marchmeena29/iStock via Getty Images

Chimera Investment Corp. (NYSE:CIM) has an appealing double-digit dividend yield as well as an appealing book value valuation. At the same time, the yield and the trust’s current quarterly dividend of $0.33 per share are covered by distributable earnings. A low pay-out ratio of 73% indicates the possibility of a dividend increase. Even though mortgage trusts are risky investments for yield-seeking dividend investors, Chimera Investment’s 30% discount to book value provides investors with a safety margin.

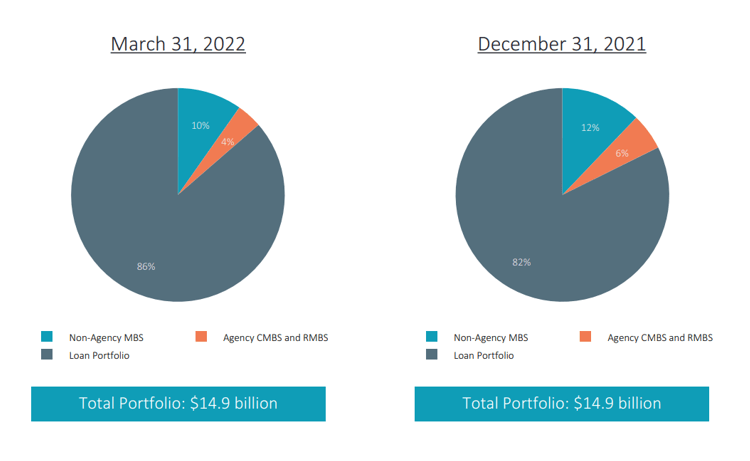

Loan-Heavy Investment Portfolio

Chimera Investment’s investment portfolio is made up of 86% residential mortgage loans, 10% non-agency mortgage backed securities, and a small portion agency commercial and residential mortgage backed securities (4%). Chimera Investment’s total invested assets were $14.9 billion on March 31, 2022, implying that the total portfolio value remained unchanged from the previous quarter.

Investment Portfolio (Chimera Investment Corp)

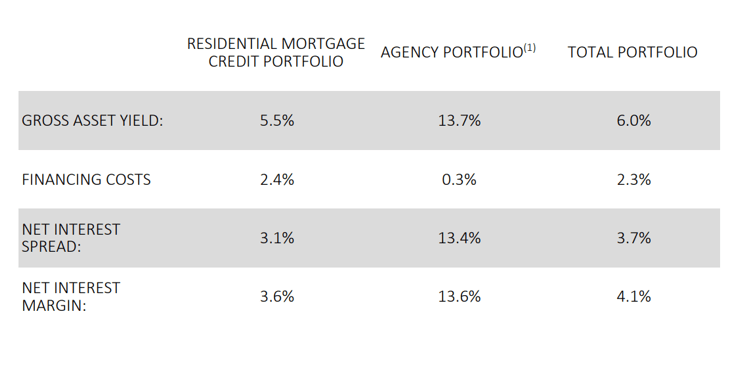

Chimera Investments earns a net interest spread as a mortgage trust, which is the difference between the yield on the trust’s assets and its borrowing costs. Chimera Investment’s total portfolio net interest spread, which includes Residential Mortgage Credit and Agency Securities, was 3.7% in 1Q-22, down 0.4 percentage points from the previous quarter due to lower gross yields.

Rising interest rates threaten to raise Chimera Investment’s funding costs and reduce its net interest spread in the future. The Fed is expected to follow up with aggressive rate hikes in 2022, which could mean higher costs for the trust’s debt-driven business model.

Net Interest Spread (Chimera Investment Corp)

Currently Trading At A Very Attractive Valuation

Chimera Investment currently trades at a P/B ratio of 0.7x, representing a 30% discount to book value. A large discount protects against rising inflation, interest rates, and negative net interest spreads.

Mortgage trust valuation discounts have increased significantly in 2022 as investors priced in the possibility and extent to which the Fed will raise interest rates this year. The central bank raised interest rates by half a percentage point in May, to a target rate range of 0.75% to 1%, and more hikes are expected.

In general, dividend investors should buy mortgage trusts only if they are selling at a significant (10% or greater) discount to book value, to allow for valuation errors and changing variables in the mortgage market that could result in a lower net interest spread.

With mortgage and interest rates expected to rise in 2022, mortgage trusts’ book values fell significantly in 1Q-22. To prepare for further book value losses, it is prudent to buy mortgage trusts only when they are selling at a significant discount to book value.

Mortgage trusts have begun to trade at (higher) book value discounts as book value risks have increased due to higher mortgage and interest rates in 2022. The mortgage trust comparison below shows that Chimera Investment has a high discount to book value in comparison to its competitors.

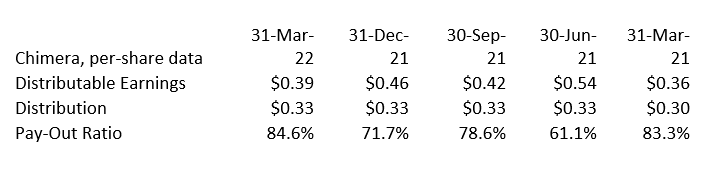

Dividend Is Covered And Could Be Raised

Chimera Investments’ dividend will not be reduced. The mortgage trust reduced its dividend from $0.50 per share in 1Q-20 to $0.30 per share in 2Q-20, but it was increased 10% in 2Q-21 due to an increase in income. The current dividend of $0.33 per share is covered by distributable earnings, and Chimera Investment’s pay-out ratio was 72.9% last year.

Dividend And Pay-Out Ratio (Author Created Table Using Trust Information)

Why Chimera Investment Could See A Lower Stock Price

Rising interest rates and higher borrowing costs are two factors that should worry mortgage trust investors. Mortgage trusts rely on debt to finance the acquisition of mortgage securities, and if capital becomes more expensive, Chimera Investment’s net interest spread may contract, resulting in lower portfolio income. New book value losses could result in a lower book value multiple.

My Conclusion

Chimera Investment is now trading at an attractive level, and the mortgage trust’s valuation adequately reflects concerns about rising interest rates.

Chimera Investment is particularly appealing as a high yield dividend investment because the trust covers its dividend with distributable earnings and the stock can be purchased at a significant discount to book value.

Be the first to comment