sbayram/E+ via Getty Images

Investment Thesis

Cleveland-Cliffs (NYSE:CLF) is in the steel-making business. And steel-making stocks have been on fire in the past six months.

Here I make the argument that Cleveland-Cliffs has three catalysts that will propel its stock higher in 2023.

That being said, I acknowledge one notable risk that investors should also be mindful of.

Investing in Steel, Better Than Tech

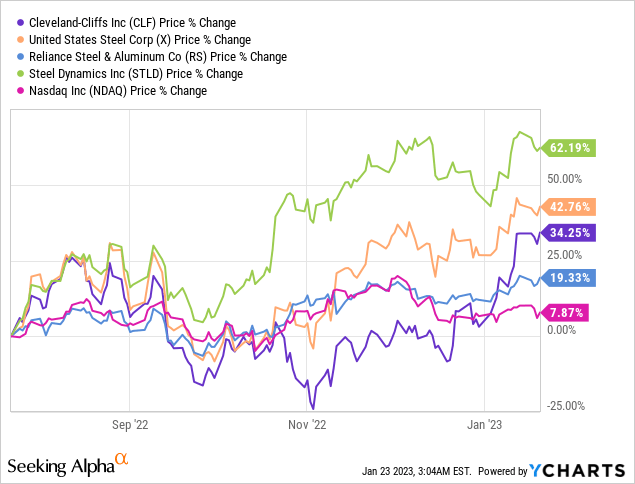

In the graphic that follows, you can see a basket of steel stocks.

Keen followers of mine will know that I own U.S. Steel (X), and in hindsight, X wasn’t the best-performing stock in steel. Nevertheless, anyone that has invested in steel in the past six months has outperformed the S&P500 (on average).

And you didn’t need to go back in time and pick the best-performing steel stock at the lowest price point of the last six months. Simply being long steel companies to the best of my knowledge, you’d have beaten the Nasdaq average.

And as a value investor, I feel some level of vindication. Why? Because it shows that even if over the past five years, value investing has been out of favor, as soon as interest rates moved beyond abnormally low rates, it makes sense to be a stock picker and think about companies’ underlying prospects.

Put another way, it wasn’t just about the best story. But about strong and growing profits.

But What About the Bear Case?

As investors, we find it all too alluring to be compelled by stories. And investment stories work, because there’s enough of a grain of truth to them, that they often enough become a self-fulfilling prophecy. At least in the short term.

Here’s what steel investors are concerned about. That, in 2023, there’s going to be a recession. This so-called recession was ”supposed” to hit the US in late 2022. And then, it got pushed out to early 2023. Now, it’s been pushed back to late 2023.

Economists are so feverishly attempting to forecast with a high degree the oncoming recession, that it appears to me that the steel investors have already long ago factored in this outcome and moved on.

So, what’s driving steel demand?

The Bull Case for Cleveland-Cliffs

There are three catalysts driving the upside for Cleveland-Cliffs.

- The great energy transitions

- Chinese real estate finding its footing

- US competitors have an energy moat

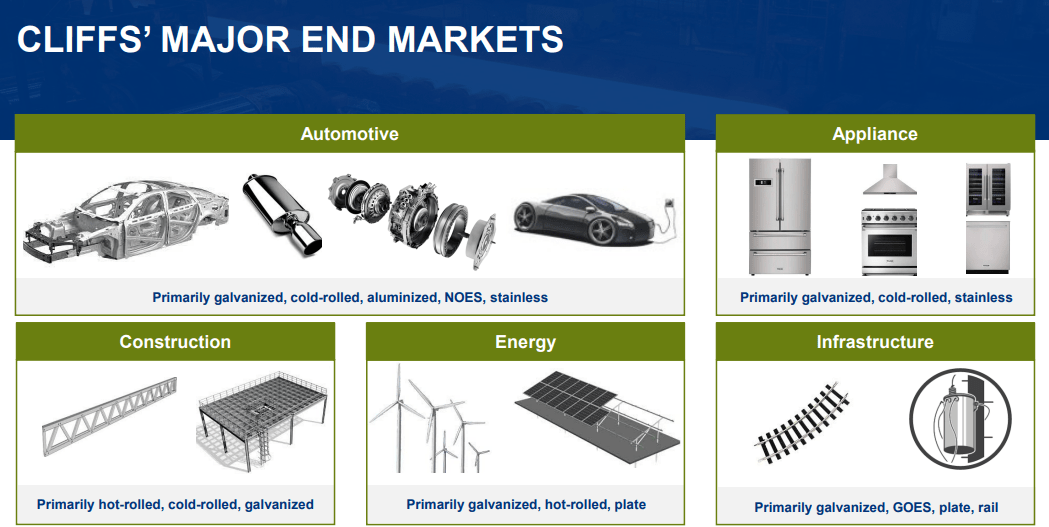

In the first case, consider Cleveland-Cliffs’ end markets.

CLF investor presentation, January 2023

From EVs to building the future energy infrastructure – nothing is going to happen without steel being present. Clearly, steel is cyclical. But my argument is that steel is a lot less cyclical than many investors have been led to believe.

The second consideration has an indirect impact on CLF. And that is, steel is a global commodity. And the biggest consumer of steel is the Chinese real estate market.

If one believes the rumors that China is intent on stabilizing its real estate market, this could see one of the biggest headwinds for the steel sector in 2022, turn into a tailwind.

More specifically, if there’s increased demand for steel, steel prices will increase globally.

Next, CLF has a huge advantage compared with European steel producers, namely that CLF is based in the US.

CLF investor presentation, January 2023

And with five electric arc furnaces, CLF can produce more valuable grades of steel at cheaper input costs when compared with its European peers. The reason for this is that energy prices in the US are about a quarter of the price in Europe.

Consequently, this will mean that CLF has a moat compared with its European peers. CLF can underprice European steel producers and still see significant profits.

Why it’s Different This Time

Analysts following CLF have not revised CLF’s revenue growth rates upward.

CLF’s revenue estimates

What you see here is that for the past several months, analysts following CLF have for the most part maintained their revenue estimates.

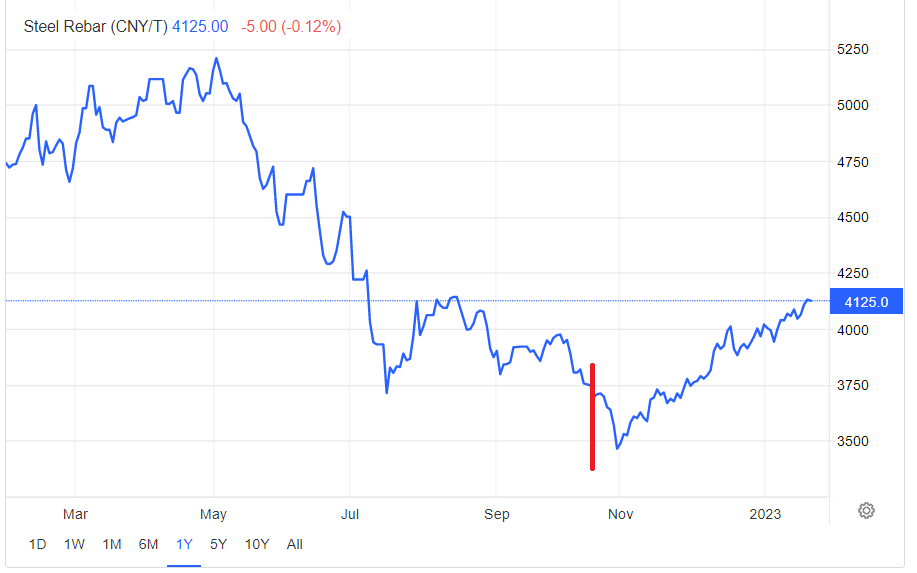

But we know that in the past few weeks, steel prices have been climbing higher again.

Trading Economics

And thus far, analysts have yet to factor in these new higher steel prices.

The Bottom Line

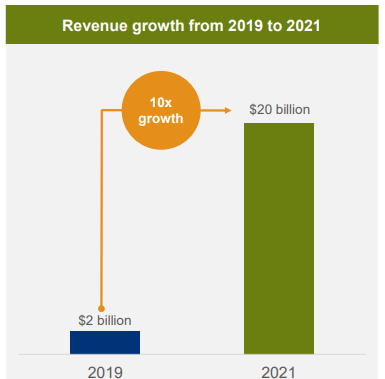

Cleveland-Cliffs CEO Lourenco Goncalves has sometimes been seen as someone with a propensity for hyperbole. Nevertheless, when the facts are in, on the back of two key acquisitions under Goncalves’ leadership CLF has seen its revenues jump 10x in a couple of years.

CLF investor presentation, January 2023

Accordingly, I don’t believe that investors have fully priced where this company is now headed.

On the other hand, these acquisitions have come at a cost. As it now stands, CLF’s balance sheet holds close to $4 billion of net debt. Therefore, steel prices need to remain cooperative for this investment thesis to have a happy ending.

Altogether, there’s a lot to like in CLF. Good luck ahead.

Be the first to comment