Anastad/iStock via Getty Images

With the market returning to high volatility, it’s time for long term-oriented investors to get their shopping lists out. A lot of high-growth tech stocks are still underwater after this year’s deep bear market correction, and a handful of iconic names are now trading far below their pandemic highs.

Datadog (NASDAQ:DDOG) is one stock that bears close watching. I have long considered Datadog one of the premier, highest-performing stocks in the software sector. Its rise from a relatively unknown startup to the dominant vendor in infrastructure monitoring, completely knocking aside incumbent player New Relic (NEWR), has been almost unheard of. In sympathy with other SaaS peers, Datadog has shed 40% of its market value year to date, though its fundamental performance has remained at sky-high levels.

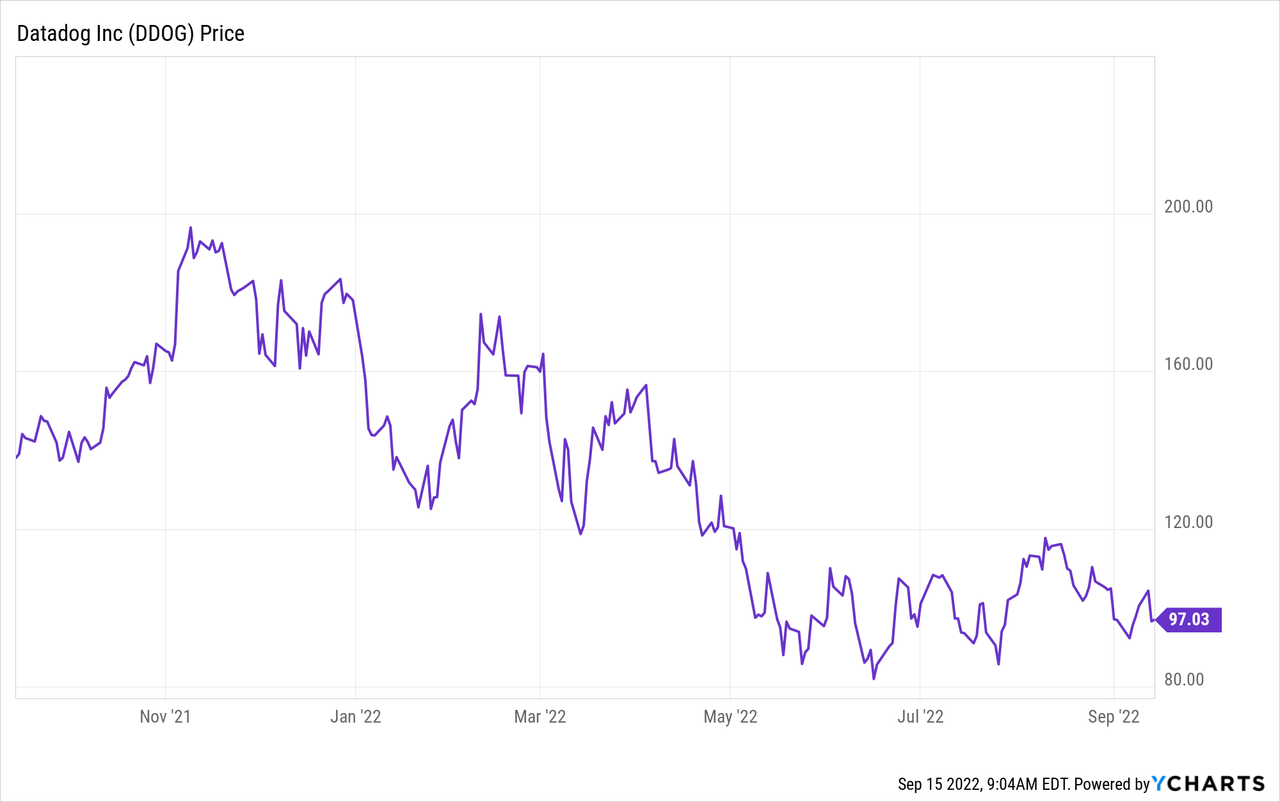

I’m retaining my neutral, watch-and-wait stance on Datadog: though in my view, the stock is nearing closer and closer to a buy point. I’m enticed by the prospect of buying into this high-quality stock at a price that is currently ~50% below pandemic-era highs near $200, but I think from a valuation perspective (especially with fears of an upcoming 100bps Fed rate rise) Datadog has a little bit more to give before it rebounds.

As a reminder of all the fantastic fundamental qualities that Datadog possesses:

- Incredible execution and growth at scale. There are very few companies that can reach a nearly $2 billion annual revenue run rate and still be growing at >70% y/y. This is a testament both to the largesse of Datadog’s infrastructure monitoring market (a crown it stole from incumbent New Relic in a rapid amount of time) as well as the company’s own sales execution.

- Huge $53 billion market opportunity. Datadog recently sized the observability market as a $53 billion total opportunity by 2025, which means that Datadog is still only single-digit penetrated into this overall market opportunity.

- Mission critical, recurring revenue software. Once installed, Datadog becomes a fixture of a company’s IT stack, necessary to maintain performance and security. This gives Datadog a rich, reliable stream of recurring revenue to build on. Its expansion rates and number of customers using multiple products is also quite high.

- Already profitable. Very few companies growing as quickly as Datadog are able to achieve meaningful profitability. Datadog has 20%+ pro forma operating margins. On top of 70%+ revenue growth, this puts Datadog into a stratospheric “Rule of 100” club, whereas most software companies struggle to even meet the “Rule of 40”.

These strengths, of course, come at a price: even after Datadog’s generous fall to date. At current share prices near $97, Datadog trades at a market cap of $30.71 billion. After we net off the $1.70 billion of cash and $737.2 million of debt on Datadog’s most recent balance sheet, the company’s resulting enterprise value is $29.74 billion.

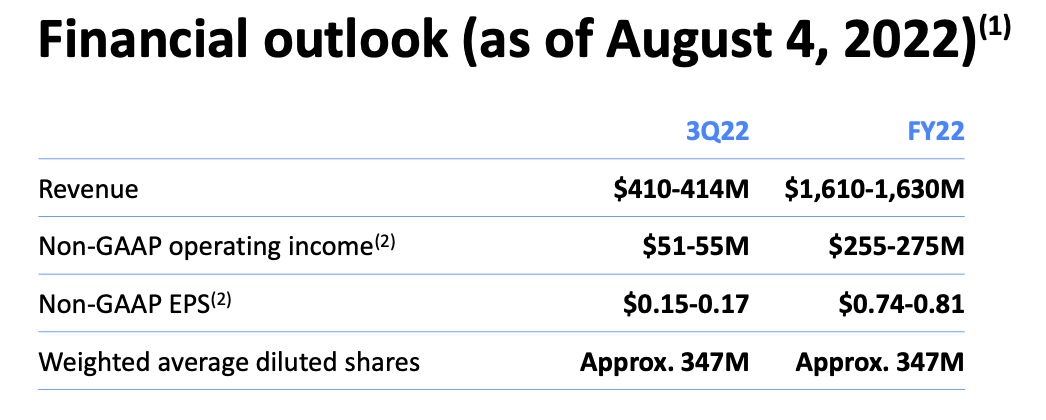

Meanwhile, for the current fiscal year, Datadog has guided to $1.61-1.63 billion in revenue, representing 56-58% y/y growth (representing a slight one-point increase versus a prior outlook of 55-57% y/y growth):

Datadog outlook (Datadog Q2 earnings deck)

Looking ahead to FY23, Wall Street consensus puts Datadog’s revenue at $2.24 billion, representing 39% y/y growth (data from Yahoo Finance). This puts Datadog’s valuation multiples at:

- 18.3x EV/FY22 revenue

- 13.2x EV/FY23 revenue

To me, I’m more comfortable buying Datadog at an 11x FY23 revenue multiple, implying a price target of $81 – a level the stock briefly touched in June and quickly rebounded from, and a price I think we’ll see again as more volatility hits the market in the last quarter of the year.

The bottom line here: keep Datadog firmly on your watch list, but be patient and hold out for a better price. In the low $80s, Datadog is a firm steal.

Q2 download

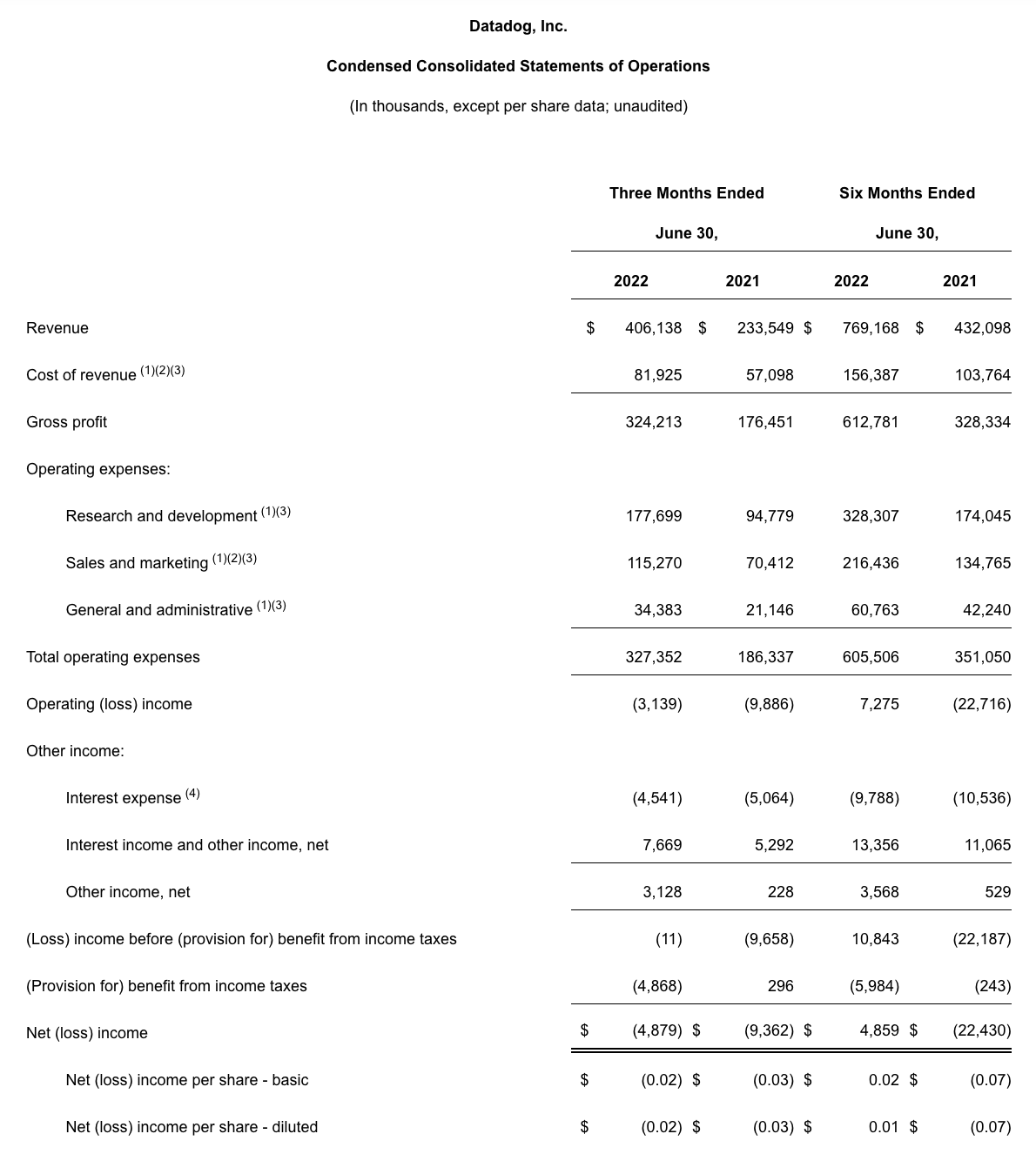

Let’s now cover Datadog’s latest Q2 results in greater detail. The Q2 earnings summary is shown below:

Datadog Q2 results (Datadog Q2 earnings release)

Datadog’s revenue in Q2 grew 73% y/y to $406.1 million, beating Wall Street’s expectations of $381.2 million (+63% y/y) by a huge two-point margin. Growth did decelerate, however, from 83% y/y growth in Q1 – though investors must acknowledge that Datadog cannot expect to continue growing at its hyper-growth pace forever.

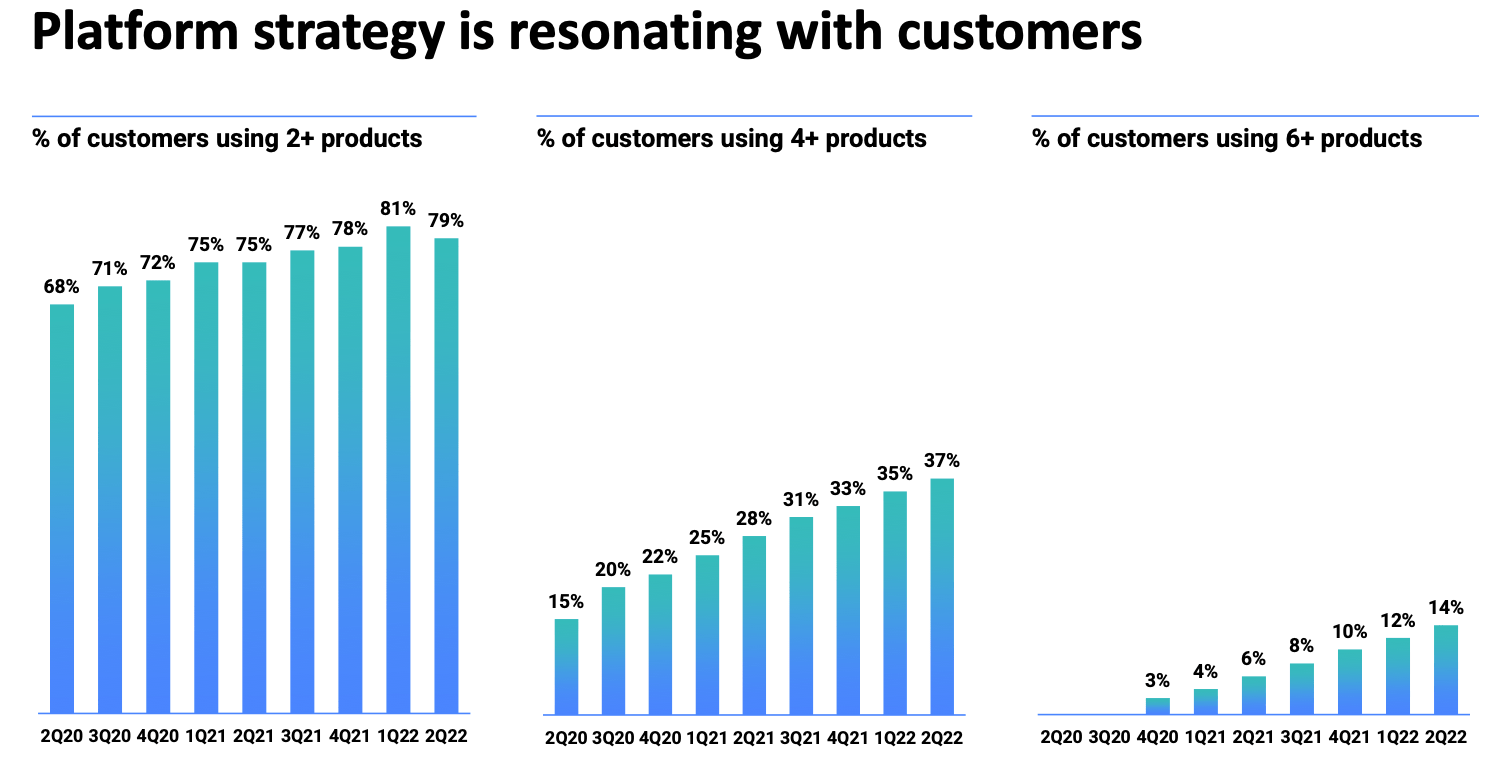

Still, there are a lot of strong metrics to call out. In particular is the number of customers that Datadog is managing to cross-sell into other products on its platform. Sequentially, the percentage of customers using 4+ Datadog products grew two points sequentially to 37%, while the number using 6+ products grew two points as well to 14%:

Datadog multi-product customers (Datadog Q2 earnings deck)

Year to date so far, the company has already added 2.4k net-new customers (putting it on track to outpace last year’s 4.6k total adds for the full year). Datadog has also continued to notch a >130% net revenue retention rate, indicating very strong upsell activity.

Management commented that while Datadog remains broadly shielded from current macroeconomic conditions, it did notice a slight slowdown in spend from its enterprise customers. Per CEO Olivier Pomel’s remarks on the Q2 earnings call:

In Q2, while we overall saw strong customer growth dynamics, we have seen some variability in growth among our customers. We saw our larger spending customers continue to grow but at a rate that was lower than historical levels. This effect was more pronounced in certain industries, particularly in consumer discretionary, which includes e-commerce and food and delivery customers and affected more specifically our products with a strong volume based component such as log management and APM suite. Note that we did not see this with our SMB and lower spending customers who continued growing with us as they have in the past.

While these near growth data points and the current micro climate are leading us to be prudent with our short term outlook, we remain very bullish about our opportunities and confident in our execution as we continue to see positive trends underpinning our business.”

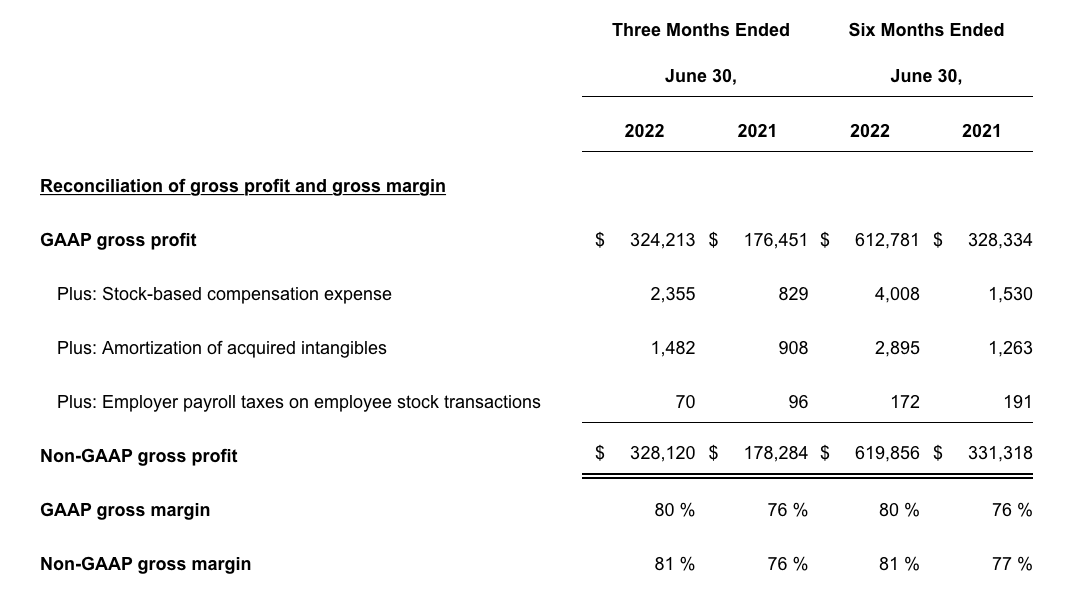

Moving down the P&L, one positive highlight is that Datadog managed to boost its pro forma gross margins from 76% last year by five points to 81%:

Datadog Q2 gross margins (Datadog Q2 earnings release)

This five-point boost was driven primarily by greater economies of scale on cloud costs. In turn, this helped Datadog increase its pro forma gross margins by eight points to 21%.

We’ll step back and recognize that with 73% revenue growth and 21% pro forma operating margins, Datadog’s “Rule of 40” score is 94: an incredible feat considering most software companies even fail to hit the basic rule of 40.

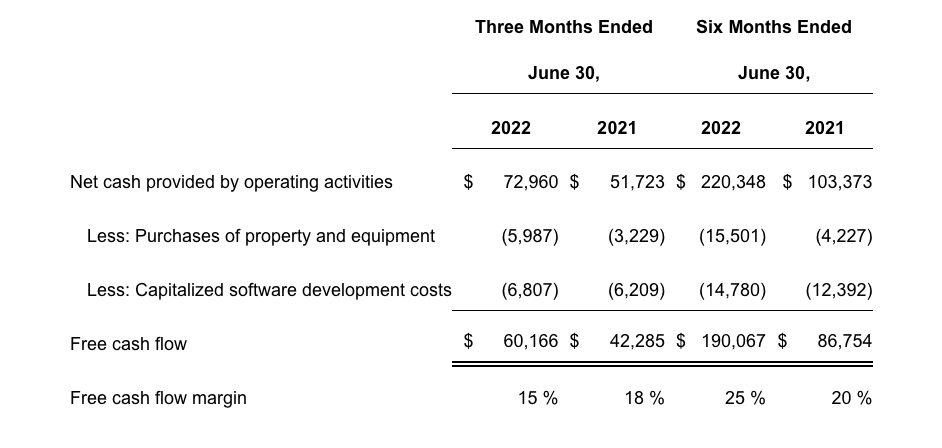

YTD free cash flow also more than doubled to $190.1 million, representing a 25% FCF margin; five points richer than in the year-ago quarter.

Datadog operating margins (Datadog Q2 earnings release)

Key takeaways

There’s certainly a lot to like about Datadog: blazing growth rates, built-in cross-sell and expansion momentum, a wide-open >$50 billion market opportunity, and established profitability. Wait until stock prices come down to the low $80s before making a move here.

Be the first to comment