JHVEPhoto/iStock Editorial via Getty Images

Note: All figures are Canadian dollars throughout this article.

Well managed banks are easy to value. Both sides of the balance sheet comprise the equivalent of cash. Book value of equity is a proxy for intrinsic value if return on equity is equal to the expected return on market indices, and understates intrinsic value if return on equity is higher than returns expected from market averages. There is no need to go through the complexity of the capital asset pricing model to come to this conclusion since it will universally arrive at the same outcome for Canada’s big five banks in general and Canadian Imperial Bank of Commerce (NYSE:CM) in particular.

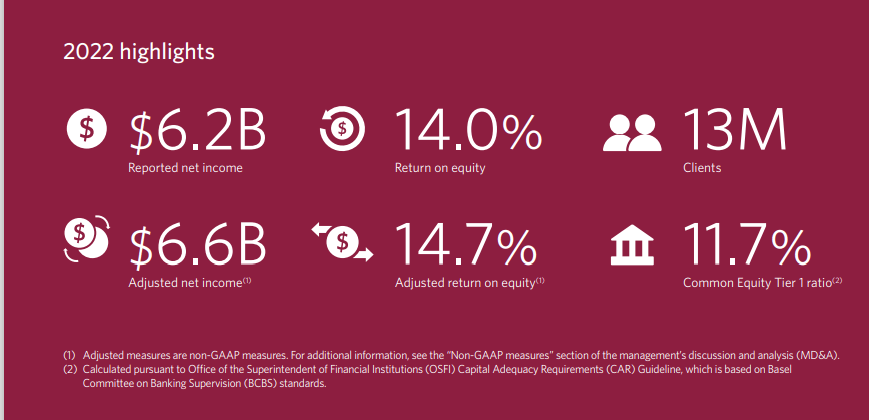

CIBC reports a return on equity capital of about 14%.

Screen clipping (CIBC annual report for 2022)

Market returns have averaged about 9.5% for the past 50 years and there is no reason to expect a different trajectory for the next 50 years, although there is no doubt there will be years where major indices return both more than 9.5% and less than 9.5%.

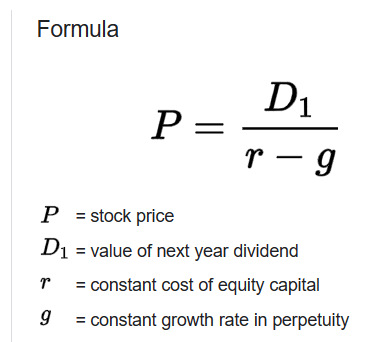

Canada’s banks are good candidates for valuation based on the Gordon dividend pricing model which estimates intrinsic value as the present value of future dividends. The Gordon formula is:

Screen clipping (Investopedia)

I prefer to use the term “value” instead of “stock price” and “required rate of return” instead of “cost of capital”. Restated, the formula is:

Value = Dividend/(Required return less growth rate in dividends)

For the last 20 years (2003 to 2022) CIBC net earnings have grown from $2.1 billion to an estimated $6.2 billion, a compound growth rate of 5.4%. I see no reason that the trend will not continue for many years to come, albeit with ups and downs.

CIBC pays a $3.40 dividend ($0.85 quarterly). For CIBC, the value of a share using the Gordon dividend growth model and assuming investors continue to be satisfied with a 9.5% rate of return is:

CIBC share value = $3.40/(.095 – .054) = $83.00

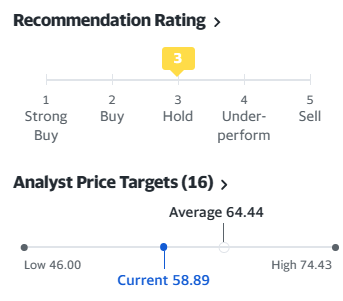

According to Yahoo.com finance, most analysts rate CIBC stock as a “hold” with “price targets” ranging from $46 to $74.43 with an average of $64.44.

Screen clipping (Yahoo.com)

My opinion is that sell-side analysts undervalue CIBC owing to a short-term bias reflecting concerns of a pending recession and the potential for higher loan loss provisions during an economic downturn. I have no doubt a recession is likely and will cause higher loan losses, but valuation is not a bet on the short term vicissitudes of the economy but a long term look at likely returns.

In the case of CIBC, I see the stock as worth at least $80 a share and expect investors who buy the stock at current prices will benefit from a robust and growing stream of dividends for many years to come.

If a recession does emerge and CIBC stock trades at lower prices, I consider such an event an opportunity. If the price dips to below book value, a possibility in a recession, I would be an aggressive buyer of the shares expecting returns in the low teens for decades to come.

Be the first to comment