skynesher

Investment Summary

After a brutal selloff across the bulk of 2022, it’s time for another fair appraisal of Cryoport, Inc (NASDAQ:CYRX). CYRX leverages its proprietary technology to facilitate security and cross-border compliance by providing transparency at all points along the shipment pipeline. As such, it enables those in the life sciences domain to monitor their biologic commodities and in-market biologic assets during shipment, an integral combination for end-market delivery, and for those completing clinical trials.

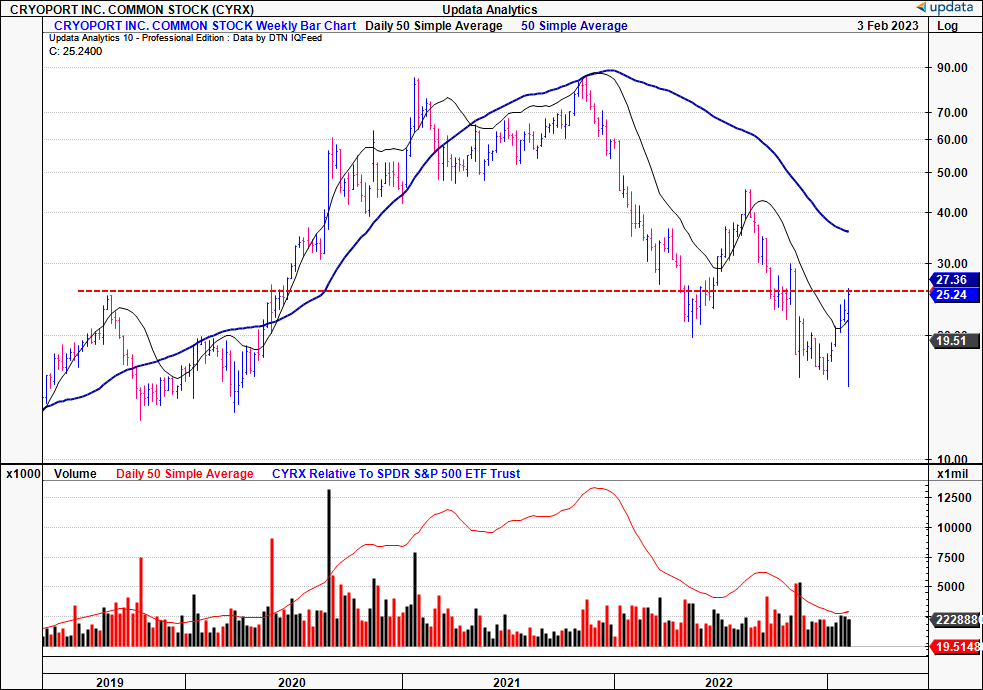

We believe CYRX sits at the tip of the spear in thermoregulatory logistics at all points along the biologics supply chain. Over the last 2-years, the topic of ensuring supply chain certainty has been magnified, hence, CYRX presents as an attractive value proposition in this regard. The problem is the market hasn’t agreed with this proposition since the end of FY21. Prior to this, we saw the stock run from $16 in December FY19 to an all-time closing high of $83 by November FY21, before reversing sharply to its current market cap [Exhibit 1].

Exhibit 1. CYRX price evolution since FY19′, now back at 2019 range

Note: Weekly bars, log scale (Data: Updata)

There are several explanations for this selloff, however. First and most obvious, the broad market repricing witnessed in late FY21 to the end of last year. Second, in November of that year, CYRX launched a two equity offerings back-to-back, the first a direct placement at $81.10/share, followed by a $350mm convertible note issue, due 2026. Note holders can convert at $117 per share or accrue 75bps interest [semi-annual] until maturity.

Convertibles can be a win-win for both company and investors. Companies receive a ‘cheap’ form of debt financing, with the ability to wipe the debt from the balance sheet if it is converted. Investors achieve a cheap form of equity, with downside cover should the stock fail to run to the conversion price. One identifiable tension point with the convertibles issue is that CYRX used a mix of convertible preferred and common equity ($250mm of preferred at 4%, and $25mm, respectively) to finance its MVE Biological Solutions transaction in FY20. Hence, it’s likely investors were unsatisfied with the structuring of all three deals. Alas, following both issues in FY21, investors immediately exited CYRX, creating a near lethal recipe for its market value and a descent into chaos for its share price.

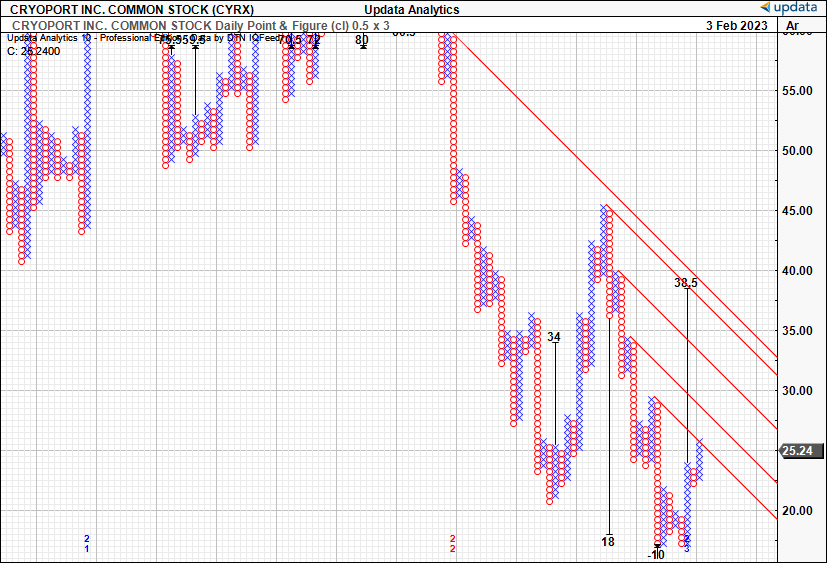

Nevertheless, we remain very constructive on the long-term outlook for CYRX. Undoubtedly, this is a name that needs to be managed actively as a part of a broader equity risk in portfolio construction. The question we sought to answer was whether the selloff has finished in its duration, and, if this now presents an option to buy the stock. Heading into its FY22 full-year earnings later this month, this is a relevant discussion to be had. Net-net, we rate CYRX a buy, seeking upside targets to $38.5.

Note: The key risks to this investment thesis are largely centred around the company’s upcoming FY22 earnings. Should it report a weak set of numbers at this point, there’s a high chance investors could continue selling off CYRX shares, adding more downside pressure. Should the broad market also turn south, there’s additional selling pressures that must be considered by investors. These are the main identifiable risks that investors must consider before continuing any further.

CYRX core business advantages

As mentioned earlier, CYRX is a leader in thermoregulatory logistics. There’s multiple data points to evidence this, however we point investors to the company’s client base to signify its importance in transporting biologic commodities. By Q3 last year, it was supporting 643 clinical trials and 9 commercial therapies, and has been assigned major shipment tasks from several large pharmaceutical players. The major standouts in its client base include:

- Kymriah by Novartis

- Yescarta, and Tecartus by Gilead [via Kite]

- Breyanzi, and Abecma by Bristol-Myers Squibb.

As a reminder, Yescarta recently received FDA approval as a second line treatment for relapsed/refractory large B-cell lymphoma (“R/RLBL”) whereas Breyanzi received EU approval for the third line treatment of R/RLBL.

CYRX’s logistics platform is quite sophisticated and is the keystone to its differentiated offering along the life sciences value chain. The platform is engineered to streamline global distribution of biologic and cell-based commodities and assets, typically regulated by the FDA and other international regulatory entities. In fact, CYRX’s offerings are essential in ensuring cross-border compliance and quality assurance for ‘ingredients’ required during crucial stages of pre-clinical trials. Mostly, the coverage of biologic assets includes candidates ready for investigational new drug applications (“IND”) status, those applying for biologics license applications (“BLAs”), and new drug applications (“NDA”), along with global clinical trials in other countries where strict regulatory compliance is mandatory.

As a result, a substantial portion of the company’s revenues are based on long-term offtake agreements, like those listed above. The business model involves the following segments:

1). The provision of Cryoport Express shippers (“CREs”) to customers through long-term master service agreements (“MSAs”) in exchange for a fee. These MSAs cover a specified duration, and include a predefined shipping cycle, during which the customer has the use of the shippers. Upon completion of the shipping cycle, they are returned to the company, which retains the title.

2). Revenue is recognized when the shipper is delivered to the end-user requiring the enclosed materials. The company also provides vacuum insulated aluminium dewars and cryogenic freezer systems, where revenue is recognized upon satisfaction of delivery.

3). In addition, CYRX offers a global temperature-controlled logistics service. This is a nice – but quintessential service – as mentioned earlier. Here, revenue is recognized as each service is rendered. The bulk of this serves includes integrated temperature-controlled biostorage solutions. Each one of the above is also offered to customers under long-term MSAs. These encompass a wide spectrum of services, namely:

- Biological specimen cryopreservation storage and maintenance

- Archiving

- Monitoring and tracking

- Receipt and delivery of samples

- Transport of frozen biological specimens, and

- Management of incoming and outgoing biological specimens.

4). One of the key differentiators that piques our interest is its cloud-based logistics management platforms. These are reported under the Cryoportal Logistics Management Platform, and the CRYOPDP Unity platform. Key to the offering, is that both services are managed from an integrated control tower.

Collectively, the systems are known as the “Cryoportal”, and the segment integrates with CYRX’s wider offering. To illustrate, the Cryoportal provides a fully documented history of all CREs, including the Elite shippers, including, chain of custody, chain of condition and chain of identity services. For its customers who need shipment of the various biologic commodities,, this ensures that all stability and compliance measures are maintained throughout the supply chain.

Upcoming catalysts

CYRX’s upcoming full-year earnings could provide a meaningful upside catalyst should the company beat the Street’s estimates at the top and bottom lines. We’d also caution that the opposite could be true if it comes in with another weak quarter. Moreover, CYRX hopes to launch 2 additional products this year, the Cryoport Elite shipper and its Cryosphere segment. This is a gravitationally stabilised cryogenic shipper that will be used in transporting various cell therapies. The Elite shipper will be a negative 80°C shipper that will expand CYRX’s offering into upstream viral vector products. These will be complementary to the CRE segment. We look forward to hearing more of these products as the company releases its full year earnings in the coming weeks.

CYRX market generated data

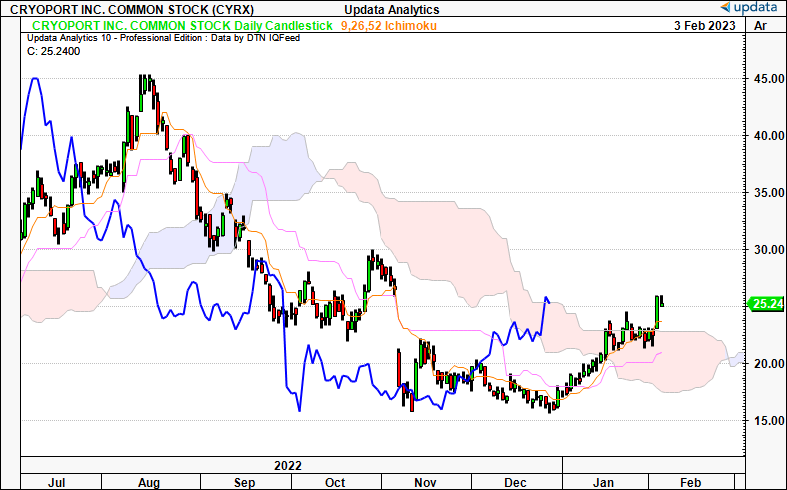

Looking at various technical indicators, with the latest shift off its 52-week lows, CYRX has crossed the cloud and this lets us trade the upside targets listed below. The lagging line [in blue] has also crossed above and is testing the cloud top, telling us that price is bullish at this point.

Exhibit 2. CYRX crossed the cloud in January and this is a bullish setup

Data: Updata

As a result, we have upside targets to $38.5, and we are seeking a move to this level over the coming weeks. A lot rests on the company’s FY22 financials, and, if they are reasonably strong, we believe there’s scope for the stock to re-rate to these levels.

Exhibit 3. Upside targets to $38.5

Data: Updata

In short

CYRX has been heavily punished over the last 12 months of trade. The question now turns to whether this is an appropriate entry point. We are constructive on CYRX’s position in the life sciences value chain and believe the company has scope to rate higher, seeking upside targets to $38.5. Net-net, we rate CYRX a buy.

Be the first to comment