jimfeng/E+ via Getty Images

Recommendation

I recommend buying Core & Main (NYSE:CNM). CNM had a prosperous quarter thanks to rising demand in municipal and non-residential end markets, an increase in market share, and a very inflationary economic climate. Valuation worries regarding the construction cycle and the long-term viability of pricing and margins have caused the stock to underperform over the past year. However, I expect the stock should improve from here because of the improved outlook for this year’s results.

Latest earnings highlights

In the October quarter, organic sales rose by 27% and total sales rose by 29%, both slightly exceeding the 27% rise recorded by (FERG) (CNM’s peer) for its Waterworks unit. The expansion was fueled by a 22% increase in prices, a volume increase in the mid-single digits, and a 3% increase via acquisitions. Management feels that it was the successful execution of growth objectives that allowed the company to beat end markets and increase market share throughout the quarter. The residential market decreases were partially mitigated by the rise in the municipal and non-residential sectors. PVC pipe’s pricing has leveled out despite having more formidable competition, although non-commodity products have seen further increases in price. This trend is anticipated to continue into the fourth quarter, with embedded price increasing by the low-double digits as comps for commodity pipe products grow more challenging as measured by the relevant PPI categories.

Overall, the underlying revenue forecast for 4Q is for an increase in the low-single digits to low-double digits, driven largely by pricing, with volumes down in the middle- to upper-single digits against more difficult year-ago comparisons. As for gross margins, a favorable product mix and adequate inventory drove the higher-than-anticipated gross margins (27.5%). Management expects a transitory gain in year-to-date gross margins of roughly 100 bps to 150 bps from price, cost, rebates, and mix shift effect, which would imply a normalized gross margin of 25.5% to 26% (a minor decline from 26.9% year-to-date).

Volume updates

Third quarter municipal repair and replacement activity was high, and this trend is anticipated to continue into the fourth quarter and beyond, as municipalities with good budgets are able to engage in upgrades to their aging water infrastructure. I think the near-term catalyst that might generate more momentum in this sector is when the infrastructure bill budget goes into municipal projects in 2023.

Management believes that a 12- to 18-month lag from residential building, as well as storm drainage projects for roads and bridges, is the reason for the uptick in non-residential construction that has accompanied the expansion of suburban areas. As for residential, even though shipments were booming in the third quarter, they started to lag behind the strong volumes at the close of the period.

Considering the current backlogs of CNM customers, I anticipate that both municipal and non-residential demand indicators will continue to show growth in the near future. Moreover, I expect municipal repair and replace to expand and be positive in the last quarter, while non-residential bids and backlogs should also be positive and should see steady demand through the end of the year. While I am optimistic about the residential market as a whole, I do expect it to face challenges in the fourth quarter as it competes with high volumes and as the number of new single-family homes is continuing to decline recently. I also expect this year’s average 4Q seasonality, which, when combined with the challenge of measuring up to last year’s robust 4Q21, which benefited from unusually good weather, will lead to a drop in volume in 4Q22.

Management has speculated that resilient end markets will support above-average expansion through FY23, although they have been cagey about the company’s projected volume growth. Still, they admitted that things are different now than before the economic downturn of 2009.

Pricing update

Due to increasing demand and continued supply chain issues, prices have been higher than planned for a longer period of time. As a result, costs went up all through the third quarter, and I anticipate that trend maintaining itself until year’s end. In my opinion, continued price rises are warranted because of the persistent scarcity of numerous things. However, management did note improved lead times and stock levels for some products, which contributed to price stability. The company’s management thinks its products’ industry-specific nature gives them some protection from price fluctuations, but they’re keeping an eye on the effects of increased supply and decreasing demand. As product availability improves, I anticipate management will begin reducing inventory levels for those products. If this is the case, CNM may reduce its inventory holdings without compromising service, and it should do so in the fourth quarter and into fiscal year ’23. This will help the company’s working capital position.

Margins

The boost in gross margins that occurred in the third quarter was largely attributable to a one-time benefit from a shift in the product mix, but it still managed to push margins over expectations. Due to normalizing mix and catching up inventory to market prices, I expect margins to fall sequentially in the fourth quarter. According to the company’s projections, gross margins for the year as a whole could be reset by 100 basis points to 150 basis points if supply chains reach a new normal. On the other hand, the incremental profit from new acquisitions and the success of the private label product strategy should more than makeup for any reduction in gross margin. In addition, I think CNM still maintains a sizable stock of low-cost non-commodity products, which could aid in delaying this normalization until FY23.

Valuation & model

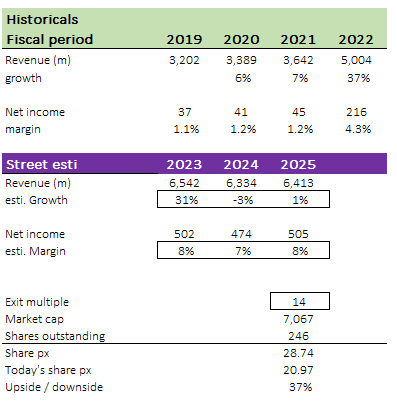

I still believe the stock has a 37% upside over the next three years, based on my updated model based on Street revenue and net income estimates. Similar to the consensus, I believe revenue will grow rapidly in FY23, then slow in FY24 due to the weak global macro environment, before recovering in FY25. The most important factor to consider is profitability. I anticipate that net margin will remain stable in the future.

My opinion on the valuation at which CNM should exit in FY25 remains unchanged. CNM is currently trading at 9x TTM earnings, which is 5x lower than its average before the recent decline. I believe the recent de-rating is simply volatility, and CNM will trade back to its average once the macroeconomic cycle improves.

Author’s own calculation

Summary

To conclude, I still think CNM is undervalued. I still view CNM as a frontrunner in the US waterworks sector, which, in my view, has favorable tailwinds in the near to medium term. Its size and prominence in the industry should allow it to expand its share of the market. Efforts to increase margins appear realistic, which bodes well for my theory that multiples will eventually revert to their historical norms.

Be the first to comment