FeelPic

Investment Thesis

The Clorox Company (NYSE:CLX) is facing headwinds from softening macro environment and supply chain disruptions, which is impacting its volume. In addition, post-COVID, the demand for its products started to moderate, impacting revenue growth. Looking forward, current macro headwinds are a concern in the near term. In the medium to longer term, the revenue should benefit from the company’s IGNITE strategy focused on delivering long-term organic growth, and easing supply chain disruptions. Margins should benefit from price increases along with the company’s cost-saving initiatives. While I believe the company should deliver growth in the medium to long run, it’s already priced in valuation with the stock trading much above its historical P/E levels. Hence, I have a neutral rating on the stock.

Revenue Outlook

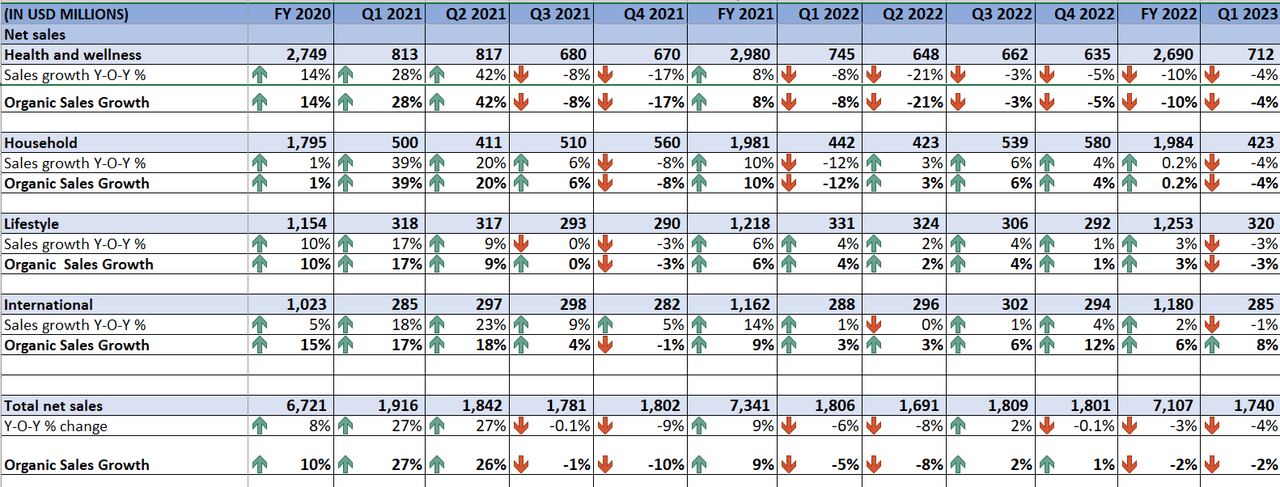

During the initial phases of the pandemic, Clorox experienced a surge in demand for its Cleaning and Disinfectant products. The company’s net sales growth benefitted in fiscal 2020 and fiscal 2021 as a result. However, post-COVID, the demand for its products started to moderate, affecting sales growth. The company is facing headwinds from supply chain issues, tough comparisons from the prior year’s surge in demand for Cleaning and Disinfectants, demand elasticities associated with price increases, and adverse FX. This has resulted in sales decline in FY2022 and Q1 FY2023.

CLX’s Historical Revenue Growth (Company Data, GS Analytics Research)

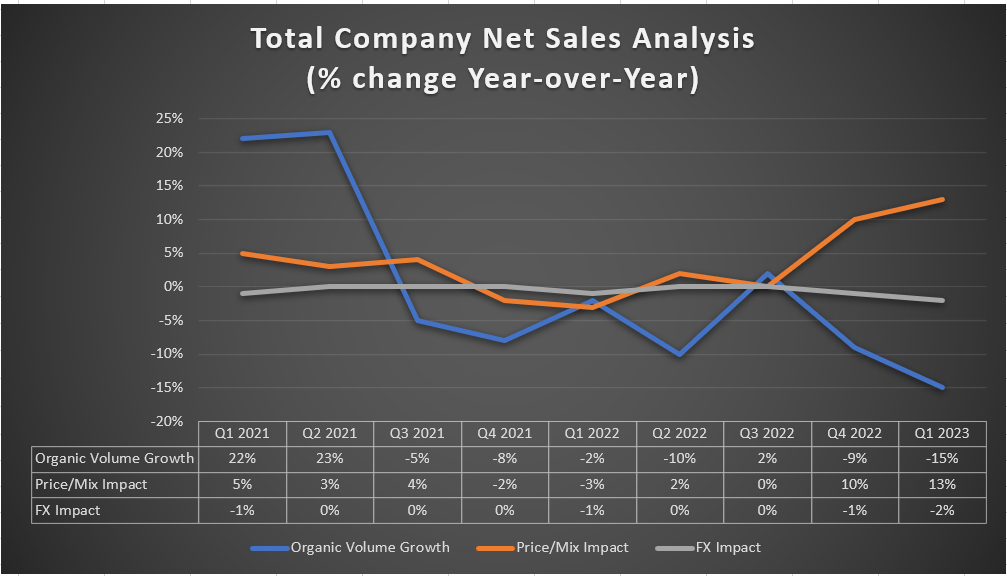

CLX’s Historical Net Sales Analysis (Company Data, GS Analytics Research)

Looking forward, I believe current macro headwinds should continue to impact revenue growth in the near term adversely. The company implemented an additional pricing increase in December to offset inflationary costs. This price increase may negatively impact volume due to unfavorable demand elasticities associated with pricing. The near-term results, especially Q2 FY2023, should also see a headwind from a volume decline from the impact of a voluntary recall of certain Pine-Sol scented products due to quality issues. Further, supply chain disruptions should also continue to be a near-term revenue headwind.

So, I am not optimistic about the near-term revenue growth prospects. My view is at variance with some bullish investors who think that there remains a chance of multiple Covid waves continuing at regular intervals (like the one we are seeing in China), which should help CLX’s near-term results. While I agree with their view that we may continue to see new mutations and future Covid waves, I don’t think CLX might see a similar revenue uplift from these waves as it has seen during the panic in the initial post-Covid period. The new variants of Covid are more infectious, but the mortality rate is lower than delta or initial variants, especially in the vaccinated population. In my opinion, these variants will likely end up like the flu or the common cold, and people will get used to them. So, the extra precautions people took due to the panic in the previous waves might not recur, and we might not see a significant jump in CLX sales during future Covid waves. We saw something similar during the Omicron outbreak in the U.S. around the same period. While the number of Covid cases made a new peak a year ago, CLX’s Health and Wellness segment didn’t see any boost and posted a decline in organic sales during that period (refer to Q2 and Q3 2022 segment organic sales from the CLX historical revenue growth table above.)

The company’s medium to longer-term revenue growth prospects looks slightly better. The current supply chain disruptions are unlikely to continue forever and should eventually ease. That’s one less headwind for the sales.

CLX’s IGNITE strategy should also support sales growth in the medium term. The strategy focuses on making significant investments in its brands. The company’s brand holds the No.1 or No.2 market share positions in their category. The No.1 and No. 2 market share positions help the company save on excessive marketing spending and focus on R&D to support new product innovations. These product innovations help in further market share gains and attract demand for its products. The company launched new products in more than 25 categories in FY2022. In addition to gaining market share through new product innovation, the company also announced a significant investment in digital infrastructure under this strategy in August 2021. This investment is focused on replacing Clorox’s more than 20-year-old enterprise resource planning system (ERP) with a cloud-based advanced ERP platform. This should help in modernizing the company’s digital infrastructure to leverage consumer data to gain insights for innovations and brand building for the longer-term growth of the company. Management has indicated their longer-term organic sales growth target of 3-5% which is achievable.

However, it is not going to be that easy a path, and I believe management will have to eventually make a choice between topline growth and margin expansion. While brand investments and innovations under IGNITE strategy are important sales drivers, the company must also be careful about its price point and price differential versus its peers to make sure it is able to maintain or grow its market share.

One of my worries is that management might be overestimating CLX’s ability to raise prices without losing market share in the current environment. I understand management’s compulsion to raise prices as the company’s margin has corrected meaningfully in recent years due to cost inflation. However, we are transitioning from a very strong demand environment during COVID to a slowing consumer spending environment. I believe significant price increases during this period are a risky proposition and may lead to market share loss against competitors if these competitors don’t follow up with equally steep price increases.

In my experience, market share usually takes priority over margins for any consumer company. So, if management has to choose between revenue growth and margins, I believe they will likely choose the former and go easy with price increases. This makes me optimistic about the company’s ability to achieve its low to mid-digit long-term organic sales growth target. However, it also makes me a bit skeptical about the pace of margin recovery which I have discussed in the next section.

Margin Outlook

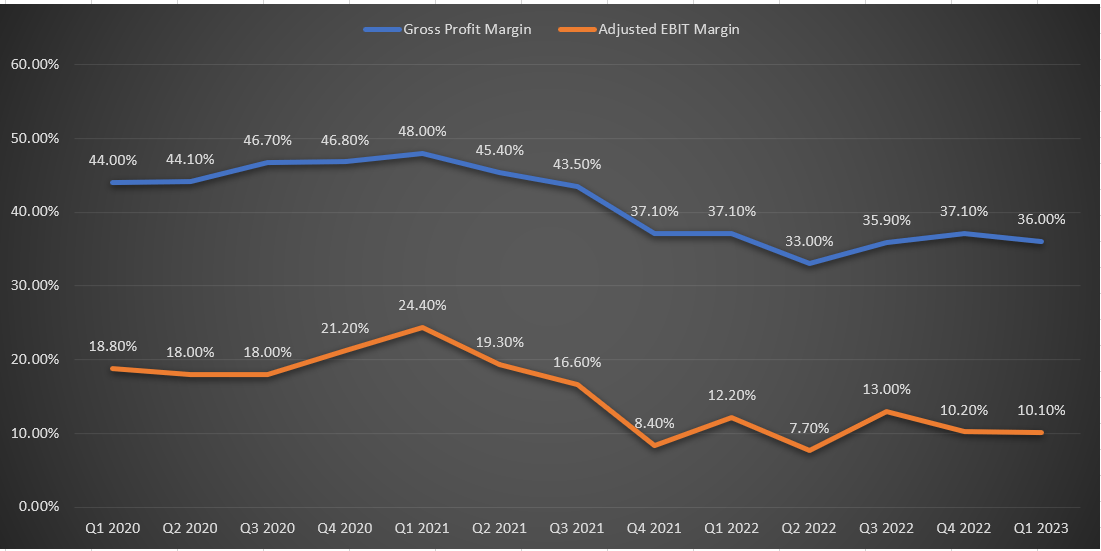

Clorox’s gross margin has declined meaningfully from the pre-pandemic levels. This significant decline was due to inflationary pressure (particularly with higher commodity, manufacturing, and logistics costs), volume deleverage, and higher investments by the company in digital infrastructure.

CLX Historical Gross Profit Margin and Adjusted EBIT Margin (Company Data, GS Analytics Research)

Looking forward, I believe the current macro headwinds are a concern in the near term, as the company expects cost inflation of $400 million this fiscal year. This is over and above the ~$800 mn cost increase seen last year.

To improve margins, the company launched a streamlined operating model at the beginning of the fiscal year 2023 under its IGNITE strategy. The new model aims to reduce costs by $75-100 million, with benefits beginning in the second half of the fiscal year 2023. As a part of this initiative, the company plans to reduce headcount and decentralize decision-making at the lower level to respond quickly to changing consumer behaviors and efficiently save costs through the supply chain. Moreover, the new ERP system should also help in reducing the unnecessary cost associated with the supply chain.

However, in my opinion, the real problem here is not the bloated operating cost structure but the cost inflation. With the company seeing ~$1.2 bn cost inflation in FY22 and FY23 combined, there is little $75 or $100 mn cost cuts can do in terms of taking margins to prior levels. The only way to improve margins to pre-pandemic levels is by increasing prices significantly. But as mentioned in the prior section, it is not going to be an easy task in this weakening demand environment.

Don’t get me wrong. I am not saying margins will not improve from here. Given the current margins are significantly below pre-pandemic levels and management is willing to raise prices, there is a good chance that they will improve. It is just the pace and extent of recovery where I am conservative.

If we look at sell-side numbers, they are estimating 28.24% Y/Y growth in EPS in FY24 and 19.74% Y/Y growth in EPS in FY25. The Y/Y revenue growth in both these years, according to consensus estimates, is around 3%. This indicates their EPS growth estimates are relying on significant margin expansion. Management has also shared their goals to regain CLX’s gross and adjusted EBIT margins to pre-pandemic levels i.e. 43-44% and 18-19%, respectively.

I don’t think sell-side estimates or management’s margin goals are achievable over the next few years as that would mean significant product price increases continuing, which is difficult in the current weakening demand environment.

Valuation and Conclusion

The Clorox Company is currently trading at 34.92x FY2023 consensus EPS estimate of $4.13. This is a premium versus its 5-year historical average forward P/E of 26.97x. Before the pandemic, CLX was trading at a P/E multiple in the low 20s. I believe investors are building in expectations of a significant margin increase over the next few years. That is why they are giving the company a significantly higher than usual P/E multiple. Most of the margin improvement seems to be already priced in the stock at these valuations. While I agree that the business fundamentals will bottom in the current fiscal year and see recovery beyond FY23, the pace and extent of recovery may disappoint some bulls limiting the potential upside. Also, while EPS should increase in the medium term, P/E multiple is likely to compress resulting in the stock trading sideways. Further, there are near-term headwinds that may impact the short-term results over next couple of quarters. I would like valuations to correct, near-term headwinds to fade and sell-side expectations on margins to reset before becoming more positive on the stock. For now, I have a neutral rating on the stock despite medium-term revenue growth and margin expansion prospects.

Be the first to comment