SOPA Images/LightRocket via Getty Images

Cloudflare’s (NYSE:NET) growth rate deteriorated significantly in the third quarter of 2022, after two years of fairly consistent performance. This is a result of the macro environment, but further weakness could begin to undermine investor confidence in the business. Despite this, the company continues to innovate rapidly and is amassing a portfolio of complementary solutions that position the company for long-term growth. The path forward remains uncertain as tech spending weakened throughout 2022, but lower inflation and waning recessionary fears could lead to a more stable environment going forward.

Cloudflare recently released a digital experience monitoring solution to give insights into employee collaboration and productivity. Cloudflare Digital Experience Monitoring is a dashboard that provides information on how applications and Internet services are performing across an organizations network. This provides insights into application outages, network issues and performance issues that could impact employee productivity. At least 60% of I&O leaders are expected to use digital experience monitoring to measure application, services and endpoint performance by 2026, up from less than 20% in 2021. While this type of service may not be a meaningful revenue contributor in the near term, it highlights how Cloudflare’s network positions them to offer a broad range of services.

Edge Computing

Cloud computing has resulted in virtualization of existing infrastructure, rather than a rethink of computing in the internet-scale era. Instead of buying servers and installing operating systems, organizations must choose regions, provision virtual machines, and keep code artificially warm. Cloudflare aims to make scaling easy by removing the need to think about infrastructure. This can also potentially help to reduce costs by ensuring that resources are only consumed as they are needed.

At the end of the third quarter there were 2.2 million unique applications running on Cloudflare Workers. Cloudflare Pages also has 367,000 projects, doubling since May, and Cloudflare has over a million developers building on their Supercloud. This level of engagement has been achieved while Cloudflare is still introducing basic functionality to their Workers service. The R2 storage product was made generally available in September 2022, along with Workers KV and Durable Objects. Cloudflare’s first database product, D1, is currently in private beta and expected to enter public beta soon.

Cloudflare has stated that they are talking to large companies about utilizing R2 to save money on egress fees and utilize stored objects across different cloud platforms. The financial impact of storage solutions will be interesting to observe over the next 12 months, as it appears to have been the announcement of R2 in 2021 that made investors realize Cloudflare’s potential and kicked off a share price frenzy. Despite the hype around Cloudflare as the fourth hyperscaler, they remain a networking company, which comes with advantages and disadvantages. This should help them to rapidly achieve success in some areas, but it is not clear that they will ever reach the same sort of scale as AWS (AMZN) and Microsoft’s (MSFT) Azure.

To support growth of the Workers service, Cloudflare is working with 40 venture capital firms to finance startups built on the Workers service. Funding for the program was initially expected to be $1.25 billion, but grew to $2 billion on the back of strong investor appetite. It should be noted that this funding is being provided by VCs rather than Cloudflare, shielding Cloudflare from accusations that they are buying demand for their platform. There are 25 startups being funded initially, including a privacy firewall that seeks to address data privacy issues and a company that aims to speed up back-end development for front-end and mobile developers. The ultimate success of this initiative remains unclear, but it helps provide Workers with visibility and could lead to significant demand growth in the future.

Network Security

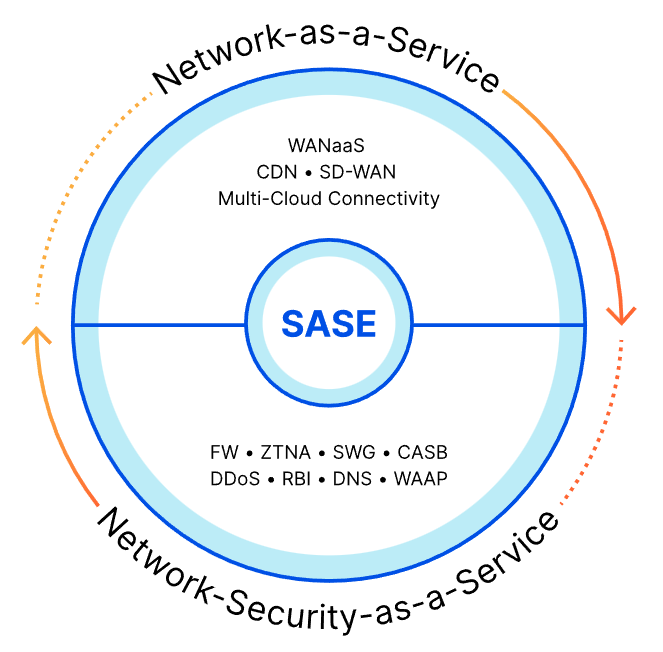

Network security is shifting towards a Secure Access Service Edge (SASE) model, led by companies like Zscaler (ZS) and Palo Alto Networks (PANW). SASE combines software-defined wide area networking capabilities with a number of network security functions, including:

- Secure web gateways

- Cloud access security broker

- Zero trust network access

- Firewall-as-a-service

The SASE model aims to enable employees to securely connect to an organizations network from anywhere and provide organizations with granular control over the traffic that enters and exits their network.

Figure 1: SASE Services (source: Cloudflare)

Cloudflare recently introduced Magic WAN Connector to make Cloudflare One a truly integrated SASE solution. Magic WAN Connector securely connects any network to Cloudflare’s global network. As part of Cloudflare’s One SASE solution, this allows for access to a full suite of security tools including Zero Trust Network Access, Data Loss Prevention, Intrusion Detection System and Cloud Access Security Broker.

There are only a handful of vendors currently able to offer a truly integrated SASE solution, with most vendors having to take a partnership approach to offer a full suite of solutions. It is expected that by 2025 around one third of new SASE deployments will be based on a single-vendor offering, up from 10% in 2022.

It is not really clear how Cloudflare’s security solutions stack up against Zscaler and Palo Alto Networks, but given Cloudflare’s differentiated network, they are likely to have advantages in at least some areas. Cloudflare recently highlighted how their forward proxy services are much faster than Zscaler’s. These products are part of Cloudflare’s Zero Trust platform, which helps secure applications and Internet experiences out to the public Internet. Cloudflare has estimated that the Cloudflare Gateway is 58% faster than ZIA, based on internal tests. Cloudflare Access is estimated to be 38% faster than ZPA worldwide, and Cloudflare Browser Isolation 45% faster than Zscaler Cloud Browser Isolation worldwide. Zscaler is quite dismissive of Cloudflare’s solution though, suggesting that they are not currently competitive.

Cloudflare also recently introduced a Zero Trust SIM for Mobile Devices to help secure corporate networks by securing every packet of data leaving mobile devices. Cloudflare will also be launching Zero Trust for Mobile Operators, a wireless carrier partner program that will allow any carrier to offer mobile security tools based on Cloudflare’s Zero Trust platform.

Financial Analysis

Cloudflare has been warning of a growth slowdown due to macro factors for the better part of a year, and this began to show up in their third quarter results. The macro environment didn’t change significantly through 2022 though, rather softness that was observed at the start of the year simply became apparent in the financial results.

The strong USD has also been a headwind in recent quarters, although the USD has weakened significantly over the past few months. Cloudflare bills in USD, which puts pressure on customers outside of the US but doesn’t directly impact their revenues. Cloudflare has made some concessions to help alleviate this pressure, continuing the company’s history of forgoing short-term performance to strengthen the business long-term.

From a geographic perspective, the US and EMEA have been performing relatively consistently, while APAC has improved relative to 2021 but is seeing more price sensitivity and buying decision delays. Cloudflare’s growth outside of these regions has also declined significantly over the past 12 months.

Cloudflare’s security business has been an area of strength, driven by increasing awareness of their solutions and geopolitical tensions. Cloudflare also recently earned FedRAMP Moderate Authorization which should be supportive of their growing government business going forward.

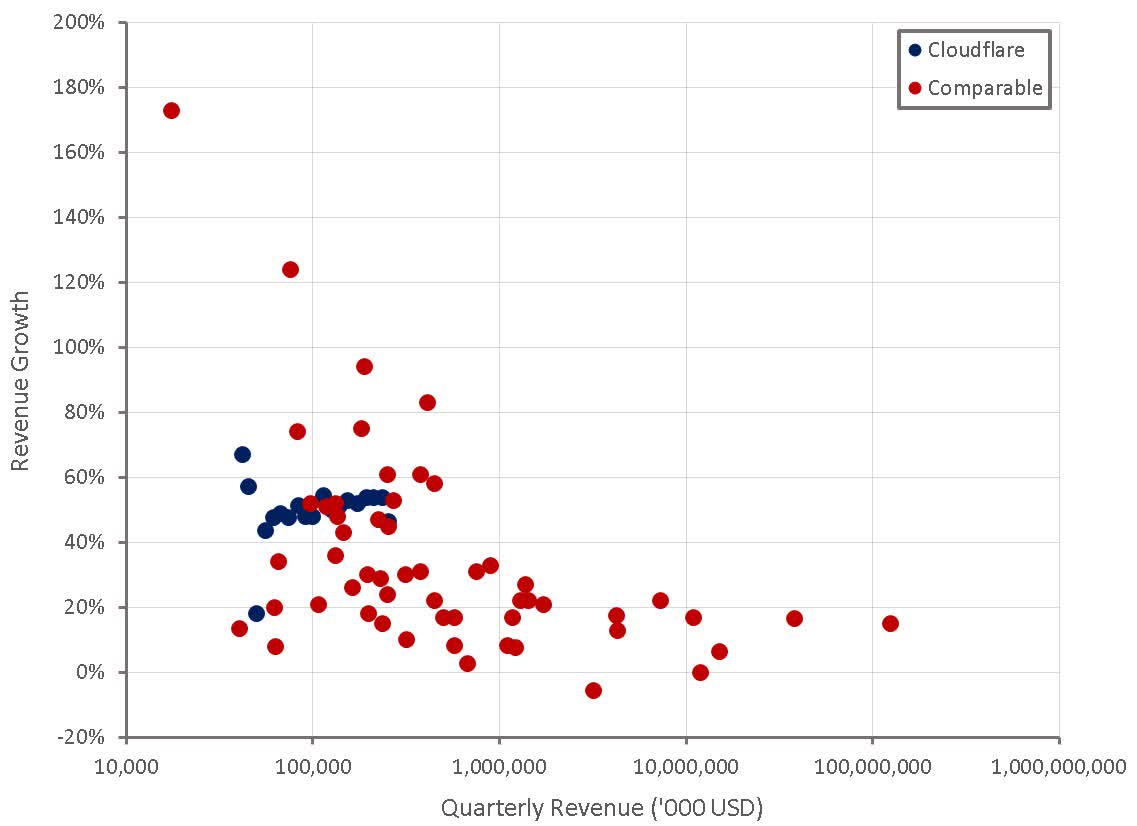

Cloudflare highlighted crossing $1 billion in annualized revenue during the quarter, something that only 6% of public software companies have achieved. This type of analysis is often used as an argument against cloud stock valuations, highlighting the low probability of companies reaching a certain size threshold ($1 billion ARR, $10 billion ARR, etc.). While there is some truth to this, it ignores the fact that these thresholds were reached in the past, when IT markets were significantly smaller. For example, Oracle (ORCL) crossed the $1 billion revenue mark in 1991. Directly comparing Cloudflare’s achievement to Oracle’s 31 years later makes little sense. Cloudflare reaching $5-$6 billion in annual revenue now would be more comparable to Oracle’s 1991 performance.

Cloudflare believes they have penetrated less than 1% of the market for their existing products and continue to innovate, driving expansion of their addressable market. The current growth slowdown should therefore not be over extrapolated, as it is clearly due to macro factors rather than Cloudflare approaching market saturation. Cloudflare continues to target $5 billion in annualized revenue within the next five years, a figure that only 1% of public software companies have achieved so far.

Figure 2: Cloudflare Revenue Growth (source: Created by author using data from company reports)

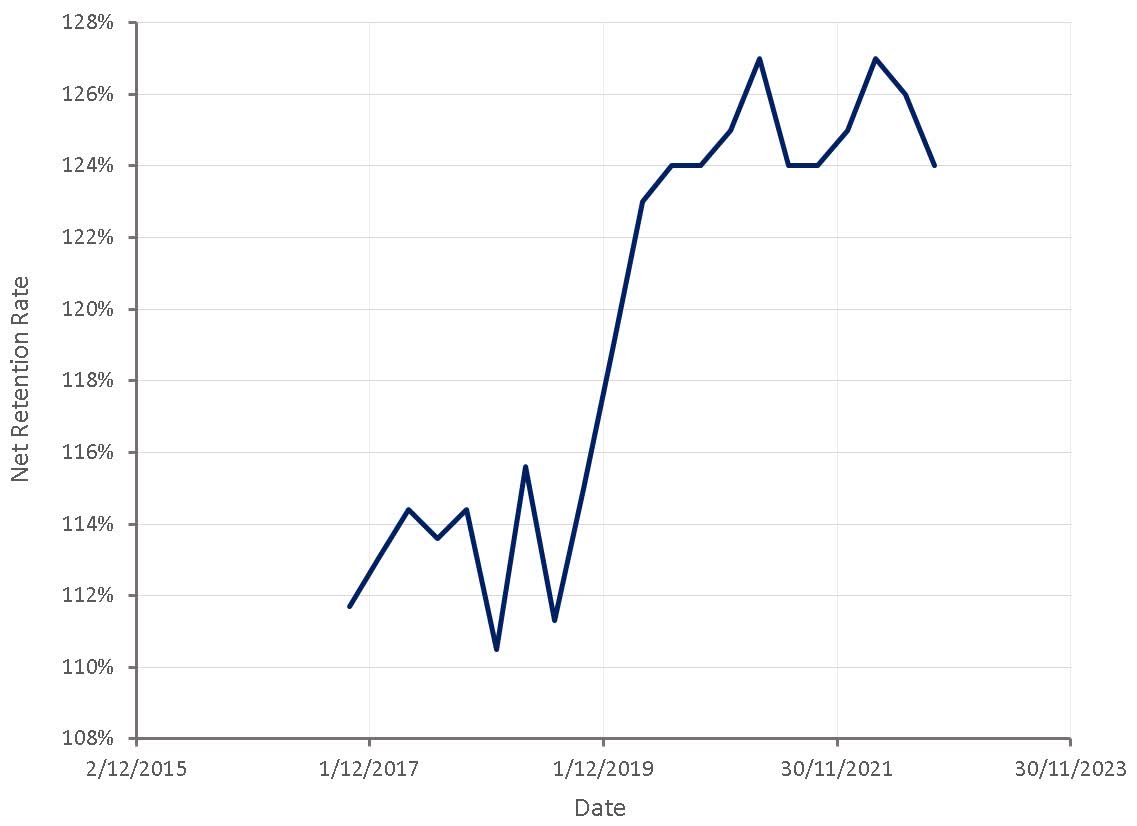

Cloudflare’s dollar-based net retention rate has been fairly stable over the past few years in the 124-127% range, compared to an internal target of greater than 130%. Cloudflare believes this is achievable through the addition of seat and storage-based products like Zero Trust and R2. Given Cloudflare’s rapid product innovation, the net retention rate would ideally have continued expanding over the last 1-2 years, but in the current environment stability is reasonable.

Figure 3: Cloudflare Net Retention Rate (source: Created by author using data from Cloudflare)

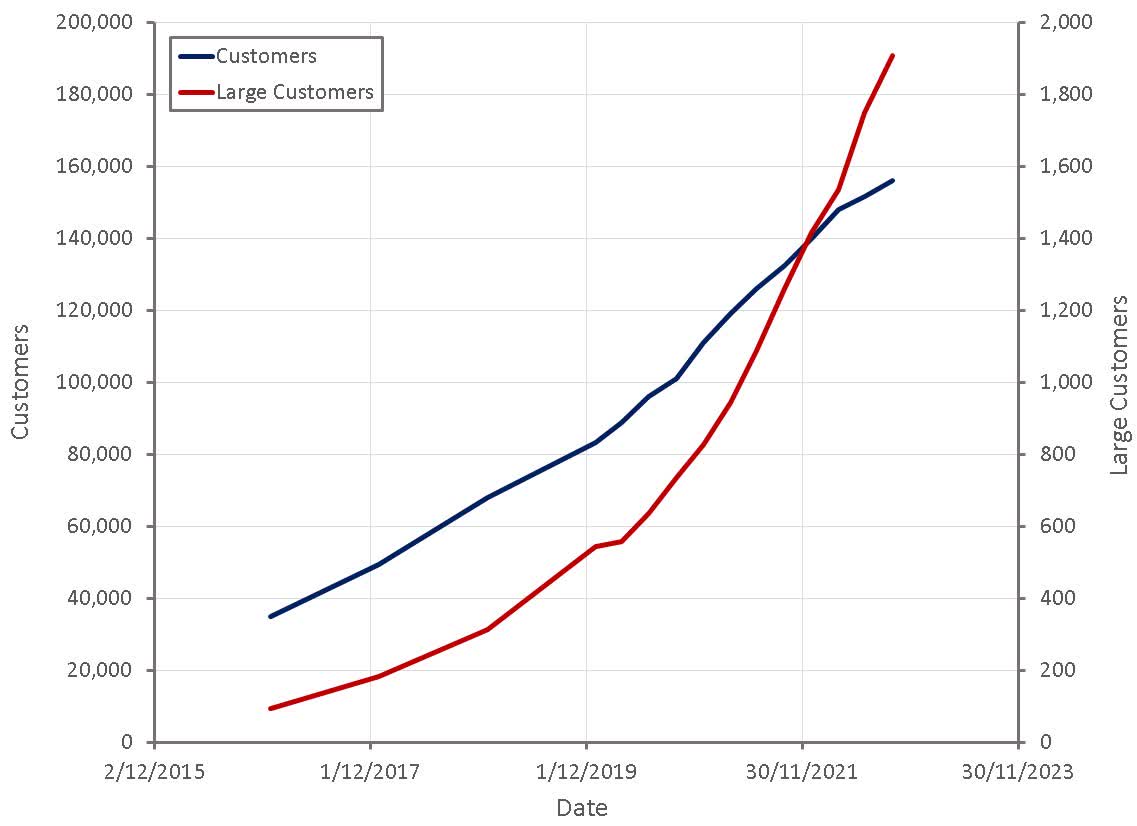

Customer growth has slowed significantly over the past two quarters, although this is primarily due to smaller customers. Part of this deterioration is due to PAYG customers trading down to the free tier. Sales cycles are also elongating amongst very large customers and expansion in the mid-market segment has slowed.

Growth of customers generating in excess of $100,000 revenue annually continues to be robust, and these customers now account for 61% of Cloudflare’s revenue. The number of customers spending over $500,000 annually grew 88% YoY in the third quarter, and customers over $1 million grew 63%. These figures highlight Cloudflare’s march upmarket and their growing portfolio of solutions. Only 32% of the Fortune 500 are currently Cloudflare customers, leaving significant growth for expansion amongst larger customers.

Ideally customer additions will accelerate in 2023 as this is a driver of long-term growth, but in the near-term expansion within the existing customer base and the addition of large customers are arguably more important.

Figure 4: Cloudflare Customers (source: Created by author using data from Cloudflare)

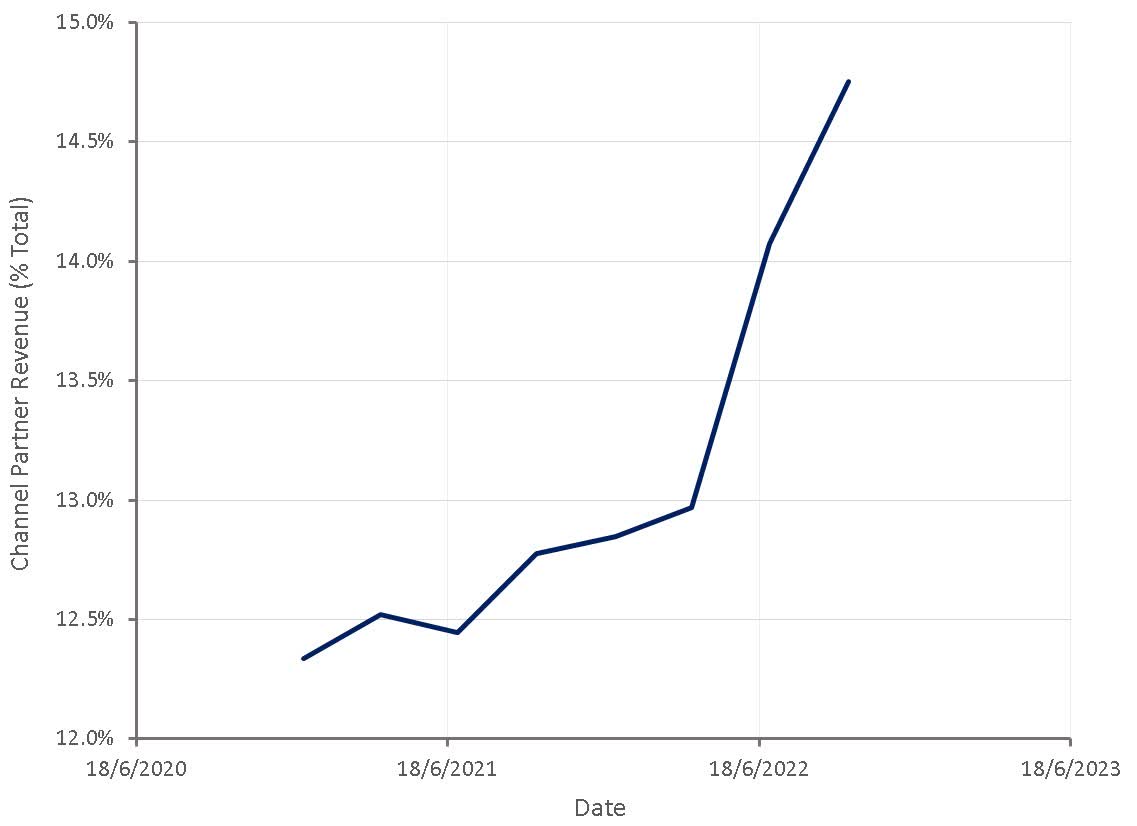

Channel partner revenue is rapidly becoming a more important part of the business. Cloudflare highlighted their channel strategy on the third quarter earnings call, with the Zero Trust space a particular focus. Win rates against Zscaler and Palo Alto Networks continue to be strong in this market, although Cloudflare believes they still need to raise awareness of their products.

Figure 5: Cloudflare Channel Partner Revenue (source: Created by author using data from Cloudflare)

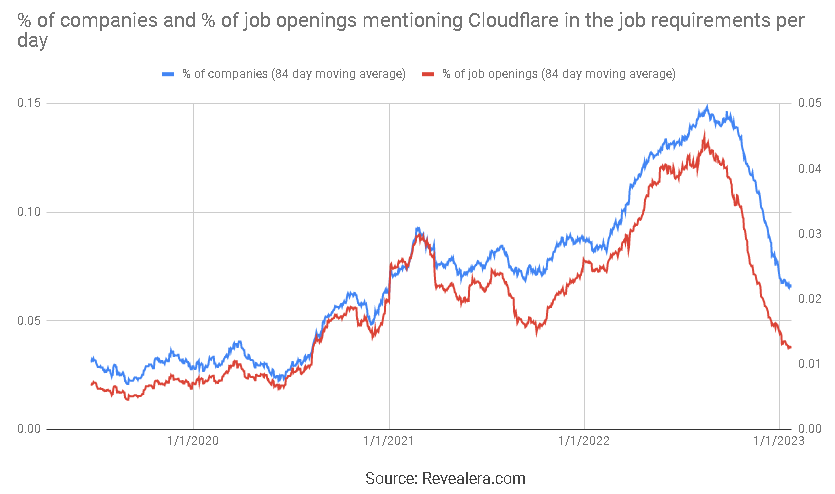

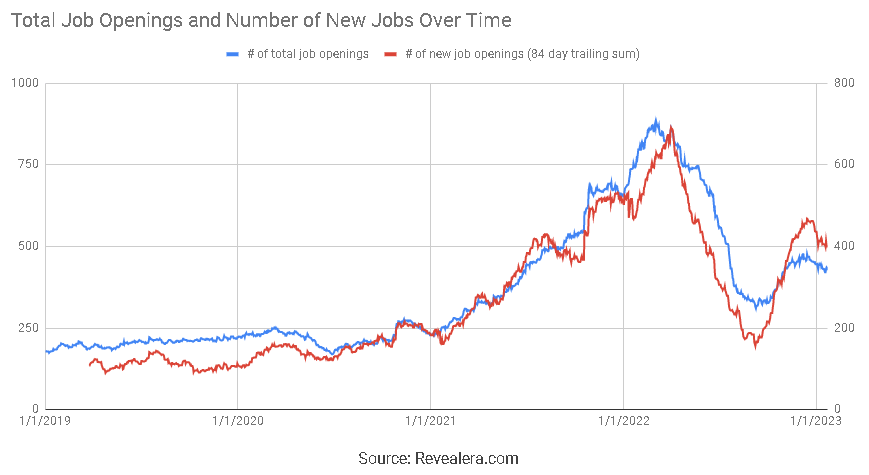

The number of job openings mentioning Cloudflare declined significantly in the second half of 2022, which could indicate further weakness in coming quarters. This is difficult to ascertain though, due to Cloudflare’s shift upmarket. Large customer growth may offset broader weakness to a considerable extent.

Figure 6: Job Openings Mentioning Cloudflare in the Job Requirements (source: Revealera.com)

Cloudflare’s gross margins have deteriorated slightly in recent quarters, which is another indication of pressure on the business. Gross margins should be stable or increasing as Cloudflare introduces higher value services, but this is possibly being offset by lower network utilization and customer incentives.

Figure 7: Cloudflare Gross Profit Margins (source: Created by author using data from company reports)

Operating profit margins continue to be fairly stable and are likely to remain so going forward. Cloudflare has shown a commitment to continue investing in the future of the business, holding margins down in a similar manner to Amazon. This is unlikely to be appreciated by investors in the current market, but provided these investments continue to efficiently generate growth it is a positive.

Figure 8: Cloudflare Operating Profit Margins (source: Created by author using data from company reports)

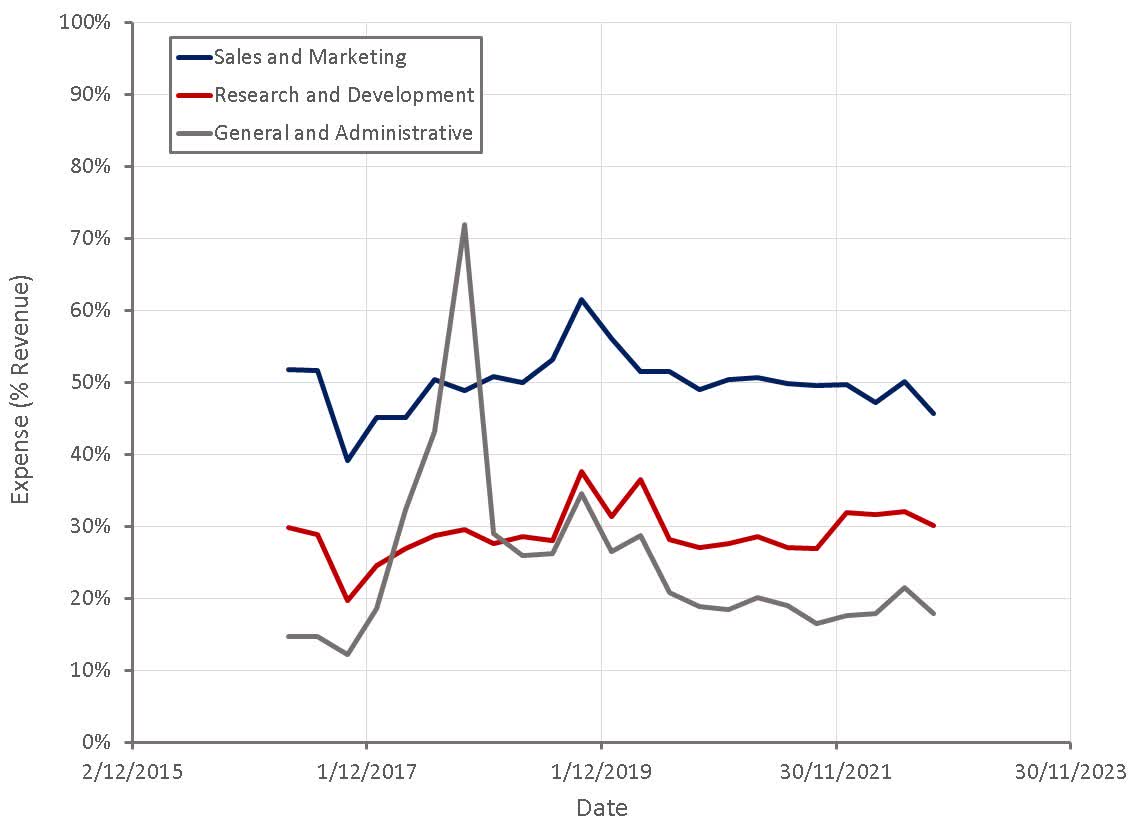

Figure 9: Cloudflare Operating Expenses (source: Created by author using data from Cloudflare)

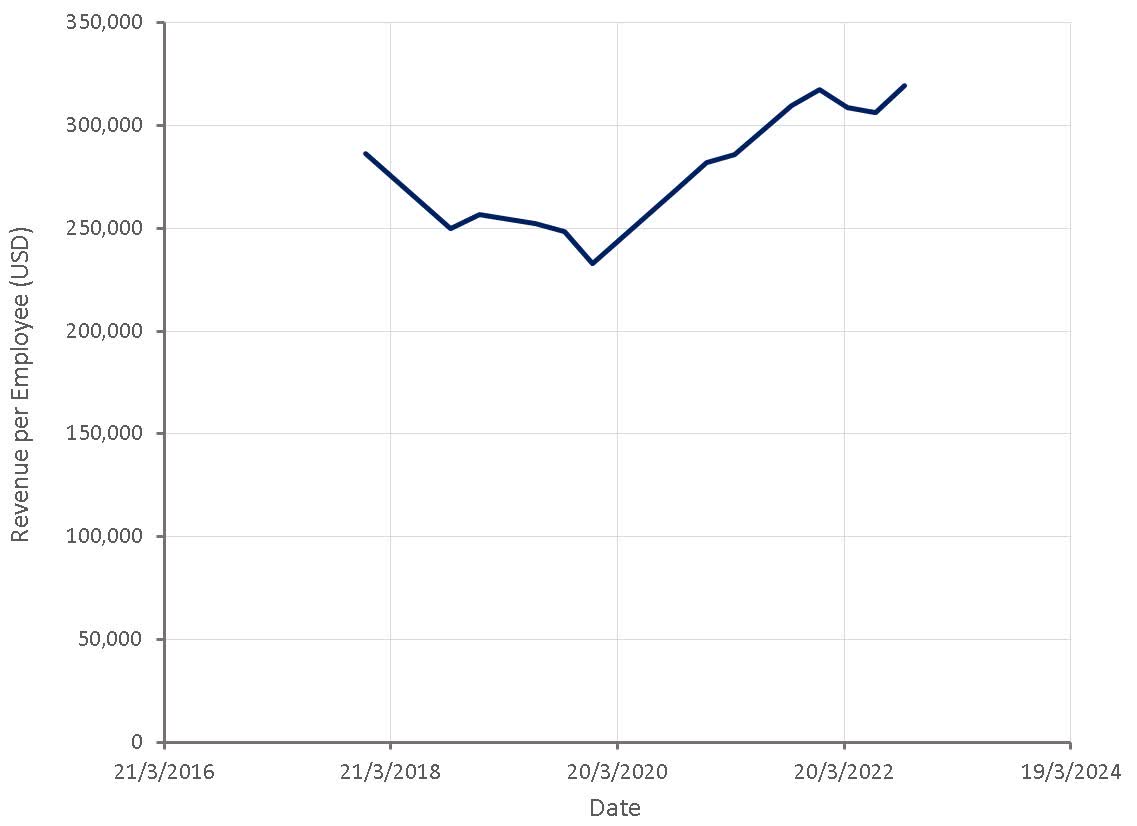

Figure 10: Cloudflare Revenue per Employee (source: Created by author using data from Cloudflare)

Cloudflare’s job openings fluctuated substantially through 2022. Cloudflare has stated that their pace of hiring is based on current market conditions, which could indicate that the environment is now far more favorable than it was in September.

Figure 11: Cloudflare Job Openings (source: Revealera.com)

Valuation

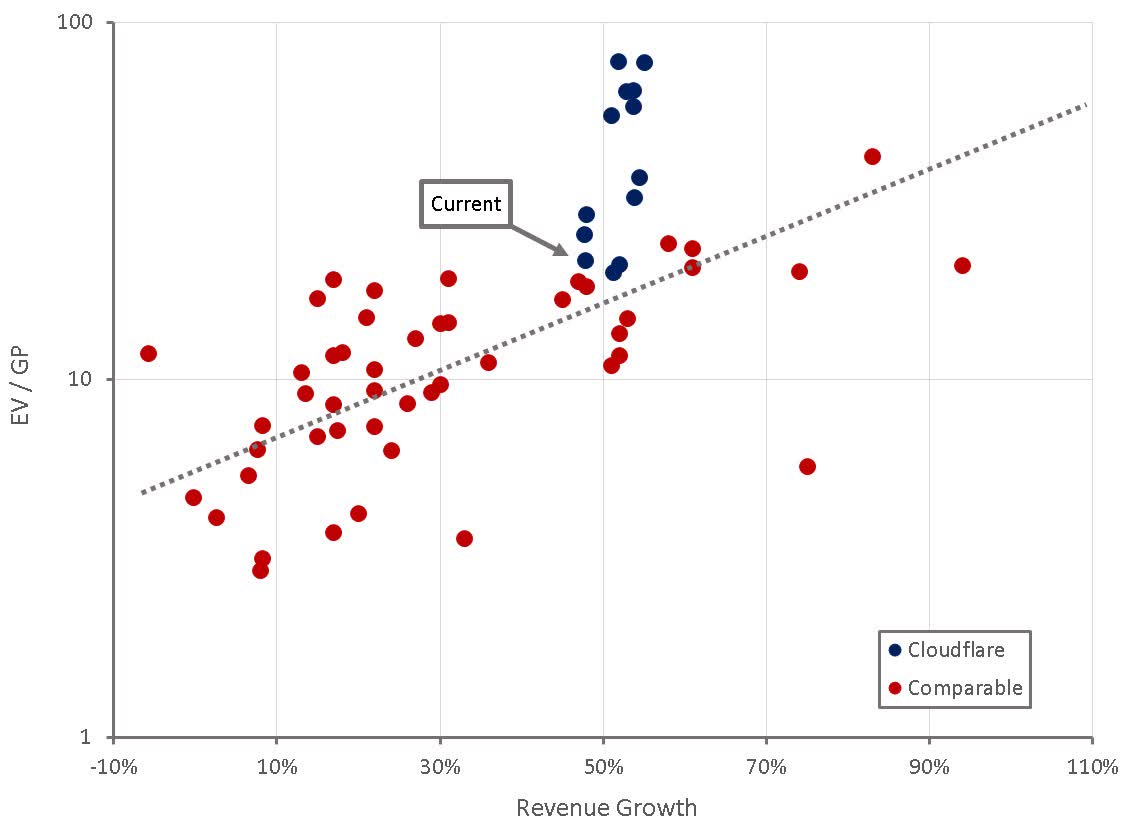

Cloudflare’s stock now appears more reasonably valued than it has in the past, but is still expensive relative to peers. Cloudflare’s current financial performance alone doesn’t really justify their valuation premium. It is based more on an understanding of the optionality the company’s network provides and the company’s strong execution.

Figure 12: Cloudflare Relative Valuation (source: Created by author using data from Seeking Alpha)

Conclusion

Further deterioration in Cloudflare’s growth rate is likely to pressure the stock price, bringing the company’s valuation more into line with peers. While growth may remain under pressure in 2023, declining inflation rates and less fear of a recession could lead to IT budgets stabilizing. Regardless of short term performance, Cloudflare remains well positioned for long term success, particularly if the Workers service continues to gain traction.

Be the first to comment