring revenue for the quarter was around $5.4 billion, a yearly increase of 11%.

With regards to profitability, Dell reported super strong results–in fact, record results. During Q3 2022, Dell managed to accumulate $2.4 billion of operating income, and adjusted earnings per share equal to $2.30 (beating consensus by $0.69), up 39% year over year.

Dell Q3 2022 results

Dell ended the third quarter of 2023 with $39 billion in remaining performance obligations and $27.1 billion in deferred revenue. The company had $6.5 billion in cash and investments and returned $847 million to shareholders through a combination of buybacks and dividends. Notably, on an annualized basis, Dell’s equity return continues to anchor close to 12% (referencing a $30 billion market capitalization).

On the backdrop of a difficult demand environment, Dell continued to gain commercial PC unit share in Q3 and the company voiced confidence to extend its industry-leading share in servers and storage. With that frame of reference, the company’s innovation agenda remains intact with a target of 30 new infrastructure launches and the availability of PowerFlex on AWS.

Profitability Expansion On OPEX Discipline

While the demand for PC sales is expected to start recovering in late 2023, Dell is focused on expanding profitability through OPEX discipline. Since Q1 2022, Dell has already executed notable cost-cutting measures and managed to reduce operating expenses by approximately $300 million.

Dell is reportedly planning to lay off around 6,650 employees, or 5% of its global workforce, due to declining demand for personal computers (PCS). The company generates about 55% of its revenue from PCs, and recent data from industry analyst IDC showed that Dell saw the largest decline in PC shipments, with a 37% drop in the fourth quarter of 2022 compared to the same period in 2021. The job cuts follow cost-cutting measures, including a hiring pause and limits on travel, which the company deemed no longer enough to drive efficiency. After the reduction, Dell will have its lowest headcount in at least six years, with about 39,000 fewer employees than in January 2020.

Although management will likely provide further details on the financial impact of the job cuts when it reports its fiscal fourth-quarter results, analysts can approximately do the math: Assuming that the average annual cost per employee for Dell is somewhere between $85.000 and $95,000, including benefits and overheat expenses, then cost-savings would likely total $565 million – $630 million annually. Further assuming a structural P/E of about x10, an analyst may reasonable estimate that the layoffs may add a reasonable $5 billion of shareholder equity (about 16% value accreditive as compared to the company’s current market capitalization).

Personally, I calculate that Dell’s cost cutting measures will likely defend an operating profitability margin of above 5% in 2023 (likely range of 5% – 5.5%). And anchoring on a an estimated $91.5 billion of revenues, I model operating profits of between $4.05 an $4.45 billion.

Valuation: Set TP At $73.87 Per Share

To estimate a company’s fair implied valuation, I am a great fan of applying the residual earnings model, which anchors on the idea that a valuation should equal a business’ discounted future earnings after a capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

With regard to my Dell stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal ’till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor Dell’s cost of equity at 10.75%.

- For the terminal growth rate after 2025, I apply 2.25%, which is approximately in line with estimated long-term nominal GDP growth and thus neither optimistic nor pessimistic.

Given these assumptions, I calculate a base-case target price for Dell of about $73.87/share, which implies that Dell could be undervalued by as much as 75%.

Analyst Consensus EPS; Author’s Calculation

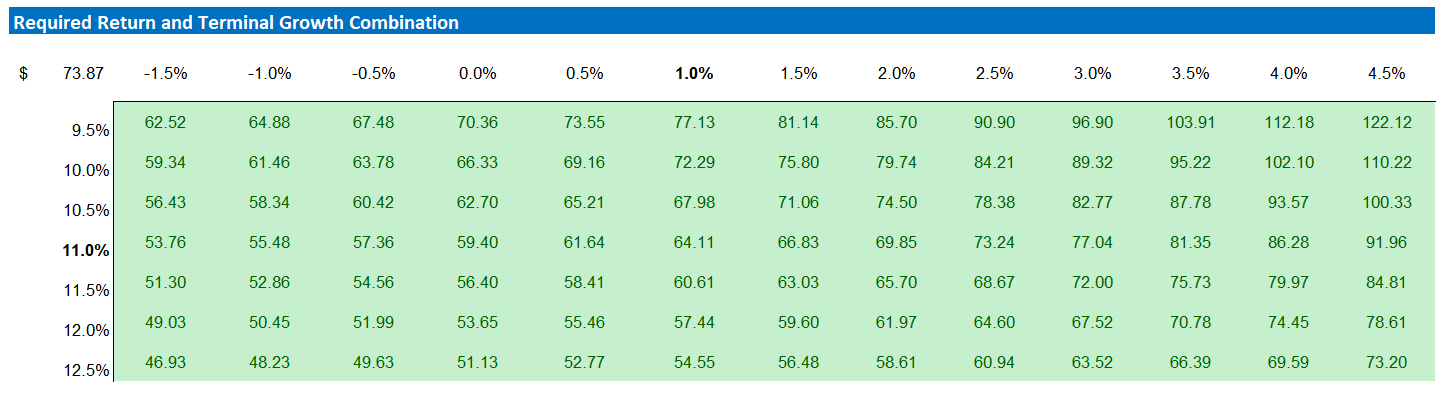

My base case target price does not calculate a lot of upside. But investors should also consider the risk-reward profile. To test various assumptions of Dell’s cost of equity and terminal growth rate, I have constructed a sensitivity table. Note that the matrix looks very favorable from a risk/reward perspective.

Analyst Consensus Estimates; Author’s Calculations

Reiterate Risks To My Thesis

As I see it, there has been no major risk updated since I have last covered Dell stock. Thus, I would like to highlight what I have written before:

In my opinion, the major risk associated with an investment in Dell is a continued and prolonged slowdown in IT hardware spending and PC sales. Such a scenario is not unlikely, given that the global economy is pressured by multiple simultaneous headwinds, including low economic growth, high inflation, rising interest rates, financial markets distress and geopolitical tensions.

Moreover, even if the slowdown for IT spending is less severe than feared, Dell stock might nevertheless fail to deliver near-term price appreciation, given that market sentiment could remain depressed well into 2023 (personal opinion).

Conclusion

I reiterate my bullish stance on Dell Technologies and continue to believe it is a “Buy”, despite the challenging demand environment. With a stronger focus on cost management and a recovering demand for PCs, Dell is, in my opinion, expected to see an operating profit of between $4 and $4.5 billion in 2023, which would result in a favorable EV/EBIT ratio of between x11 and x13 (in a structural downturn!). I personally value Dell’s stock using a residual earnings model and estimate a fair share price of $73.87.

Be the first to comment