RonFullHD

Investment Thesis

Coterra Energy (NYSE:CTRA) makes more than 60% of its revenues from natural gas. That means that what happens in the natural gas market, both good and bad, will have a full impact on Coterra’s stock.

I make the argument that Coterra has an investment-grade balance sheet and no debt maturities in 2023. That means that Coterra has more than enough flexibility to sustain its $2.68 dividend. This translates into an 11.3% dividend yield right now.

Also, I lay out the bull and bear case facing the natural gas market right now.

The Warm Weather

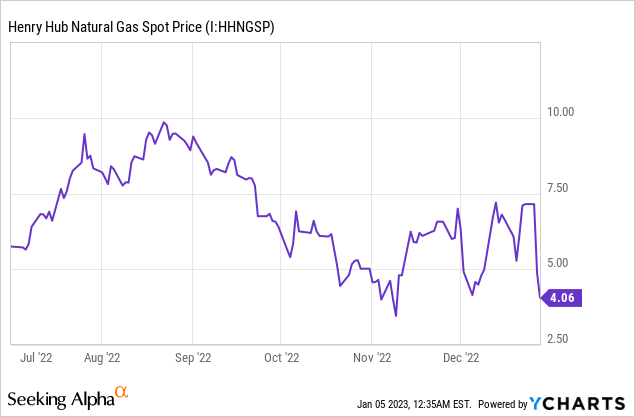

Natural gas prices have fallen dramatically. This has been widely reported and investors will have undoubtedly recognized this already.

Now, this is my argument. The investment thesis for natural gas has not been derailed. Sure, this was unexpected and it made the very near term less bullish than many, myself included, expected.

That being said, I don’t believe that anyone should be attempting to invest in natural gas prices based on what the weather will do over the next two weeks. After all, the weather is, well, the weather. And if you have unseasonal weather, that unnecessarily complicates the setup.

My argument is about the medium and long-term use of natural gas.

Natural Gas, A Bridged Between the Old and New

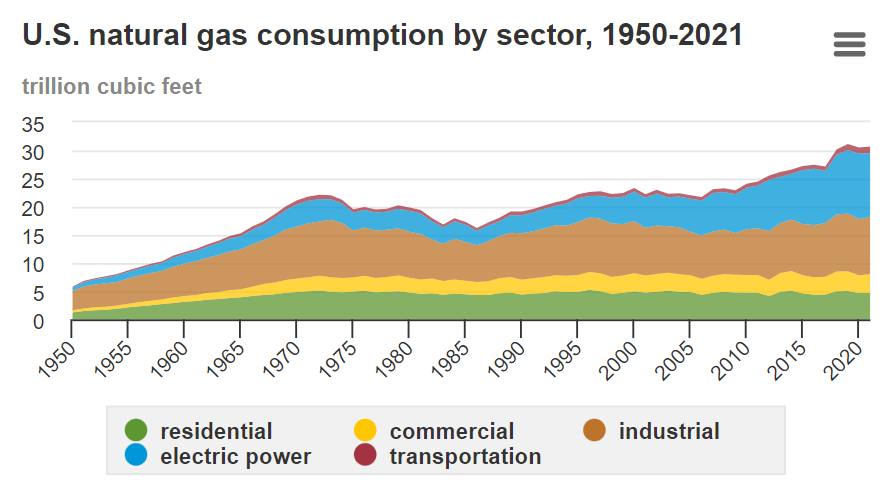

Natural gas is used for heating. And that’s what many investors associate with natural gas usage. Natural gas is used particularly during cold weather.

However, residential consumption of natural gas amounts to 15% of the US’s total consumption usage.

EIA website

And what’s more, that’s not where the bulk of the growth is coming from. The bulk of the growth in natural gas is associated with generating electricity.

Further, approximately a third of natural gas usage in the US goes to produce chemicals, fertilizer, and hydrogen.

However, even this is not where my bull case lies. My bull case for natural gas can be surmised into three bullet points.

- It’s the “greenest” of fossil fuel. Natural gas is accepted by COP27 as a key energy source in the great energy transition that we are already embarking on.

- It’s cheap, reliable, and extremely flexible in its end usage.

- Even now, despite the warm weather, there’s a price arbitrage between natural gas prices in the US and Europe.

Now to elaborate on that third point.

How to Think About 2023

I urge readers to think about winter 2023.

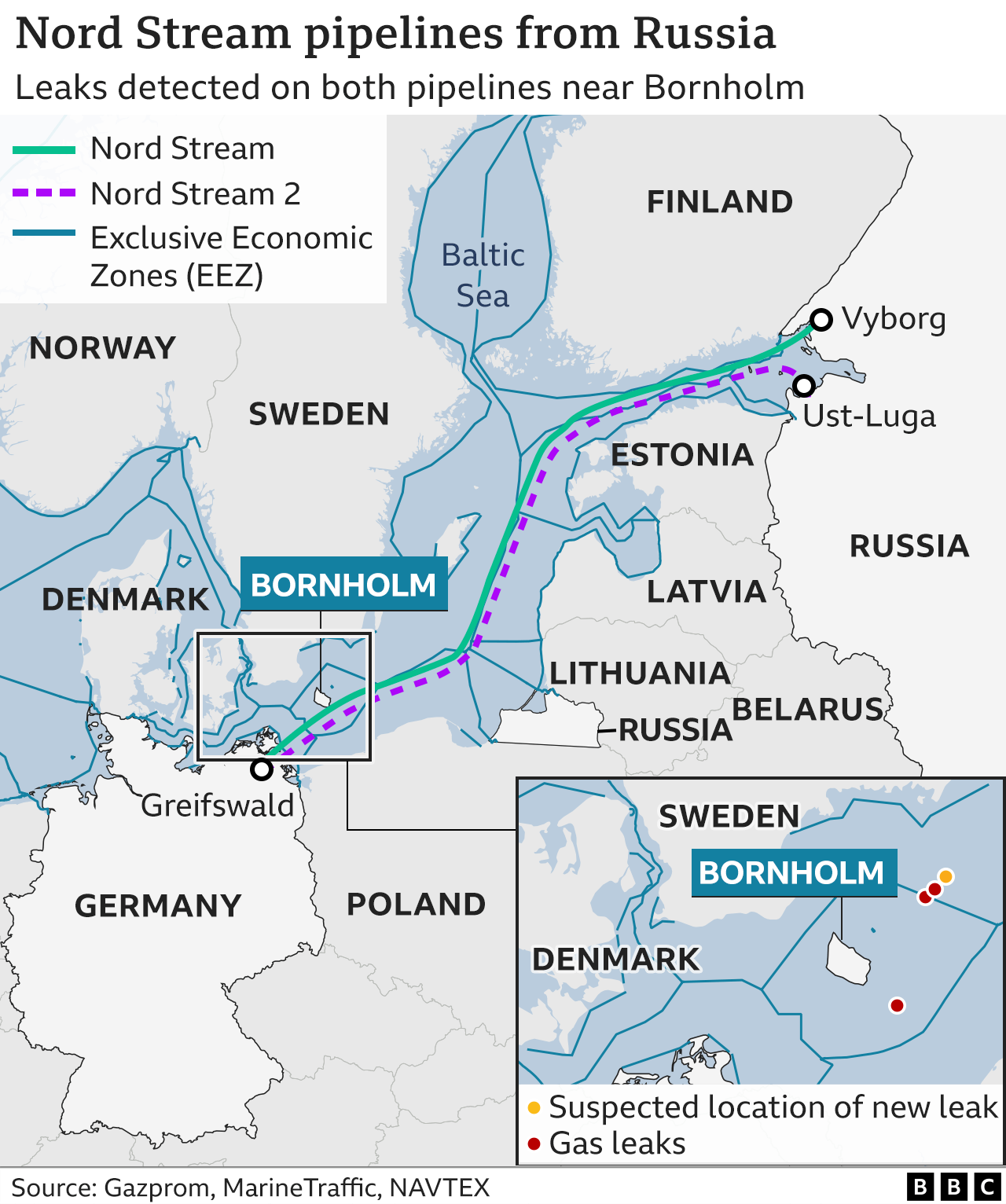

For winter 2022, Europe had plenty of time to fill up gas storage. Russia was still supplying Europe via its Nord Stream pipelines.

Bbc.co.uk/news/world-europe-60131520

But for winter 2023, that’s not the same setup. And just because in winter 2022 Europe not only had plenty of time to prepare and fill storage ahead of time, not to mention that Europe also benefitted from unseasonably warm weather, this will not be the same dynamic next winter.

In fact, it’s extremely unlikely that Russia will now resume flows of natural gas to Germany.

So, how should Coterra investors think about their investment?

Set, Forget, and Collet Your Dividend +10% Dividend

Coterra is committed to returning 50% of its free cash flow via variable dividends.

Furthermore, Coterra has demonstrated over the past several quarters that it’s eager to return excess capital to shareholders via share repurchases and debt paydown, rather than investing in exploration.

This is a theme that is echoed throughout most public companies in the energy space.

What this means in practical terms, is that if 2023 turns out to be substantially less cash flow generative than 2022, Coterra is likely to suspend its buybacks in the first instance, rather than breaking away from its commitment to returning capital to shareholders via its dividend.

As of Q3 2022, Coterra’s total combined dividend was $0.68. This annualizes at $2.72.

That means that if we assume no further dividend increases for 2023 as a whole, investors will get close to an 11.3% total yield from Coterra.

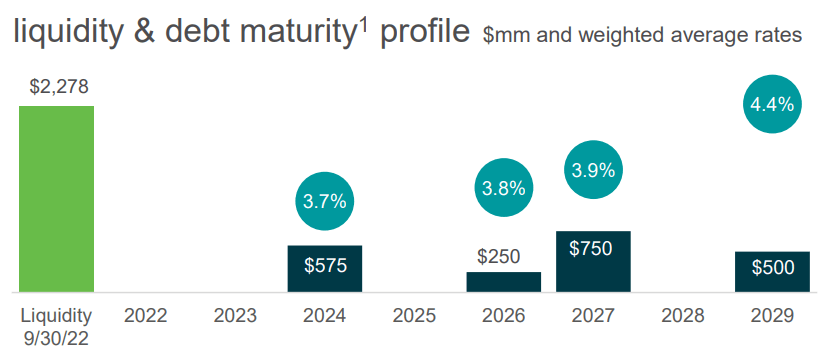

Moreover, consider the graphic that follows, showing Coterra’s debt profile:

Coterra Energy Q3 presentation

As you can see above, Coterra’s debt stack has no debt maturities in 2023. That once again reinforces my contention that Coterra is highly likely to do everything in its power to keep its total dividend for 2023 at $2.72.

The Bottom Line

Coterra is not only part of the energy transition. Centerra is “required” for the energy transition. Energy security is now a serious consideration for many governments. Countries can no longer consider energy as always cheap and always available.

What’s more, by my estimates, investors in Coterra are not just exposed to a secular growth natural gas opportunity. But they’ll also collect approximately an 11.3% dividend yield in 2023.

Be the first to comment