JHVEPhoto

Financial stocks currently offer some of the best deals on the market today. While I see value in the big names like JPMorgan Chase (JPM), what often gets ignored are regional banks, which currently throw off higher yields and in some cases are way more undervalued.

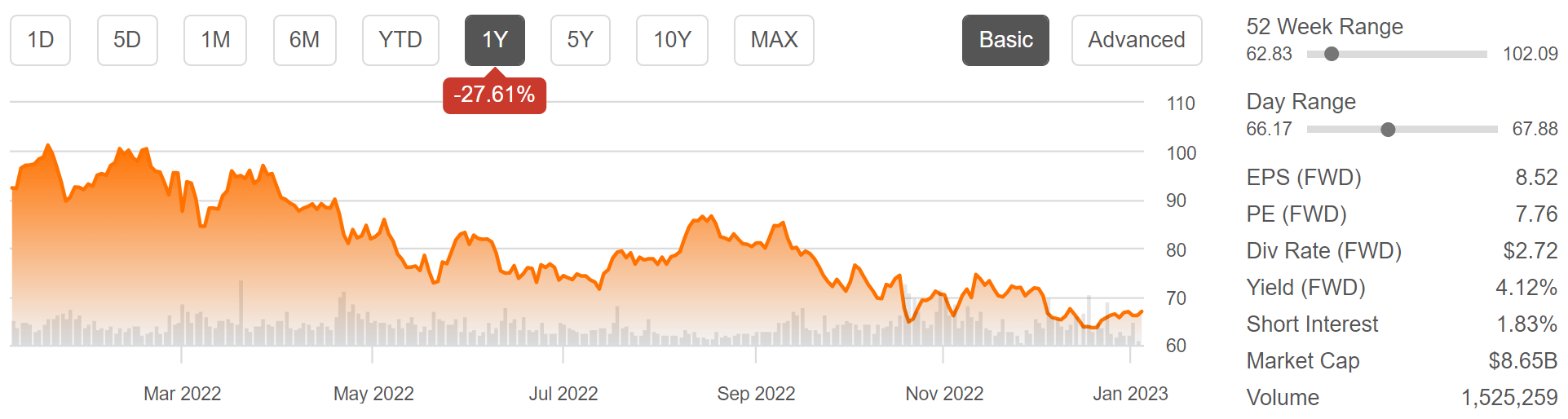

Such I find the case to be with Comerica (NYSE:CMA), which as shown below, has declined by 28% over the past year. At the current price of $66.89, CMA trades well off its 52-week high of $102, which investors willingly paid early last year. This article highlights why CMA is currently a good opportunity for value and income.

CMA Stock (Seeking Alpha)

Why CMA?

Comerica is a large financial services company based in Dallas, TX, that operates in the three business segments of commercial banking, retail banking, and wealth management. It has a long operating history, having been founded in 1849, and in addition to its home state, also operates in Arizona, California, Florida, and Michigan (where it was originally founded). Over the trailing 12 months, CMA generated $3.3 billion in total revenue.

Comerica is among the bigger beneficiaries of higher interest rates, especially considering a report that came out today stating that Fed officials see higher rates for “some time ahead”. Markets are now largely expecting another 50 to 75 basis point rate hike at the next meeting. CMA is well positioned to benefit from higher rates, due to its higher exposure to adjustable rate loans, as noted by Morningstar in its recent analyst report:

Comerica remains very leveraged to interest rates, as the vast majority (roughly 80%) of its loans are adjustable rate, making the bank one of the most interest-rate-sensitive names we cover. This, combined with the bank’s sticky deposit base from its core commercial clients, makes the bank ideally positioned for rising rates. The flip side of this business model is that the bank can be more pressured during extended periods of low rates. With a rising rate environment now on the horizon, Comerica should see its profits materially increase. We forecast Comerica will be one of the biggest beneficiaries of this rate backdrop.

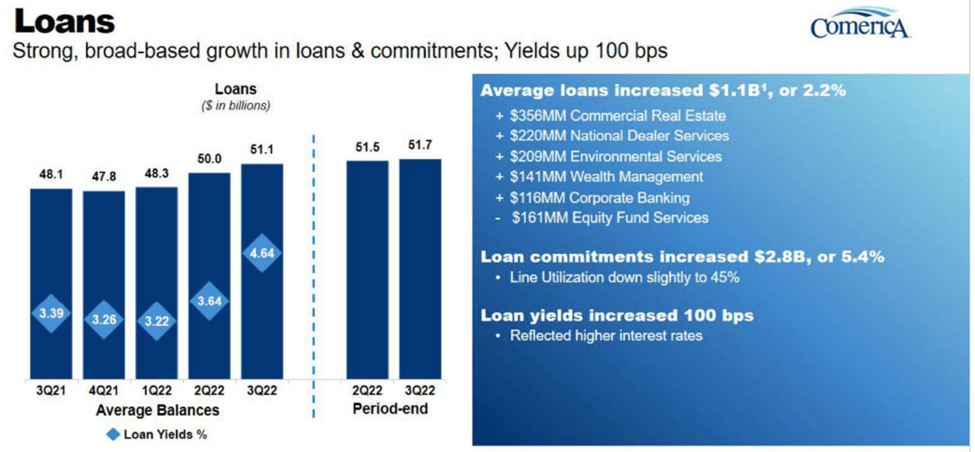

In addition to higher rates, CMA is also benefiting from loan growth, with 6% YoY growth to $51 billion in the third quarter. These factors contributed to 30% revenue growth YoY. As shown below, CMA’s loan balance has grown in 3 out of the past 4 quarters, driven by diversified segments across the bank.

CMA Loan Growth (Investor Presentation)

At the same time, CMA is seeing positive operating leverage, with its efficiency ratio (calculated as total expenses divided by revenue) declining to 51% from 61% in the prior year period. Credit quality remains solid, with a non-performing assets to loan ratio of 0.51%, down 11 basis points from the prior year period.

Potential headwinds to CMA include lower customer deposits, as customers shop around for higher rates at other banks. However, CMA’s loan-to-deposit ratio of 71% remains strong, and it remains well-capitalized, with a CET1 ratio of 9.92%, sitting well ahead of the minimum 4.5% required by the Federal Reserve and carries a BBB+ credit rating.

Another risk is the ability for customers to absorb higher interest rates. This was brought up during the Q&A session of the last conference call, and Chief Credit Officer stressed on its underwriting standards, as noted below:

I would say that, overall, we feel really good about our customers’ ability to kind of manage through the current interest rate environment. Every time we do an underwriting, we stress interest rates, whether we’re in a low rate environment or a high rate environment. And we think we do a really nice job of making sure that whatever the debt load is of the customer that they’ve got the ability to manage through that.

Meanwhile, CMA’s material price weakness has pushed the dividend yield up to 4.1%. The dividend is well-covered by a 36% payout ratio. While dividend growth has been non-existent since 2020, I would expect for growth to resume after the economic picture clears up.

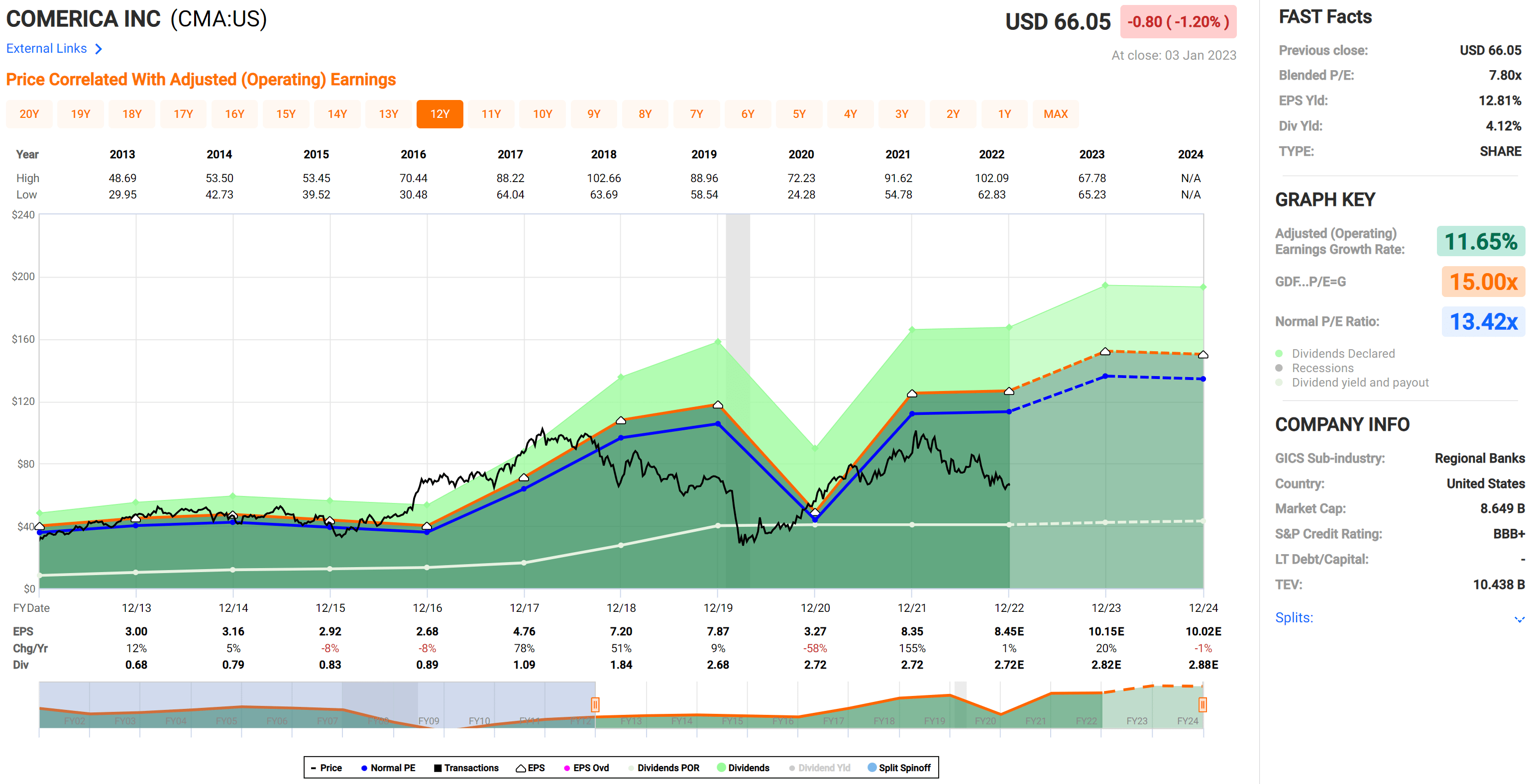

Turning to valuation, CMA appears to be undervalued at the current price of $66.89 with a forward PE of just 7.8, sitting well below its normal PE of 13.4. Raymond James sees value in the stock, giving it an Outperform rating, citing:

We see its strong capital/liquidity position, density in both attractive/stable markets, historically strong asset quality, and hedging strategy providing downside NIM/NII protection if/ when the Fed pivots.

Analysts estimate 15% EPS growth this year, and have a consensus Buy rating with an average price target of $82, translating to a potential 27% total return from the current price.

CMA Valuation (FAST Graphs)

Investor Takeaway

Overall, Comerica’s diversified segments, solid credit quality and loan growth are encouraging signs for the bank’s outlook. It’s well positioned to benefit from rising rates and maintains a strong balance sheet. Lastly, the stock is attractively valued and is trading well below historical norms. Income investors get paid a healthy dividend yield while waiting for the stock price to revert to its mean valuation.

Be the first to comment