gorodenkoff/iStock via Getty Images

This is my second article on ClearPoint Neuro (NASDAQ:CLPT). And while I’ll begin with a brief overview of the company, I recommend that those new to the company also read my initial submittal which goes into the company background, offerings, business model and perceived moat in more detail.

Today I’d like to focus on the company’s growth path and outlook as well as reviewing its valuation and longer term cash management. Note that in its most recent earnings call, the company gave much more color than is typical, so I’ll be highlighting a number of these earnings call comments herein.

Company

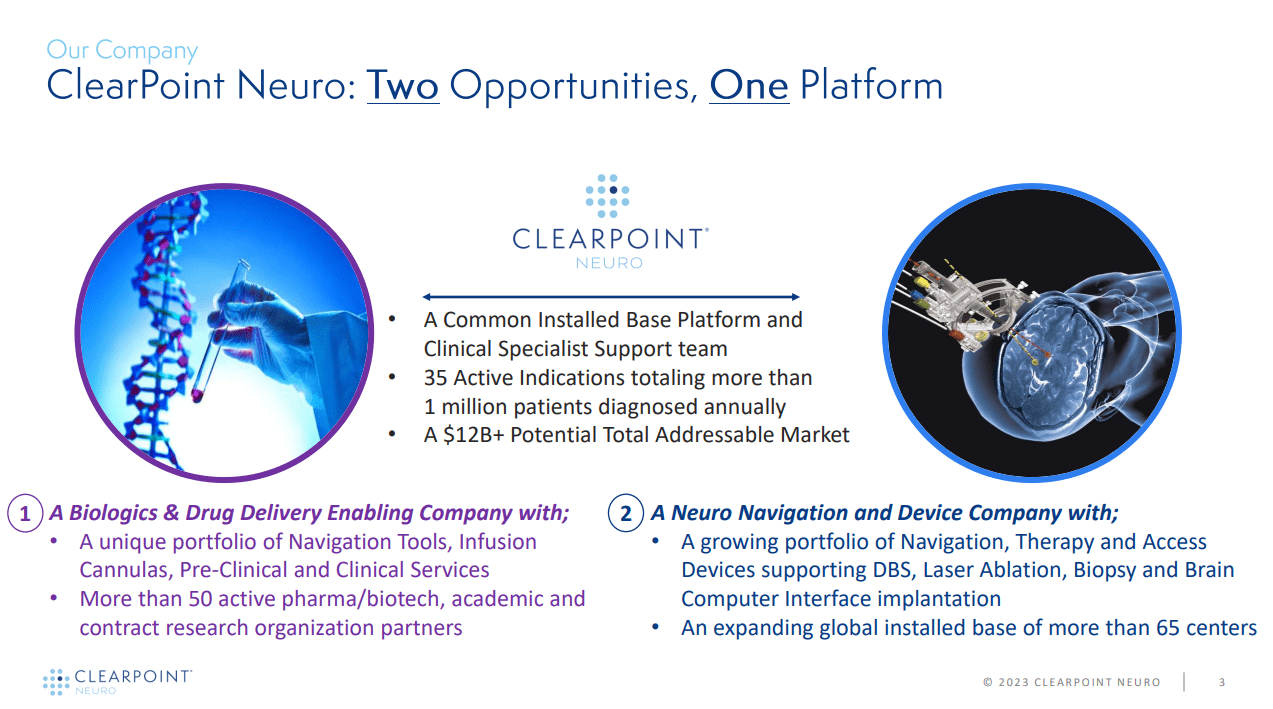

As well illustrated in the company’s January 2023 investor presentation, CLPT is a company focused on providing highly accurate guidance to medical specialists either delivering biologics or performing brain surgery/stimulation in an MRI setting. The company estimates that the total addressable market for these services is on the order of $12B.

Investor Presentation Investor Presentation

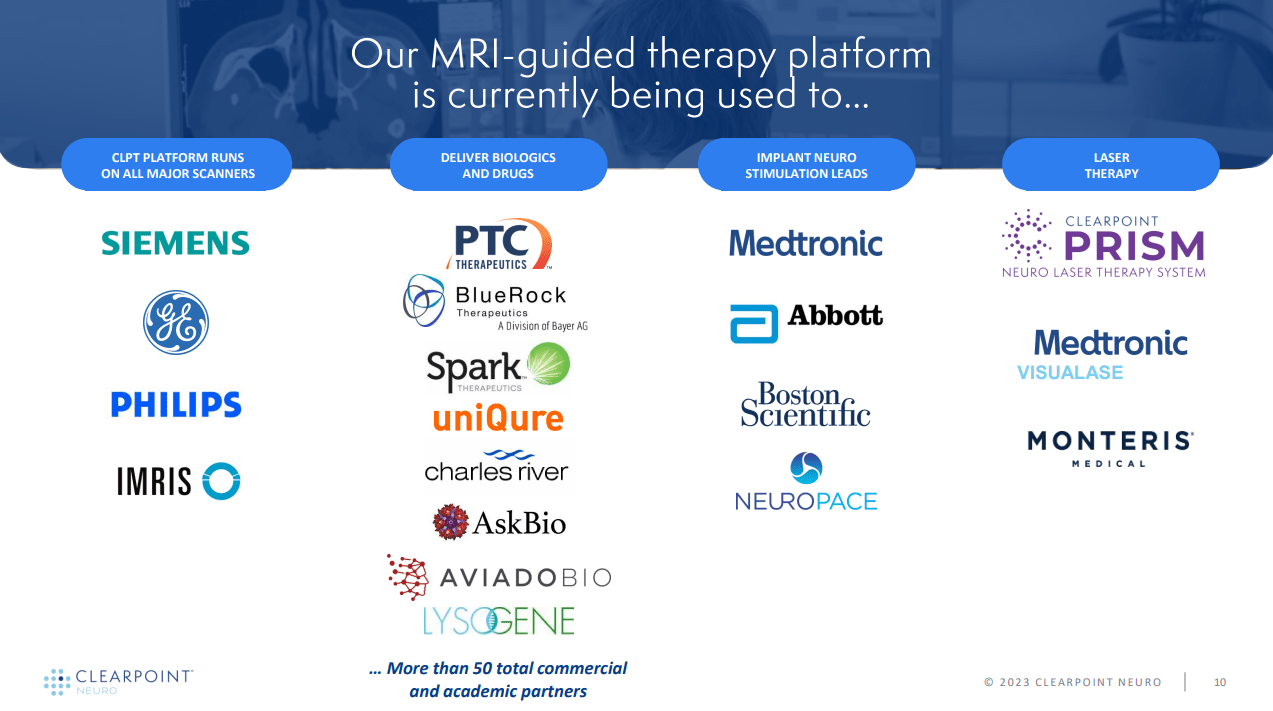

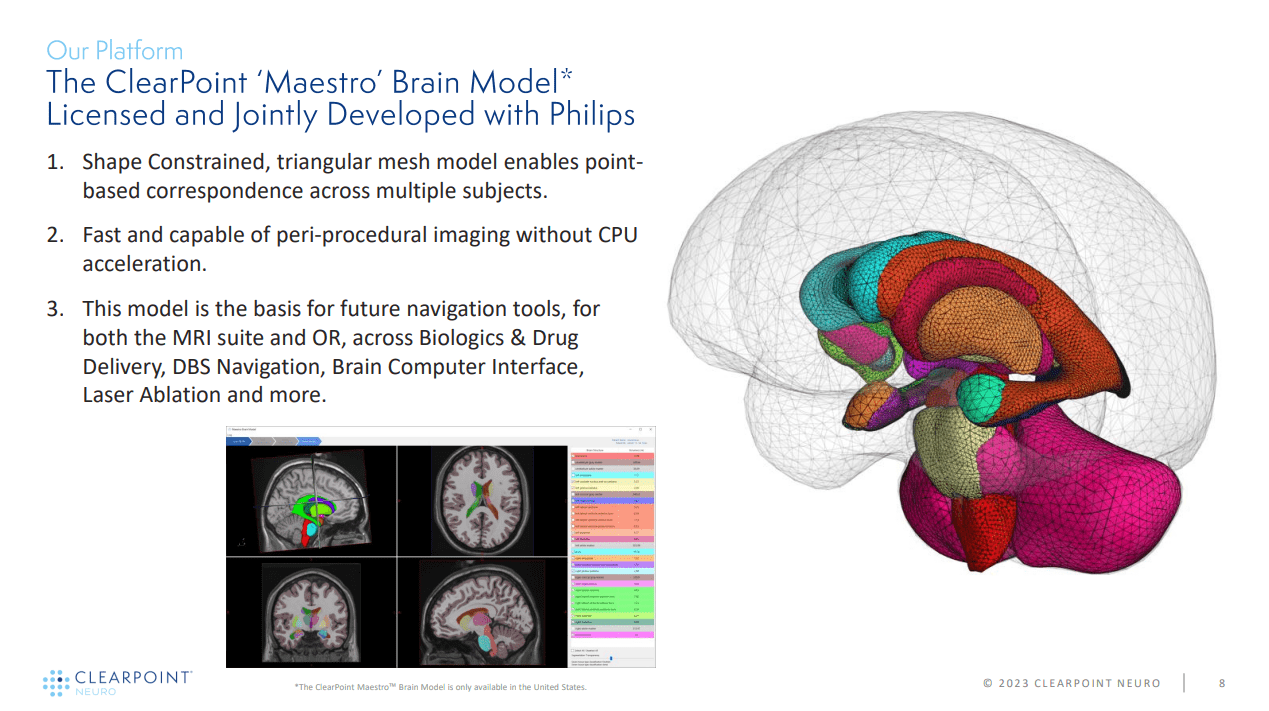

Perhaps most importantly, CLPT has major partners across the spectrum of MRI providers through to end users. Of particular interest is that its proprietary Maestro Brain Model was jointly developed with the very large medical diagnostic company Koninklijke Philips (PHG).

Investor Presentation Investor Presentation

Revenues and Cash Flow

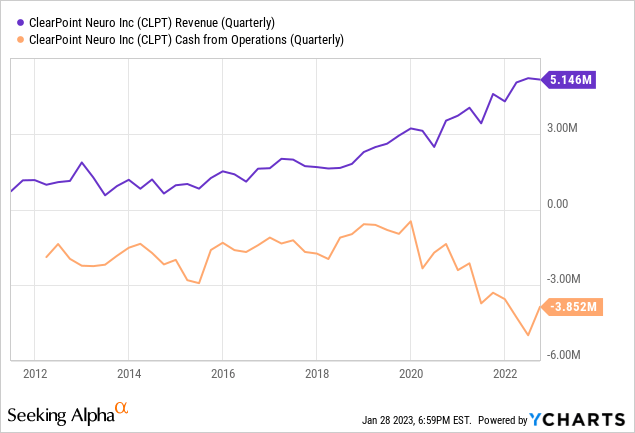

The most important part of the CLPT story is whether or not it will be able to maintain high revenue growth and eventually achieve significant positive cash flows. I’m going to look at several aspects related to this question, but let’s commence by reviewing the historical quarterly revenues and operating cash flows.

As can be seen, CLPT has been growing revenues consistently and recently its cash flow from operations has improved (though still negative). This data has been augmented with unaudited results released on January 11th which show that 4Q revenues are estimated at $5.2M and cash burn at about $3M. In that same release, the company guided 2023 revenues to range between $25M and $27M which would represent year over year growth in the range of 22% to 31%.

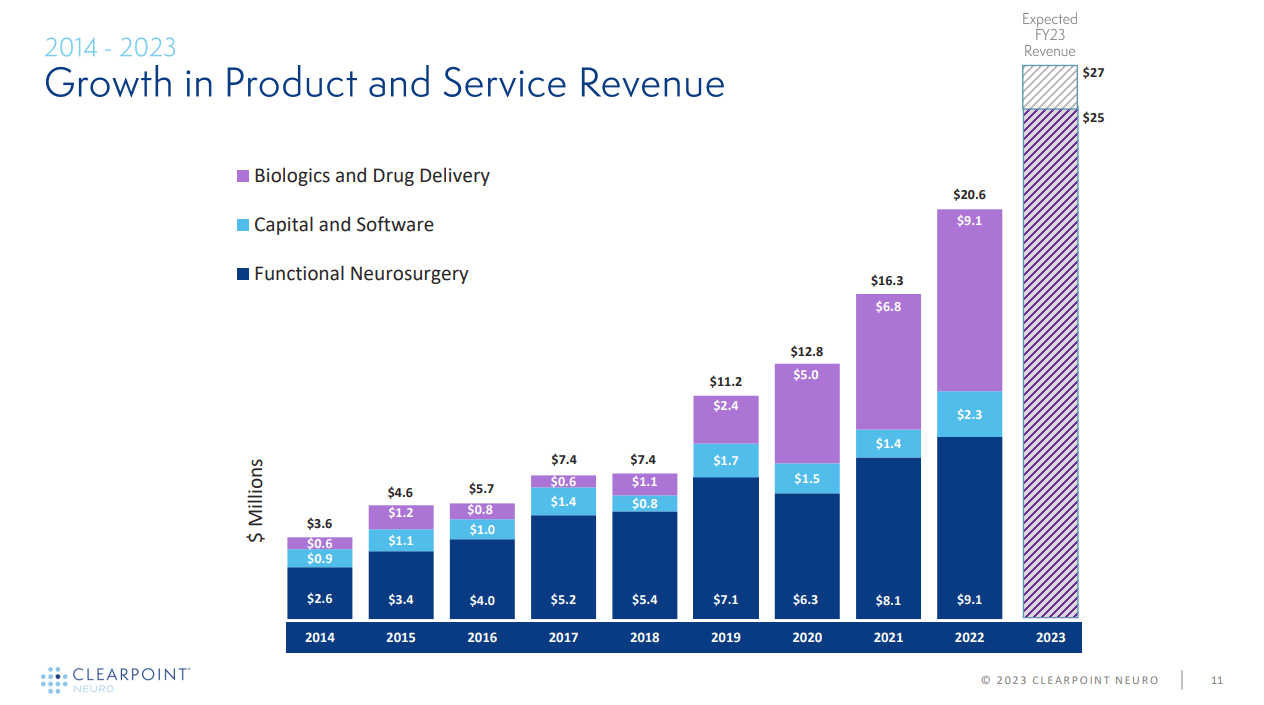

The January investor presentation includes this new guidance in a slide showing the historical breakdown in revenues.

Investor Presentation

Overall I think the progress is evident and should be sustained going forward, but let’s look at some of the details behind my opinion.

Growth

In order to evaluate the company’s likelihood of growing revenues, there are several factors to consider, which I will list with a G# prefix.

G1. New Partners

Perhaps the single most important revenue driver is expanding the number of partners and programs that CLPT is involved with. This drives revenue growth if or when the initial program advances into and through the clinic (and of course it becomes very large if and when a product becomes commercially available). CLPT has performed very well in this pursuit, continuing to add about one partner per month, as confirmed on the earnings call:

First, our biologics and drug delivery team continued to add additional partners and services into the third quarter, adding multiple new partners to our accounts, which is now approximately 50 active relationships in the space. We continue to keep pace with our past two years history of adding approximately one new partner every month.

Moreover, CLPT has added to the services that it can offer partners, such that a program going through to Phase 3 trials can now generate about $10M in revenues versus only $5M a few years ago. Here’s management’s statement on this, again from the earnings call.

If one of our partners or even one of the programs within a partner, would purchase the entire suite of products and services that our team can now provide, the total value of those products and services from initiation of the program through the completion of a Phase 3 clinical trial could potentially add up to $10 million per program before the drug or biologic is even approved.

All of this is very positive, but there was one negative mentioned on the call, namely that some partners are conserving cash, such that growth from any given customer may be slower than it had been in the past. Here’s that excerpt with my emphasis:

And then in some of cases, we’ve heard that some partners have had to sort of prioritize some of their internal programs. Just to go ahead and kind of reduce the burn and save capital, especially some of the smaller companies that might be — might see a capital raise on the horizon. They might be forced to slow down their second and third options and focus their attention and detail on option number one in their platform.

G2. Protecting the “Moat”

This second point is in a way part and parcel of growing partners, but in this case the focus is on maintaining each and every partner it lands. Here’s how I explained the importance of this in my first article:

The biggest reason I like CLPT is that it has a very strong moat, viz. that when any company uses its products as part of any procedure that will need FDA approval, CLPT’s products become part of the package that is submitted to the FDA. Changing to another vendor would thus mean re-testing and re-submitting to the FDA, a costly and timely exercise that every company would seek to avoid. Thus, once CLPT is chosen by a partner, barring completely dismal execution, CLPT will be part of the process indefinitely.

Admittedly we’re still in the very early innings here, but so far this thesis is bearing out. For example, on July 20, 2022, CLPT partner PTC Therapeutics (PTCT) made this announcement (with my emphasis):

Upstaza™ (eladocagene exuparvovec) was granted marketing authorization by the European Commission. Upstaza is the first approved disease-modifying treatment for aromatic L-amino acid decarboxylase (AADC) deficiency and the first marketed gene therapy directly infused into the brain. It is approved for patients 18 months and older.

[…] Upstaza is the first and only approved disease-modifying treatment for patients living with AADC deficiency. We are ready to deliver this long-awaited treatment to patients as soon as possible.”

As it relates to CLPT’s moat, here’s what was said on the most recent earnings call:

Our multiyear strategy has played out as expected where the labeling for Upstaza includes our SmartFlow Cannula directly in the surgical guide as the only infusion cannula to be used in combination with this gene therapy.

To say it another way, the very first gene therapy ever approved for direct injection into the brain is co-labeled with our device in the marketing authorization for administration of the therapy. We believe this first approval along with the exhaustive bench preclinical and clinical testing required for submission is a sign of things to come for many of our approximately 50 active partners that could see a similar path to approval.

G3. Covid and “Ghosting”

While the first two growth factors are going swimmingly for CLPT, this third factor is likely a long term drag on growth. Procedure cancellation rates have increased from a historic 10% value to about 30% now. The company blames Covid primarily, but I wonder if this isn’t a secular change in attitudes that’s related to people ghosting both jobs and dates. Maybe ghosting medical procedures has also become a thing? In any case this negative has to be factored in along with the positive aspects of CLPT’s growth story.

Here’s the color from the earnings call (my emphasis):

In the third quarter of 2022, we continued to make progress across our four pillar growth strategy, including biologics and drug delivery, functional neurosurgery navigation, therapy and access products and in achieving global scale. Despite a continued high cancellation rate due to COVID, historically high surgeon transitions and daily supply chain and hospital staffing challenges, our team was able to achieve near record revenue of $5.1 million for the third [Technical Difficulty] representing 13% year-over-year growth.

[…]

Yeah. I mean, I don’t have too much to add other than, it’s always the worst surprise when you show up at the hospital that morning all ready to go and the patient fails their COVID test and has to postpone for a couple of weeks because in general, we’ve then lost the airfare, we’ve lost the day of capacity from our clinical team and we’ve lost the MRI day. So it’s kind of painful for us. It’s great. We don’t lose the patient. We’re still able to treat them and help them in the next two weeks. However, that day we lose the case.

And historically, pre-COVID, our sort of routine cancellation or postponement rate was always in the 8% to 12% range. Since COVID initiated and sort of has calmed down from the initial stoppage, that postponement rate has been north of 30%/ So the good news is, we’re scheduling more cases, but there’s still a very high percentage that currently are being canceled. And I think we’re seeing this in a number of different avenues.

G4. Domestic versus International Revenue Growth

The final element is analyzing CLPT’s growth path is to consider US vs international growth. According to the company, it will be focused domestically for the foreseeable future, though it will open international sites if the need is driven by one of its partners. Here’s an excerpt from the earnings call discussing this (my emphasis):

So domestically, I think that’s where most of the revenue dollar growth is we expect in the next couple of years as well, whether it’s through our laser program, through new customers that are in doing MRI guided DBS and MRI guided laser procedure and eventually our expansion into the operating room as well. So the U.S. is still going to be the primary focus.

Arguably, we’re going into Europe a little bit earlier than we normally would. But again, this is in order to support our biologics and drug delivery customers that are interested in enrolling clinical trials across Europe with local researchers especially for our European partners. So where we don’t expect a massive revenue opportunity for DBS or laser ablation in the near term in Europe. We are expecting to initiate a number of clinical trials in the next couple of years in Europe.

Overall I think that these four growth factors are overwhelmingly positive for CLPT and I look forward to tracking the progress going forward.

Cash on Hand

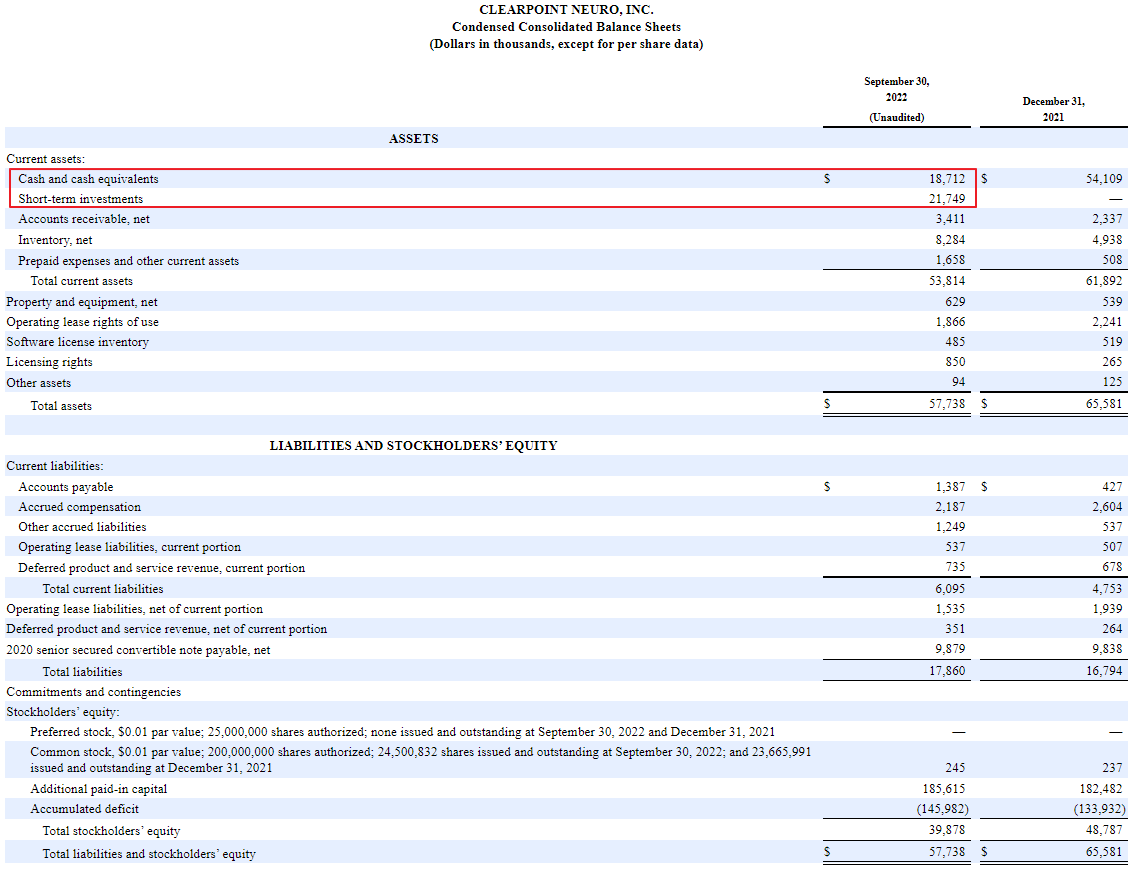

According to the most recent 10Q, the company had about $40M in cash and short term investments available to it. With a cash burn rate of about $3.5M a quarter, that gives about 11 quarters of cash runway, assuming that the company doesn’t turn cash flow positive in the interim.

sec.gov

CLPT confirmed this take on the earnings call, again with my emphasis:

We continue to expect a further step down in our operational cash burn in the upcoming fourth quarter and remain confident we are well capitalized to achieve our mid-term growth ambitions. With respect to our cash position, we finished the quarter with cash and short term investments of $40.5 million compared to $54.1 million as of December 31, 2021.

Given this, I don’t worry too much about the company engaging in a dilutive financing any time in the next two years. So that’s one less thing to be concerned about when evaluating CLPT as a potential investment.

Valuation

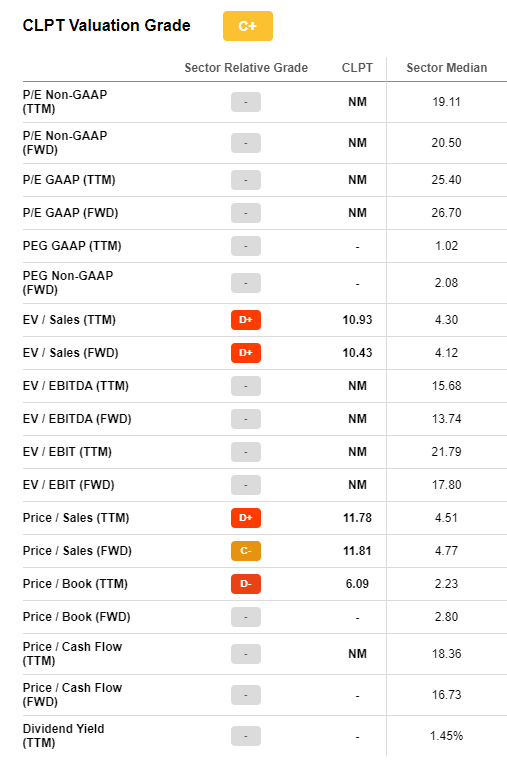

CLPT does not sport high valuation grades, but that is to be expected from a company that’s still generating losses and negative cash flows. The key will be how quickly it grows and whether or not that growth will lead to significant positive cash flows. Nonetheless, the poor valuation suggests that investors should be judicious in their entry points when purchasing the stock.

Seeking Alpha

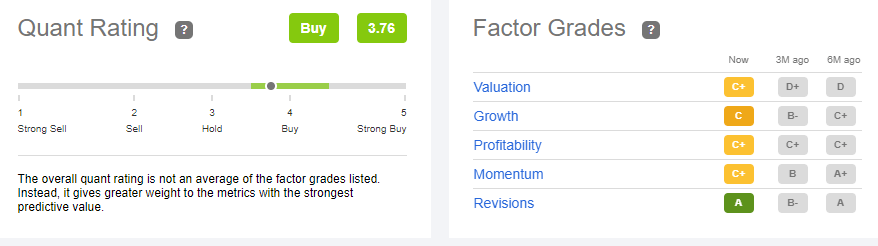

Quant Ratings & Factor Grades

Seeking Alpha currently rates CLPT as a buy, which is the same verdict I have. In particular, the revisions grade is very positive.

Seeking Alpha

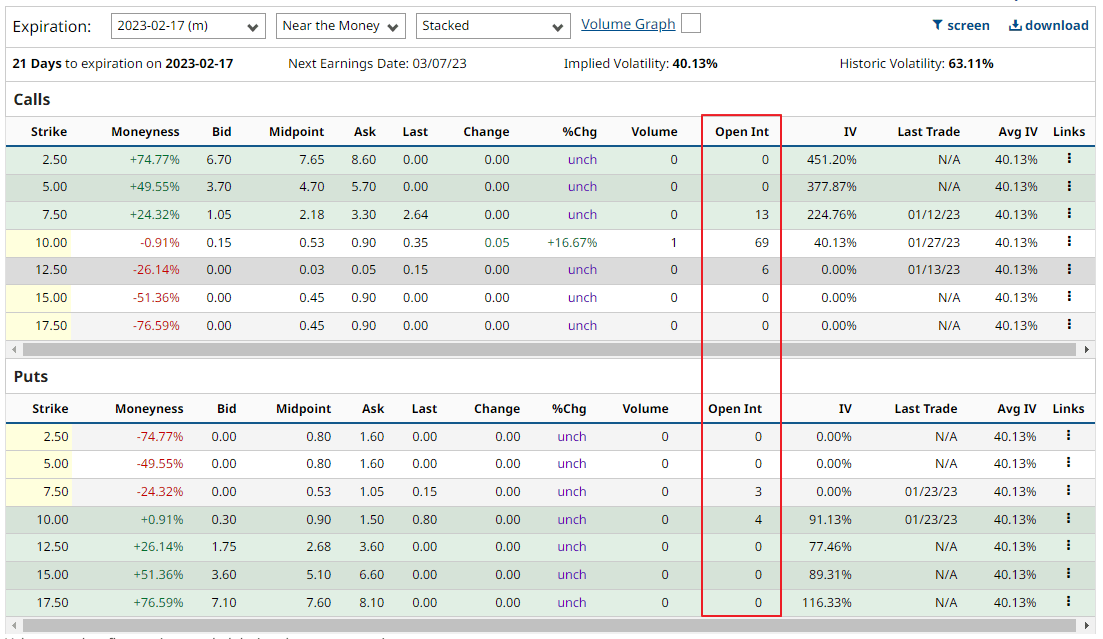

Options

CLPT trades options, but currently they’re not very liquid. Nonetheless, given that I would like to add to my position, I may try to do so via writing cash secured puts.

barchart.com

Risks

The biggest risk with CLPT is poor execution. In particular if it can’t continue to grow revenues while simultaneously improving cash flows, then it will risk dilutive financings in the best case and complete failure in the worst case.

My analysis above suggests that the company is doing the right things to avoid this outcome, but it is definitely a risk.

Summary

I continue to like CLPT’s business model, its moat and growth story. I believe that it is executing well and that future growth can become exponential as its partners advance their candidate therapies through the clinic and eventually make some of them commercial. As such I’m looking to add to my existing position but will likely wait for pullbacks before doing so.

Be the first to comment