Dilok Klaisataporn

Many infrastructure stocks remain deeply discounted due to higher interest rates and economic concerns, despite holding moat-worthy assets that should rise in value over time. This includes Charter Communications (NASDAQ:CHTR), which as shown below, trades well under its 52-week high of $621. In this article, I highlight what makes CHTR a compelling value stock at current levels, so let’s get started.

CHTR Stock (Seeking Alpha)

Why CHTR?

Charter Communications is one of the two “big broadband” service providers in the U.S., alongside peer Comcast (CMCSA). Through its Spectrum brand, CHTR serves more than 32 million customers in 41 states with internet, TV, mobile, and voice services. Charter is often the only available broadband option in its service areas, thereby giving it pricing power in many of its service territories.

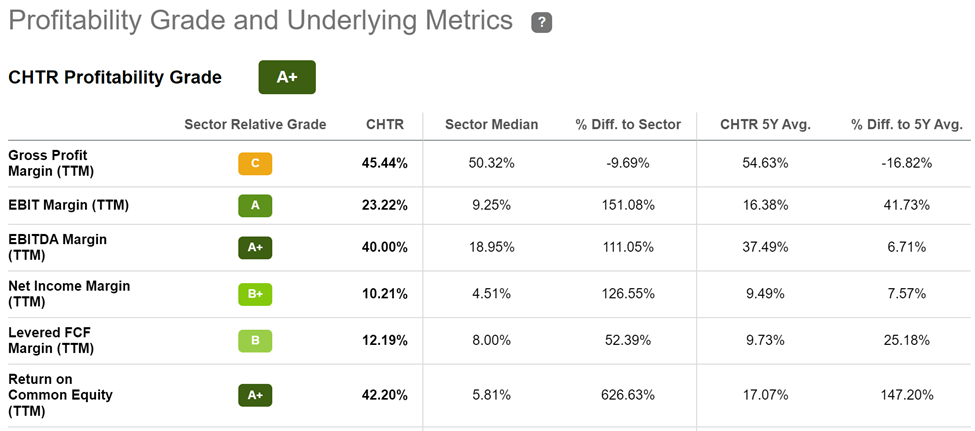

This is reflected by CHTR’s A+ profitability grade. As shown below, CHTR generates strong EBITDA and Net Income margins of 40% and 10%, respectively, which are more than double that of the sector medians.

CHTR Profitability (Seeking Alpha)

Meanwhile, CHTR is seeing healthy growth, as total residential and small and medium business internet customers rose by 75,000 during the third quarter, to 30.3 million total customers. More importantly, CHTR is quickly ramping up its mobile service as it grew residential and SMB mobile lines by a more robust 396,000. These factors contributed to revenue growing by 3% YoY to $13.6 billion and adjusted EBITDA grew by 2.4% YoY to $5.4 billion.

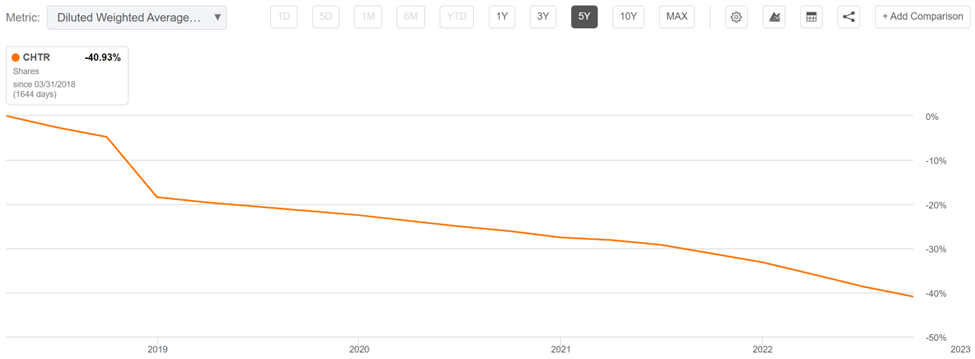

True to its form, CHTR doesn’t pay dividends, but rather returns capital to shareholders in the form of share buybacks, which are more tax efficient for investors. This included the repurchase of 5.8 million shares for $2.6 billion in the last reported quarter. As shown below, CHTR has substantially reduced its share count by a very high 41% over the past 5 years.

CHTR Shares Outstanding (Seeking Alpha)

Looking forward, CHTR has a large greenfield opportunity in mobile, as it’s still at the early stages of developing this business. Management estimates that it’s only captured 28% of its combined household spend on wireline and mobile connectivity across its footprint, leaving plenty of opportunity to add mobile customers through bundled home internet packages.

It’s worth noting, however, that CHTR likely won’t be able to maintain the same level of share buybacks going forward as management seeks to upgrade its network from its existing DOCSIS 3.1 infrastructure to DOCSIS 4.0. This is driven by high usage from its customer base. For example, management noted that internet customers who do not buy traditional video from CHTR use nearly 700 gigabytes per month on average, and nearly 25% of those customers use a terabyte or more of data per month, with a downstream to upstream ratio of 14:1.

Hence, the DOCSIS 4.0 infrastructure is needed, as management seeks to offer download speeds of 5 Gbps across the vast majority of its service territories and top-tier speeds of 10 Gbps by 2025. At a recent investor day, management pegged the cost of the upgrade to be at $5.5 billion spread across 3 years, and expects the following progress by the end of 2025, noting as follows in a report by FierceWireless:

Charter will move into Phase 3 in late 2024, deploying extended spectrum DOCSIS 4.0 in the remaining 35% of its footprint to enable download speeds of up to 10 Gbps. Between all the cable upgrades, DiGeronimo (Charter’s president of Product and Technology) said Charter expects to be able to offer 5/1 Gbps speeds to 85% of its footprint by the end of 2025. He added the operator also plans to offer a fiber-on-demand product which will be capable of delivering symmetrical speeds of 25 Gbps or more to customers who want it.

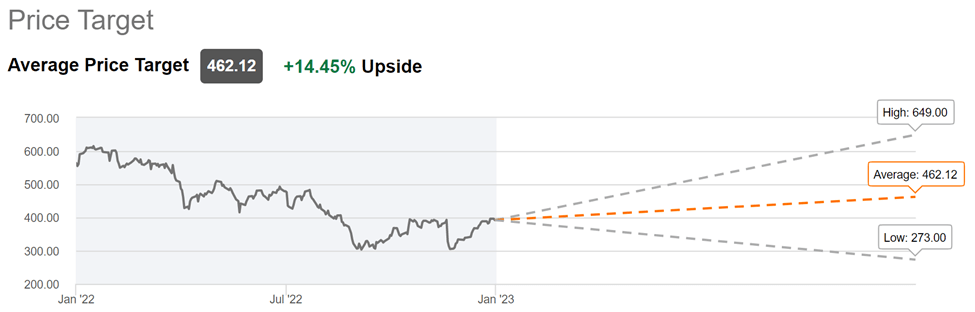

Meanwhile, it appears that the market has already discounted CHTR for its capital spend on the horizon, as the shares currently trade at $403.76 with a forward PE of 12.6. This appears to be too cheap, considering that analysts expect 11% to 24% annual EPS growth over the next 2 years. Analysts have a consensus Buy rating on CHTR with an average price target of $462, which translates to a potential one-year total return in the mid-teens and potentially strong returns thereafter.

CHTR Price Target (Seeking Alpha)

Investor Takeaway

Charter Communications has a moat-worthy presence with its broadband services across the U.S. It’s investing in broadband infrastructure for next-generation speeds and has plenty of greenfield to grow its emerging mobile business. The share price remains heavily discounted from its 52-week-high, giving value investors the potential for strong long-term returns.

Be the first to comment