fotokostic

Investment Thesis

CF Industries (NYSE:CF) is a highly profitable and very well-managed business. In the very near term, fertilizer prices have rolled off, as farmers push back against higher fertilizer costs.

The additional impact for CF Industries had been that its input costs were elevated on the back of higher natural gas prices. But this has now changed, with natural gas prices falling dramatically.

However, when all is said and done, the business is making record free cash flows and buying back shares.

I highlight that in the current quarter, free cash flows were up 65% y/y. And there’s every indication going that 2023 could be just as strong as 2022.

What’s Happening Right Now?

CF Industries has been impacted by the same factors as other potash fertilizer companies. However, CF Industries has had one additional factor impacting its results too, and that was higher natural gas prices.

When natural gas prices go higher, since it’s an input cost for the production of nitrogen, this directly impacts CF’s free cash flow potential. I’ll discuss its free cash flow in a moment.

USDA website

However, keep in mind that in the past few weeks natural gas prices have plummeted. What’s more, consider this,

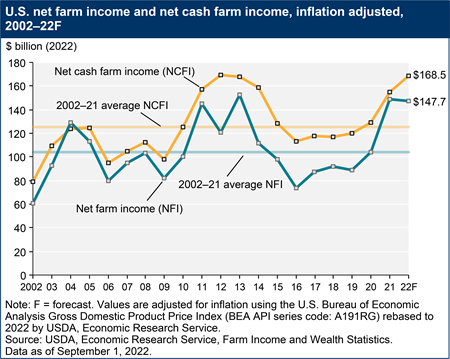

Net farm income, a broad measure of profits, is forecast at $147.7 billion in calendar year 2022, an increase of $7.3 billion (5.2 percent) in 2022 relative to 2021.

As you can see here, net farm income is strong, which is conducive for farmers to pay up for fertilizer. But for now, farmers are pushing back. And my contention is that they can’t push back for too much longer.

In essence, I believe that in early 2023, in the spring application season, farmers will have to return to buying fertilizer. And when they do, that’s going to lead to nitrogen prices increasing.

However, for my bullish thesis to work, I don’t need any massive heroics or squeezes in the nitrogen price. I just need things to remain steady or for volumes to improve slightly.

Oozing Free Cash Flow

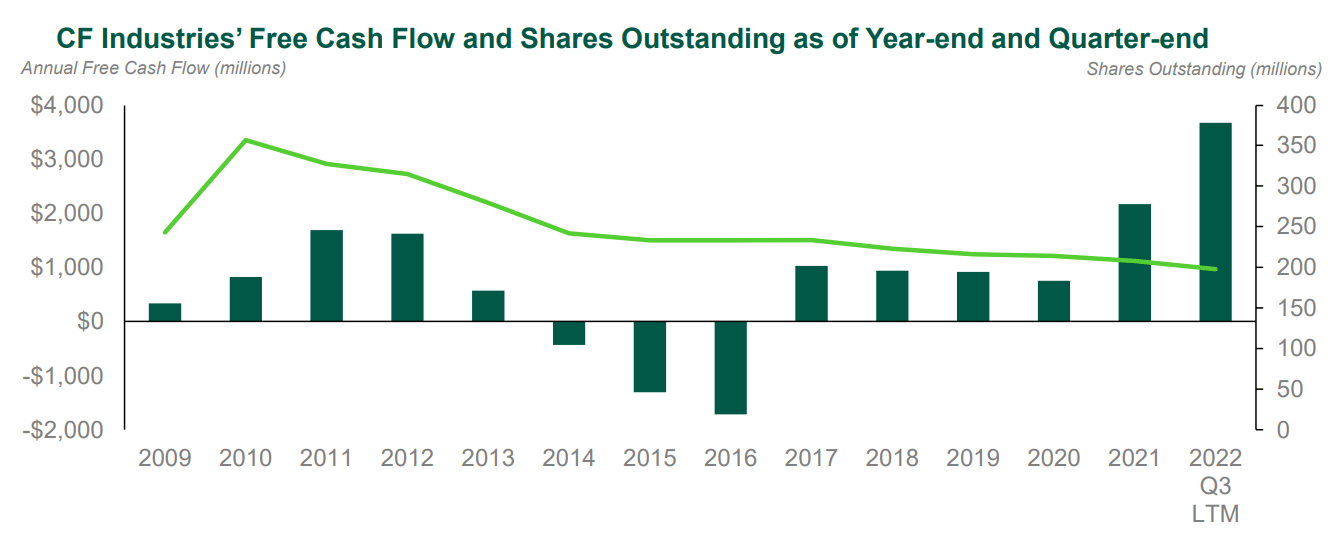

For Q3 2022, CF’s free cash flows were $800 million, up 65% y/y from $486 million in Q3 of last year.

Incidentally, I should remind members that out of this $800 million of free cash flow seen in the quarter, stock-based compensation was $10 million! No typo. Again, this is why I love investing in commodities.

CF Q3 2022 presentation

The graphic above adjusts for CF’s noncontrolling interest. And despite all these subtractions, CF’s free cash flows are moving up and to the right.

And that excess free cash flow is being used to repurchase shares at a very steady clip. And that’s why on the back of revenues being up 70% y/y, CF’s EPS figures went from negative $0.86 to $2.18. A change that is not even mathematically calculable!

Meanwhile, you can see the number of shares outstanding coming down on the thin green line, in the graph above.

And now we’ll discuss its valuation.

CF Stock Valuation — Approximately 5x FCF

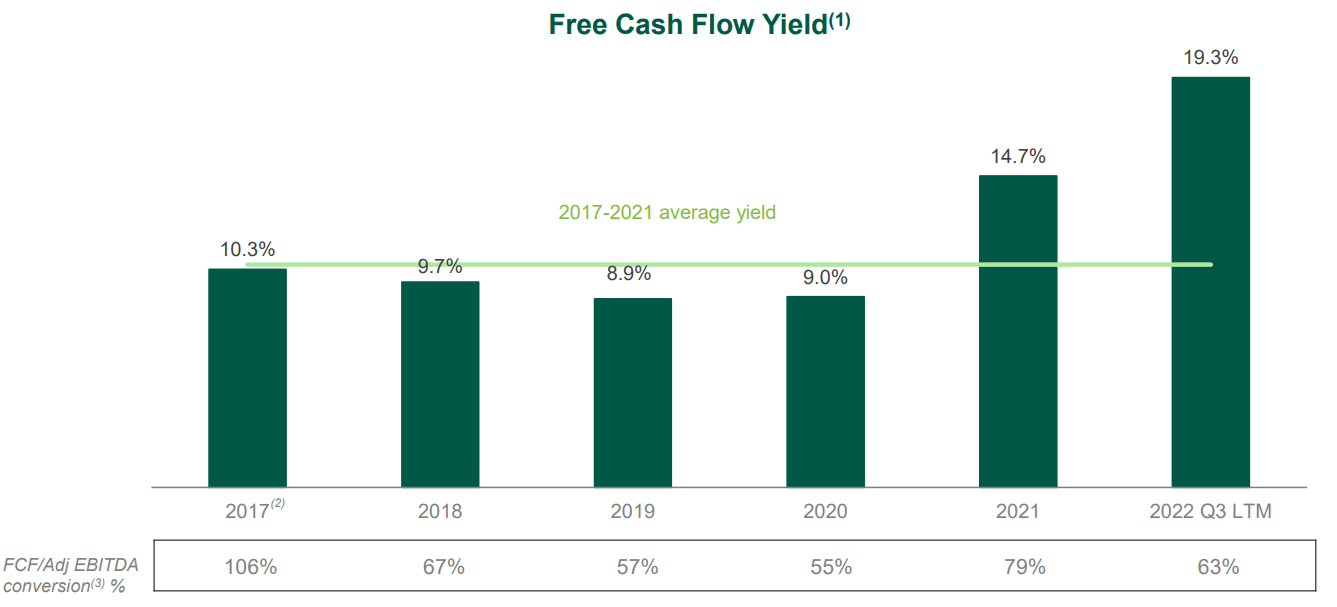

The graph that follows is self-explanatory.

CF Q3 2022 presentation

We can see that right now, the free cash flow yield is significantly higher than the 2017-2021 period.

This leads many investors to charge that CF Industries is over-earning and that it must therefore mean revert lower.

However, after everything that we have discussed, I believe you’ll agree, that even if CF Industries were to see nitrogen prices coming down in 2023, they are not likely to come down 50% anytime soon.

Put another way, even if over the next twelve months CF Industries’ free cash flow goes from $3.7 billion to $2.6 billion, for a 30% reduction, that would still only leave CF Industries priced at less than 8x next year’s depressed free cash flows.

That’s really very cheap.

The Bottom Line

The way I think about it is like this. I’m now being asked to pay somewhere around 5x to 8x FCF. That means that if I buy into CF Industries now, and hold the business for 5x to 8x years, then this business pays for itself.

But then, on top of that, I must keep in mind, that CF Industries is repurchasing nearly 5% to 10% of its market cap over the next twelve months.

That means that within 4 to 7 years, very approximately, my investment has paid for itself. And everything that this fertilizer company makes after years 4 or 7, depending on how things unfold, over the next +20 years, is all my upside coming for free.

Now, I’m not saying that one needs to hold onto a fertilizer producer for several years. But I’m saying that thinking in this way, the business is clearly not going away. And CF will continue to buy back shares.

And I can increase my total ownership of CF over time, without having to deploy any more capital. That’s really a very attractive investment profile. Particularly in an environment where I can see that food prices are very high around the world. I can participate in that inflationary environment, without having to do anything. Just from sitting and getting paid over time.

Be the first to comment