Vladimir Zapletin

Instead of an investment thesis

I published my first article on Cleveland-Cliffs Inc. (NYSE:CLF) on June 1, 2021. Since then, my coverage has grown by another 8 articles – now you are reading my 10th piece.

CLF stock did not become the fastest-growing company in its industry – on the contrary, it lagged behind its major peers in terms of total return as it didn’t pay any dividends. However, all along, the company had some characteristics that kept me coming back to it, again and again, to cover here on Seeking Alpha. If we add up the changes in CLF quotes since I started reporting on it, we end up with +3.53% versus a -0.91% decline in the S&P 500 Index (SPX) over the same period. Small, but still an advantage.

Based on the company-specific characteristics, as well as recent reports from key peers, I again rate CLF a Buy. I think investors should take a closer look at the company ahead of its Q4 2022 earnings release as it could easily beat Mr. Market’s expectations.

My reasoning

Cleveland-Cliffs Inc. is the leading producer of flat steel sheets and iron ore pellets in North America, and a significant supplier – the largest one – to the automobile industry. The company operates a fully integrated production process, starting with raw materials from mining and continuing through the production of iron, steelmaking, and the finishing stages such as stamping, tooling, and tubing. It was formerly known as Cliffs Natural Resources but changed its name in 2017. Cleveland-Cliffs was established in 1847 and is based in Cleveland, Ohio, with 26,000 employees.

Thanks to a series of successful acquisitions and the subsequent integration of the acquired companies into a single vertical structure, Cliffs has grown its revenue (TTM) by 900% from the beginning of 2019 to date; over the same period, EBITDA and net income – both TTM – grew by 469% and 116.5%, respectively. At the same time, the company’s market capitalization has grown 362% over that period – about 3.6x and >2x more than the market caps of United States Steel (X) and Nucor (NUE).

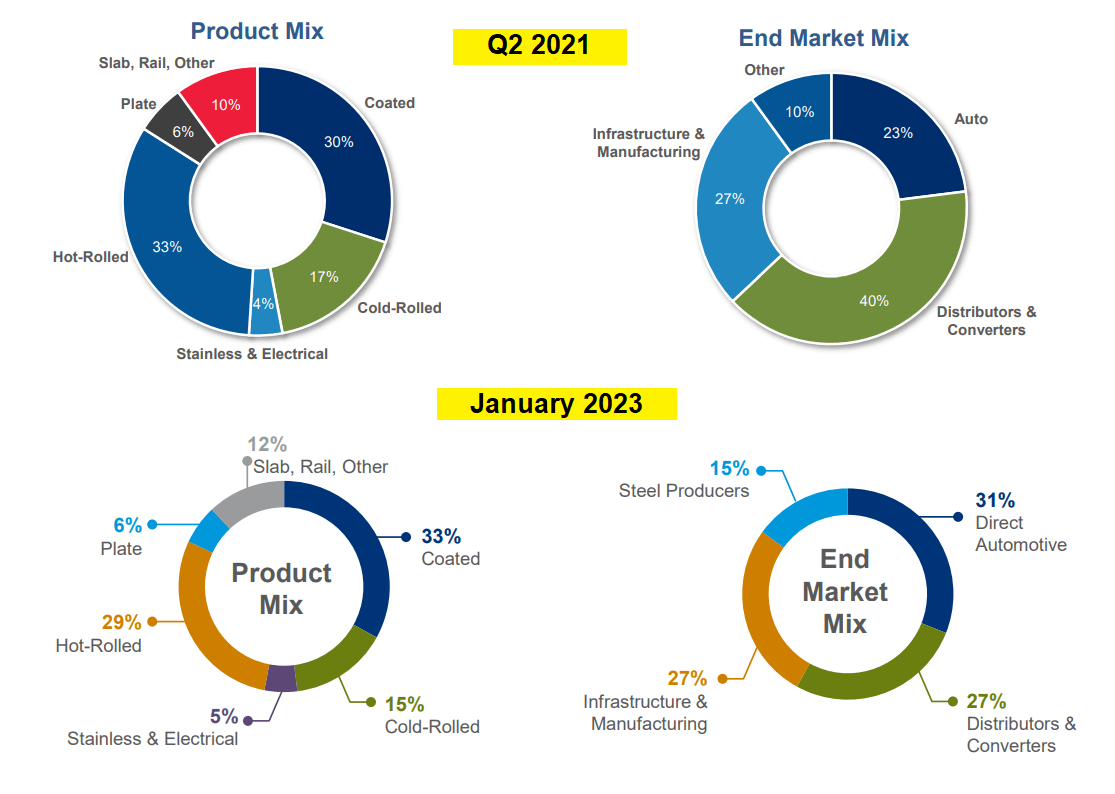

The last 4-5 years have become truly transformational for the company – this can be seen even in the way the revenue structure and addressable markets have changed since mid-2020:

Author, based on CLF’s IR presentations

Hot-rolled and coated steel together still account for over 60% of total sales, but the company is now less dependent on cold-rolled steel and somewhat more on slabs, rails, and other. CLF’s end-market mix has changed much more drastically: the share of sales to the automotive market has increased from 23% to 31%, while the distributors & converters as of January 2023 accounted for only 27% compared to 40% 2 years ago. Cliff has started to specify the former segment “Others” – now it is called “Steel Producers” and contributes 5% more to the firm’s consolidated sales.

Given the automotive industry and its greater importance to the company, I believe Cliffs may surprise everyone on February 14 – the date of the planned Q4 2022 report.

For 4Q FY2022, General Motors (GM) announced its total revenue and non-GAAP EPS were $43.1 billion and $2.12, respectively, surpassing the expected results of $40.0 billion and $1.69 set by FactSet. GM’s automotive revenue of $39.8 bn (up 3% QoQ and up 31% YoY) compares to Goldman Sachs’s previous estimate of $37.8bn.

Using the same proprietary data of GS, let’s take a look at Ford’s (F) results. The firm reported 4Q FY2022 total company revenue of $44.0 bn (up 12% QoQ and up 17% YoY), above Goldman’s $42.1 billion estimate and the Street’s (FactSet) $41.4 billion. At the same time, Ford’s automotive revenue (including mobility) was $41.7 billion (up 12% QoQ and up 18% YoY), above Goldman’s estimate of $39.9 billion.

From what I have seen from the major U.S. auto companies, volume is up year over year – especially at General Motors. In addition, on Nov. 28, Cliffs raised spot market prices for all hot-rolled, cold-rolled, and coated carbon steel products by at least $60 per ton.

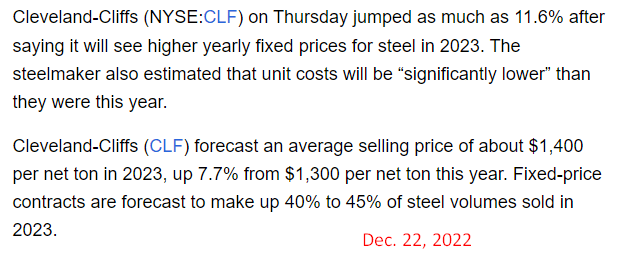

This was followed by another price increase in mid-December and another announcement in late December that Cliffs will see higher yearly fixed prices for steel in 2023.

SA News, author’s note SA News, author’s note

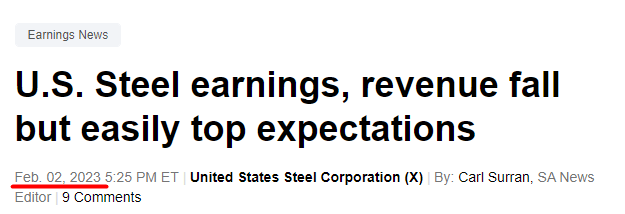

In addition to a potentially stronger automotive market in Q4 2022 than just a few months ago, we have results from critical companies like Nucor and United States Steel. As Goldman Sachs wrote in a recent note, large investors are quite bullish on Cliffs after X’s quarterly results:

We continue to see investor preference for integrated producers over the mini-mills, particularly given the rising steel price environment the greater operating leverage. Investors remain cautiously optimistic on CLF on potential for the company to deliver better-than-expected cost performance. While we noted a relative increased focus on CLF over X, the 4Q22 print from US Steel last night left investors with greater confidence around the business outlook for 2023, given seemingly strong cost control among the Flat Rolled business, improving European demand outlook and performance and a potential bottom in Mini Mills high-cost inventory challenges.

Source: GS [February 3th, 2023], emphasis added by the author

And indeed – despite the fact that both companies reported a sharp decline in sales and net income (YoY), they significantly beat market expectations for Q4 2022:

SA News, author’s notes SA News, author’s notes

At the same time, both companies remained profitable. Commenting on last quarter’s results, Nucor said it expects the profitability of its steel mills to improve in Q1 2023 from the previous quarter due to higher margins and volumes, with the biggest improvement expected at its sheet mills. In turn, X said Q1 2023 would mark a “trough” for the market, although a mild recession is very likely in late 2023.

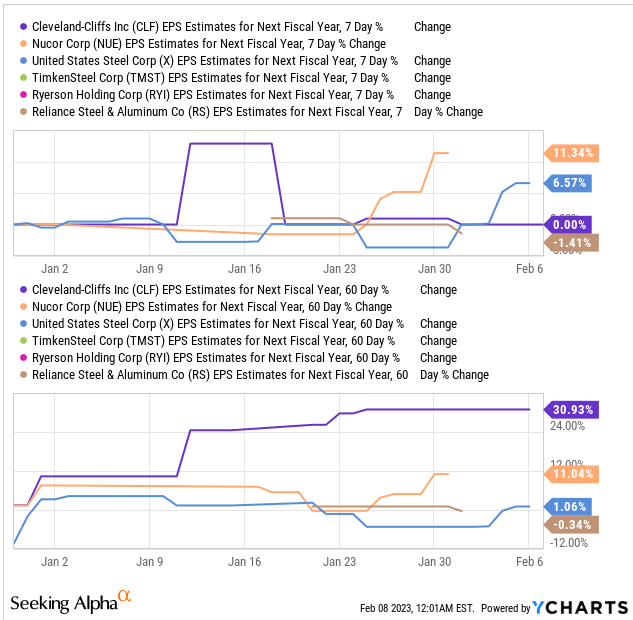

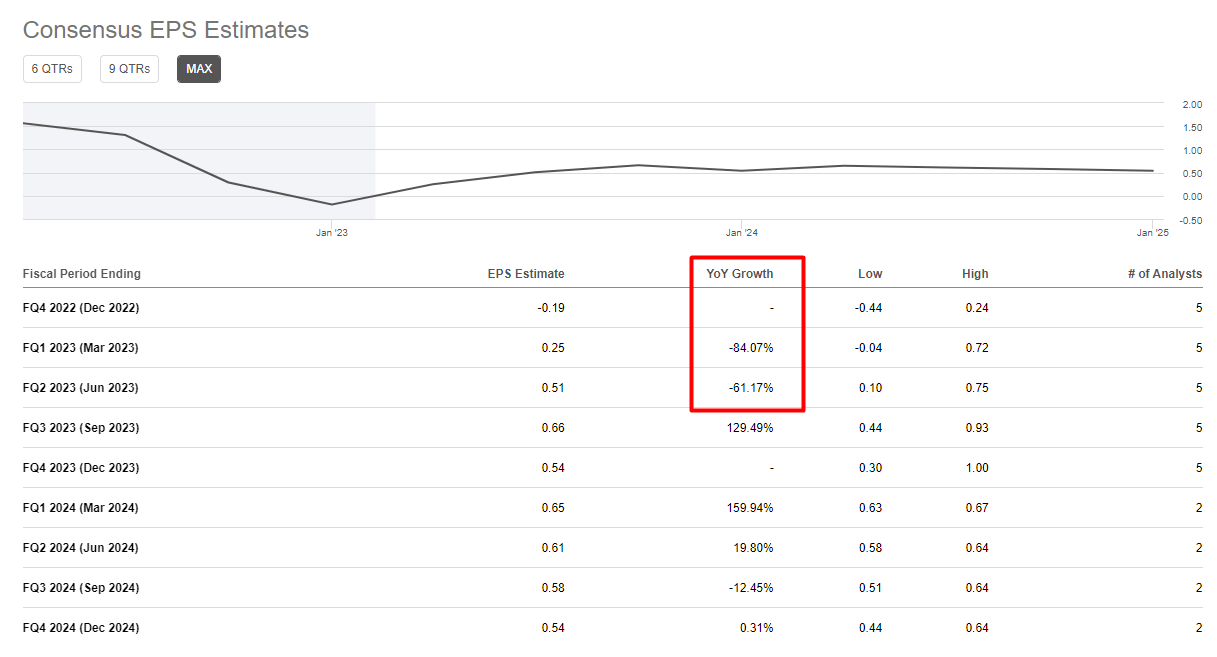

Against this background, it is interesting to see how analysts’ expectations for CLF’s EPS have changed in 2023:

YCharts, Seeking Alpha

After NUE and X released their results and expectations for FY2023 and upcoming quarters, analysts’ consensus estimates for EPS in the next fiscal year rose sharply. However, CLF’s forecast remained unchanged – that’s logical because Mr. Gonsalves has yet to speak. Once he does, I expect estimates to be revised upward – that would be a positive sign for CLF stock and its shareholders.

In general, the upward revisions in CLF were most noticeable in the last 30 days, but at the same time, according to Seeking Alpha, we will continue to see a sharp decline in EPS numbers in the coming quarters:

Seeking Alpha, CLF, author’s notes

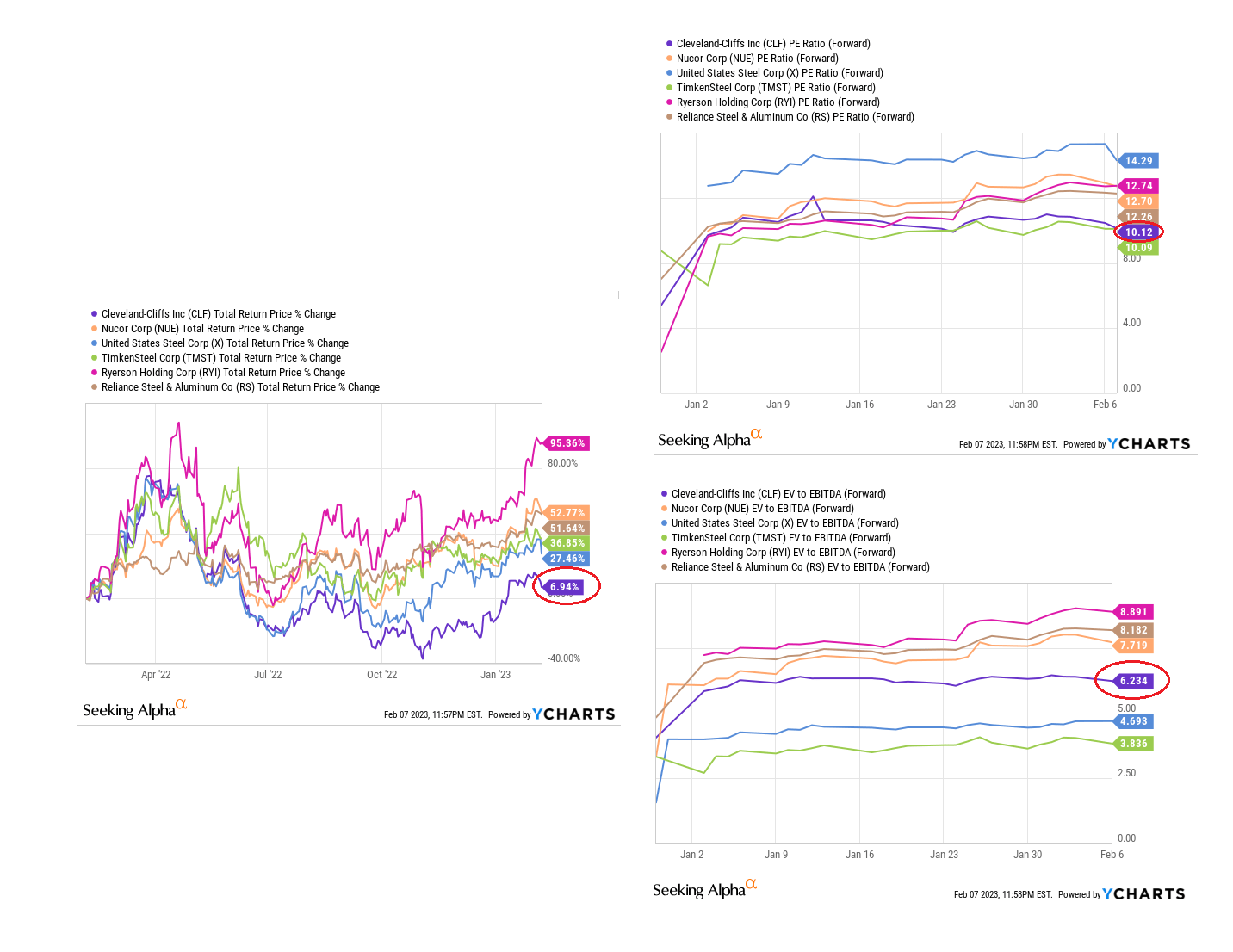

Please note that analysts are predicting negative EPS for Q4 2022. Most likely it will be so – the company’s margin was not the highest compared to United States Steel or Nucor. However, there is a chance that CLF will remain profitable if its net profit margins decline in the same manner as Nucor in Q4. This is unlikely, and it would be too optimistic to hope for this now. However, if it does happen – in the most bullish case – CLF could soar and close the performance gap between some of its nearest peers quite shortly. Incidentally, the underperformance of CLF stock over the past year has made the company quite cheap compared to its peers in the sample below:

YCharts, author’s notes

Without expecting too much from the company in Q4, I still hope that a) the CEO gives a strong outlook for FY2023 and b) the negative EPS will be easily beaten thanks to improving conditions in the auto market and analogous to what we have seen recently at NUE and X.

Risks to consider

You should note that Cleveland-Cliffs is currently a very risky investment due to a number of factors that suggest a high vulnerability to a substantial pullback soon. First and foremost is the company’s lagging marginality, which has been a persistent issue for Cliffs in recent years. Despite the company’s strong financial performance, it has struggled to achieve the kind of margins that its peers in the steel industry are able to generate. This suggests that the company may be facing headwinds in terms of its competitiveness and ability to generate meaningful returns for investors.

The other risk is macro. The global economy is currently experiencing a period of growth and stability, but this could change quickly if a number of negative factors come into play. For example, the ongoing trade tensions between the US and China, as well as the threat of a sudden downturn in the global economy, could all contribute to a slowdown in demand for Cleveland-Cliffs’ products. This, in turn, could put pressure on the company’s earnings and financial performance, making it a much riskier investment for investors.

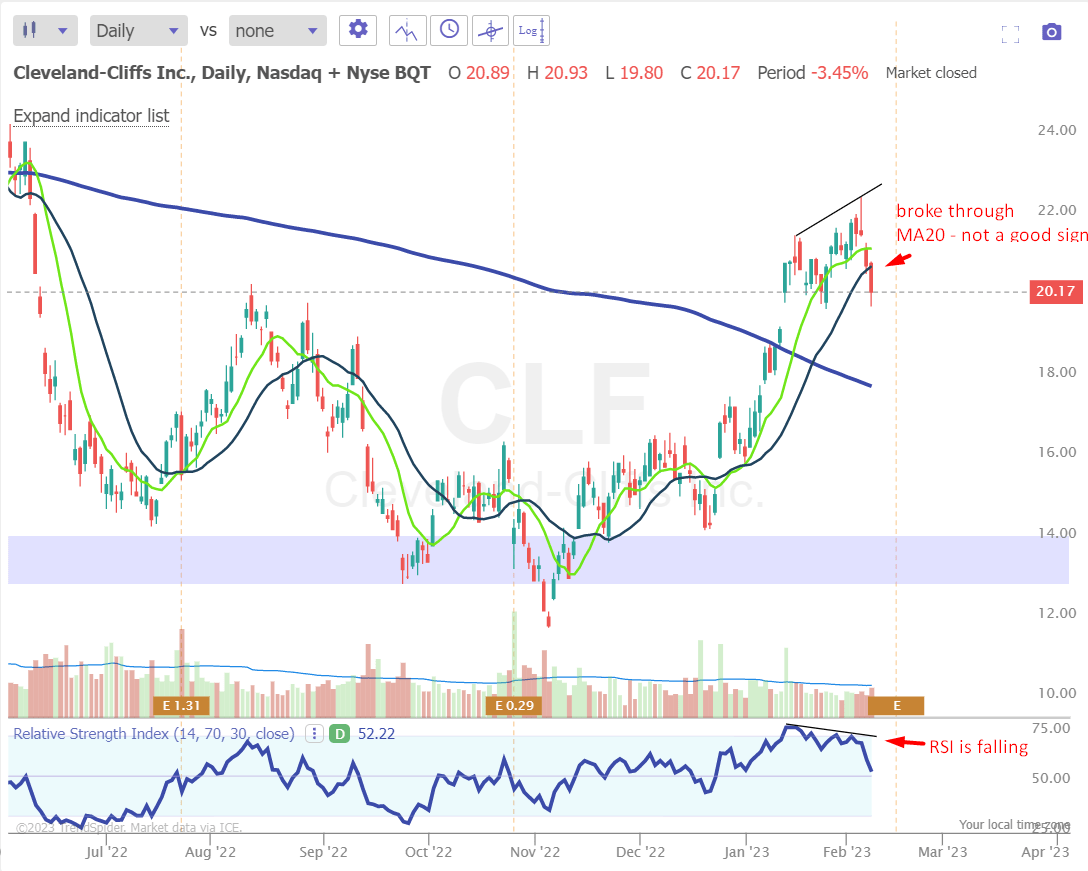

Finally, the overbought technical conditions – based on RSI divergence – on the daily chart for Cleveland-Cliffs are also causing concern.

TrendSpider Software, CLF, author’s notes

The stock has been on a tear in recent months, but this upward momentum may not be sustainable in the long term. The overbought conditions on the daily chart suggest that the stock is ripe for a pullback.

Quick conclusion

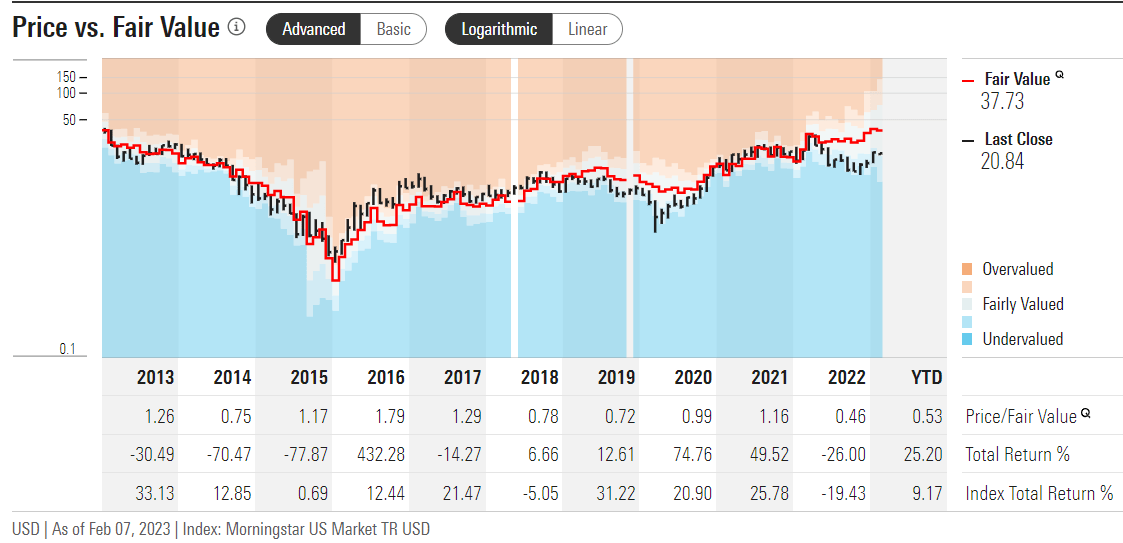

Despite all the risks, I still expect CLF to please its shareholders in the upcoming Q4 2022 release based on peers’ results and improving auto market conditions. The underperformance we have seen over the past year has created a valuation gap, not only relative to its closest peers, but also based on intrinsic value as indicated by the Morningstar system.

Morningstar, CLF

I rate Cleveland-Cliffs stock as a Buy again. My price target is $26 per share, which is based on a P/E of 10x and EPS of $2.6 for the full-year 2023, based on Argus Research’s estimate [proprietary data]. This PT implies an upside potential of 29% to yesterday’s closing price.

Be the first to comment