Chinnapong/iStock via Getty Images

Decline Opens Opportunities—Some Patience Required

Market Overview

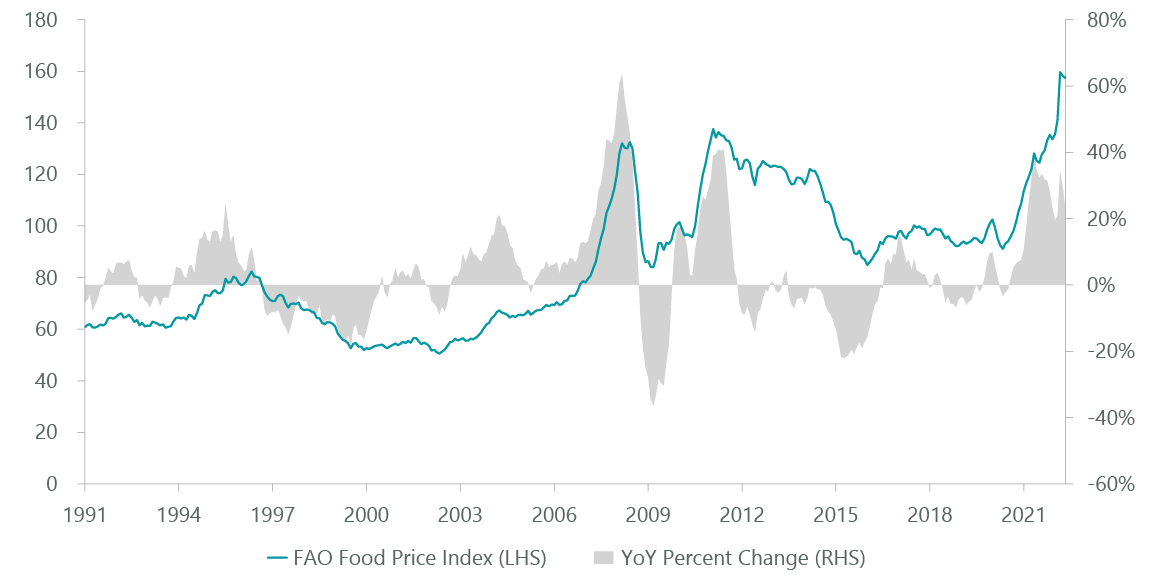

The surprising resilience of the S&P 500 Index we noted in our first-quarter commentary gave way to a dramatic decline of -16% in the second quarter. Issues that concerned us earlier in the year only deepened: the war in Ukraine has no end in sight; inflation in wages, food and energy remains persistent (Exhibits 1 and 2); the Federal Reserve has stepped up its hawkish rhetoric; and valuations remain elevated by historical standards. Signposts we referenced as predictive of future economic activity and equity market opportunity have also deteriorated. Credit spreads continue to widen, parts of the yield curve are flat, economic surveys look bleak and the Fed remains intent on draining liquidity via aggressive interest rate increases and shrinking its balance sheet.

Exhibit 1: Wages are Up…

As of May 31, 2022. Source: ClearBridge Investments, Atlanta Fed, Bloomberg Finance.

Exhibit 2: …But So are Prices

As of May 31, 2022. Source: ClearBridge Investments, United Nations, Bloomberg Finance.

Equity investors had nowhere to hide in the second quarter as all 11 GICS sectors declined. Market leadership was largely unchanged from the first quarter — remaining decidedly defensive — with the energy, consumer staples, utilities, and health care sectors producing the best relative returns. Energy sector performance remained buoyed by stubbornly high oil and natural gas prices, while investors took shelter within the regulated returns of the utilities sector. The historically defensive food and beverage industries (within consumer staples) also offered a slight refuge as investors bet consumers will still buy Corona, ketchup and Cheerios regardless of the economic outlook. A look at the health care sector provides the best example of the market’s defensive tone as the staid pharmaceutical industry buoyed returns, while health care equipment and life science tools underperformed.

Lagging sectors were also similar to those in the first quarter. Consumer discretionary, communication services and information technology (IT) all declined more than 20% April through June. Consumer discretionary weakness was broad based. Bellwethers such as Amazon.com (AMZN) and Target (TGT) fell more than 30%, caught flat-footed with excess warehouse capacity and bloated inventories as post-pandemic consumer behavior shifted away from bigger-ticket items such as electronics and home furnishings to apparel and grocery — and as consumers retrenched from inflation shock. The shift to smaller-ticket items stoked fear of deteriorating consumer spending and contributed to the staggering decline in cruise lines and casino stocks, many of which fell more than 50% in the second quarter alone. Communication services was dogged by the entertainment industry due to concerns over the growth and profitability outlook for streaming services. Finally, although technology weakness was also broad based, it was especially acute for the semiconductor industry where fears of a cycle downturn built throughout the quarter as evidence of an inventory correction mounted.

Outlook

While the market decline has begun to create opportunities, we believe a cautious stance is appropriate. Valuations still look high, and the economic path ahead looks fraught. The Federal Reserve faces a tricky path. Either it tightens sharply, hurting earnings, or it tightens too little to reduce inflation, increasing the intermediate-term level of interest rates. In both cases stock prices seem vulnerable.

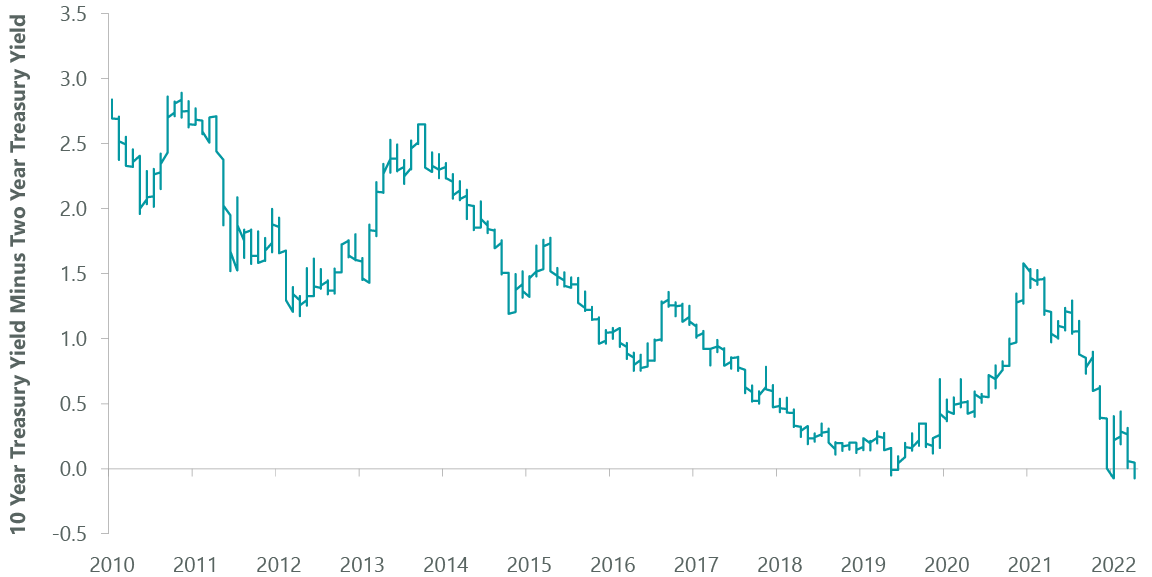

We believe liquidity is a (if not the) primary determinant of equity market performance, and the best environment for stocks is one where the Fed provides liquidity to achieve economic acceleration. Today’s environment is exactly the opposite. For the first time in decades the U.S. money supply turned negative in May. It will be another six to nine months before the impact of quantitative tightening will be felt. Several key economic indicators are flashing warning signs. Initial jobless claims have turned up, the ISM is below 50 and the Treasury yield curve is inverted (Exhibit 3).

Exhibit 3: Treasury Yield Curve is Inverted

As of July 7, 2022. Source: ClearBridge Investments, Bloomberg Finance.

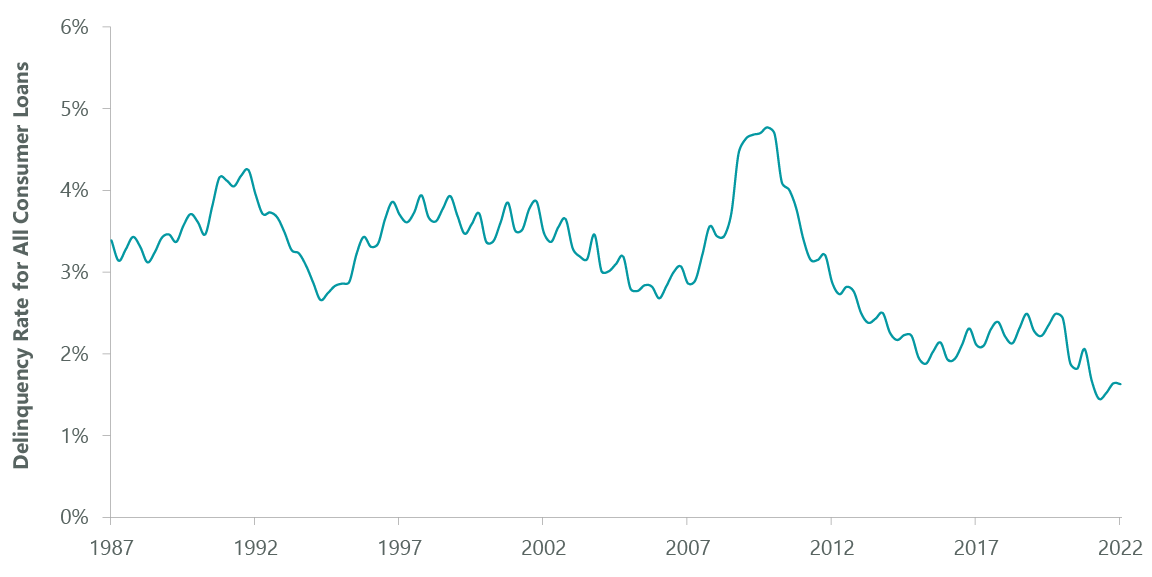

Not all is gloom and doom. We start from a very good place. Unemployment at 3.6% is full, credit costs and delinquencies are near all-time lows (Exhibit 4), consumer balance sheets are in good shape, significant pent-up demand exists for houses and cars and many raw materials are off sharply from first-quarter and early second-quarter spikes.

Exhibit 4: Delinquency Rate for All Consumer Loans

As of March 31, 2022. Source: ClearBridge Investments, Federal Reserve, Bloomberg Finance.

Although the market decline brought P/E ratios optically in line with the 15-year average of 16x, we remain concerned about the market’s valuation. In the mid-2000s, when the federal-funds rate fluctuated between 2% and 5%, a 16x market P/E multiple was more of a ceiling than a floor. Consensus earnings estimates have yet to be revised lower to reflect more challenging economic fundamentals — so the “E” in P/E is too high. Alternative measures of the market’s valuation (such as the Buffett Indicator, which pits the total market valuation to GDP, or the CAPE or Shiller P/E ratio, which is cyclically adjusted) suggest stocks remain aggressively valued (Exhibit 5). It seems we are in the early innings of an expectation adjustment period and although the market is down it is hard to argue it is cheap.

Exhibit 5: Hard to Argue Market is Cheap

As of June 30, 2022. Source: ClearBridge Investments, Bloomberg Finance.

Our emphasis is always to own companies with robust earnings and cash flow throughout the business cycle. The investment environment is likely to remain hazardous for hyper growth companies who have yet to produce profits or free cash flow. We believe software companies with high gross margins and pricing power can perform relatively well even in a high-inflation environment. We remain cautious on semiconductor stocks. Oil and materials prices appear to have peaked. Coatings and other specialty chemicals companies will benefit from lower raw materials prices while volumes should remain healthy even in a recession. The market decline has created opportunities in some stocks in the renewables and renewable energy sectors.

Conclusion

We continue to believe investors should stay the course in equities, although total return expectations should be muted for the near term. We continue to recommend a balanced approach to the markets, including both growth and value stocks with an emphasis on high-quality companies. That said, we believe effective Fed policy will reduce inflation over time and offer patient, long-term investors the opportunity to purchase high-growth shares at better prices later this year.

Portfolio Highlights

The ClearBridge Appreciation ESG Strategy outperformed the benchmark in the second quarter. On an absolute basis, the Strategy had gains in two of 11 sectors. The real estate and health care sectors were the contributors, while the main detractors were the information technology (IT), financials, consumer discretionary and communication services sectors.

On a relative basis, overall stock selection and sector allocation effects positively contributed. In particular, stock selection in the health care, IT, consumer discretionary, communication services and real estate sectors as well as an overweight to the consumer staples sector and an underweight to the consumer discretionary sector were positive. Stock selection in the consumer staples sector and an underweight to the utilities sector detracted.

On an individual stock basis, the largest contributors were Merck (MRK), Eli Lilly (LLY), T-Mobile (TMUS), Pfizer (PFE) and UnitedHealth Group (UNH). The main detractors were Apple (AAPL), Microsoft (MSFT), Amazon.com (AMZN), Costco (COST) and Berkshire Hathaway (BRK.A, BRK.B).

During the quarter we exited positions in Texas Instruments and Salesforce in the IT sector.

ESG Highlights

Analyst-Led Engagements Uncover Value

Environmental, social and governance (ESG) investing has made much progress over the last two decades. Investors in public equities and corporations have taken more ownership of the impact they can have mitigating climate change and making progress on social goals such as diversity, equity and inclusion; ESG data and investment products have proliferated; and ESG assets under management have continued to grow, with most continuing to be actively managed.

Amid such growth has come scrutiny over potential differences between the claims and realities of ESG investing. This has come on the part of regulators, asset owners and increasingly in the public eye, among business and government leaders.

In this environment we think it worthwhile to highlight the value added by ClearBridge engagements and their role in our investment process and stewardship activities. We have made steady improvements and progress in our process, marked by several milestone years, from 2005, when we established a central research platform that began integrating ESG factors by sectors, to 2012, when we explicitly incorporated ESG analysis in analyst compensation and performance reviews, to 2014 when we formally introduced proprietary ESG ratings, which capture company-specific drivers of risk and return related to sustainability. Currently, 100% of our actively owned companies have an ESG rating assigned.

A key through-line in our history of ESG integration, and a key point of differentiation, is that it is carried out by our analysts: we think there is immense value in having the same person responsible for covering a company’s fundamentals and its ESG characteristics. Company engagements, therefore, are likewise led by ClearBridge sector and portfolio analysts, an approach that we believe gives them insights that might not be top of mind for other investors and a fundamental edge, gained through long-term discussions with CEOs and CFOs of portfolio holdings.

Transforming Climate Risks to Opportunities

In many cases, ClearBridge engagements have specific objectives, such as encouraging the retirement of fossil fuels and increasing use of renewables. Such has been the case with electric power company AES (AES), with whose executives and board members we have been engaging for several years on the company’s path to reduce its carbon footprint. We believe our voice, as a top shareholder, has been a valuable addition to AES’s decision making along this path, and our engagements have helped us identify where climate-related risks in a company’s operations could be climate-related opportunities.

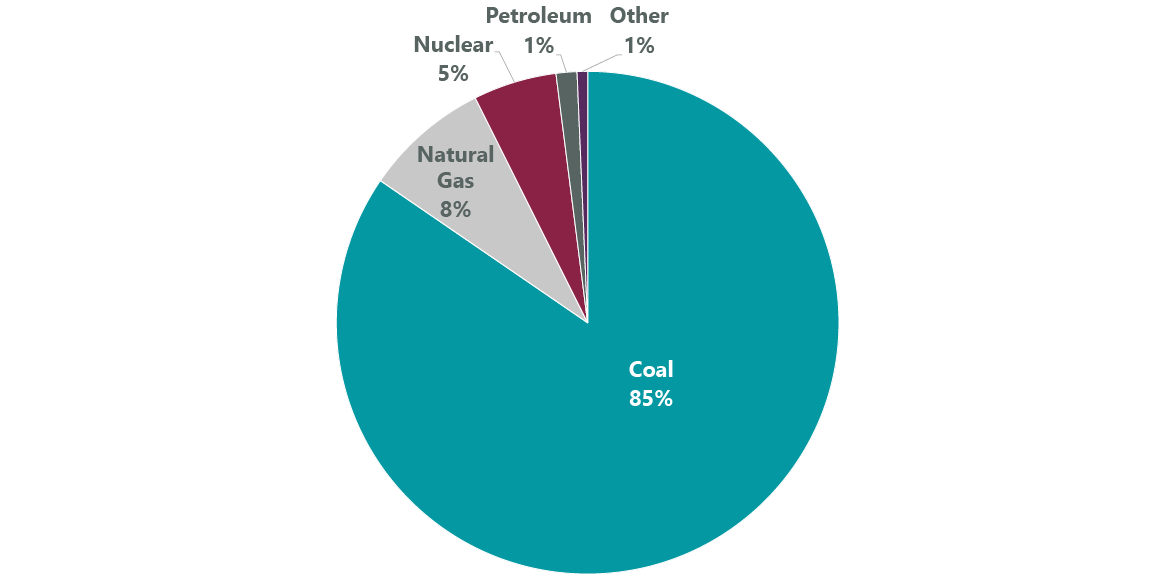

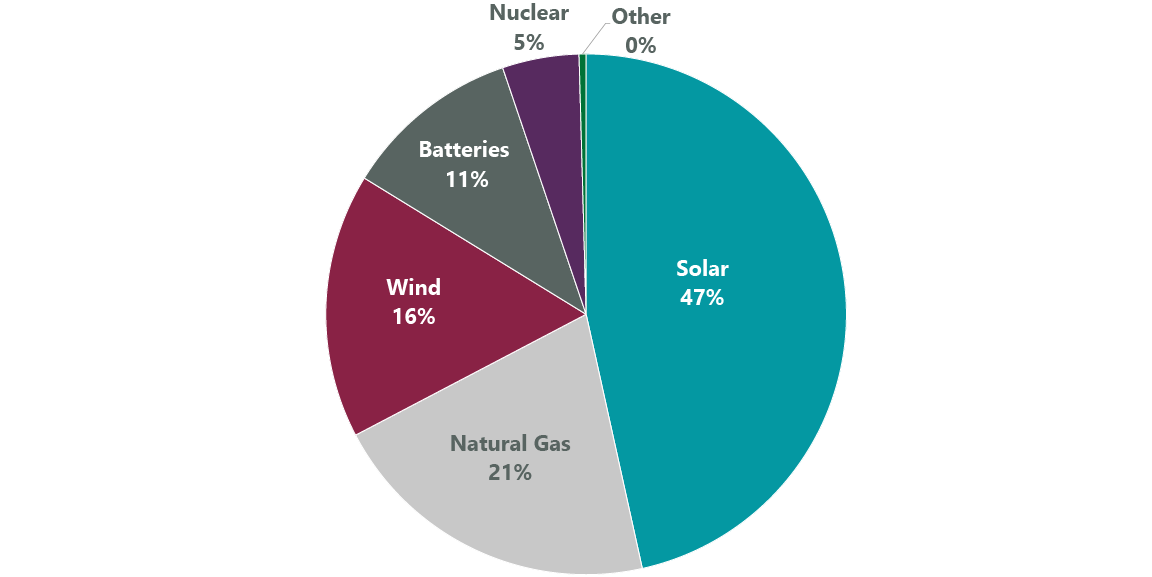

Several years ago, we began discussing with AES the lack of terminal value from coal (Exhibit 2), and we expressed how coal-related ESG concerns were weighing on AES’s valuation multiple, as the ESG risk premium was rising. We helped convince AES to stop investing in coal plants and start shutting down existing coal capacity. The next step was to add renewable energy exposure in the form of wind, solar and industrial scale battery storage (Exhibit 3), in line with U.N. Sustainable Development Goal (SDG) 7: Affordable and Clean Energy (we discuss how an investment framework may further the SDGs in our 2022 Stewardship Report). We shared our belief that any lost near-term operating earnings would be made up with a higher valuation multiple.

Exhibit 6: Planned U.S. Utility-Scale Electric Generating Capacity Retirements 2022 (14.9 GW Total)

As of Jan. 11, 2022. Source: U.S. Energy Information Administration.

Exhibit 7: Planned U.S. Utility-Scale Electric Generating Capacity Additions 2022 (46.1 GW Total)

As of Jan. 11, 2022. Source: U.S. Energy Information Administration.

As our discussions have progressed, AES has been increasingly aggressive in reducing its carbon intensity by lowering coal capacity and investing in renewable energy, as evidenced by its declining GHG emissions. As we had anticipated, AES’s valuation multiple recovered as its product mix shifted from coal to renewables.

ClearBridge encourages companies to align their net-zero goals with the Science Based Targets Initiative’s (SBTi) standards, which clearly define pathways for companies to reduce carbon emissions in line with the Paris Agreement goals. In April 2022 we met with AES Investor Relations and its General Counsel to discuss setting science-based targets as the latest step in this path, and in line with SDG 13: Climate Action. At the meeting, AES confirmed it is exiting coal in 2025. The company continues to develop as a leader in renewable energy, in June 2022 announcing the formation with other leading U.S. solar companies of the U.S. Solar Buyer Consortium, which will invest more than $6 billion in solar panels to scale up domestic solar manufacturing.

Grasping Realities Behind Net-Zero Targets

Environmental impact is a major issue for the transportation industry, including logistics and freight companies such as portfolio holding United Parcel Service (UPS). Recent engagements with the company have given us a better understanding of the challenges in lowering emissions in transport as well as where innovations may be coming from in the years ahead. In ESG-focused engagements in March and May 2022, we discussed UPS’s path to net-zero using science-based targets.

Though it has a 2050 net-zero goal in line with SBTi, UPS has issues complying with SBTi standards because aviation constitutes 60% of UPS’s Scope 1 and 2 emissions. This is an area over which UPS has little control, however, and the maximum exclusion for a source of emissions for SBTi approval is 5%. UPS has committed to a 2050 carbon neutral goal, which is the same as the SBTi’s goal, although UPS takes a different view of the first 15 years of the path, finding existing technology unable to warrant as aggressive a path as SBTi’s.

Over the course of our engagements, we discussed the technical challenges facing the logistics and freight industry and the state of several key technological developments that will be crucial to helping the industry continue to lower emissions. For example, UPS is looking to sustainable aviation fuels, which are biofuels used to power aircraft with a smaller carbon footprint than jet fuel; however, planting to create the enormous amount of feedstock required to replace crude oil is not sustainable. Electric aircrafts are another potential solution, and UPS will have the first of 10 electric aircraft by Beta Technologies delivered by 2024, with an option for 1,400 more. While these planes help time-sensitive health care deliveries and benefit small and medium-size businesses, they have a range limited to 250 nautical miles. A more sustainable path, particularly for long-range transportation, could be the use of hydrogen, but the technology and infrastructure is in nascent stages of development and largely out of UPS’s control. We have encouraged the company, however, to increase pressure on its suppliers to accelerate the development of these technologies. ClearBridge also has ongoing active discussions with aerospace manufacturers on these issues.

Connecting Governance and Long-term Shareholder Value

In addition to finding value in engaging on climate risks, net-zero targets and new technologies, we also add value to our investment process with engagements on a variety of governance topics. For example, we have long supported toy and game maker Hasbro’s (HAS) management and board on strategic, operational and ESG-related topics; the company ranks highly on almost all areas of ESG evaluation, including diversity at board and all-employee levels. We maintain long-term relationships with Hasbro management, and in April 2022, after an activist shareholder started pushing for strategic change at the company, we stepped up our dialogue with senior management and the board.

While we appreciate some of the concerns raised by the activist, we were against most of its suggestions, which we believed would be destructive to long-term shareholder value. We did not believe it was in our best interest to replace three board members with activist-nominated board members — the existing board is replete with talent from the media, technology, content, gaming, entertainment and social media industries.

Over multiple meetings with Hasbro’s CEO and CFO and as many as three board members, our strong relationships helped us better understand what changes would be made where appropriate, and what strategies would remain intact. We had frequent opportunity to share our thoughts on board composition, long-term strategic priorities, compensation, capital allocation and disclosures. All of these became import topics for review during this time. In June 2022 the activist’s proposals were rejected by shareholders. We remain in support of management as it continues on its path of brand-building and growing digital content for its customers.

Advancing a Smart Farm Future

In our engagements with farm equipment maker Deere, we have followed new technology as it has developed from early promise of environmental and social benefits to market reality. In March 2022, Deere’s (DE) Chairman & CEO and CFO met with ClearBridge’s investment team in our New York offices. While prior to the pandemic we had regularly hosted the company, this meeting was among the most interesting as the relatively new CEO outlined a bold plan that placed improved environmental stewardship squarely at the center of the company’s future.

Industrial farming, at its core, is not an especially environmentally friendly enterprise. Agronomic practices have improved over time, but fertilizer, herbicide and pesticide applications and water usage remain problematic. Deere believes its precision farming technology can drive down chemical and fertilizer volumes materially — possibly by as much as 70% — as sensors and cameras attached to tractors, sprayers and combines help determine the exact level of chemicals that might be required. This more precise methodology is expected to: 1) improve crop yields; 2) reduce farmer input costs; and 3) improve overall land management capabilities. Farmers will make more money and grow more food to support global populations while at the same time better caring for the soil. There are also substantial environmentally positive knock-on effects because fertilizers largely are either carbon-based or mined.

There are also social benefits to Deere’s precision farming, such as increasing access to cost savings for smaller, non-commercial or family farms, and the contribution of improved crop yields toward SDG 2: Zero Hunger. This is in addition to its benefits for SDG 15: Life on Land through promoting sustainable use of terrestrial ecosystems. Deere’s technological strength also includes bringing connectivity to farmers in emerging markets, for example improving Wi-Fi access for farmers in Brazil.

New equipment pricing has moved much higher recently as Deere upgrades its offerings to support this effort. That said, the company has introduced substantial aftermarket packages so farmers using older equipment, who may not be able to afford completely new items, benefit from this technology.

Lastly, we discussed a timeline for transitioning large farm equipment away from diesel to an alternative fuel. At present, however, there is no viable alternative that has the power requirements necessary to drive a tractor for an hour, much less a full day, making any such transition a more distant opportunity.

Overall, we had been waiting to have this discussion for several years, and we were pleased the company’s technologies finally appear to have caught up to precision farming’s initial promise.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment