JHVEPhoto

Banks were thought to benefit from higher interest rates. Unfortunately, the yield curve has now inverted to the point where the 6-month T-Bill yields above 4.6% – above the Fed’s policy rate and significantly higher than the 10-year Treasury yield. That can mean trouble for lenders.

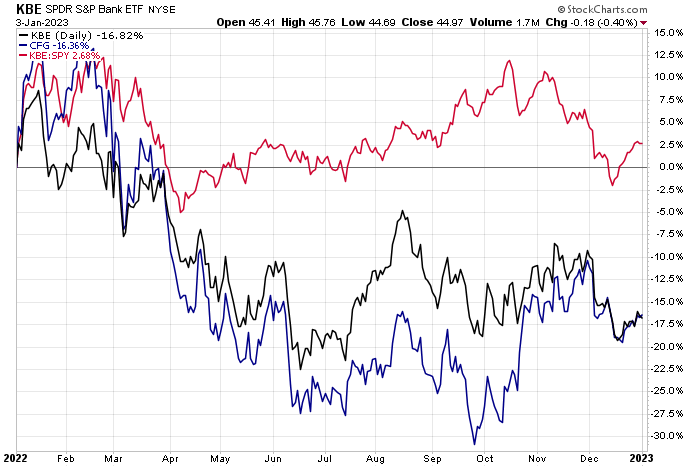

Moreover, capital markets are cold, and corporate borrowing could be lighter now that the cost of debt is higher. As a result, the SPDR S&P Bank ETF (KBE) has struggled since November and has underperformed since mid-October. One regional bank has a better chart, but are shares of Citizens Financial Group (NYSE:CFG) a value? Let’s dig in.

Banks Bouncing Around

StockCharts.com

According to Bank of America Global Research, Citizens Financial operates 1,200 branches primarily throughout 11 states across the New England, Mid-Atlantic, and Midwest regions. It has consolidated total assets of $227 billion. CFG offers a broad range of retail and commercial banking products and services to more than five million individuals, institutions, and companies.

The Rhode Island-based $19.4 billion market cap banks industry company within the Financials sector trades at a low 9.9 trailing 12-month GAAP price-to-earnings ratio and pays a high 4.3% dividend yield, according to The Wall Street Journal. Being a regional bank, there are macro risks that could hurt CFG. In fact, Wedbush recently cut Citizens to neutral for that reason. The good news is that the firm beat estimates in its Q3 earnings report, and all eyes are on the soon-to-be-released Q4 results.

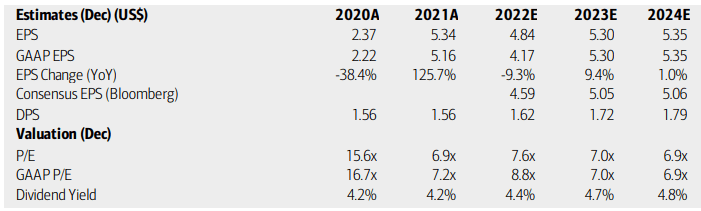

On valuation, analysts at BofA see earnings having fallen more than 9% in 2022 but then recouped nearly all the losses this coming year before EPS growth stabilizes in 2024. The Bloomberg consensus forecast is not quite as sanguine, however. Meanwhile, dividends should increase in the coming quarters while both the operating and GAAP earnings multiples drift down. While the growth prospects on CFG are not incredible, the valuation remains compelling.

Citizens Financial: Earnings, Valuation, Dividend Forecasts

BofA Global Research

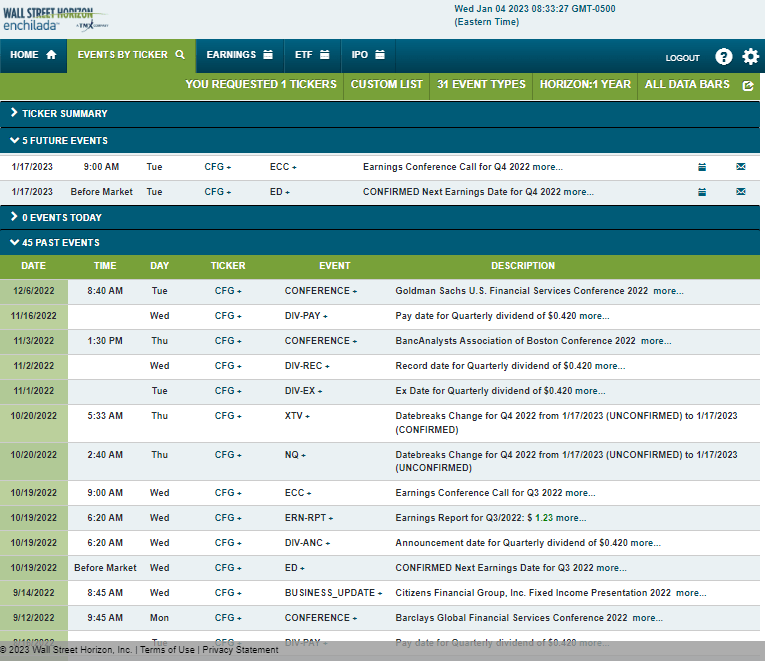

Looking ahead, corporate event data from Wall Street Horizon show a confirmed Q4 2022 earnings date of Tuesday, January 17 BMO with a conference call immediately after results cross the wires. You can listen live here. CFG’s event calendar is light on volatility catalysts aside from the earnings date.

Corporate Event Calendar

Wall Street Horizon

The Options Angle

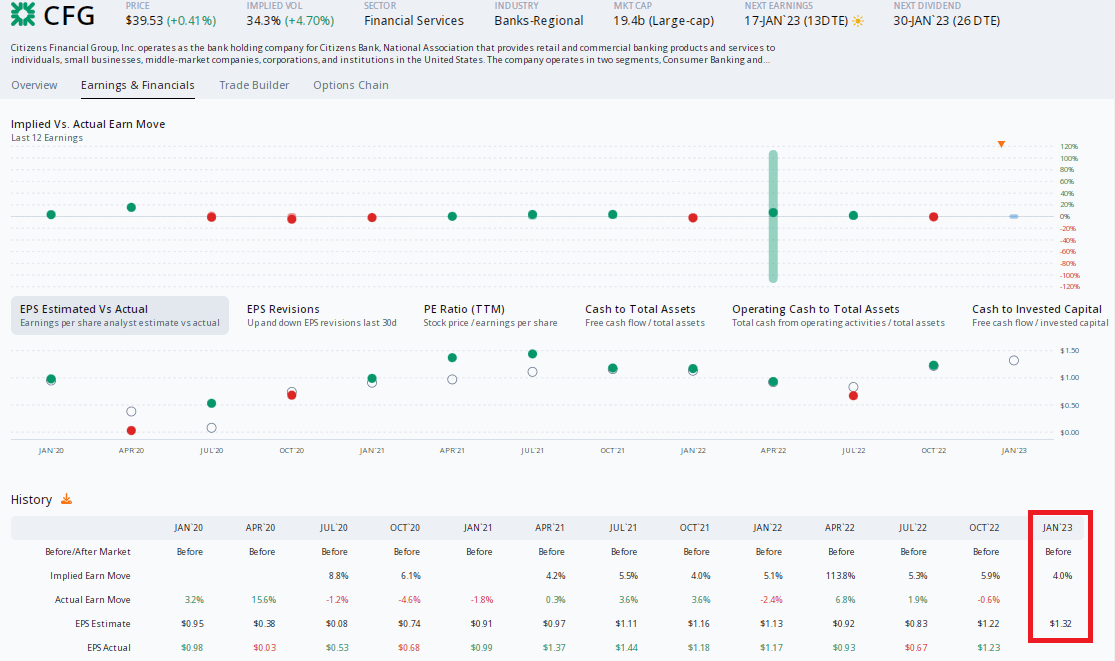

Data from Option Research & Technology Services (ORATS) show a consensus earnings estimate of $1.32, which would be a 13% rise from $1.17 in per-share profits earned in the same quarter a year ago. The company has topped Wall Street forecasts in 7 of the last 8 reports but shares generally don’t move much post-reporting.

Right now, options traders have priced in a modest 4.0% change after the earnings release on the 17th using the at-the-money straddle that expires soonest after the earnings date. Consider that CFG moved just -0.6% and +1.9% in the previous two reports. I would rather just play the stock given a light options market on CFG. But what directional bet should you take? Let’s assess the chart.

+13% YoY EPS Growth Expected

ORATS

The Technical Take

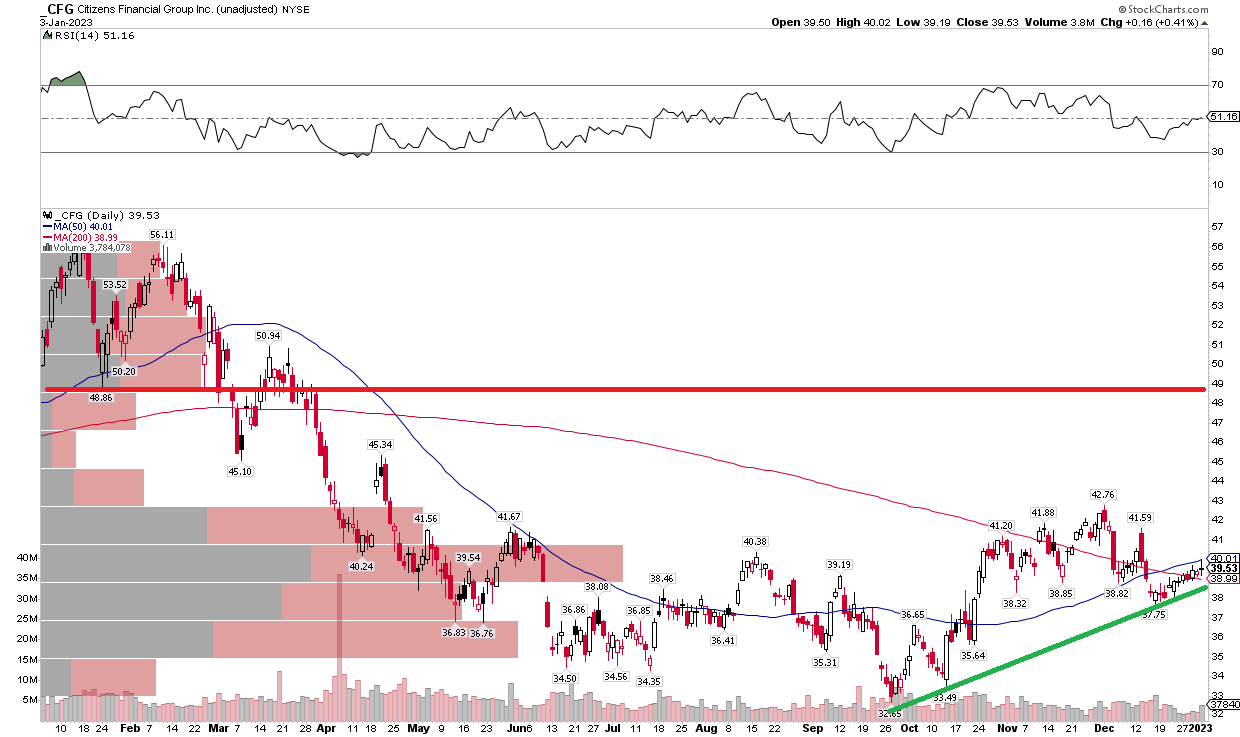

CFG appears to be putting in a broad bullish rounded bottom. Notice in the chart below that shares briefly undercut their June/July lows during a September dip, but then began to make higher lows as the market struggled into mid-October. I see an uptrend support line near the $39 price right now, with resistance at the December peak just below $43. Above that, there is not a high amount of volume until you get near the upper $40s on the one-year chart.

Overall, the trend appears to have reversed, and the stock should continue to rally. A break below $37.50 would be bearish, though.

CFG: Bullish Rounded Bottom With Uptrend Support

StockCharts.com

The Bottom Line

CFG still sports a low valuation while the chart has improved somewhat from a few months ago. I reiterate my buy recommendation but am concerned about macro risks that could weigh on the stock over the next couple of quarters.

Be the first to comment