Editor’s note: Seeking Alpha is proud to welcome Tangerine Capital as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thomas Kelley

I believe Churchill Downs (NASDAQ:CHDN) will generate index-beating returns over a five-year period. Here’s why: The stock appears to be undervalued, even when using conservative estimates in the discounted cash flow analysis. In addition, there is potential for margin improvement by expanding their online betting business. The market as a whole is also growing, and they can capitalize on that through mergers and acquisitions. The management also stated that they will maintain their strategy of returning cash to shareholders via share buybacks, dividends, or other value-adding initiatives.

Brief Introduction

Churchill Downs is a company that operates horse racing tracks, most notably the Churchill Downs racetrack in Louisville, Ky., which is home to the Kentucky Derby, one of the most famous horse races in the world. The company also owns and operates several other racetracks across the United States, as well as off-track betting facilities and online wagering platforms. In addition to its horse racing operations, Churchill Downs Inc. is also involved in the casino industry, with a number of properties across the country. The company was founded in 1875 and is headquartered in Louisville, Ky.

Analysis

My analysis is based on numbers from Fundsmith and my own research.

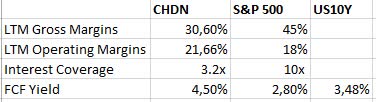

As is evident from this data, there are drawbacks in terms of interest coverage. This is primarily caused by recent borrowing. This will be discussed in more detail in the risk report. However, there are clear advantages over the S&P 500 in terms of free cash flow yield and operating margins, making the company superior to the index in overall performance based on these key metrics. The free cash flow of $387 million provides a safety cushion against the low interest coverage and still offers financial flexibility.

In addition, the free cash flow yield, margins, and interest coverage are expected to improve within the next year due to ongoing improvements within the company. Further information on this topic will be provided in the following sections. Here are my calculations, based on financial information from CHDN:

- ROC: 5-year average is 26.13%

- ROE: 5-year average is 38.14% (TTM is 100.94% due to new debt)

An indication of a good company is its ability to efficiently reinvest capital. To demonstrate this, I have chosen to use the two key metrics ROC (return on capital) and ROE (return on equity). The 5-year averages for both metrics indicate that the company is an effective allocator of capital and is generating returns that surpass its cost of capital. The exception in the TTM numbers for ROE is due to increased borrowing.

Should they, as I expect, be able to maintain these average values, they will achieve a value-add for their shareholders through their business activities and expansion plans. The new acquisitions are within the core business of the company, thus, there is no need to worry about diversification as it often happens when companies expand into new business fields that have no relation to their core business. We will examine these growth opportunities and others in a later paragraph.

Own elaboration in Excel

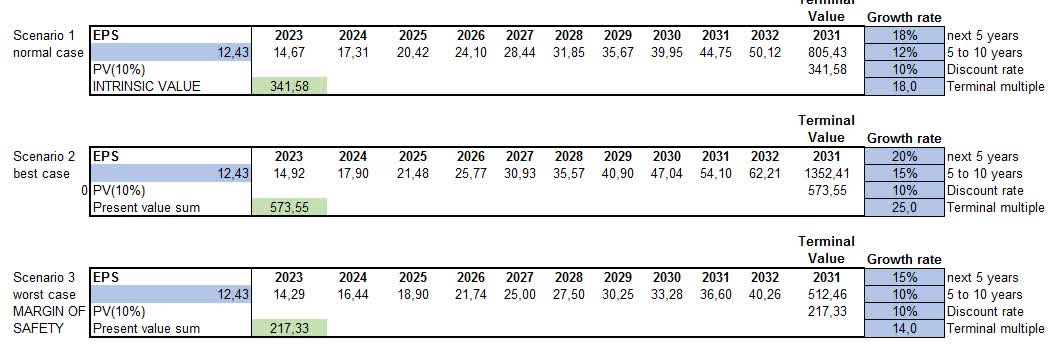

The foundation of the discounted cash flow (DCF) model is the annualized increase in earnings per share (EPS) of 33.06% over the last 5 years and 27.33% over the last 10 years. However, to incorporate a larger margin of safety, we use more conservative assumptions. The EPS was used as it better represents the decline in share outstanding due to past buybacks, compared to what would be possible using market capitalization. The discount rate used is 10% because it represents our minimum hurdle for an investment.

Within the 3 cases, various terminal multiples were used, as there is the possibility for multiple expansion or contraction in the future. Currently, the terminal value is estimated to be around 19, which is slightly higher than the value of 18 that is used in the normal case. In all cases, we calculated declining EPS growth rates after 5 years to be as conservative as possible, even as we know that some companies can maintain growth rates for 10 years or even increase them.

Based on these calculations, we can anticipate the following annualized returns, assuming that the assumptions hold true

- normal case: 12.86%

- best case: 18.87%

- worst case: 7.87%

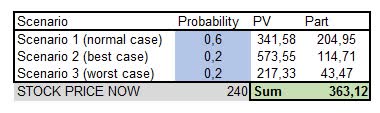

The average annualized return could be 10.49% if we multiply the cases with the probabilities from the table below.

Own elaboration in Excel

If we take a current price of $240 as a starting point, this gives us an upside of just about 50% to the potential fair value of $363. This would mean that the company is currently undervalued, but of course, our assumptions about the future would have to prove to be true for this value to be realistic. We already know that they are able to efficiently deploy their capital. The current and planned M&A activities should therefore lead to an increase in the company’s value. They also have other areas that could contribute to increasing the value of the company.

Share Buybacks Plus Insider Ownership

The share buyback figures and also the statements of the management show that the objectives of the shareholders and the management are in line. In the past 7 years, approximately 15% of the current market capitalization has been used for share buybacks. Furthermore, an additional $300 million is accessible for buybacks. At the current share price, this equates to slightly over 1 million shares or approximately 3% of the current market capitalization. In the last quarter, 289,000 shares were repurchased at an average price of $204. This is equivalent to $58,958,000. Likewise, they keep emphasizing that they will stick to their strategy of being shareholder-friendly, be it through share buybacks, dividends, or other activities that maximize shareholder return.

Fourteen insiders collectively own 5.31% of the company’s stock. This should serve as evidence that management has faith in the company, and that their goals and compensation are aligned with the share price.

Margins

The company’s partnerships with DraftKings (DKNG), FanDuel (DUEL), and Bet365 provide opportunities to gain new customers, increase revenue, and enhance margins. To bet on the Kentucky Derby or other races at Churchill Downs, the racetrack must be compensated for each bet. Along with creating content for the races, this provides the opportunity to generate high margins. Content fees for content distributed by Churchill Downs offer the possibility of earning more attractive margins than in the core business.

As revenues from online betting are expected to increase in the coming years, these margin improvements in this business segment offer the opportunity to positively impact the gross and operating margins of the entire company.

Market Plus Growth Opportunities

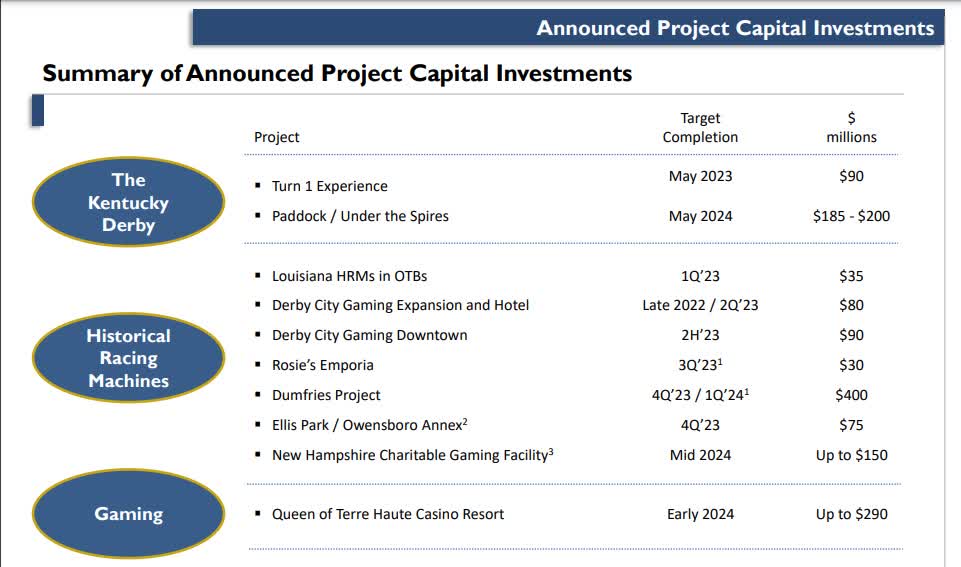

An industry report suggests that a CAGR of 17.34% can be achieved over the next five years. With licenses for more horse racing machines and barriers to entry in this market, this presents a very positive outlook for the future. The growth opportunities are present to achieve the forecasted goals. There are currently two new properties in development and five licenses for the operation of an additional 2,300 horse racing machines are still available. Additionally, there is still the potential to operate a total of 9,000 more horse racing machines at Kentucky horse racing tracks. Expansion into Europe and Asia for Kentucky Derby qualifiers will also attract new customer base.

December 2022 Investor Presentation

The table above displays the planned investments for the next two years. The expansion of HRM properties is expected to result in organic growth. If the management continues its successful record of integrating new businesses and implementing organic growth projects, these investments are likely to result in an increase in free cash flow and earnings that can then be distributed to shareholders.They also acquired Peninsula Pacific Entertainment in late 2022 for approximately ~10.5x EBITDA.

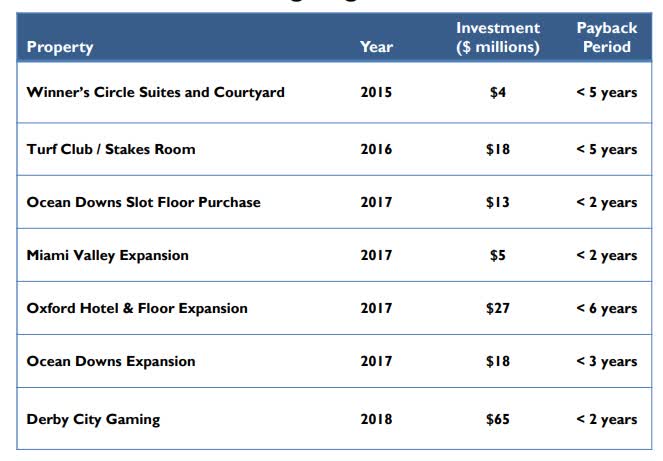

In the last investor presentation, they stated that the acquisition would immediately be accretive to free cash flow and earnings per share. The acquisition should also aid in decreasing taxes paid in cash, as a result of the classification of the acquisition as an asset purchase for tax purposes. The management emphasized in the reports and investor calls that they are looking for suitable deals that fit the portfolio and bring in a suitable return. The table below illustrates the payback times of past deals and should make it clear that the management is capable of finding suitable deals.

Investor Presentation December 22

Risks

As already mentioned, the debt situation may be a deterrent for some investors. A debt coverage of only 3.22 and a net leverage of 4.4 are not optimal. However, this scenario is expected to improve in 2023 as the sale of the Arlington property in Q1 2023 will generate $197 million and the new acquisitions made in 2022 will boost free cash flow. This should result in an increase in cash reserves and subsequently, an improvement in key performance indicators. In addition, no debt is due until 2024 and even then only just under $400 million. The next debt will then not be incurred again until 2027.

By using the historical FCF growth rate, it should be possible for the FCF to be greater than the debt incurred in 2024. This, in conjunction with the cash balance, should provide additional protection for the debt that will be due in that year. Nevertheless, the debt situation should be kept under review and appropriate action taken if debt increases. The 61.76% YoY increase in debt to $3.174 billion is hopefully an isolated occurrence. Another risk to consider is the potential for a recession that could lead to a decrease in player numbers due to decreased incomes. Additionally, there is a risk that additional taxes may be imposed on gambling.

In summary, I believe that the risks are manageable and the management, with its long-term expertise, should be able to manage and respond to these risks as necessary.

Conclusion

In my opinion, at the current share price, the risk/reward ratio is relatively attractive for buying a company that is likely to outperform the S&P 500 over a five-year period. Prices below $225, or even below $200, would add to the margin of safety. I believe these prices are possible, depending on how the market reacts to the Federal Reserve’s decisions in the upcoming months

Even at today’s prices, Churchill Downs should be an attractive investment opportunity for long-term investors. After all, management has demonstrated in recent years that they are highly responsive to shareholders as Incentive goals are based on results that the committee believes drive company and shareholder success. I would closely monitor the debt situation and how the return on capital evolves over the next few quarters. If both of these factors continue to be favorable, then Churchill Downs would likely be a worthwhile investment over a five-plus-year time frame, with the potential for a 10+% CAGR over that period. The potential to retire 1 million shares and increasing profits could greatly benefit shareholders.

Be the first to comment