Wirestock/iStock Editorial via Getty Images

The rebound we’ve seen on Wall Street since last October has taken many stocks with it. However, there are names that preceded this bull market by several months, and have already posted massive gains. One such name is Deere (NYSE:DE), and while it’s been great if you’ve owned it since July, I’m afraid the party may be up from the long side.

Deere’s fundamental picture looks okay for now as far as I can tell, but the chart is showing some major signs of a huge, longer-term top. For that reason, I’m recommending that if you own the stock, you consider selling. If you are more enterprising, maybe you could even consider shorting it below the consolidation zone, but I’m not suggesting you short it.

Let’s dig in.

Signs of a major top

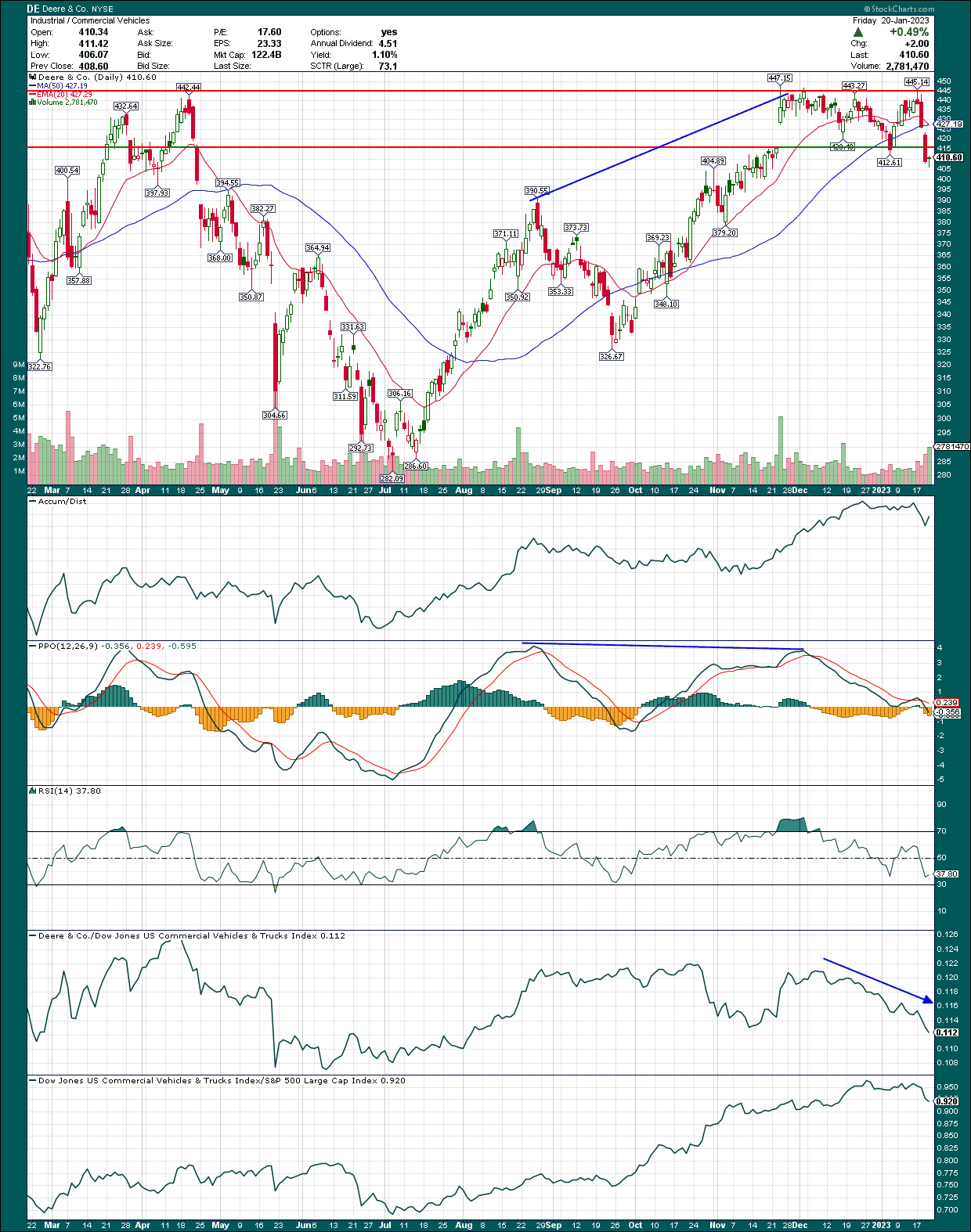

Deere put in a multi-month, enormous advance that saw the stock move nearly 60% higher in the space of several months. That’s impressive, but I see several things that should worry the bulls over the coming months.

StockCharts

First, the 20-day exponential moving average is making a bearish cross of the 50-day simple moving average. The last time that happened at an intermediate top, which was last spring, the stock fell from $442 to $282 in a straight line. Too early to tell if we’re getting something like that this time, but I certainly wouldn’t rule it out.

Next, the PPO put in a negative divergence as the stock made its new highs late last year. Basically, a negative divergence occurs when a momentum indicator fails to make a new high while price is making a new high. That often signals slowing bullish momentum, and therefore, a potential top. I believe that’s what we have here.

Third, Deere has been underperforming its peer group since December, which is especially worrying because the group has been pretty good. That just means money is rotating out of Deere and into other stocks in the group. Again, not a good sign.

Lastly, the very worst part of the chart is the fact that price has broken down out of the consolidation channel drawn above, at a time when all of those other things are occurring. The confluence of these events is very bearish, in my view, and I wouldn’t even think of buying/holding this stock right now.

The thing is that the fundamental picture doesn’t look bad. In fact, we’re seeing upward revisions and strong commentary from management. However, it’s clear to me that Wall Street sees something they don’t like, and they’re voting with their money and going somewhere else.

Fundamentals look okay

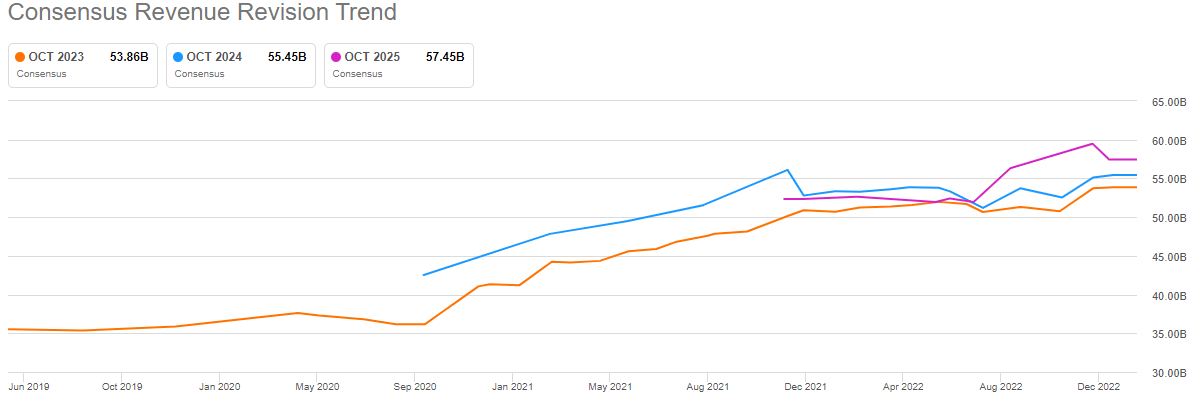

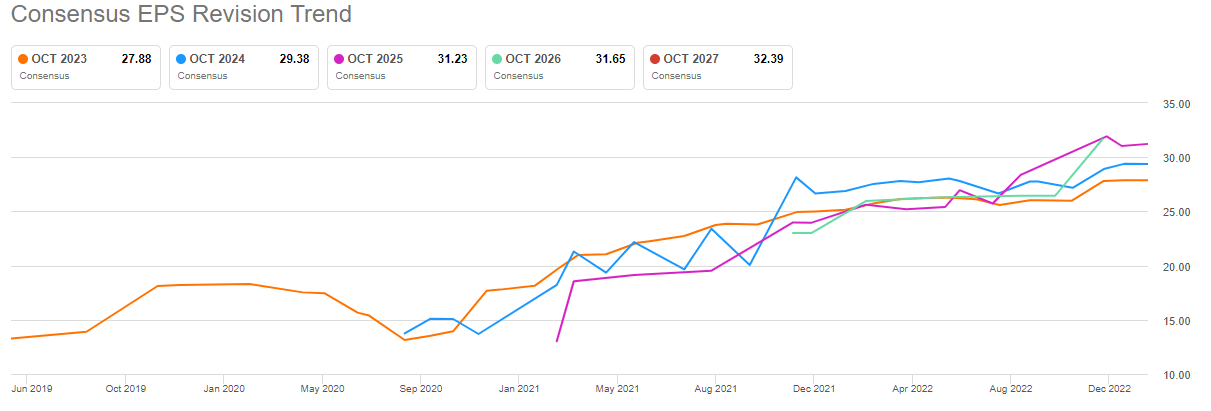

Let’s start with a look at revenue revisions, which gives us a good look a top line expectations from the analyst community. The picture here looks great, other than year-over-year growth is leaving a bit to be desired. However, we’re going up and to the right, and that’s all you can ask for.

Seeking Alpha

Estimates are way up from the COVID panic months in 2020, with estimates for fiscal 2023 up more than half since 2020. That’s outstanding, but the flip side of this is that there is a lot of good news priced in already. Is that what Wall Street is worried about? Perhaps, but we won’t know until fiscal 2023 results come in. After an advance like this, it surely wouldn’t be shocking to see some moderation of revenue estimates.

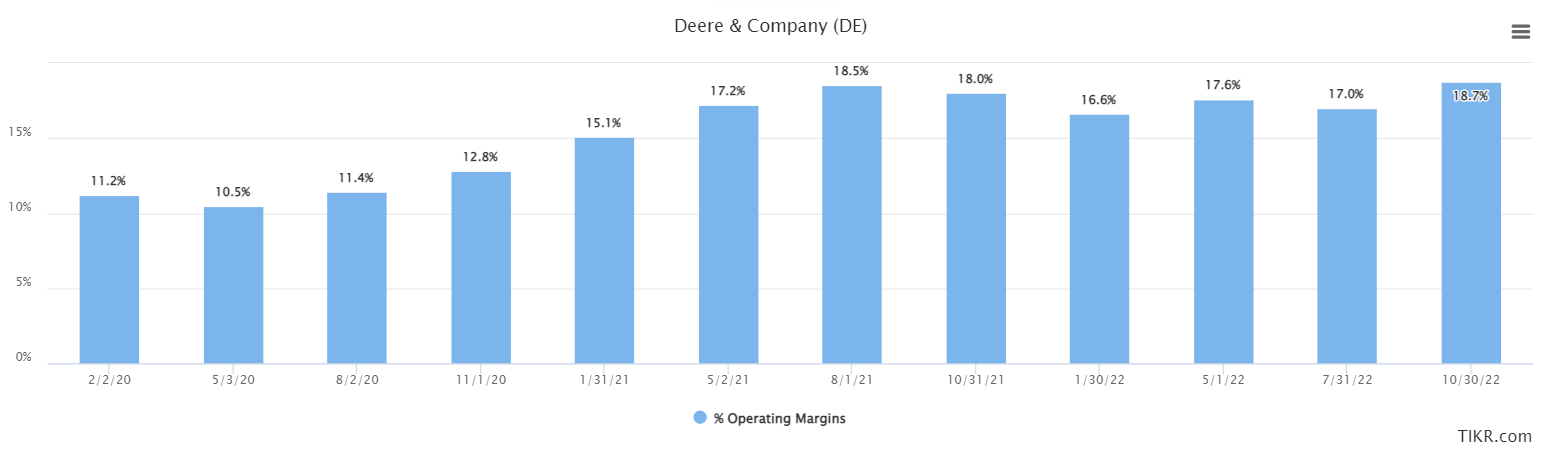

Second, the company is already producing all-time high operating margins. Again, while that’s great, one wonders how much there is left in the tank. Below we have trailing-twelve-months operating margin performance for the past few years.

TIKR

Deere has been focused for years on reducing costs and its SVA metric (shareholder value added), and we can see the fruits of those labors here. However, I’ll note that revenue performance has been overwhelmingly dominated in recent quarters by supply chain inflation-fueled price hikes, and I have a hard time believing that sort of thing is sustainable. If we get a recession, all bets are off with Deere and other highly cyclical names, so again, this is another possible reason institutions may shy away from the stock. Keep in mind that massive price increases help margins, too, so I would not be surprised to see a top in profitability with the Q1 report in a few weeks.

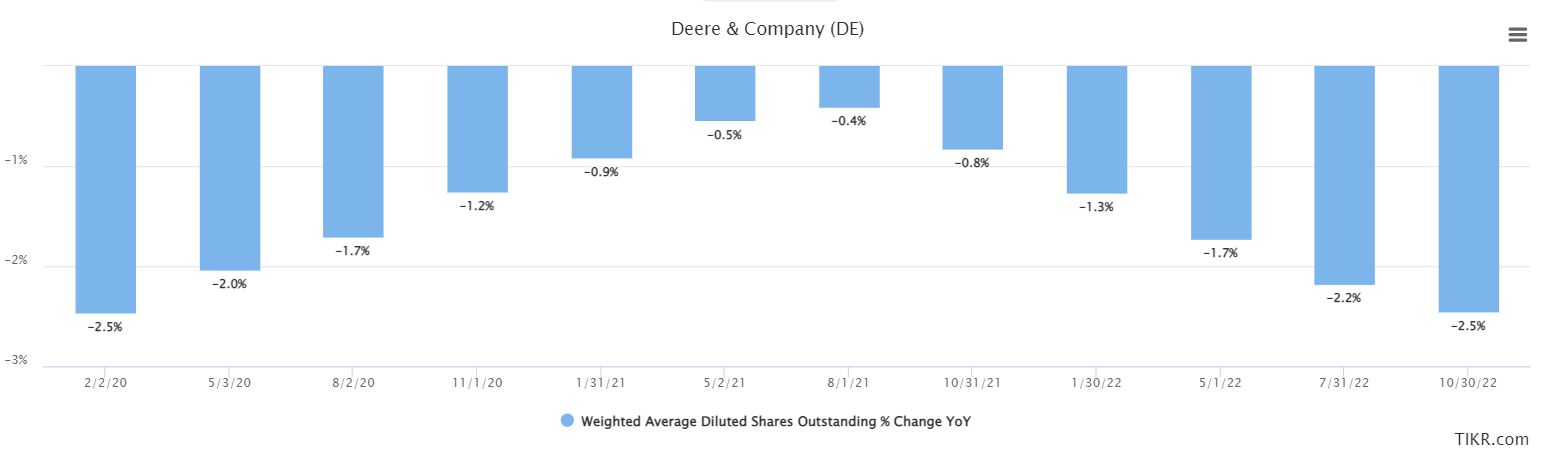

Analysts are forecasting 12% growth in revenue this year, followed by ~3% in 2024 and 2025, respectively. I happen to think we’re going to see margins top – and potentially start to fall – in 2023, so that leaves just the share count to make up the remainder of EPS growth. Below we have the change in the number of shares outstanding on a trailing-twelve-months basis for the past couple of years.

TIKR

We can see that Deere is at an annual run rate of 2%+ in share reductions, which is a direct tailwind to EPS. So, if we assume 3% revenue growth for 2024, and a 2% tailwind from the buyback, the final wildcard is margins. At the very least, I think upside from here on margins is quite limited. After all, recent gains have been generated in no small part due to COVID supply chain issues that still linger. Customers will not accept massive pricing increases forever, so I wonder what – if any – levers Deere might have for margin growth.

Perhaps that’s why analysts expect only 5% to 6% growth in EPS in the coming years, which is underwhelming to say the least.

Seeking Alpha

This chart is beautiful, but again, I think the odds that this move has run its course are high. Consider also that if we do get a recession, there is likely very strong downside potential to these numbers, whereas the upside is almost certainly quite limited.

Thus, you have to ask yourself if the risk of holding and hoping for a bit of additional upside is worth the risk there could be quite sizable downside in estimates. Given the way the price chart looks for the stock, it is my belief institutions have weighed this, and come to the conclusion it is in fact not worth it.

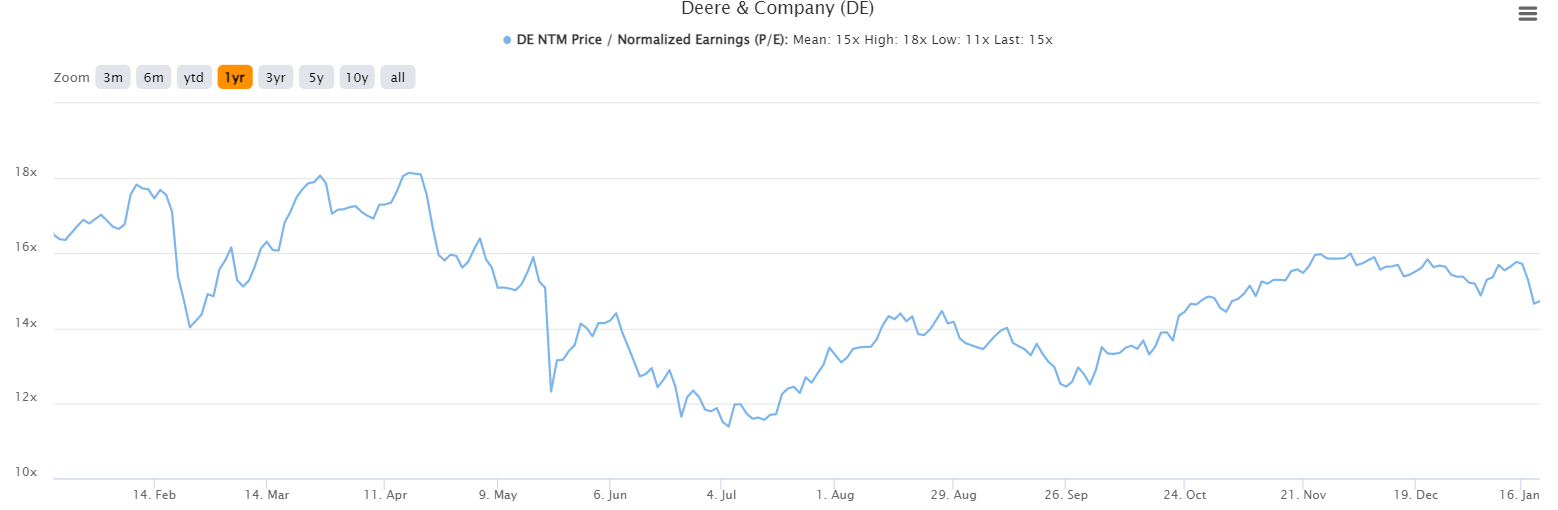

On a forward P/E basis, the stock looks pretty good. Here’s a one-year chart to start the valuation conversation.

TIKR

The problem, again, is that if the “E” portion of the P/E starts to fall – which I believe has a high possibility of occurring – the “P” portion of the ratio is likely to fall as well.

The point is that with the lateness of the cycle, and the fact that there is a lot of rosiness priced into estimates right now, I’m thinking the risk of holding this stock is far too high for the potential reward. The stock has broken down below what I believe is key price support (or was), and therefore, I think this one is going a lot lower.

I’m not suggesting you short it, but I am suggesting that if you own it, you take a long, hard look at whether that’s still a good idea or not. I don’t think it is.

Be the first to comment