Sensay

Situation Overview

Cengage (OTC:CNGO) is facing a near-term maturity wall. The bond is due on June 15, 2024 and there is a springing maturity on its term loan, which means that if the bond is not refinanced 90 days ahead of the stated maturity, the ~$1.6 billion term loan becomes due immediately. This puts the nearest maturity date for Cengage in March 2024 or roughly one year from now.

I believe there are a lot of refinancing solutions for Cengage. Cengage is not the most straightforward refinance case but the business should be financeable. It operates in an oligopoly market structure and the demand has been relatively stable over economic cycles. In fact, past labor-market-led recessions (let’s assume we are headed for one) have boosted enrollments as unemployed workers need to retrain their skills. Even If all straight refinance effort fails, I believe the majority owner, Apax Partners, will backstop the deal to protect their equity interest.

Company Description

Cengage Learning is an education and technology company that provides innovative teaching, learning and research solutions for the academic, professional and library markets. It offers a range of resources, including textbooks, e-books, digital solutions, and educational technologies to help students, instructors and institutions achieve their learning and teaching goals. Cengage Learning has a diverse portfolio of well-known brands, including Gale, National Geographic Learning, and Heinle. The company is dedicated to delivering content and technology that engage students and support success in the classroom and beyond. Cengage Learning’s mission is to help people develop the skills they need to succeed in their careers and personal lives.

Capital Structure

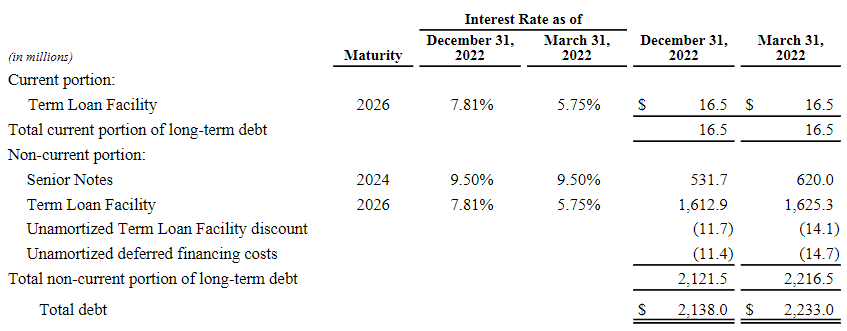

Cengage has a simple capital structure – a ~$1.6 billion first lien term loan and a senior unsecured bond. The senior unsecured bond had a face value of $620 million but the company has been buying back some bonds in the market. The face value is reduced to ~$530 million as of December 2022.

Quarter Report

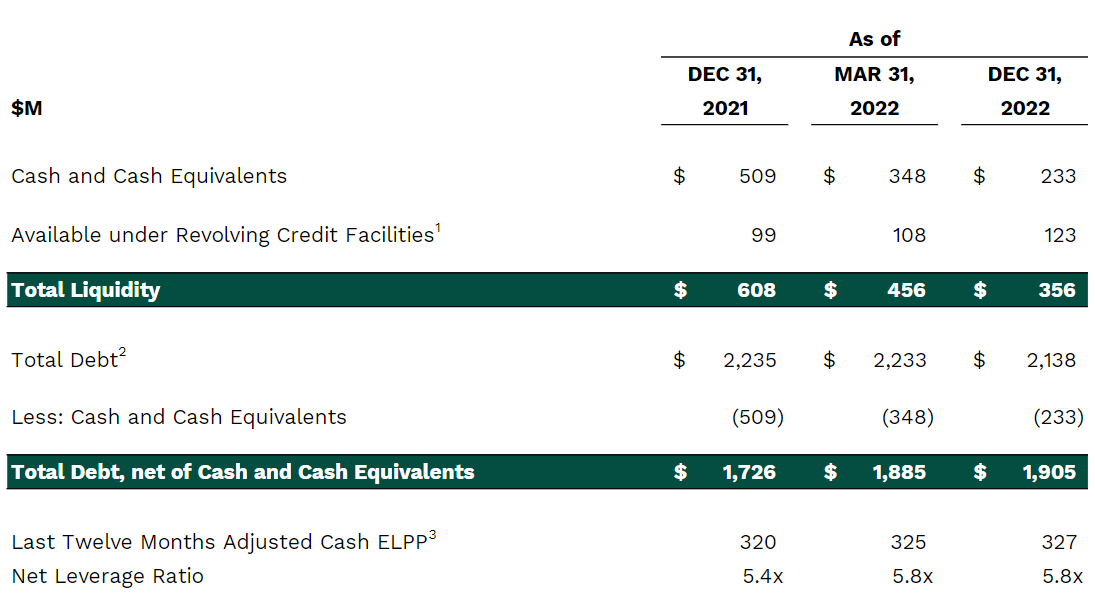

The leverage has increased from 5.4x to 5.8x in a year, but the company reconfirmed the guidance that net leverage will finish the fiscal year (March 31, 2023) at 5.3x. Cengage generally have good visibility to their business after the enrollment period and we are less than 2 months away from the date, so the guidance should be solid.

Company Presentation

Credit Market

The credit market seems to be wide open as the soft landing scenario takes over the narrative. The credit spread of the US high-yield market dropped to 424 basis points from the recent high of 550 basis points in September 2022. Cengage is a single-B credit and the spread on the single-B index is ~442 basis points, indicating a healthy market condition (Note that the bond is traded CCC due to the subordination of the unsecured bond but I believe Cengage will issue a second lien bond that could bring the rating closer to the parent rating of single-B).

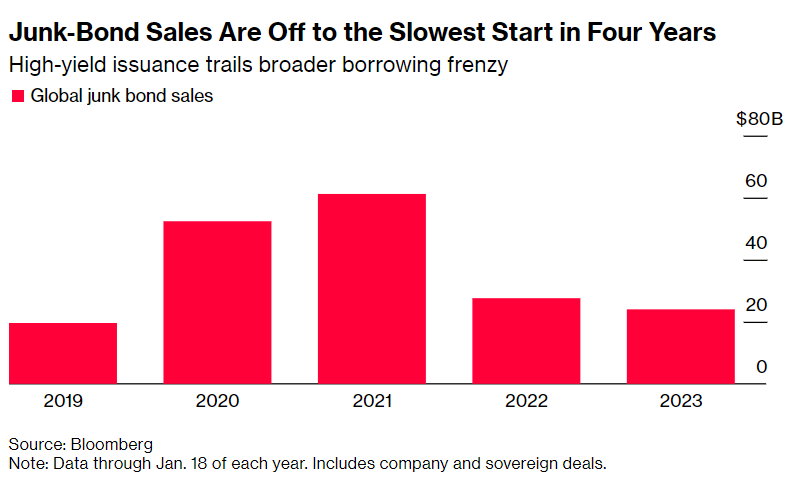

Although high-yield market new issuance is a little behind compared to history, it’s still very much open. We’ve also seen a number of issuers in the higher risk spectrum got priced. On the call, Cengage said that they are looking at all options. I believe the market is open to Cengage right now, it’s just a matter of pricing.

Bloomberg

Sponsor

Cengage is a long-time investment for Apax. It started with an LBO back in 2007. Cengage filed for Chapter 11 in 2014 but Apax was able to maintain the majority owner status by purchasing debt at a deep discount and exchanging them for new equities. Given the time and capital investment into Cengage, I highly doubt that Apex is ready to let this investment go. More importantly, there is too much equity value to give up. Pearson trades at ~10.5x EV/EBITDA, which means at ~5.3x leverage and ~$350 million EBITDA, ~$1.8 billion of equity value is at stake.

In addition, KKR, Searchlight Capital Partners, and Monarch Alternative Capital are the other equity owners. These are large institutional investors with deep pockets who can all potentially backdrop a refinancing deal.

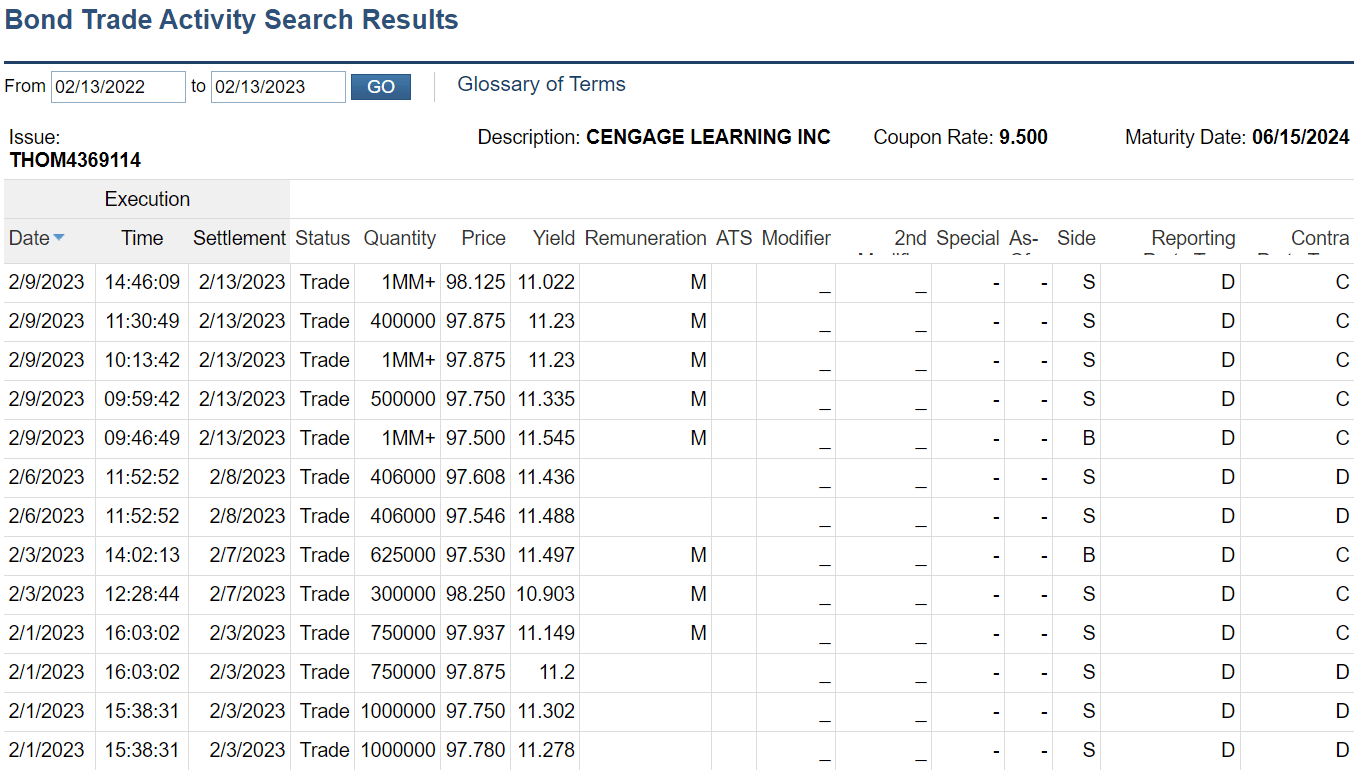

Cengage 9.5% 2024

I see $2 million bonds offered at $100.54. Below is a yield using this price and at different redemption dates. Given my view on the downside (which is essentially zero since I strongly believe the bond will be refinanced), investors can obtain an attractive yield between 3-9% depending on the holding period. I think if you are patient with the execution, it’s possible to get the bond below par.

TRACE

Conclusion

In this uncertain market environment, the return of capital is more important than return on capital. I believe Cengage is a unique situation that offers outsized yield and downside protection. My expectation is that Cengage will refinance the bond within 2023. The sponsors will do everything they can to help with the refinance if there is any hiccup.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment