Galeanu Mihai

Introduction

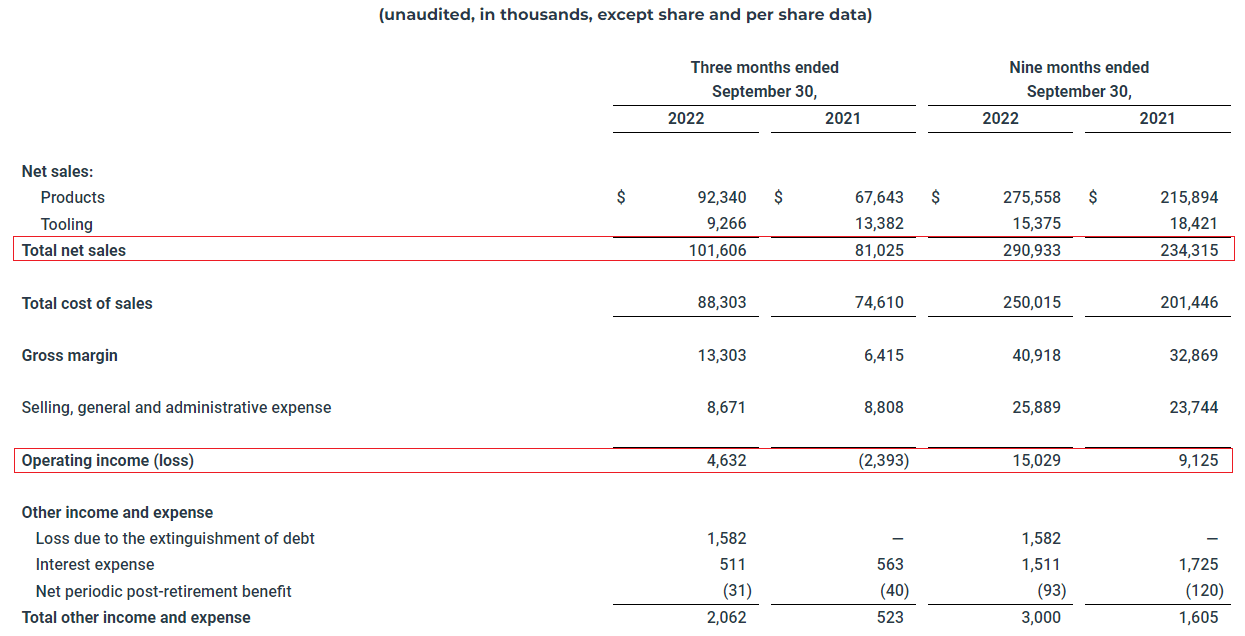

I like to write about companies that lack coverage on SA, and today I’m taking a look at Core Molding Technologies (NYSE:CMT). It’s a relatively small engineering materials company focused on reinforced plastics, and I think it looks undervalued considering its financial results have improved significantly over the past few years. During the first nine months of 2022, sales rose by 24.2% while the net income soared by 74.3% to $7.4 million. Let’s review.

Overview of the business and financials

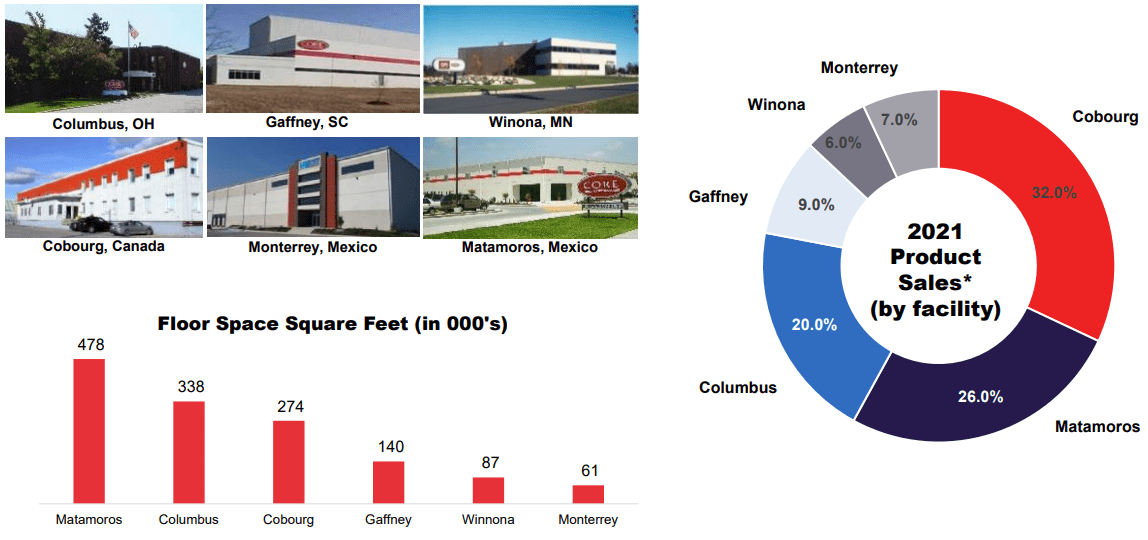

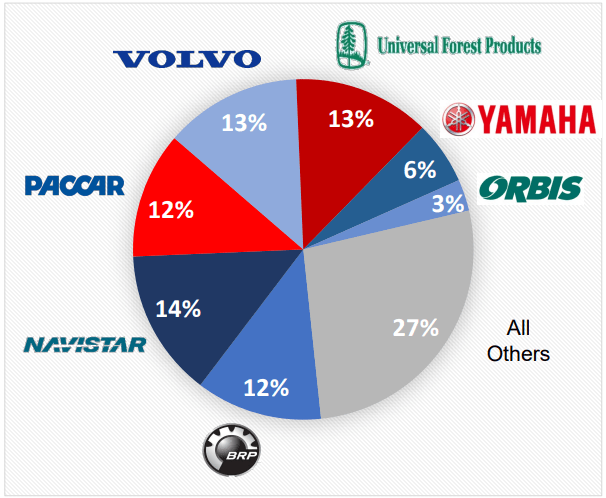

Core Molding Technologies was founded in 1980 under the name Columbus Plastic Operations, and it focuses on the advanced fabrication of fiber-reinforced plastics and plastic composites for custom applications such as industrial fan blades, structural reinforcements, and vehicle roofs. Reinforced plastics represent a combination of resins and reinforcing fibers that get molded to a certain shape and the company’s target markets include medium and heavy-duty trucks, power sports, building products, and utilities among others. Core Molding Technologies currently has 6 production facilities across the USA, Canada, and Mexico which have a combined area of over 1.3 million square feet. The company’s main clients include major companies such as Navistar, Volvo (OTCPK:VOLVF, OTCPK:VOLAF, OTCPK:VOLVY), UFP Industries (UFPI), and Paccar (PCAR). As you can see from the charts below, Core Molding Technologies is heavily reliant on the truck industry.

Core Molding Technologies Core Molding Technologies

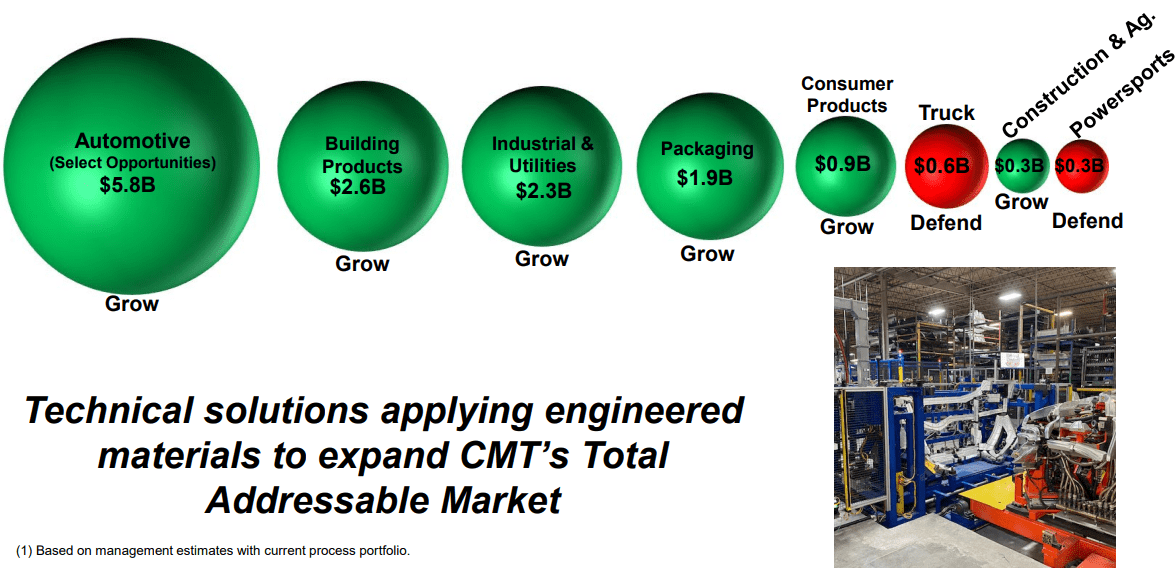

According to a recent report from Global Industry Analysts, the global reinforced plastics market was worth $240.1 billion in 2022 and is projected to grow at a compound annual growth rate (‘CAGR’) of 3.4% to $314.5 billion by 2030. The U.S. reinforced plastics market was estimated at $70.2 Billion in 2022. According to the latest corporate presentation of Core Molding Technologies, the total addressable market (‘TAM’) considering its current process portfolio is about $15 billion and there are high barriers to entry. As you can see from the slide below, the automotive sector accounts for the largest share of the TAM.

Core Molding Technologies

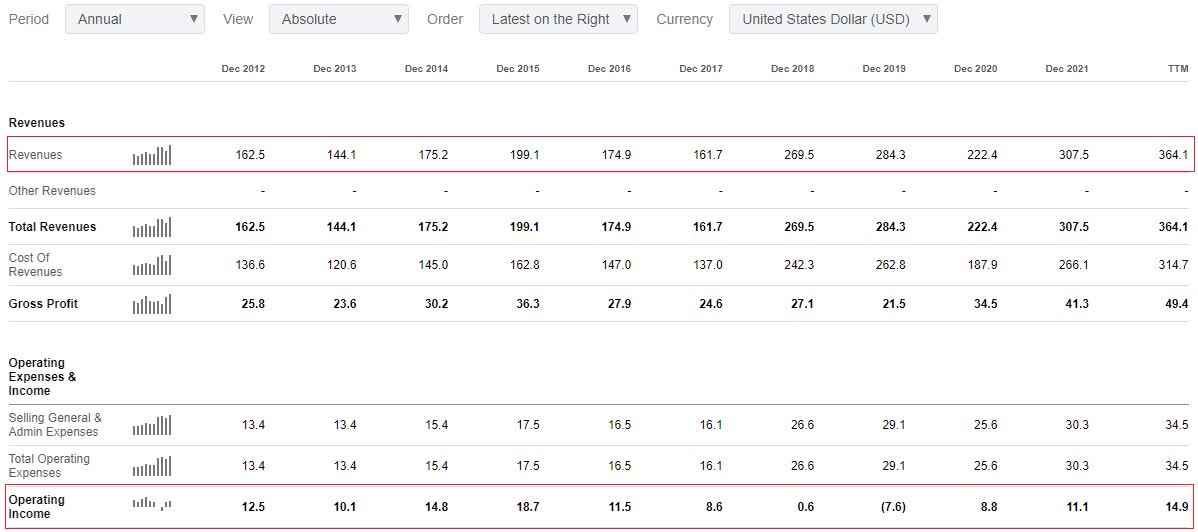

Turning our attention to the financial results of Core Molding Technologies, we can see that revenue growth was erratic until 2017 and that the company has been on a path of rapid growth since then (except in 2020 due to the COVID-19 pandemic), and that operating income has improved significantly over the past few years.

Seeking Alpha

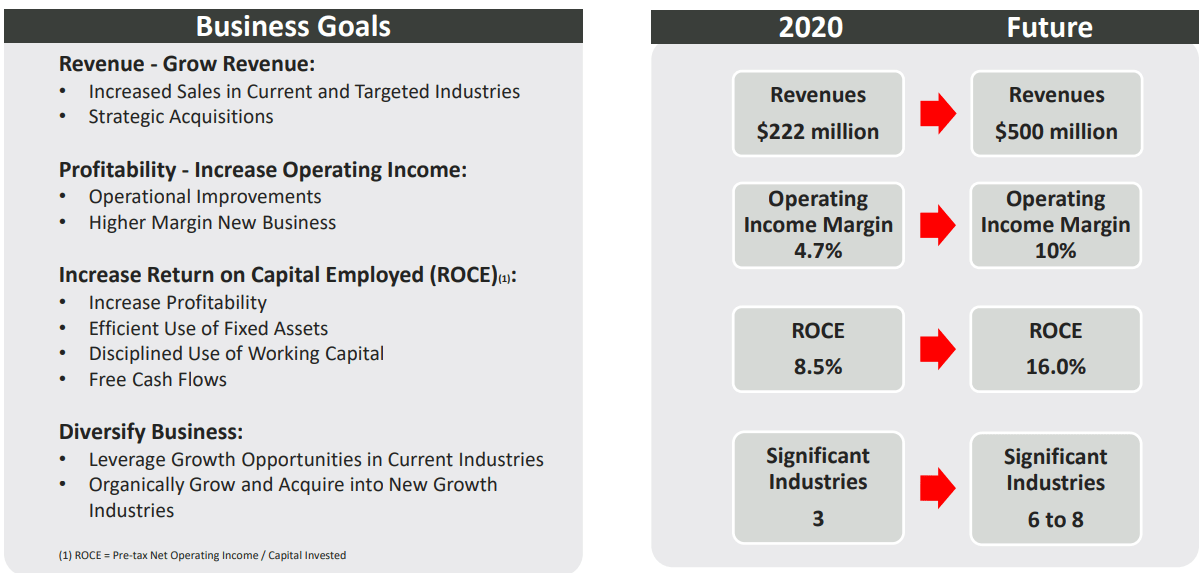

Well, a large part of the growth in 2018 came from the $63 million purchase of a competitor named Horizon Plastics International, which had revenues of $62.6 million during that year. The remainder of the recent growth has been organic, as Core Molding Technologies has also been expanding its capabilities over the past years, with around half of its revenues coming from processes and materials acquired since 2015. Looking at the improved margins, Core Molding Technologies embarked on an operational turnaround in late 2018 which included the replacement of the operational management team, the implantation of new operational systems and processes, as well as the increase of repair and maintenance spending to improve asset reliability. This turnaround was completed in 2019 and paved the way for Core Molding Technologies to increase its net income to $7.8 million for the last 12 months. The company plans to accelerate its growth through strategic tuck-in acquisitions, and its long-term goals include reaching annual revenues of $500 million and improving the operating income margin to 10%.

Core Molding Technologies

Considering TTM revenues are $364.1 million, this part of the goals seems achievable in about 3 years even without acquisitions. Net new business and program wins during the first nine months of 2022 stood at $24 million, and the company recently inked a new agreement with UFP that extended their relationship for 5 more years. However, the TTM operating income margin is just 4.1% as the business of Core Molding Technologies has been put under pressure by raw material inflation. The company has been passing on cost increases to customers in a gradual manner, and the operating income margin improved to 4.6% in Q3 2022.

Core Molding Technologies

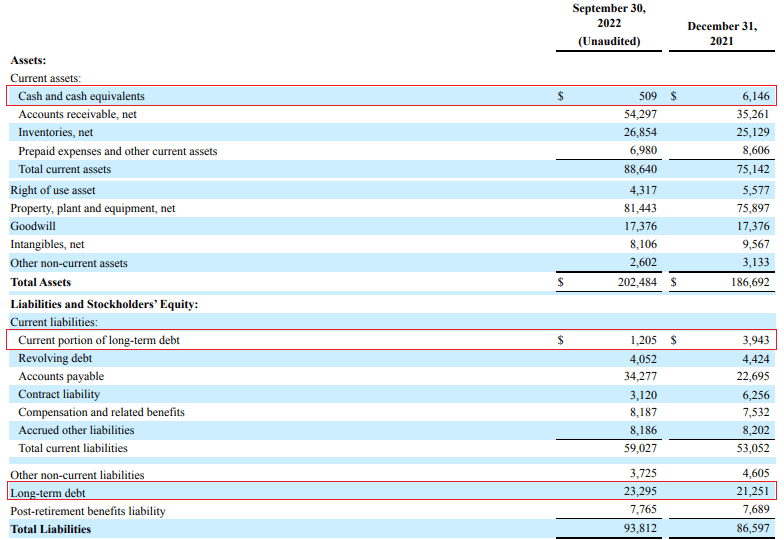

Turning our attention to the balance sheet, I think that Core Molding Technologies is in a good position to look for acquisitions at the moment as it completed debt refinancing and interest rate swap transactions during Q3 2022. In late July, the company refinanced its $50 million Wells Fargo (WFC) debt facility with a $75 million credit facility (a term loan commitment, a CapEx loan commitment, and a revolving loan commitment of $25 million each) from Huntington National Bank. The interest rate for the new revolving loan and term loan was 4.08% and 4.75% as of September 2022, respectively. For comparison, the weighted average interest rate for the Wells Fargo loans was 6.75% as of June.

In my view, the debt level of Core Molding Technologies seems manageable at the moment. As of September 2022, the company had a net debt of just $24 million, which puts the net debt to TTM adjusted EBITDA ratio below 0.8x.

Core Molding Technologies

Overall, I think that Core Molding Technologies carried out a successful operational turnaround in 2018 and 2019, but its improved performance has been overshadowed to some extent by COVID-19 as well as supply chain disruptions and inflation. In my view, the company is in good shape financially to make another acquisition of similar size to Horizon Plastics International, which should allow it to boost its revenue growth. Looking at the margins, I expect the company to pass on raw materials cost increases to customers over the coming months.

Looking at the risks for the bull case, I think there are two major ones. First, Core Molding Technologies has heavy exposure to the truck sector, and a prolonged recession in North America could lead to a slowdown in the revenue growth rate. Second, the daily trading volume rarely exceeds 10,000 shares and this means share price volatility is usually high. In my view, it could be dangerous to start a large position as it would be challenging to exit without putting pressure on the share price.

Investor takeaway

I like a good turnaround story, and it seems that the one of Core Molding Technologies has been going largely unnoticed over the past few years due to COVID-19 and inflation. In my view, the company has good organic growth and a strong balance sheet, and I expect its operating income margin to gradually improve to 10% as it passes on cost increases to its customers over the coming months. In my view, the share price could double in a couple of years if everything goes well, and I plan to open a small position on a pullback below $10 per share. I think it’s dangerous to open a large position due to the low trading volume.

Be the first to comment