nikkytok

In this article, I will introduce you to Coterra Energy (NYSE:CTRA) and explain why I believe this could be a valid investment opportunity.

Coterra Energy Overview

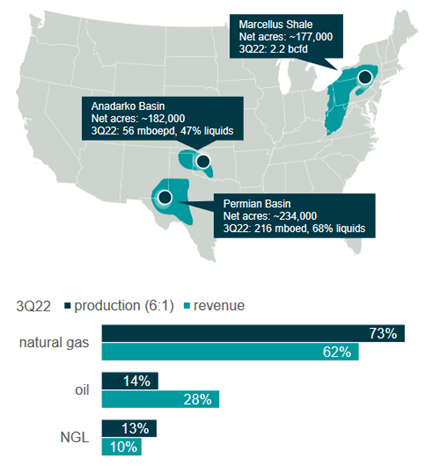

Coterra Energy is a Texas-based energy focused on exploring and developing oil and gas projects. The company was created in 2021 after the merger between Cabot Oil & Gas and Cimarex Energy and has now become a leader in the US onshore oil and gas business. Coterra Energy has production projects across three different US basins:

- Marcellus Shale: in the Marcellus, Coterra holds 177,000 acres and has 100% natural gas production from the Lower and Upper Marcellus. Reserves at year-end 2021 were 2.2 billion barrels.

- Anadarko Basin: Coterra operations are mostly based in the Woodford Shale in Western Oklahoma among 182,000 acres. Production is 54% gas and reserves at year-end 2021 were 198 MMboe.

- Permian Basin: within the Permian, Coterra is focused on the Delaware Basin region between West Texas and Southern New Mexico. Here, the production stream is mostly liquids (64%) and reserves at the end of 2021 were 514 MMboe.

Overall, according to the latest production data disclosed by the company (Q3-2022), the portfolio leans towards natural gas with 73% of production and 62% of sales generated from NatGas in Q3-2022.

Coterra Energy

Coterra Energy Stock Performance

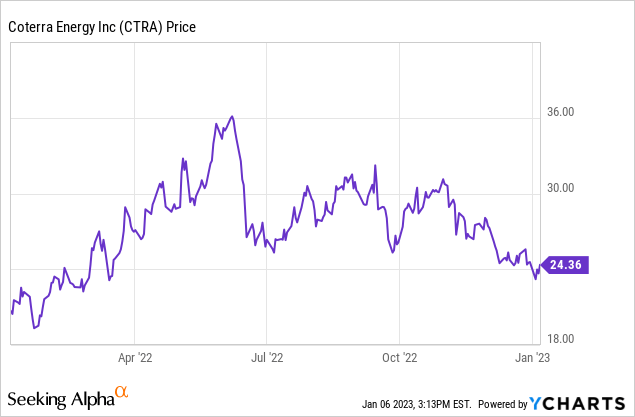

Coterra is currently trading at $24.18/share, equivalent to a market cap of $19.2 billion. The stock is up 18% year-on-year and it is affected by strong volatility: the average standard deviation for the stock price in 2022 was $3.37, or 14% of the current price. The 52-week maximum was $36.1/share (June 7th, 2022) while the 52-week minimum was $19.3/share (January 21st, 2022).

Q3-2022 Coterra Energy Financial and Operating Results

During Q3-2022, Coterra reported total revenues of $2.5B, with $1.6B coming from natural gas sales and the remainder from oil ($755 MM) and natural gas liquids ($259 MM). Obviously, a comparison with the previous year would not add value because of the merger. Operating expenses were $1 B with the largest cost items being D&A ($422 MM) and transportation, processing and gathering costs ($255 MM). Net income for the quarter was $1.2 B.

Cash flow generated from operating activities during the first 9 months of 2022 was $3.9 B while cash flow from investing activities was -$1.2 B since large investments were carried out. Cash flows from financing activities were -$3 B due to $830 MM of debt repayment, $740 MM of stock repurchases and $1.5 B of dividends paid.

At the end of September 2022, the cash available is $0.8 B while debt stands at $2.2 B, resulting in a net debt of $1.4 B. The first debt maturities are in 2024 with $575 MM to be repaid and then in 2026 ($250 MM), 2027 ($750 MM) and 2029 ($500 MM).

Daily production for Q3-2022 was 641 kboe/d, up 9 kboe/d from the previous quarter thanks to the strong well performance and improved cycle times. With current production rates, the inventory can ensure production for about 15 years.

LNG Opportunity in Europe

In Europe, winter 2022-2023 has so far been warmer than usual and, consequently, natural gas inventories are now 95% full and the TTF gas price is declining, though it still is much higher than pre-Covid times. Surviving this winter is no more the key challenge to look out for in the EU, rather being able to start winter 2023-2024 with an adequate level of gas inventory will be the new mission. The current high inventory is the result of some key factors such as gas from Russia that was delivered despite the war and lower LNG imports from China due to lockdowns. In 2023, with China reopening and very limited gas imports from Russia, filling the gas inventory up will be harder since fewer NatGas will be available to the EU. The IEA foresees a potential 30 billion cubic meters gas supply-demand gap for summer 2023, the period when usually gas storages are refilled. In this context, United States could have the opportunity to increase its LNG exports to the European market to help close the gap.

Wall Street Analysts’ rating

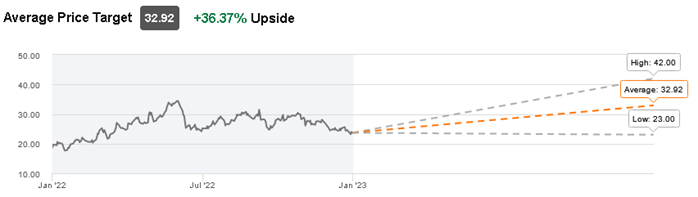

Coterra Energy is currently covered by 25 different analysts. The most common rating is “hold” (16 analysts) with 7 suggesting a “buy” or “strong buy” recommendation. However, the average target price is $32.92/share which would offer a 36% upside from the current stock price.

Seeking Alpha

Conclusion

Overall, Coterra Energy is a solid company with strong cash flows and adequate indebtedness. The lack of short-term debt maturities could enable the company to carry out significant investments in the next couple of years. Among the opportunities, Coterra Energy has stated that it is taking into consideration the possibility of developing export routes to deliver LNG to the European markets: in the first half of 2022, Coterra was among the US companies that met with a delegation from Europe to discuss LNG supply.

In addition, in a business environment that is increasingly focusing on the energy transition, the fact that Coterra’s portfolio is mostly gassy is for sure a plus.

In conclusion, I believe that the current trading price represents an entry point that can still provide an upside.

Be the first to comment