Natal-is

Thesis

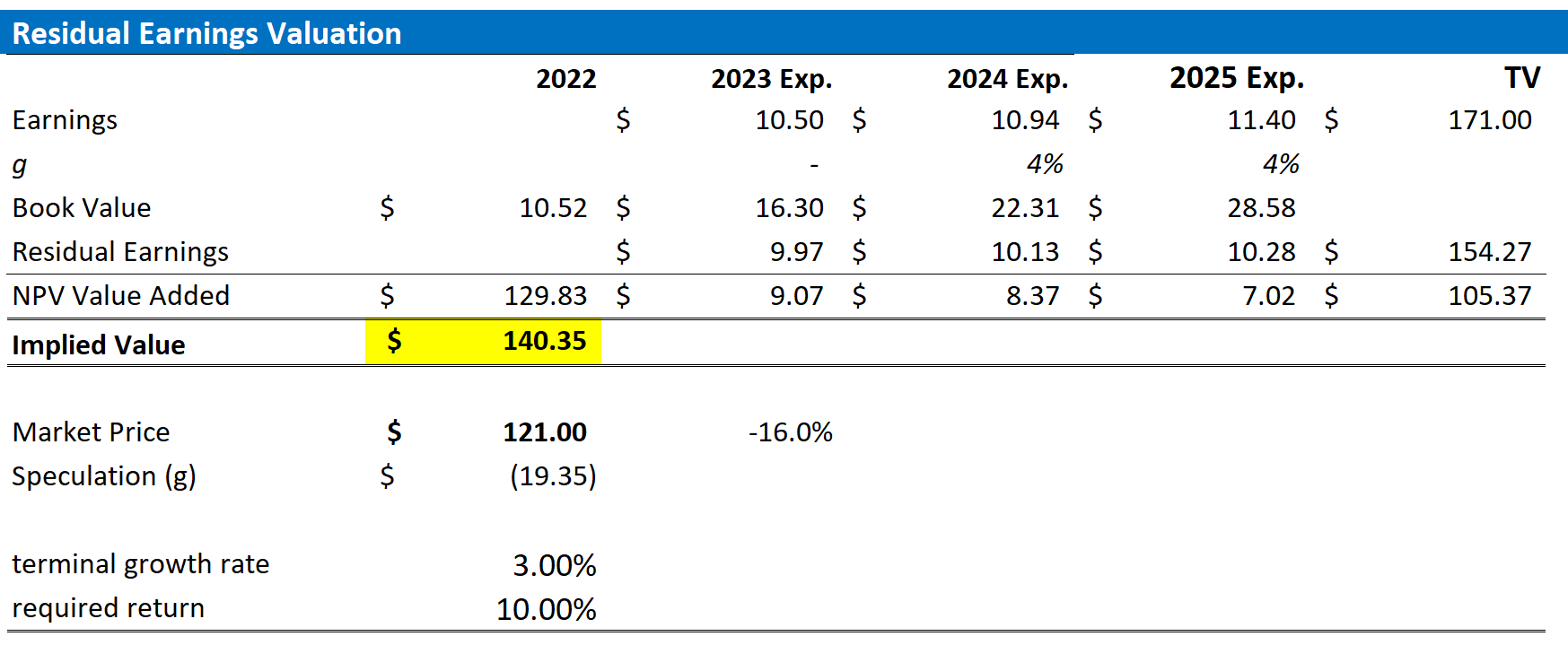

You may think about the company’s shows whatever you like, but objectively speaking it cannot be denied that Crocs (NASDAQ:CROX) is operating an excellent business, with an attractive growth record and strong profitability. Investors should also consider that at this point, after two decades of consistently building brand equity, Crocs has managed to secure partnerships with leading fashion brands such as Balenciaga or Gucci. In addition, international expansion and new product lines are likely to support more growth ahead. Personally, I value Crocs with a residual earnings model and calculate a fair implied share price of $140.35.

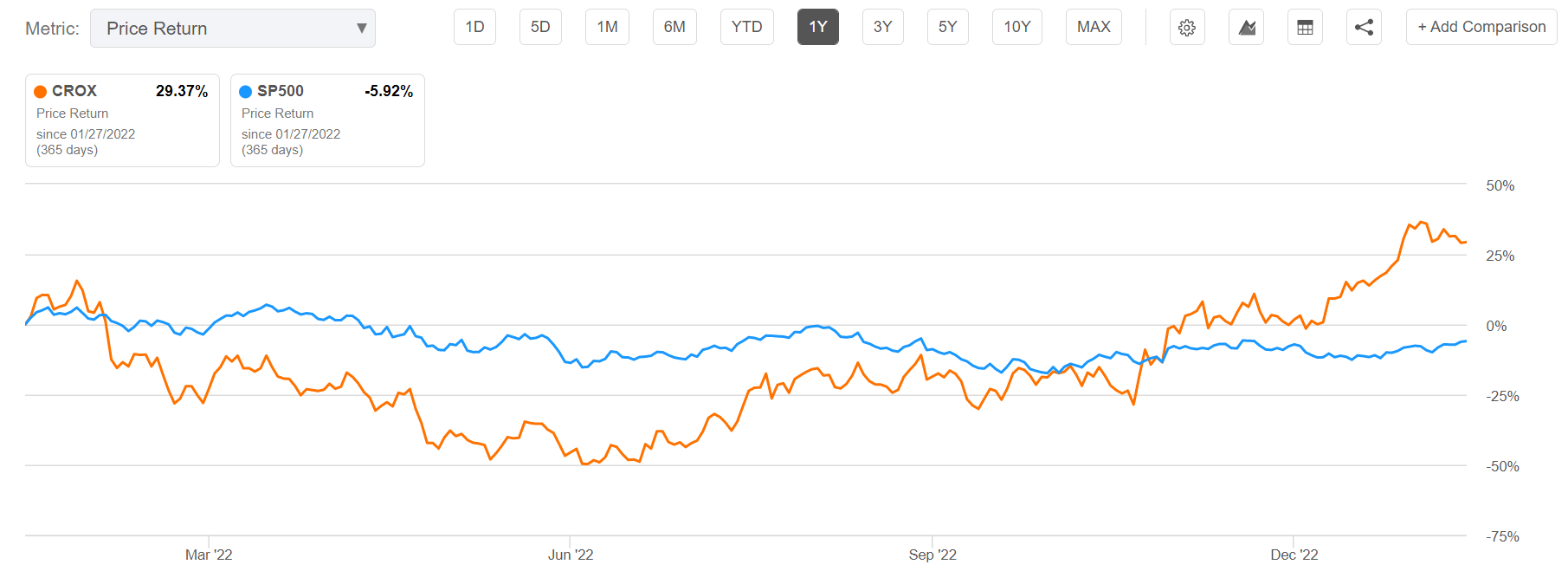

For reference, CROX stock is a relative outperformer as compared to the broad market: for the trailing twelve months, the stock is up close to 30%, as compared to a loss of approximately 6% for the S&P 500 (SPY).

Seeking Alpha

About Crocs

Crocs is a global footwear brand known for its signature foam clog design, known for comfortability and versatility. Given such qualities, Crocs has managed to build a strong brand and managed to capture a loyal customer base. To give more reference to what Crocs is doing, and perhaps it is also the best and most concise explanation, here is a picture that communicates more than a 1000 words.

Crocs website

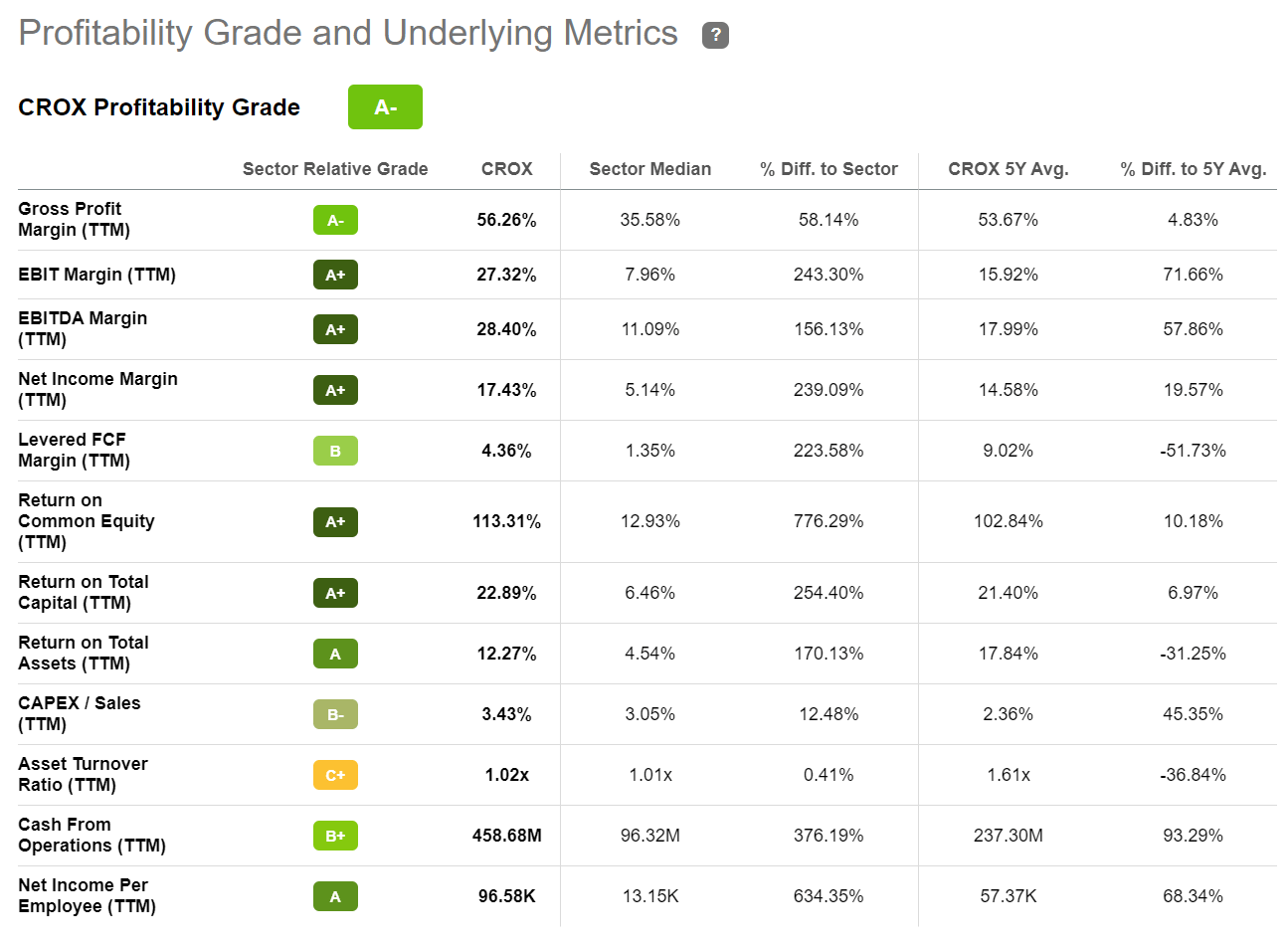

Exceptional Financials …

Looking at Crocs financials, it is hard to argue that the company’s value proposition is anchored on a ‘fad‘ — given the company’s steady track record of business expansion and value accumulation. In particular, I would like to point out the past 3 years: Crocs managed to push revenues from about $1.4 billion in 2020 to approximately $3.2 billion in 2022 TTM reference (post-pandemic). Notably, this is a 2-year CAGR of close to 51 percent! Over the same period, the company’s gross profit expanded to from $740 million to $1.8 billion, and the operating income jumped from $245 million to $873 million, a CAGR of 56% and 89% respectively.

Seeking Alpha

Admittedly, Crocs balance sheet is somewhat stretched: As of Q3 2022, the company recorded only $143 million of cash and cash equivalents, as compared to a financial debt position of $2.9 billion. However, reflecting on $458 of TTM operating cash flow, it is arguably unreasonable to worry about financial stability.

… Not Only Due To COVID

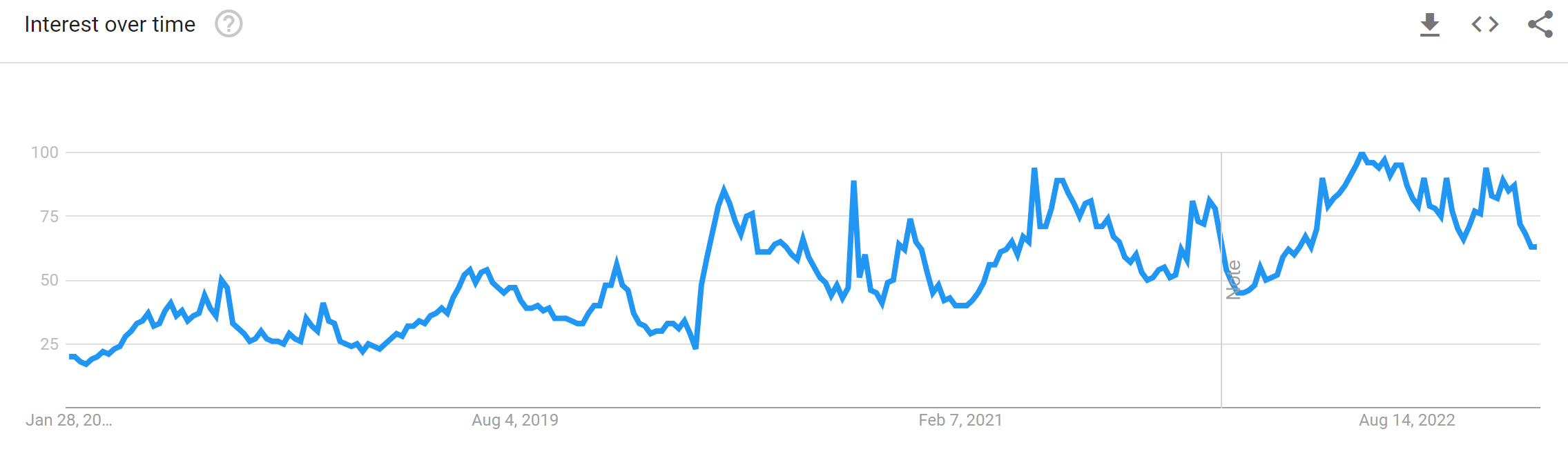

While it is understandable that the attraction for Crocs ‘highly comfortable’ footwear was accelerated by the COVID induced ‘stay-at-home’ trend, there is reason to assume that the growth is also structural. For reference, while Crocs interest always being somewhat cyclical, a Google Trends analysis highlights that during the past 5 years, search interest has been steadily increasing.

Google Trends

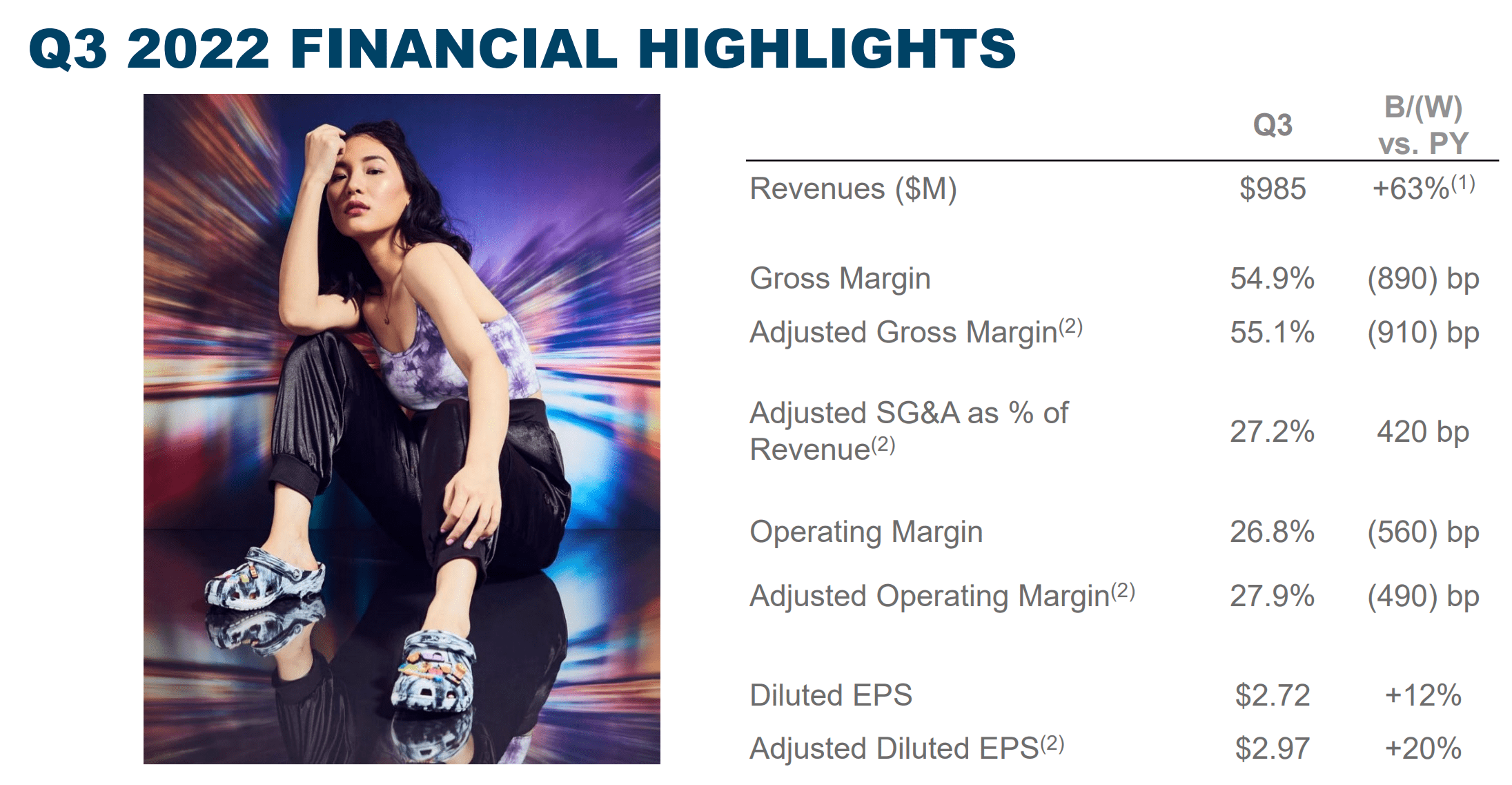

In addition, investors should also consider that as of Q3 2022, with the COVID push undoubtedly having faded, Crocs managed to report excellent results: Revenues expanded 63% year over year, to $985 million for the period.

Crocs Q3 results 2022

In my opinion, there are three key pillars that might support the company’s future growth: (1) New product lines, (2) new product partnerships, and (3) international expansion.

(1) Crocs’ efforts to diversify its product offerings beyond its signature foam clogs has shown early signs of success, and the success is likely to continue. For example, Crocs has been successfully introducing new product lines, such as sandals and boots. The company’s brand HEYDUDE, for reference, has grown at 87% year over year in Q3 2022, generating $269 million revenues.

(2) Crocs is continuing to push brand equity and customer attraction through notable partnerships with leading trend-setting individuals and fashion brands. For example, as of early 2023, Crocs has already successfully collaborated with Post Malone, Gucci and Balenciaga.

(3) Crocs is working to expand its global reach, particularly in Asia and Europe, which is expected to drive growth for the company. This includes growing its retail and wholesale presence in these regions and increasing distribution in key markets, with the goal of reaching new consumer groups and boosting sales.

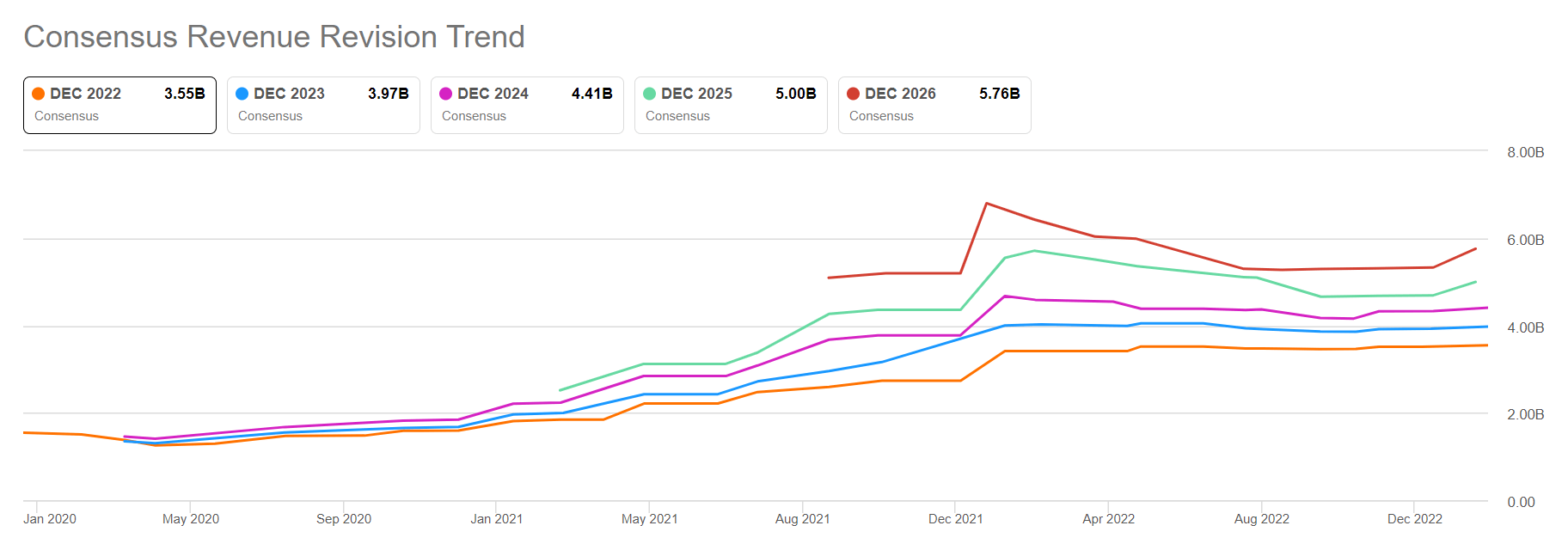

Analysts seem to agree with the thesis that Crocs has more growth ahead: Revenue consensus estimates for 2023, 2024 and 2025 are anchored on $4.0 billion, $4.4 billion and $5.0 billion respectively.

Seeking Alpha

With reference to Crocs growth trend, investors should consider that additional top line is highly value accreditive — given the firm’s strong profitability metrics. For the trailing twelve months, Crocs recorded an EBIT margin of 27.3%. This would imply, assuming similar efficiency, that Crocs would add approximately $390 million of additional operating income to the bottom line by 2025.

Seeking Alpha

Residual Earnings Model

To estimate a company’s fair implied valuation, I am a great fan of applying the residual earnings model, which anchors on the idea that a valuation should equal a business’ discounted future earnings after a capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

With regard to my Crocs stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal ’till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor Crocs’ cost of equity at 10%–which I deem reasonable, if not slightly conservative.

- For the terminal growth rate after 2025, I apply a 3% estimate, which is approximately in line with the expected long-term nominal GDP growth.

Given these assumptions, I calculate a base-case target price for Crocs equal to $140.35, which implies that Crocs could be undervalued by approximately 16%.

Analyst Consensus EPS; Author’s Calculation

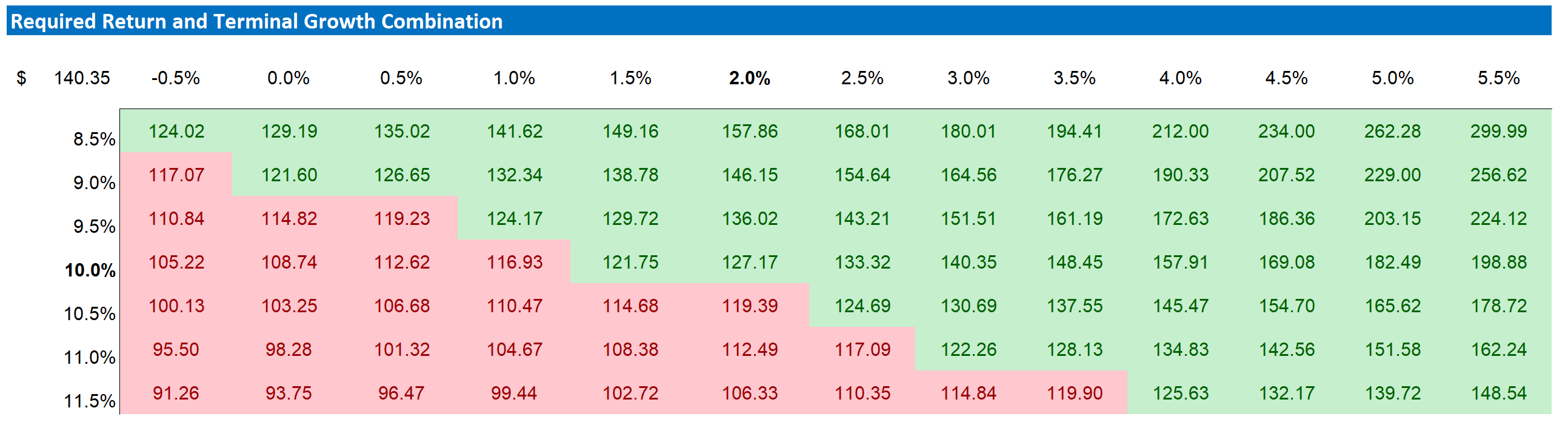

My base case target price does not calculate a lot of upside. But investors should also consider the risk-reward profile. To test various assumptions of Crocs’ cost of equity and terminal growth rate, I have constructed a sensitivity table.

Analyst Consensus EPS; Author’s Calculation

Conclusion

Crocs has captured impressive growth since 2020. While COVID certainly contributed to the company’s business expansion, COVID is unlikely to be the sole driver. In fact, on the backdrop of (1) new product lines, (2) new product partnerships, and (3) international expansion, I agree with analyst estimates that Crocs may achieve $5 billion of revenues by 2025. In that context, a price multiple of FWD x10.7 EV/EBIT looks cheap. Anchored on a residual earnings model, I calculate a fair implied share price for Crocs equal to $140.35.

Be the first to comment