imaginima

Comstock Resources, Inc. (NYSE:CRK) has one of those ideal locations that you just have to love. Management has easily some of the best costs in the industry and keeps ahead of the technology changes to continue to lead much of the dry gas industry in costs. The great location makes this company an industry leader for the foreseeable future.

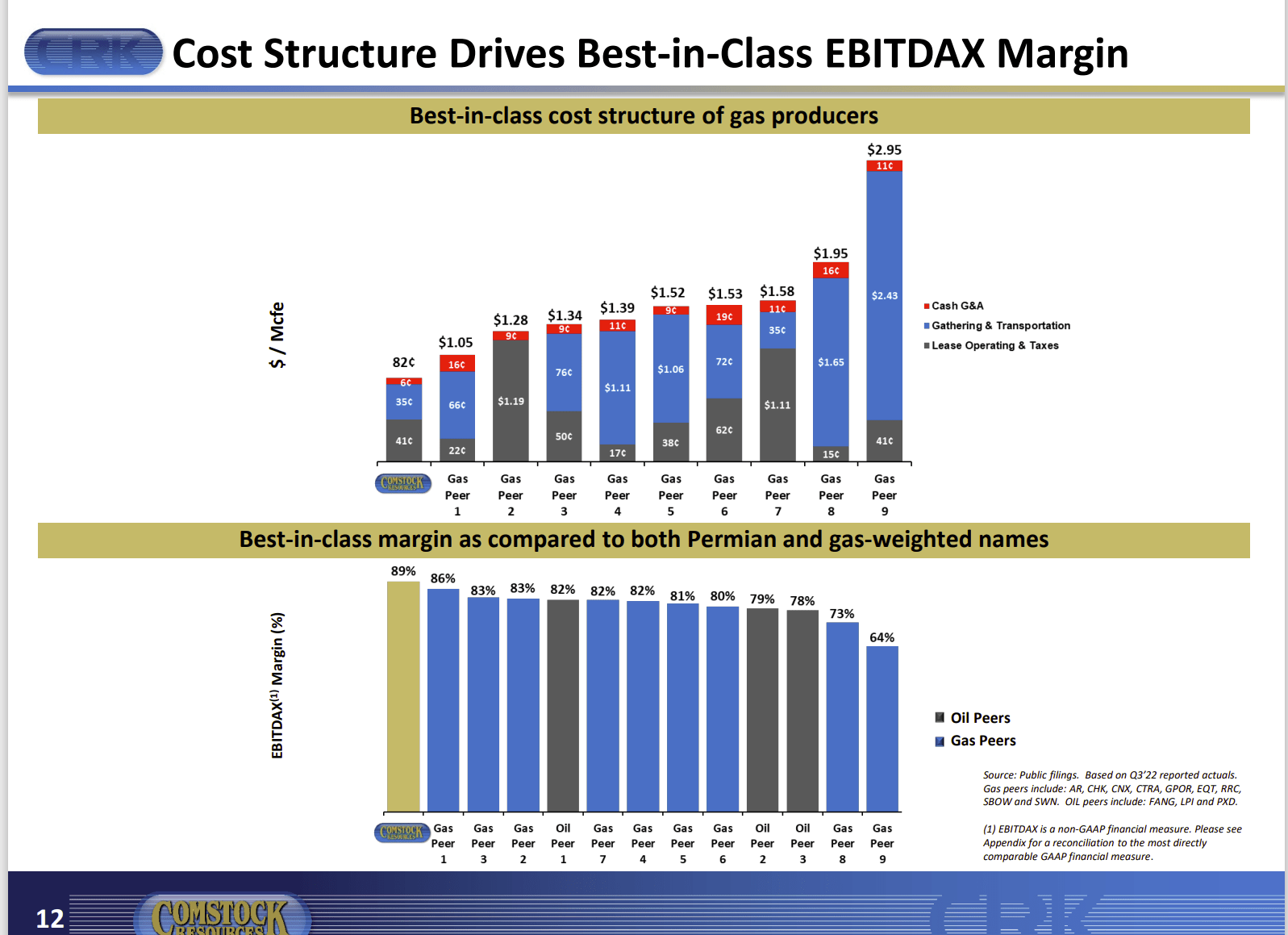

Comstock Resources Operating Costs Comparison (Comstock Resources Corporate Presentation January 2023)

Some costs are rising because they are related to the current rise of commodity prices. Even so, the overall cost structure is low, and it appears to be heading lower at various pricing points as management continues to take advantage of improving technology over time.

What is even better is this basin is one of the closest to a lot of exporting capability. So, the access to strong world prices is among the best of many companies I follow. The low transportation cost to export is a competitive moat that probably will not be matched by much of the industry any time soon. Management can easily justify higher transportation costs to some strong markets should that prove to be the case. But right now, the export market appears to be the market of the future, and this company is in “the catbird seat.”

Similarly, the administrative costs are easily among the lowest of all the companies that I follow. Those costs have been low for some time. So, it does not appear that continuing administrative costs will be climbing anytime soon.

The overall cost structure shown above leads Comstock Resources, Inc. to an industry-leading gross margin that currently hovers around 90%. When combined with the volumes produced in each well, the breakeven costs of this area are just mouth-watering.

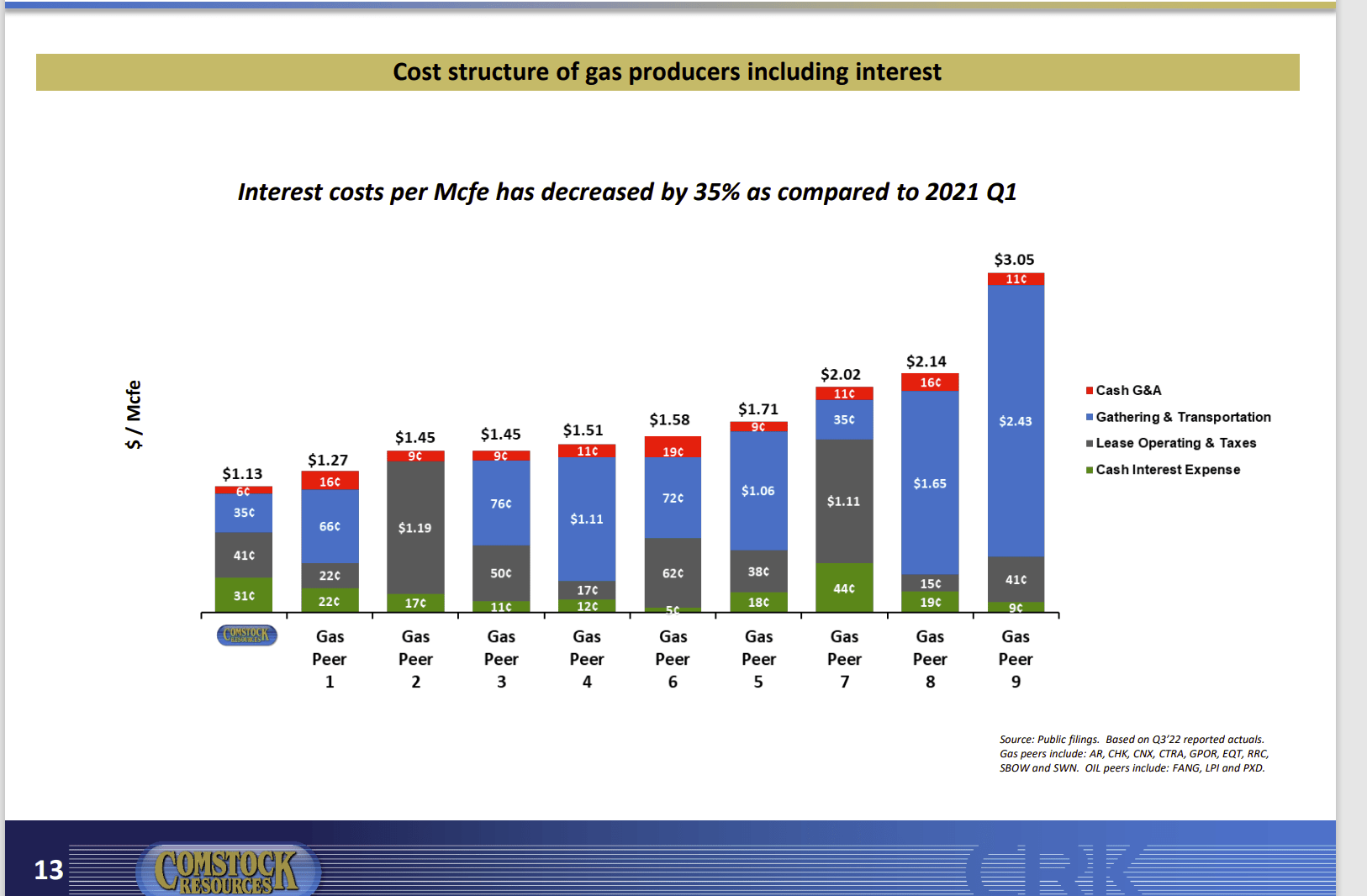

Comstock Resources Operating Costs Plus Interest Comparison (Comstock Resources Investor Presentation January 2023)

So many investors believe that high financial leverage is necessary for a big return. Yet, a lot of large investors go for operational leverage that results in superior margins and cash flows. The reason is that this industry is notoriously low visibility. The fact that debt has to be serviced and repaid even when unexpectedly weak industry conditions prevail is a serious disadvantage in a commodity industry.

Therefore, it is important to note that this company was able to dig itself out of a debt situation through a combination of a series of cash infusions combined with a low-cost structure that allowed for some debt. As shown above, the debt load is relatively substantial on a per-MCF basis. However, the whole thing works because of the low-cost structure.

All Comstock Resources, Inc. management has to do to increase the competitive advantage is repay debt to decrease the per unit cost of the debt shown above. In the current industry environment, that is an easy assignment. But it is also easy to see why management wants to get rid of as much debt as possible before the next cyclical downturn. Therefore, income investors can probably look elsewhere for a while because debt repayments will be a priority for quite some time into the future.

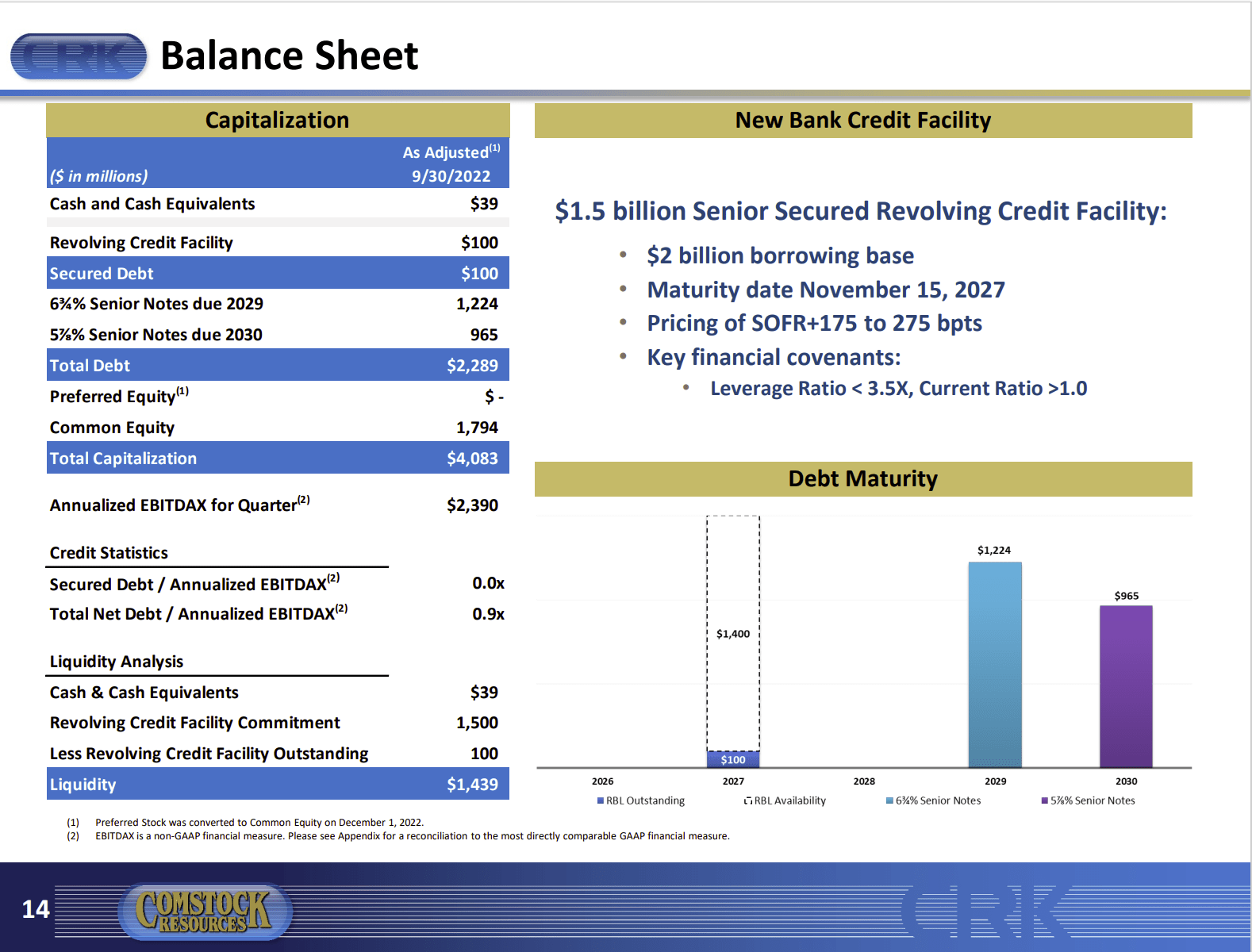

Comstock Resources Debt Profile, Capital Structure, And Key Debt Ratios (Comstock Resources Corporate Presentation January 2023)

This presentation demonstrates that with the latest quarter of robust pricing included in the debt ratio, that debt ratio is now satisfactory. The stock price has begun to respond accordingly. However, Mr. Market, and the debt markets want conservative balance sheet ratios at considerably lower prices. Hence the priority of continuing to repay debt.

This company may be able to refinance that debt at a better rate. But for the time being, management is satisfied with buying the debt to lower the absolute amount. That appears to be a darn good interest savings strategy in its own right.

It should be noted that the preferred stock has now converted to common stock (as shown above). Therefore, that senior claim to assets is now gone as far as common shareholders are concerned, as are any obligations of the preferred.

As management notes, the financial strength of the company has improved considerably from a few years ago. Clearly that improvement will continue. As it does, the competitive advantage of the company from its low operating costs will increase as interest costs decline. That should lead to even better financial performance during cyclical downturns in the future.

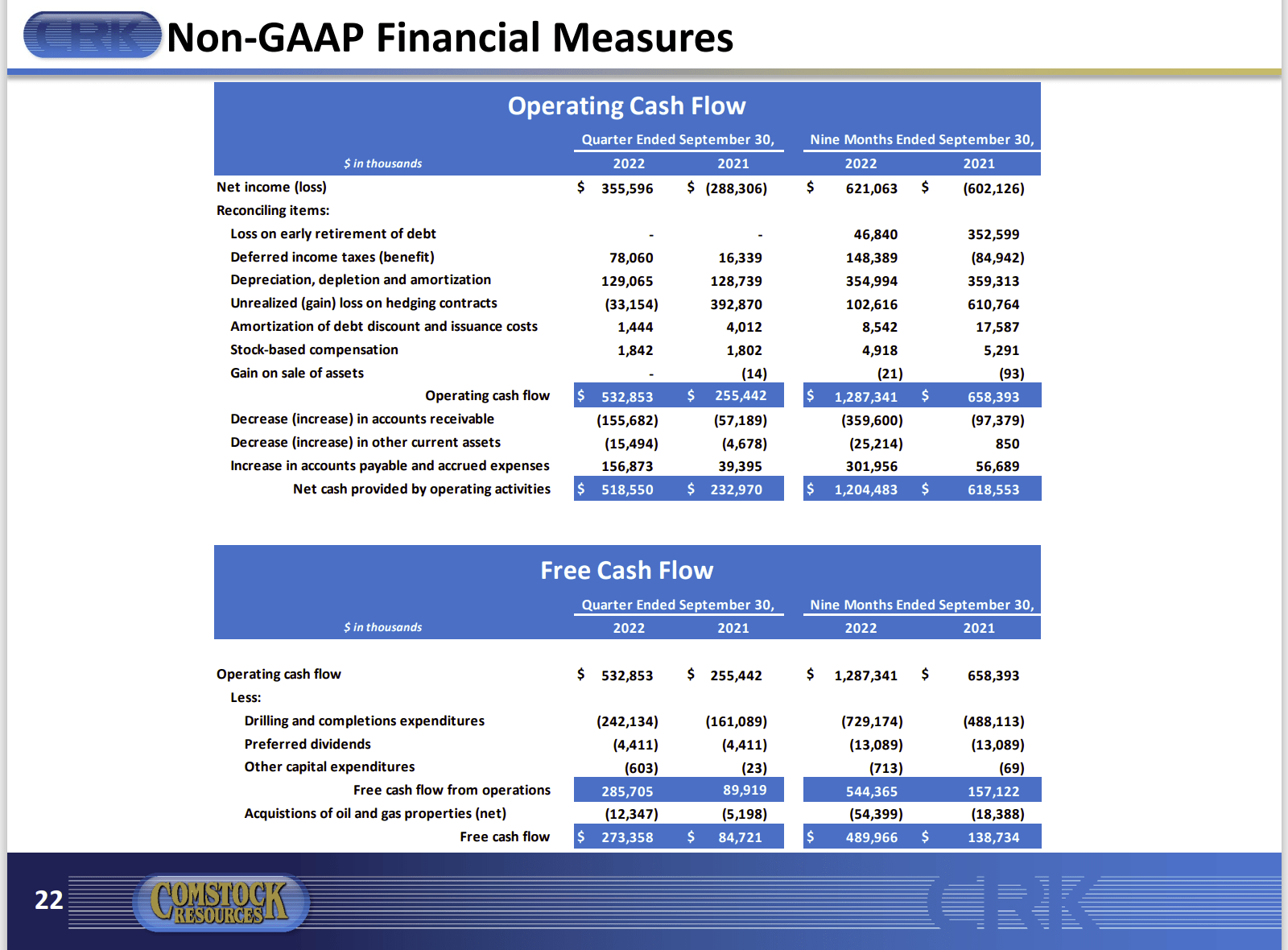

Comstock Resources Calculation Of GAAP Cash Flow And Non-GAAP Free Cash Flow (Comstock Resources Corporate Presentation January 2023)

Similarly, the low-cost structure allows for a relatively large percentage of free cash flow. As Comstock Resources, Inc. financial strength improves, the hedging policy will relax to allow the company to continue to increase participation in the robust commodity prices now available. Even if commodity prices do not increase, the relaxed hedging program in the future should allow earnings and cash flow to continue to grow.

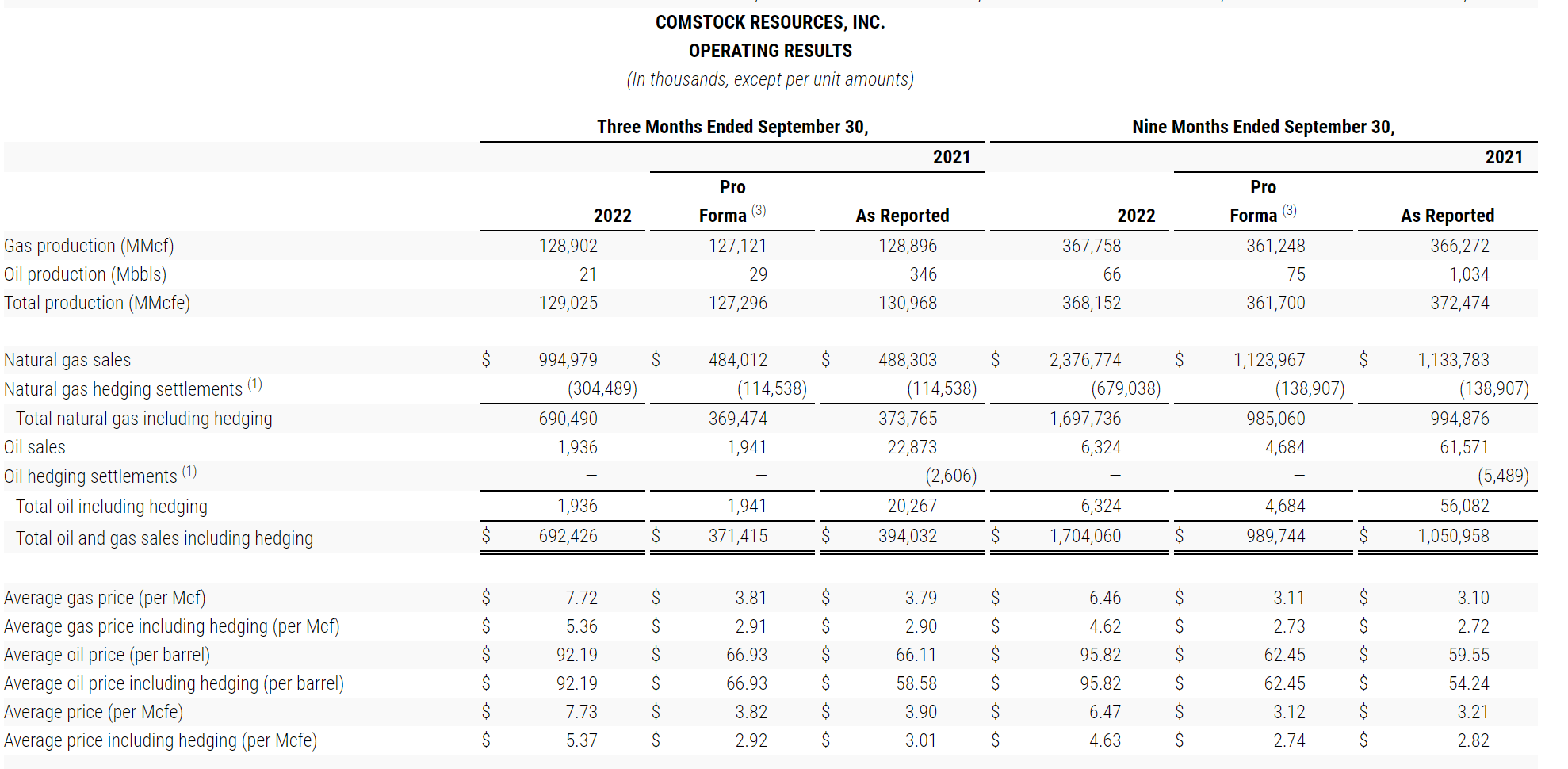

Comstock Resources Production And Selling Price Summary (Comstock Resources Third Quarter 2022, Earnings Press Release)

Management continues to grow the dry gas production. (Notice that the Bakken assets were sold. Hence the Pro-Forma column.) Some growth as well as an occasional acquisition should be expected for the foreseeable future.

This company is likely to remain a specialist in the basin it operates rather than diversifying to other basins. There are just not that many locations with the advantages of this basin. So, diversification would likely increase costs without increasing benefits.

That means that the future of the company will remain heavily dependent upon the price of natural gas. That is probably a good thing, because North America is increasing its capacity to export natural gas. That means that the price of natural gas will likely join the considerably stronger world pricing. The whole world of natural gas pricing circle is generally higher. A low-cost company like Comstock Resources, Inc. would profit quite a bit from such a pricing change.

The stock price has rallied quite a bit from its lows. But the valuation of Comstock Resources is still pretty cheap compared to its history. There would appear to be considerable upward potential as the ability to export natural gas increases over the next few years. Many natural gas stock prices do not reflect those potentially future stronger prices.

Probably the chief risks here would include a sudden and unexpected period of weak commodity prices before the debt reached optimal levels. The other possibility would be a risk of a technology improvement that causes another basin to become the low-cost leader.

Overall, the outlook is very good for the price of Comstock Resources, Inc. stock. A dividend has been initiated and will likely be increased as debt gets repaid. But Comstock Resources, Inc. management is likely to keep the base dividend at a level that can be maintained with considerably weaker commodity prices than are currently available.

Be the first to comment