jetcityimage

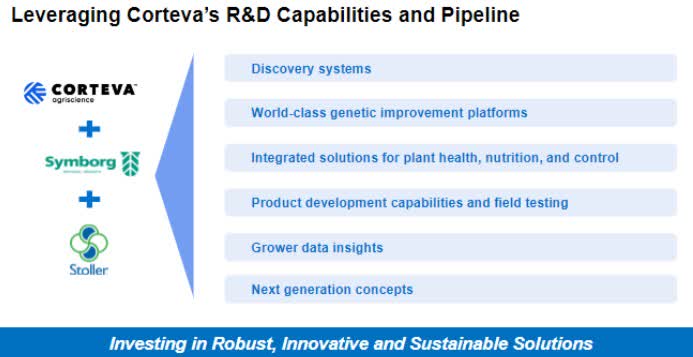

Corteva (NYSE:CTVA) has had a very active 2022. The company has signed a major commercial agreement, started the acquisition of Stoller (biologicals company), opened a seed center in Europe, and made an agreement with BASF and MS Technologies for a new biotech trait for soybean protection.

On December 5, 2022, Corteva announced it is set to acquire biologicals company Stoller. CTVA spent $1.2 billion cash and the deal is expected to finalize in the first half of 2023 pending regulatory approval.

While in March 2022, Corteva signed an agreement with Symborg to exclusively market its products in a host of geographical areas, with an option to expand to other areas as Corteva sees fit. In April 2022 CTVA opened its first Center for Seed Applied Technologies in Europe.

Corteva Inc.

I see all these deals creating great growth potential for CTVA, but let’s talk about the acquisition. The company will use the Stoller platform to move existing biological products. Plus the products that Corteva will sell in its agreement with Symborg.

Corteva will also adopt various products from Stoller that will be incorporated into the plant health treatments line. In a call with analysts, the Corteva CEO mentions that they expect to gain value from synergies, such as a unification of back offices.

However, he mentions that the real potential they see for growth is from Stoller’s sales platform and its seed treatment products. But it reminded me that of course, they should gain in value from such synergies also.

Going back to the commercial agreement with Symborg, their product helps fixate nitrogen from the air. This technology provides a sustainable way to source nitrogen. I feel this product could be a large revenue source going forward.

I say that as we have seen examples all around the world where policies have hindered or drastically reduced nitrogen-based products.

I believe this company has a solid future ahead and most growth will be driven by an expanding market. As we will see further down, the industry trend looks positively strong. We’ll also take a look at some fundamentals and technicals for CTVA.

Corteva Fundamentals

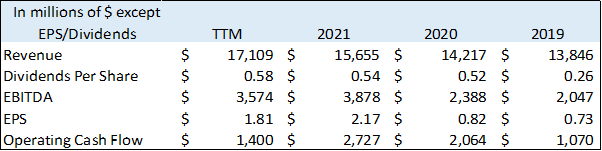

There’s nothing not to like about the fundamentals here. I see consistent growth in revenue and earnings. Revenue has increased by 23.6% from 2019 to the TTM. While earnings, as measured by EBITDA, have increased by 74.6% over the same period.

EPS and FCF have also been on a consistent increase. And cash from operations shows the company has a very long runway in the case of unforeseen adversity. The liabilities to assets ratio is low in absolute terms at 0.38 and low compared to the average of its closest peers of 0.53.

Seeking Alpha

Corteva is a relatively young company, founded in 2018 as a division of DuPont and subsequently spun off in 2019. So, it’s early to make definite assumptions about dividends. However, they have been paying dividends over the past 3 years, and dividend growth has been in line with the market sector or slightly better.

Quant Rating

The Quant rating is a Hold. And the reason for the grade is the Valuation factor that gets a D-. In fact, no matter which way you look at CTVA it is over-valued when compared to its peers. If you are a value investor, my guess is you would have to give this stock a pass.

Seeking Alpha

My opinion is that the market is factoring in the future growth potential of this company and is expecting higher earnings going forward. This is the only factor weighing down the overall Quant rating for Corteva, which for me is a buy.

Industry Trend

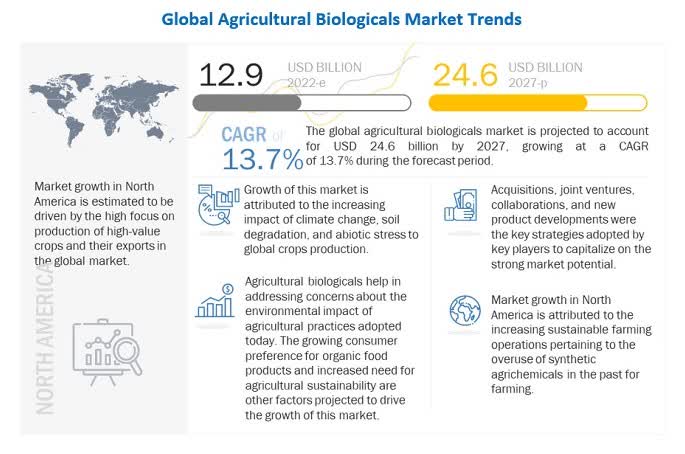

I assume there will be a lot of extra growth potential for Corteva through the acquisition of Stoller. Corteva expects the biologicals end market to grow by 8% to 10% CAGR from 2021 to 2035. The market is currently worth $9 billion and would grow to $30 billion under their forecast.

However, that’s a prudent forecast, and other reports I have accessed show a higher CAGR. The report from Fortune Business Insights sees a CAGR of 14.07% from 2021 to 2029. And the report from Markets and Markets sees a CAGR of 13.70% through 2027.

Markets And Markets

Both reports mention a growing awareness of the need for biological plant enhancement products. And the increasing cases of pest resistance to some chemical plant protection products. Soil degradation is also a rising concern that biologicals can protect against.

Given the current political and societal interest in environmental protection, the market should see a rise in the restrictions on chemical fertilizers and plant protection products. On the other hand, acceptance from farmers is hindered by the perception of higher efficiency in chemical products and cheaper prices.

Altogether, the biologicals market is still a fraction of the traditional fertilizer market. According to Precedence Research, the fertilizer market is worth $207.93 billion in 2022 and is expected to grow by 3.4% CAGR to $245.71 billion by 2027.

We can see how the biologicals market is set to expand from around 6% of the fertilizer market to approximately 10% by 2027. I believe the biologicals market could even account for a higher percentage if the political setting continues to foster environment-friendly policies as we move forward.

Technical View

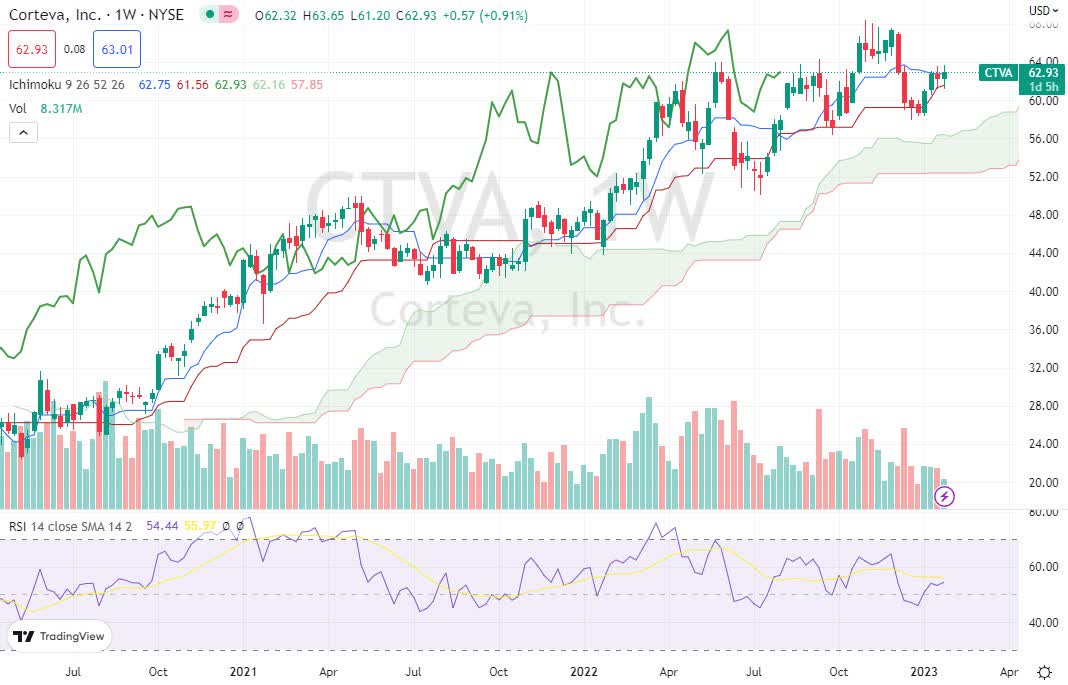

The stock has only been trading on the NASDAQ exchange since June 2019, so the long-term charts are still not meaningful yet. Looking at the weekly chart below I see a medium-term bullish trend. Price action has been above the Ichimoku cloud consistently over the past 2 years.

TradingView

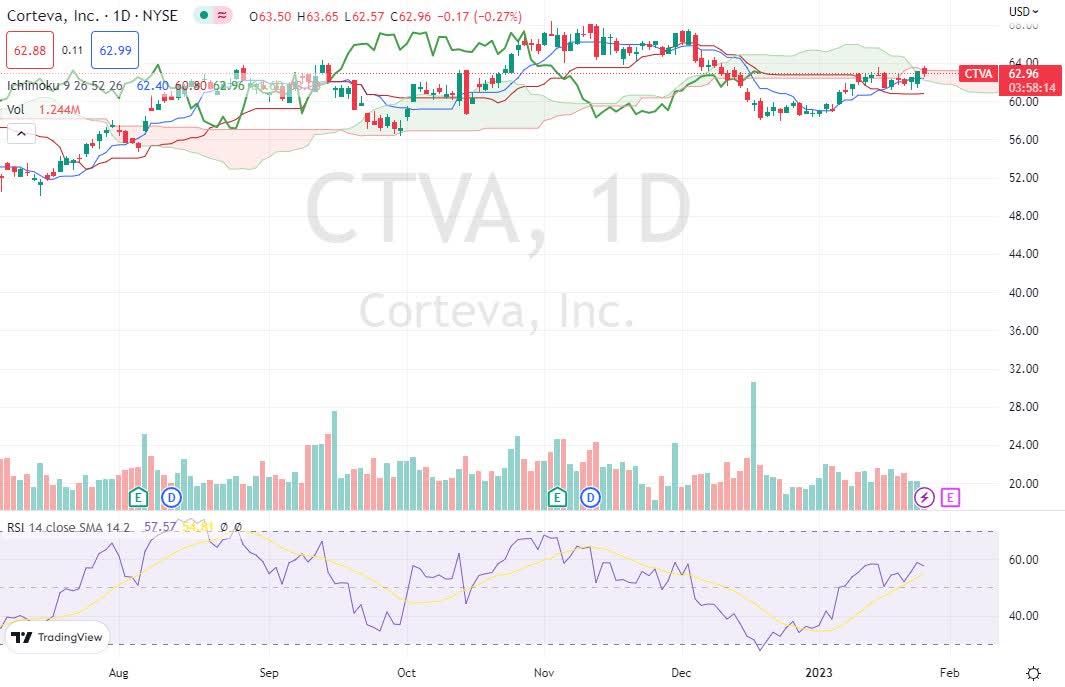

I see support for this stock at the top of the cloud around the $57 area. With more room to the upside, price action should find resistance at $68.43, its all-time high. The daily chart below shows some weakness with share prices falling below the cloud.

However, I believe any further dips south would be limited to the support area given from the cloud on the weekly chart. The RSI on the daily chart is still above 50 and its moving average, indicating bullish momentum is still intact.

Trading View

Conclusion

Corteva will announce Q4 2022, earnings on February 1, and we should have further insight into how well this company is performing most recently. We’ll see if the CTVA earnings report beats estimates again. In the recent past, this company has had 3 straight years of positive surprises in earnings releases.

Despite the high valuation compared to its peers, I see this company as well positioned to make great leverage of its recent activities. The acquisition of Stoller I feel has great potential and will add to the company’s sales capacity. As will the Symborg agreement that also adds quality products.

Be the first to comment