morfous/E+ via Getty Images

This is an abridged version of the full report published on Hoya Capital Income Builder Marketplace on June 23rd.

REIT Rankings: Cell Towers

Hoya Capital

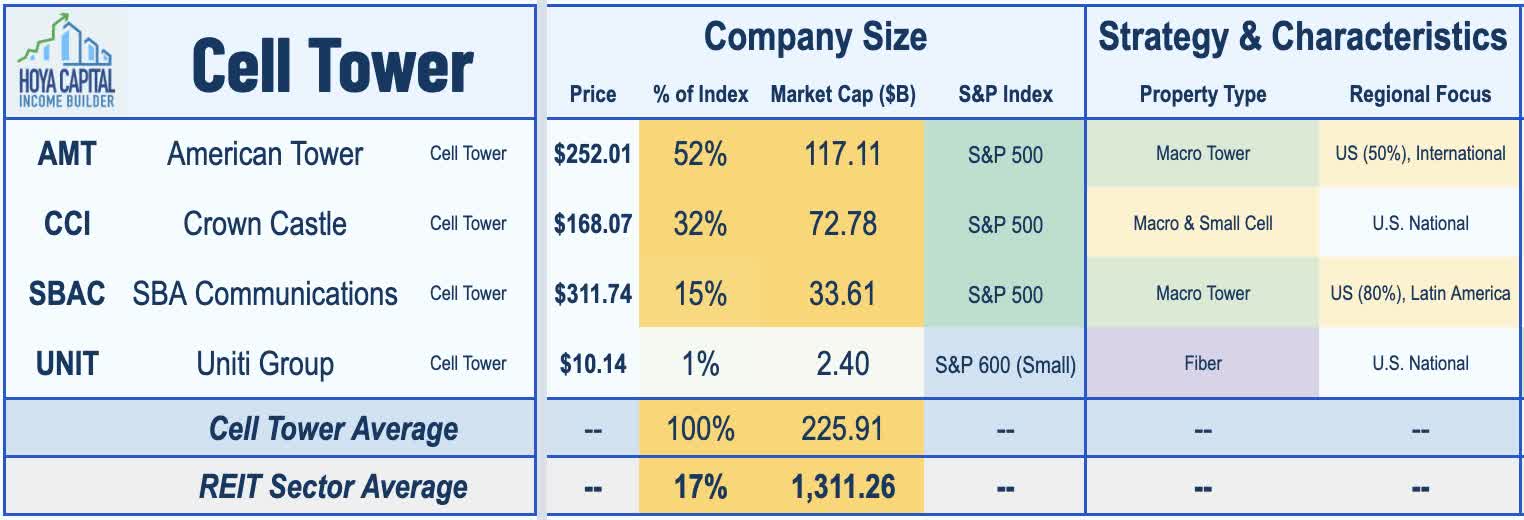

After uncharacteristically lagging for most of the year, Cell Tower REITs have been the best-performing property sector over the past quarter, benefiting from favorable macro shifts and positive industry-specific catalysts. Within the Hoya Capital Cell Tower REIT Index, we track the three Cell Tower REITs which account for roughly $225 billion in market value: American Tower (AMT), Crown Castle (CCI), SBA Communications (SBAC). We also track Uniti Group (UNIT), which owns a fiber-optic cable network that connects digital communications infrastructure. DigitalBridge (DBRG), which is tracked in the Data Center REIT sector, owns a minority stake in Vertical Bridge, which manages the fourth-largest cell tower portfolio in the U.S.

Hoya Capital

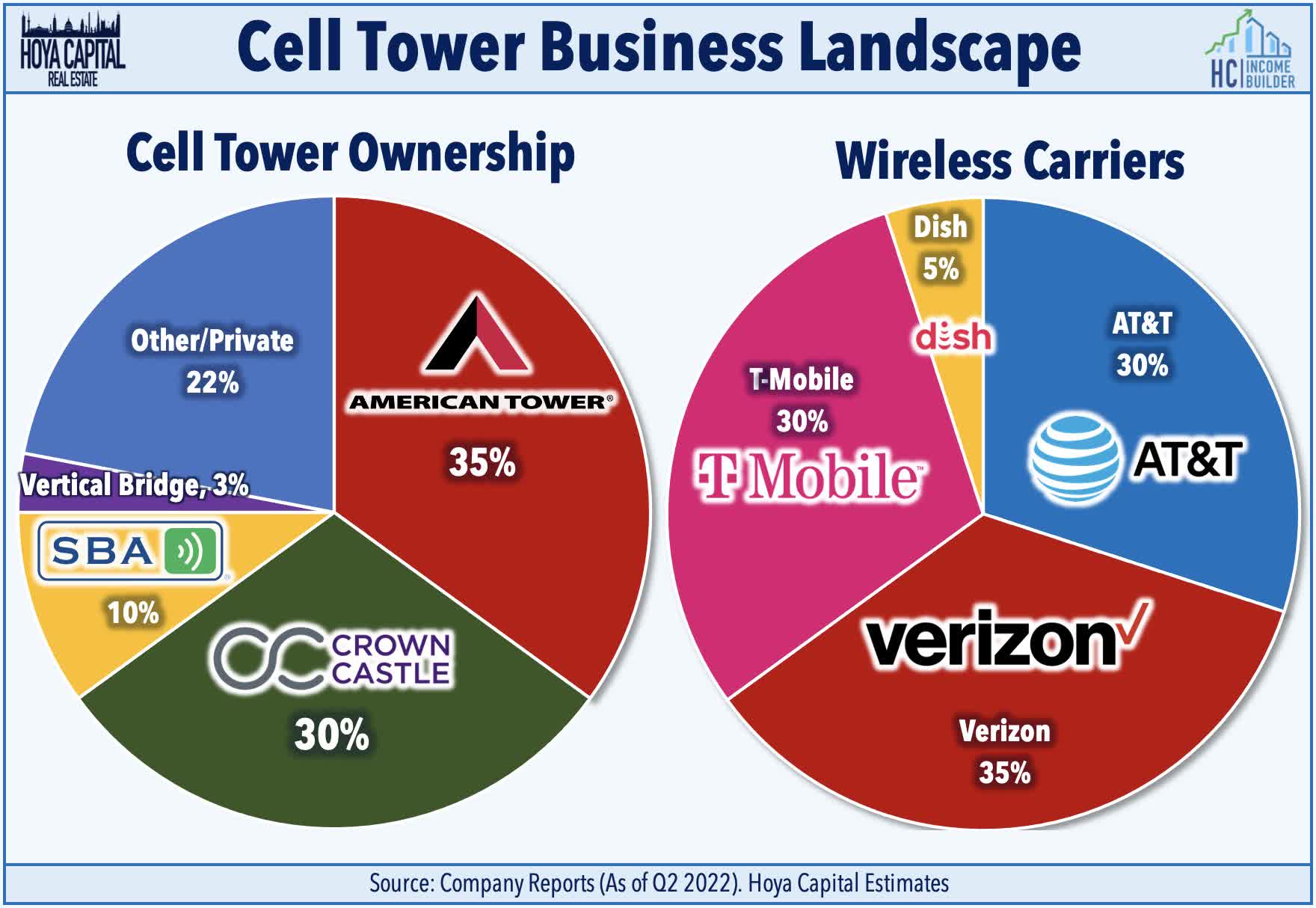

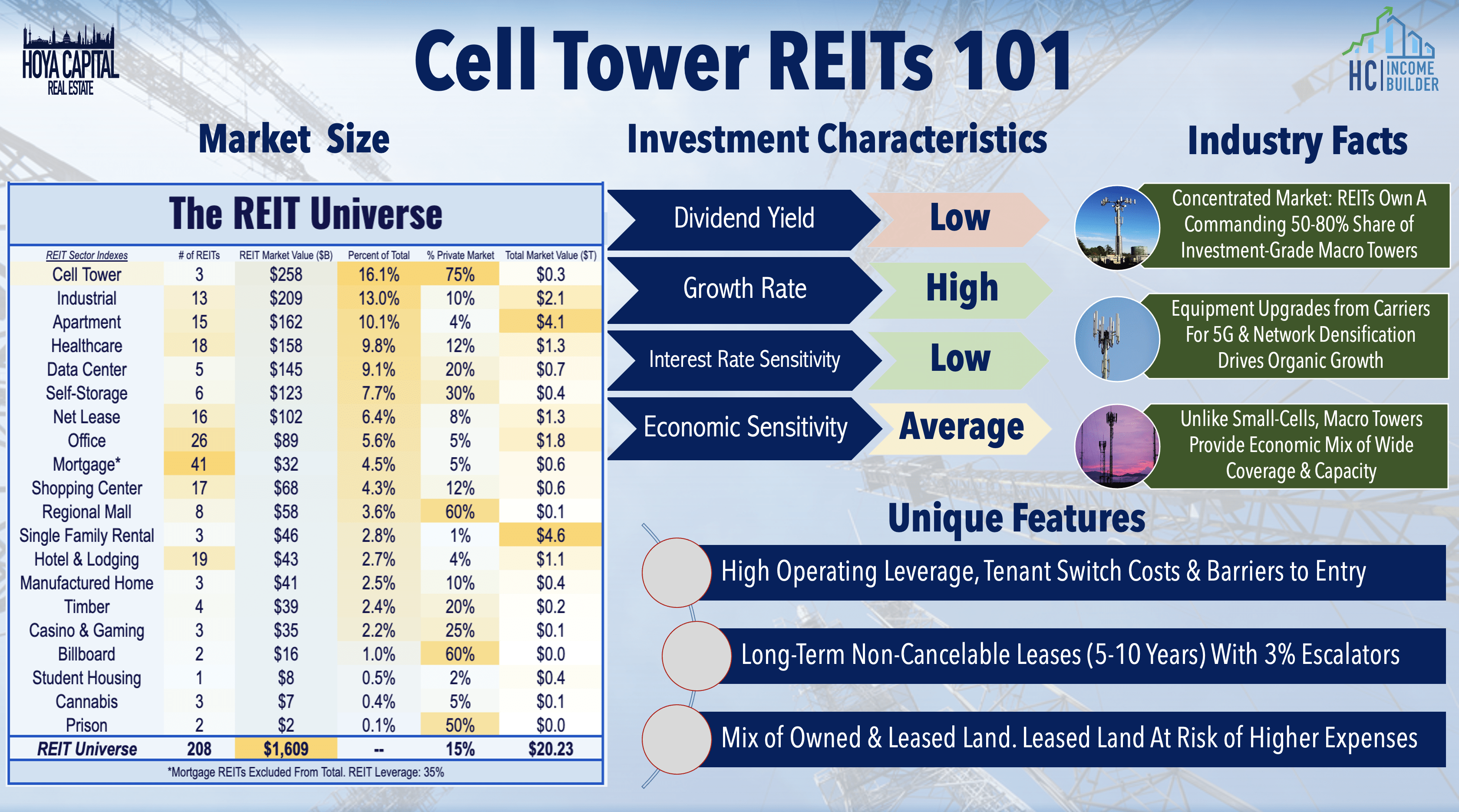

Cell Tower REITs are the single-largest property sector in the broad-based REIT indexes with a 10-20% weighting, but their relative dominance over the real estate sector is dwarfed by its dominance over the telecommunications sector, as these REITs control nearly 75% of wireless communication infrastructure in the U.S. and more than 50% in several major international markets. These REITs are the landlords to the four nationwide cellular network operators in the U.S.: AT&T (T), Verizon (VZ), T-Mobile (TMUS), and DISH Network (DISH), and own 50-80% of the 100-150k investment-grade macro cell towers in the United States.

Hoya Capital

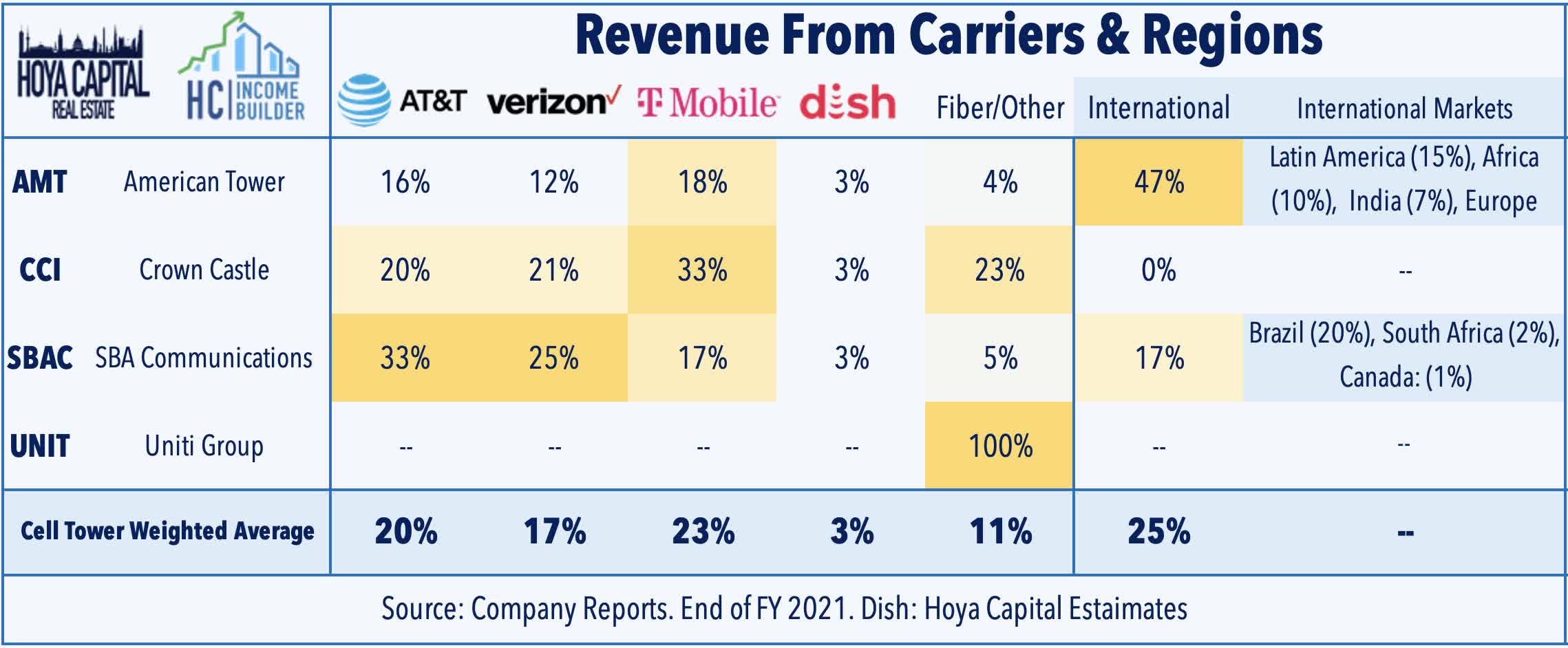

Facilitated by the more-favorable economics of “sharing” towers given the regulatory barriers to building new sites, the major carriers sold most of their tower assets to these REITs over the past two decades as AT&T sold nearly 10k towers to Crown Castle in 2013 and Verizon sold 11k towers to American Tower in 2015. Supply growth is almost non-existent in the US, and the relative scarcity of cell towers, combined with the absolute necessity of these towers for cell networks, has given these REITs substantial pricing power even as the number of potential tenants has dwindled down to just four national carriers over the last two decades. AMT generates nearly 50% of its revenue overseas with major operators in India, Brazil, and Mexico. SBAC generates roughly a fifth of its revenue from international markets with major operations in Brazil. CCI and UNIT focus exclusively on the United States.

Hoya Capital

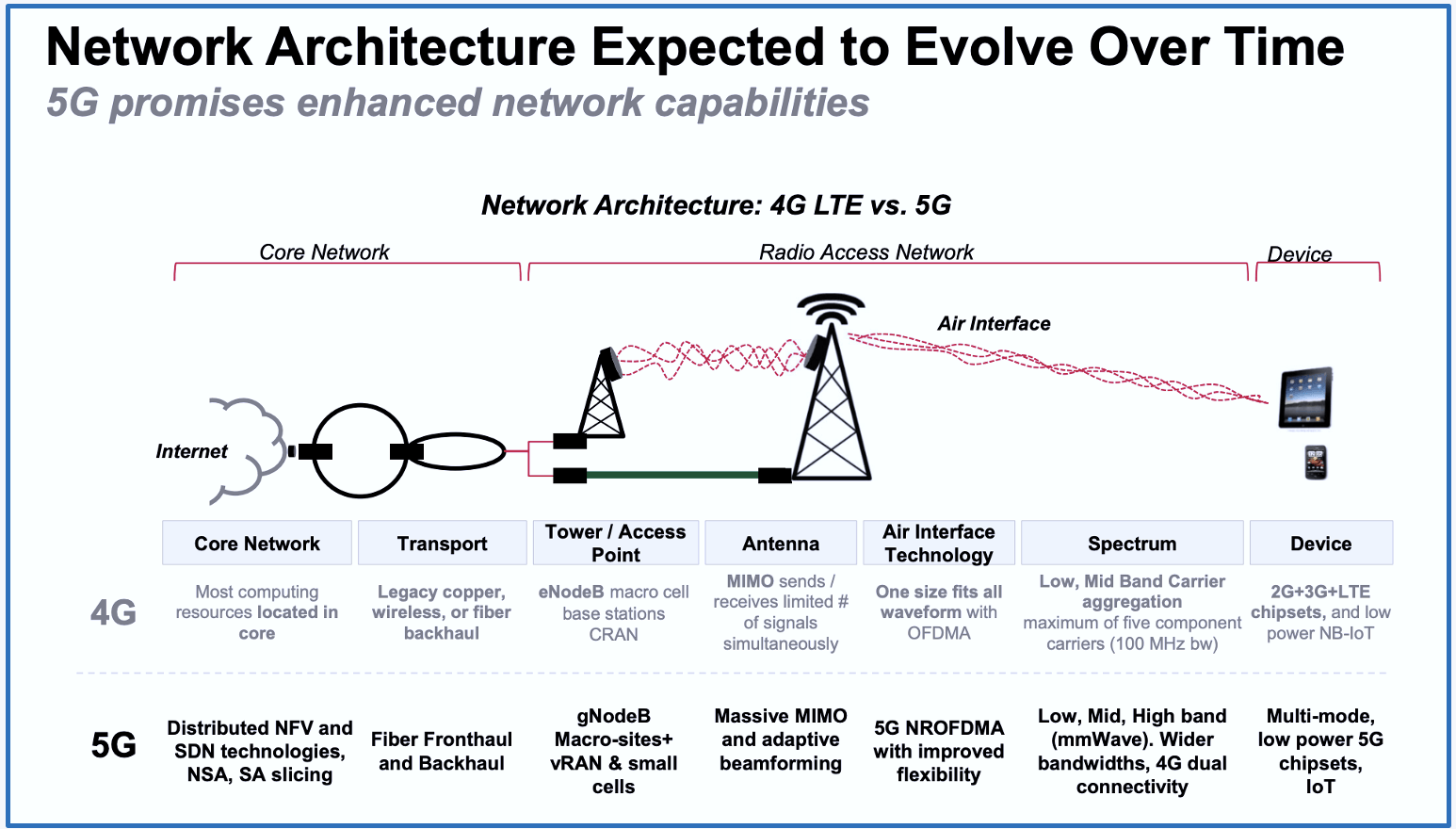

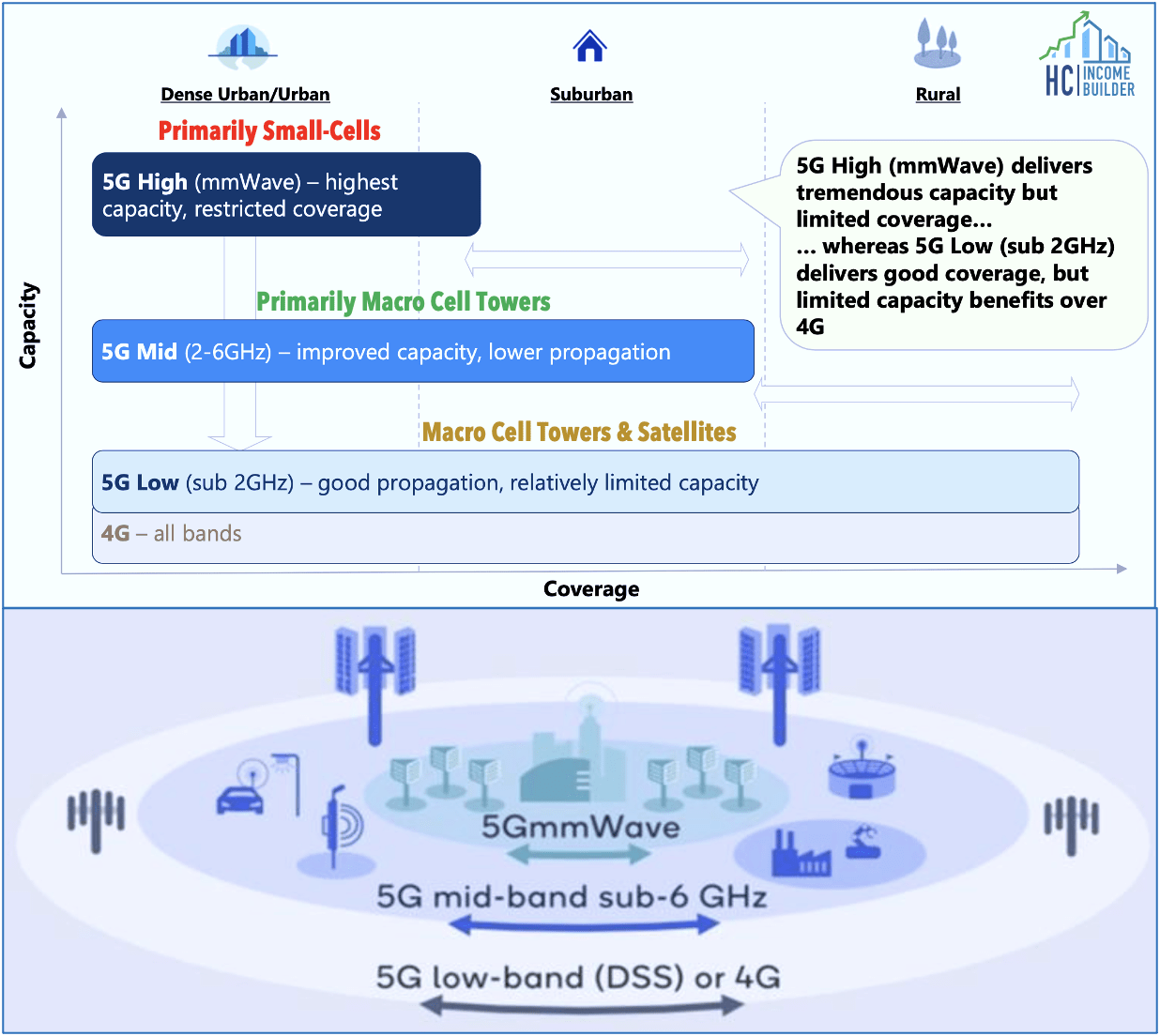

This commanding competitive positioning has given these REITs substantial pricing power amid the roll-out of 3G, 4G, and 5G wireless networks, which has translated into enviable shareholder returns. While 4G networks gave us the “streaming” and “e-commerce” age, pioneered by Amazon (AMZN) and apps like Uber (UBER) and Spotify (SPOT), 5G networks are expected to spur a new wave of technological innovation fueled by “fiber-like” speeds and ultra-low latency over wireless nodes. 5G adoption in mobile devices has been propelled by the success of Apple’s (AAPL) lineup of 5G iPhones. Nearly 60% of smartphones in the U.S. now have 5G capability, but we continue to believe that home wireless broadband – called “Fixed Wireless Access” or “FWA” in the industry – is the true “killer app” of 5G, and many Americans will soon have 3-4 additional competitive home internet options.

Hoya Capital

With the launch of DISH Network’s 5G service this past week, the four major U.S. carriers now boast “nationwide” 5G networks, built primarily by upgrading equipment on existing macro towers, an upgrade cycle that drove record levels of leasing activity in 2021 and demand has actually accelerated into early 2022, powered in part by stronger-than-expected demand from DISH. Crown Castle noted on its earnings call:

“We had the highest level of activity in the company’s history during 2021, and we’re expecting that level of activity to continue into ’22. What’s really unique about this cycle is that we’ve got 4 carriers deploying. They’ve got a significant amount of spectrum to be deployed, and they have the capital to be able to deploy that. I can’t think of another time in the history of our business where we’ve had 4 well-capitalized carriers with the spectrum and the desire to deploy their network. The focus for the legacy carriers is to touch the sites where they are already existing on the assets – on the macro assets. And we would expect the next phase of 5G build-out will be to densify their network.

Hoya Capital

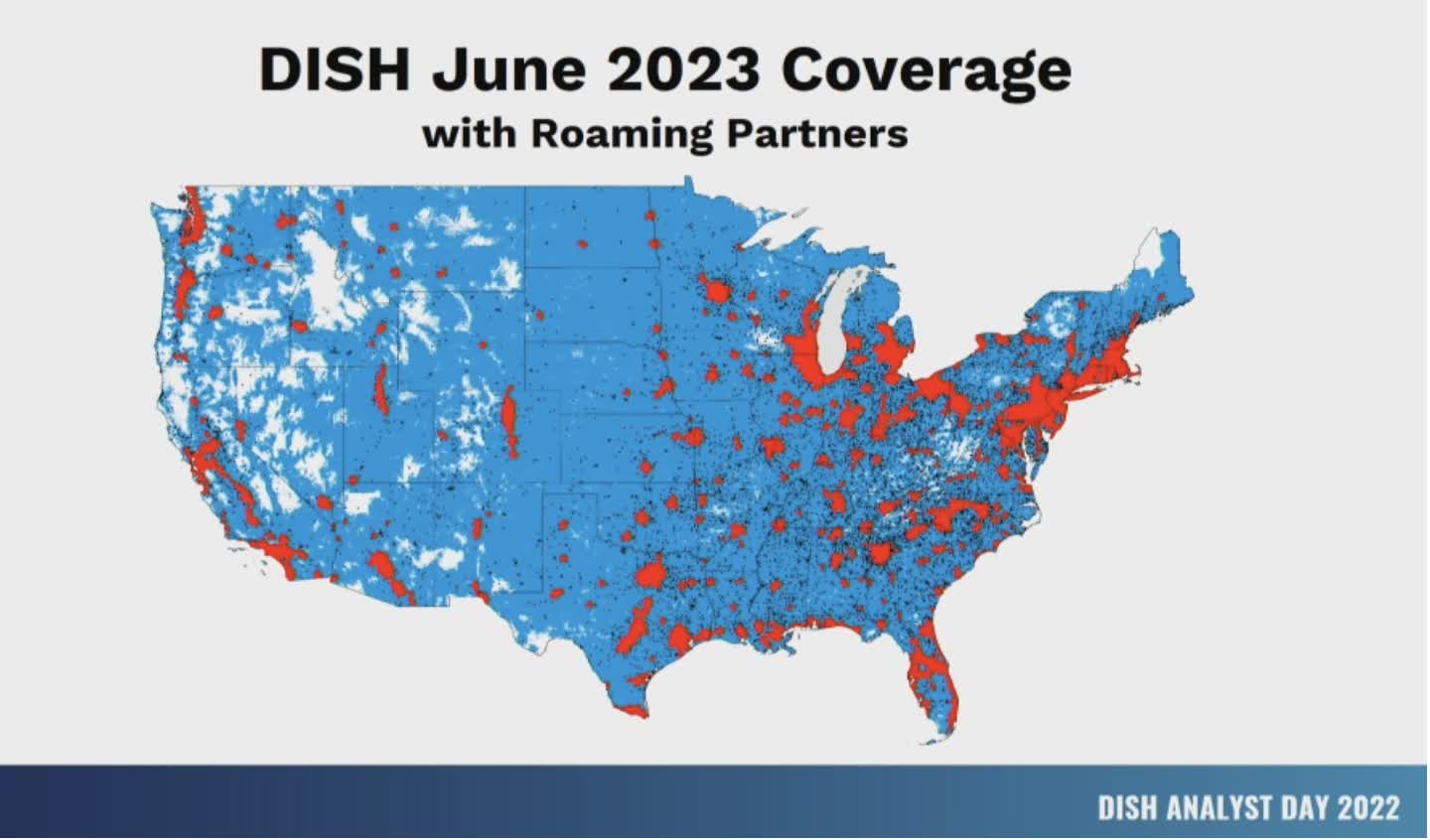

Tower leasing demand suggests that DISH intends to be a viable player, having now signed deals with both Crown Castle and American Tower for up to 20k sites each, as well as smaller deals with Vertical Bridge and SBA Communications. Given the industry skepticism over DISH’s viability, any level of success is incremental for tower REITs and is not “baked in” to the analyst numbers or guidance, in our view. DISH – which acquired Boost Mobile as part of the T-Mobile/Sprint merger – plans to compete as a low-cost provider by leveraging its existing satellite subscriber base and its network sharing agreement with T-Mobile and AT&T to provide immediate nationwide services as it deploys its 5G network, which currently covers 20% of the U.S. population. DISH is obligated to cover at least 50% of the population by mid-2023 under its agreement with the DOJ.

Hoya Capital

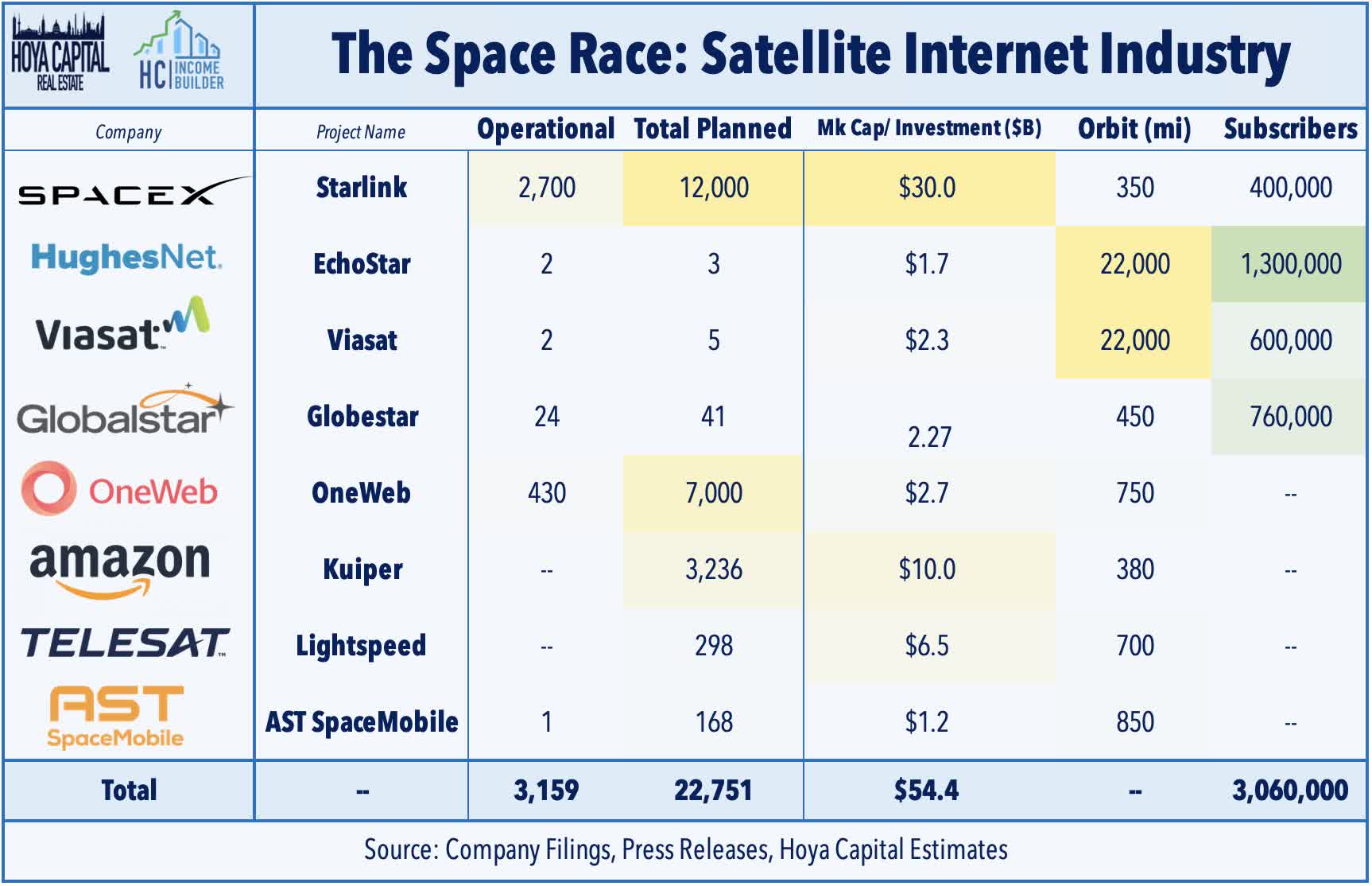

We continue to believe that DISH will require a well-capitalized partner to be viable, but we could certainly see mutual benefit in a deal with an emerging Low-Earth Orbit (“LEO) provider – Starlink, OneWeb, or Amazon’s Kuiper – that could establish DISH into a viable fourth option, which would be a clear positive for long-term tower leasing demand. Starlink – which has already deployed nearly 2,500 LEO satellites and recently surpassed 400k subscribers – is one of a handful of companies working on LEO broadband and related technologies. American Tower itself has made strategic investments in the LEO space through a partnership with AST SpaceMobile (ASTS), which seeks to provide satellite connectivity through traditional cell phone antenna systems, and its acquisition of data center REIT CoreSite is also a play on LEO networks to an extent, as network-dense data centers are ideal hosts for satellite ground stations that will become increasingly critical to minimize latency and provide sufficient capacity to meet broadband demand.

Hoya Capital

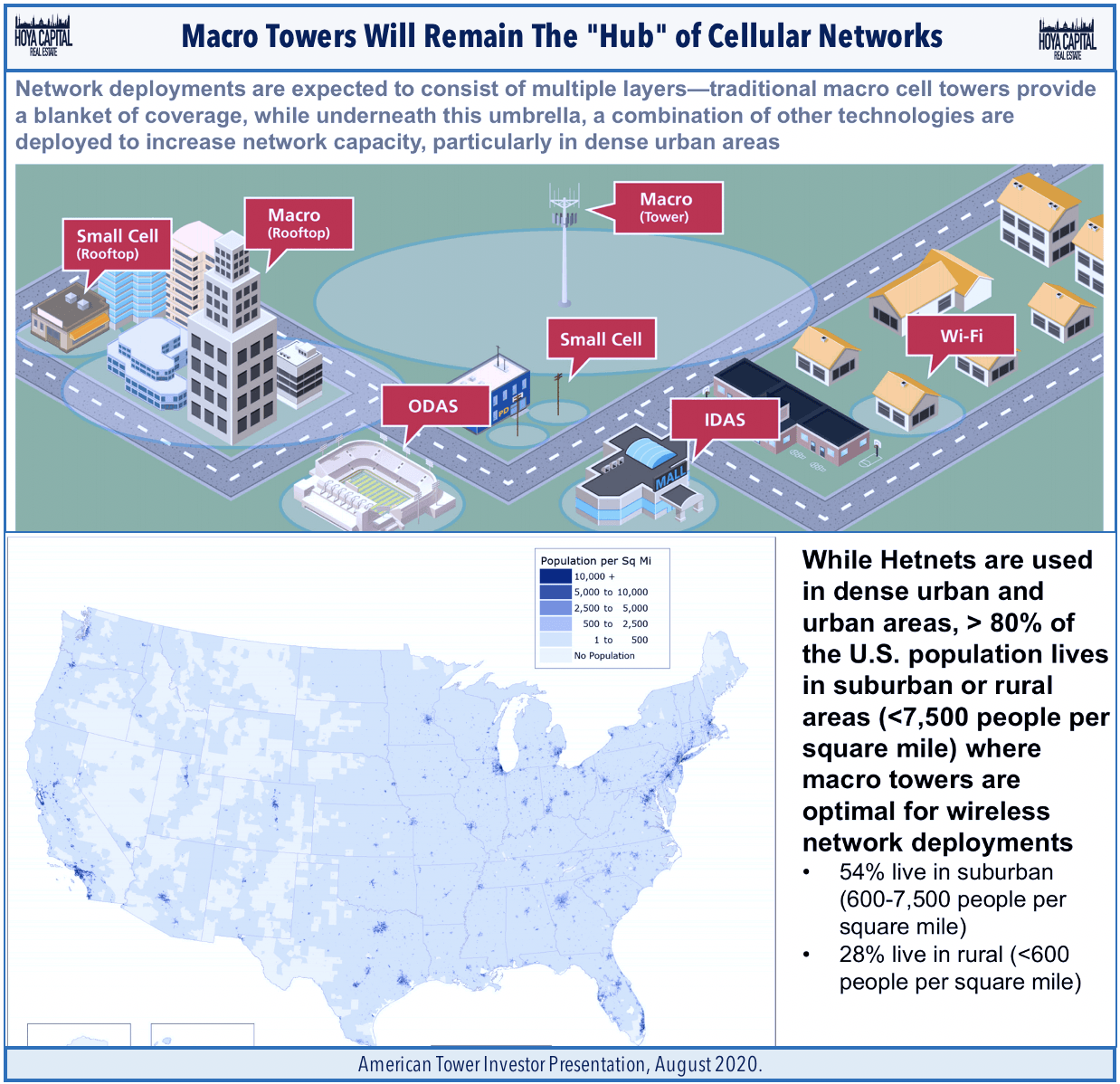

We continue to monitor – and be impressed by – the pace of Low Earth Orbit satellite service deployment. While there is some risk of disintermediation to towers if the mobility of satellite connections improves, we see a higher likelihood that LEO networks will be “customers” rather than “competitors” to tower REITs. Satellite internet has been around for decades through providers including EchoStar’s (SATS) HughesNet and Viasat (VSAT) that use geostationary satellites that are roughly 20k miles from earth, but LEO systems can theoretically provide 5G-like speeds through “constellations” of satellites that are several hundred miles above Earth. High-power “macro” cell towers currently provide the most economical mix of network coverage and capacity, and ground-based networks are almost certainly going to remain the most cost-effective means to provide coverage in urban and suburban environments for the foreseeable future.

Hoya Capital

The 5G deployment has continued despite the recent dust-up with the FAA and the airline industry, issues which have been largely resolved in recent months through modifications to antenna orientations and power output in the immediate vicinity of landing aircraft. 5G build-outs have so far focused on equipment upgrades at macro towers for broad mobile coverage using mid-band spectrum which is seen as the “sweet spot” for the ideal economical mix of coverage and capacity and is generally. The next phase of deployment will likely focus on network densification through small-cell nodes using higher-band spectrum, which will be needed to make home wireless broadband competitive performance-wise with traditional cable or fiber internet.

Hoya Capital

Cell Tower REIT Earnings

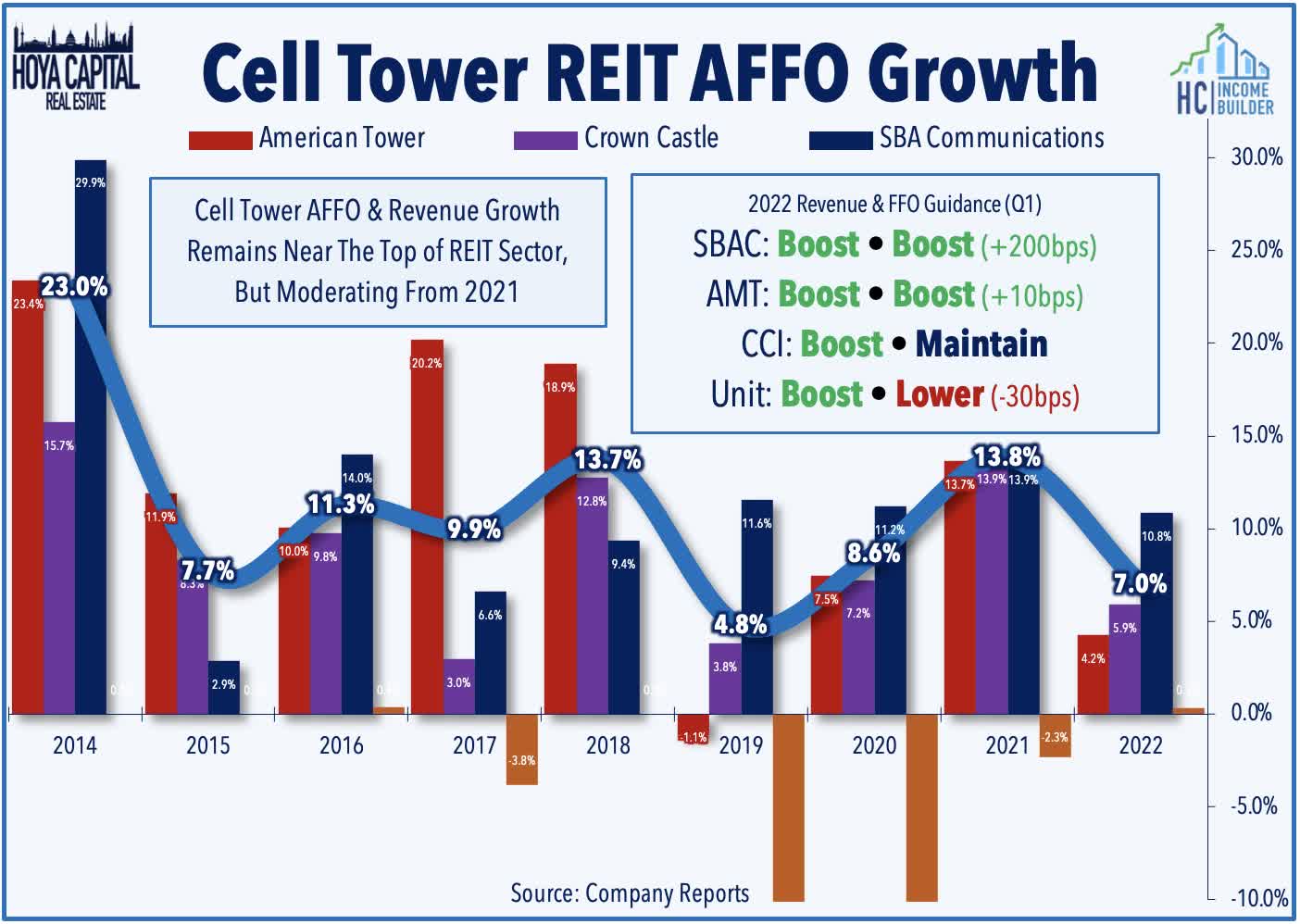

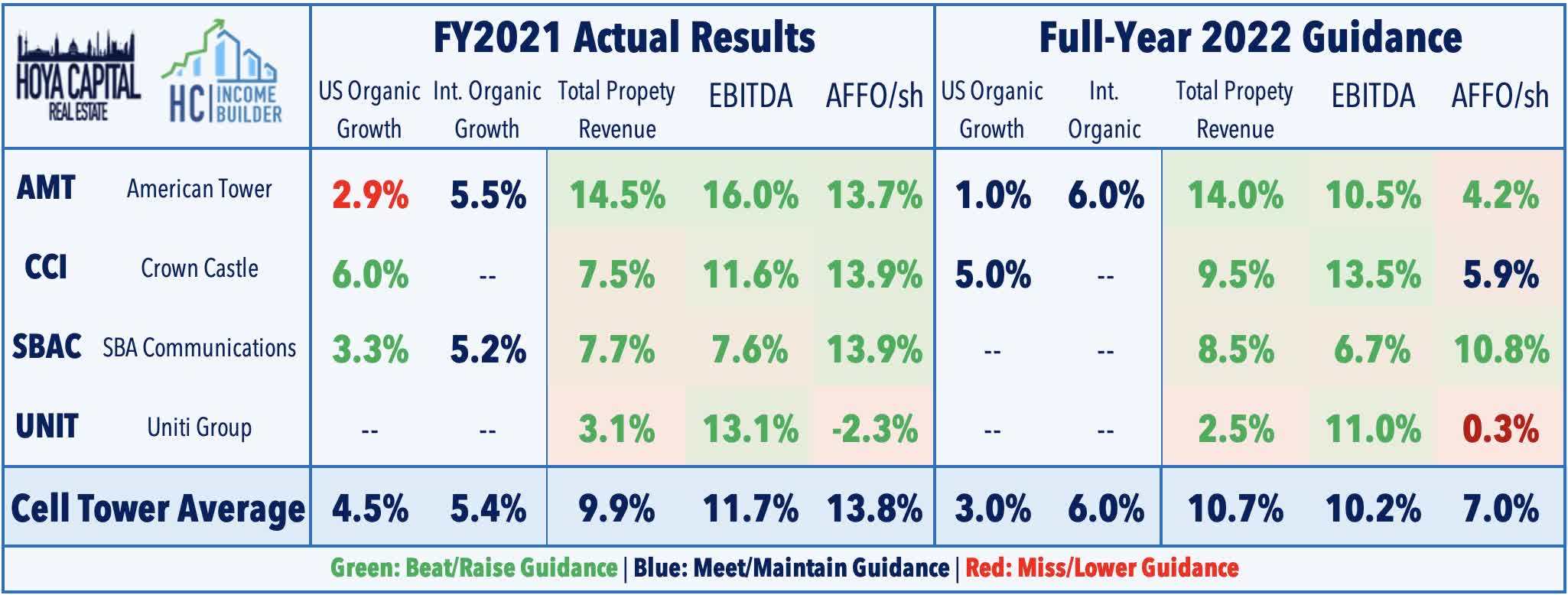

As discussed in our REIT Earnings Recap, cell tower REITs delivered another “beat and raise” quarter which notably highlighted the underappreciated inflation-hedging characteristics of cell tower REITs as international lease escalators are typically linked with local CPI. Driven by this added inflation boost in its Brazil market – which is roughly 20% of revenues and is recording double-digit lease escalations due to the CPI linkage – SBA Communications hiked its full-year FFO outlook by 200 basis points. American Tower also reported strong international results and raised its full-year AFFO growth outlook to 4.2% – up 10 basis points – and its full-year revenue growth outlook to 14% – up 80 basis points. Crown Castle – which is focused entirely in the U.S. – reported in-line results with no major changes to its outlook – modestly raising its full-year revenue growth outlook but maintaining its FFO guidance.

Hoya Capital

CCI commented on its earnings call: “With the three established network operators and a new intranet scale and DISH, all upgrading and developing nationwide 5G networks, the fundamentals in the U.S. market are as positive as I can remember during my 20-plus years at Crown Castle.” Uniti Group was the lone REIT to lower its full-year FFO guidance in Q1, fractionally lowering its outlook by 30 basis points. While cell tower REITs expect to see an uptick in churn related to the T-Mobile/Sprint merger to weigh on same-tower results over the next three years, earnings call commentary suggests that these REITs remain confident that incremental revenues from Dish will offset the drag following an initial moderation. AMT reiterated that it expects the effects of the churn to begin in Q4 of 2021 and will continue “out to 2024” with the biggest impact being in 2022, resulting in a 4% drag to full-year AFFO.

Hoya Capital

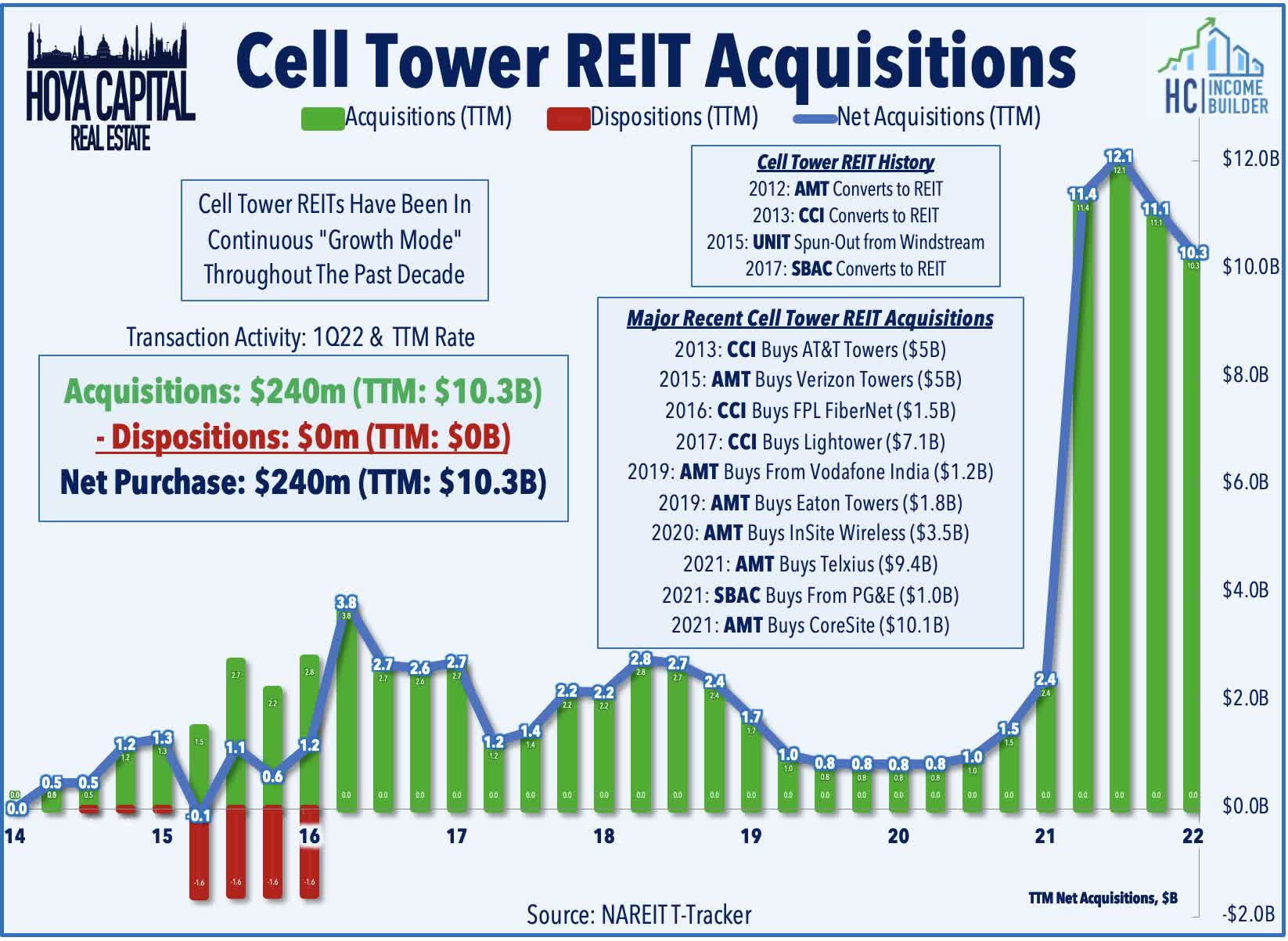

While same-tower growth is expected to moderate a bit over the next couple of years before rebounding around mid-decade, cell tower REITs have kicked their external growth initiates into a higher-gear over the last year, utilizing a sector-leading cost of capital and favorable competitive positioning to accretively expand their asset base. Just several months after closing on a $3.5B deal to acquire InSite Wireless which owns 3,000 communications sites in the U.S. and Canada, American Tower announced last January a $9.4B deal to acquire Telxius Towers, which owns 31,000 sites across Europe and South America. All three cell tower REITs also continue to expand and consolidate via smaller “one-off” acquisitions and deploying some capital into new tower builds.

Hoya Capital

Cell Tower REIT Stock Performance

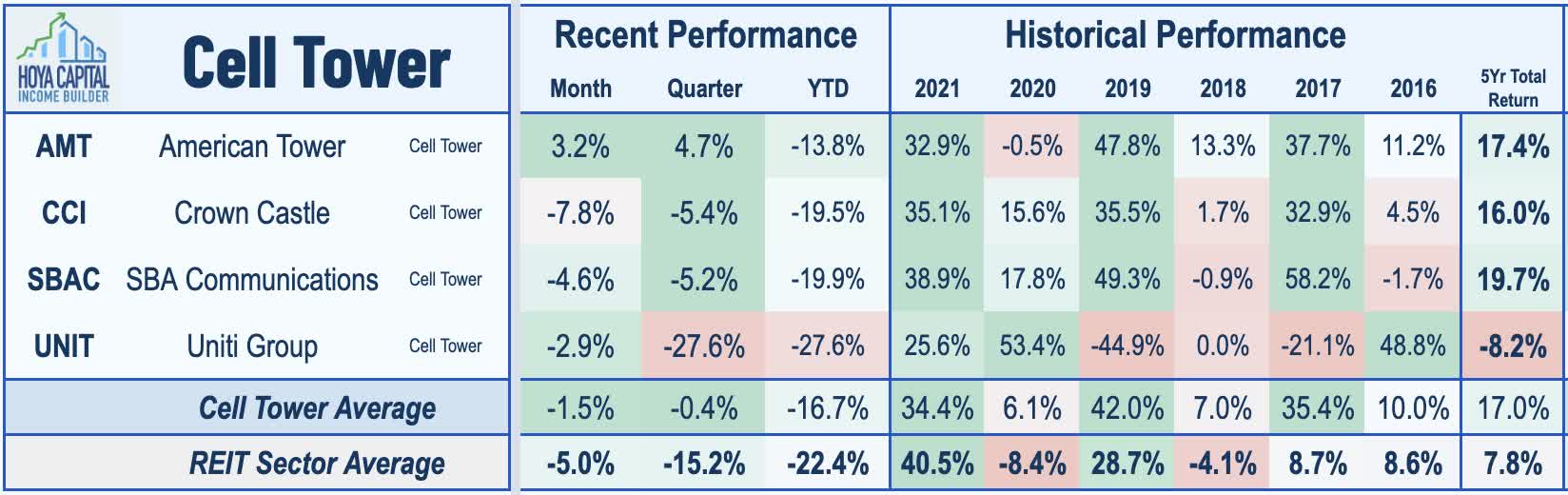

After uncharacteristically lagging for most of the year, Cell Tower REITs have been the best-performing property sector over the past quarter, benefiting from these favorable macro shifts towards “recession-resistant” market segments and positive industry-specific catalysts. While it has managed to erase its underperformance, the Hoya Capital Cell Tower REIT Index is still lower by roughly 17% in 2022, outperforming the broad-based Vanguard Real Estate ETF (VNQ), which has declined by 22%, and the S&P 500 ETF (SPY) which has declined by 21%

Hoya Capital

Cell Tower REITs snapped a six-year streak of outperformance in 2021 with total returns of 34%, trailing the 41% total returns on the Equity REIT Index, a streak of outperformance that was the second-longest in the REIT sector behind the Manufactured Housing REIT sector. Over the past five years, SBAC has delivered the highest average annual total return at 19.7% followed by CCI at 16.0% and AMT at 17.4%. Uniti Group has been a laggard over the past half-decade as it continues to work through legal issues with Windstream Holdings – its largest tenant.

Hoya Capital

Deeper Dive: Cell Tower Industry Dynamics

Cell tower REITs have benefited immensely from the increase in network spending from the four national carriers during the early stages of the 5G rollout, as carriers have focused early efforts on upgrading existing macro towers ahead of small-cell deployment. Due to the high concentration of ownership and significant barriers to entry in the United States related to restrictive zoning and the favorable economics of colocation, cell tower REITs are perhaps the only real estate sector that could be classified as true price makers rather than price takers.

Hoya Capital

Cell Tower REITs also stand to benefit from the adoption of “Edge” network architecture whereby data centers are located in close physical proximity to end-users or wireless networking hubs. We continue to see fixed wireless broadband – using a cell network for home or business broadband – as 5G’s true “killer app.” Sensing the competitive threat on their core wireline business from wireless broadband, Comcast (CMCSA) and Charter (CHTR) have made a push in recent years to compete in the cell business, primarily through “renting” capacity from the existing carriers as so-called “mobile virtual network operators” (MVNO) to supplement their public WiFi networks.

Hoya Capital

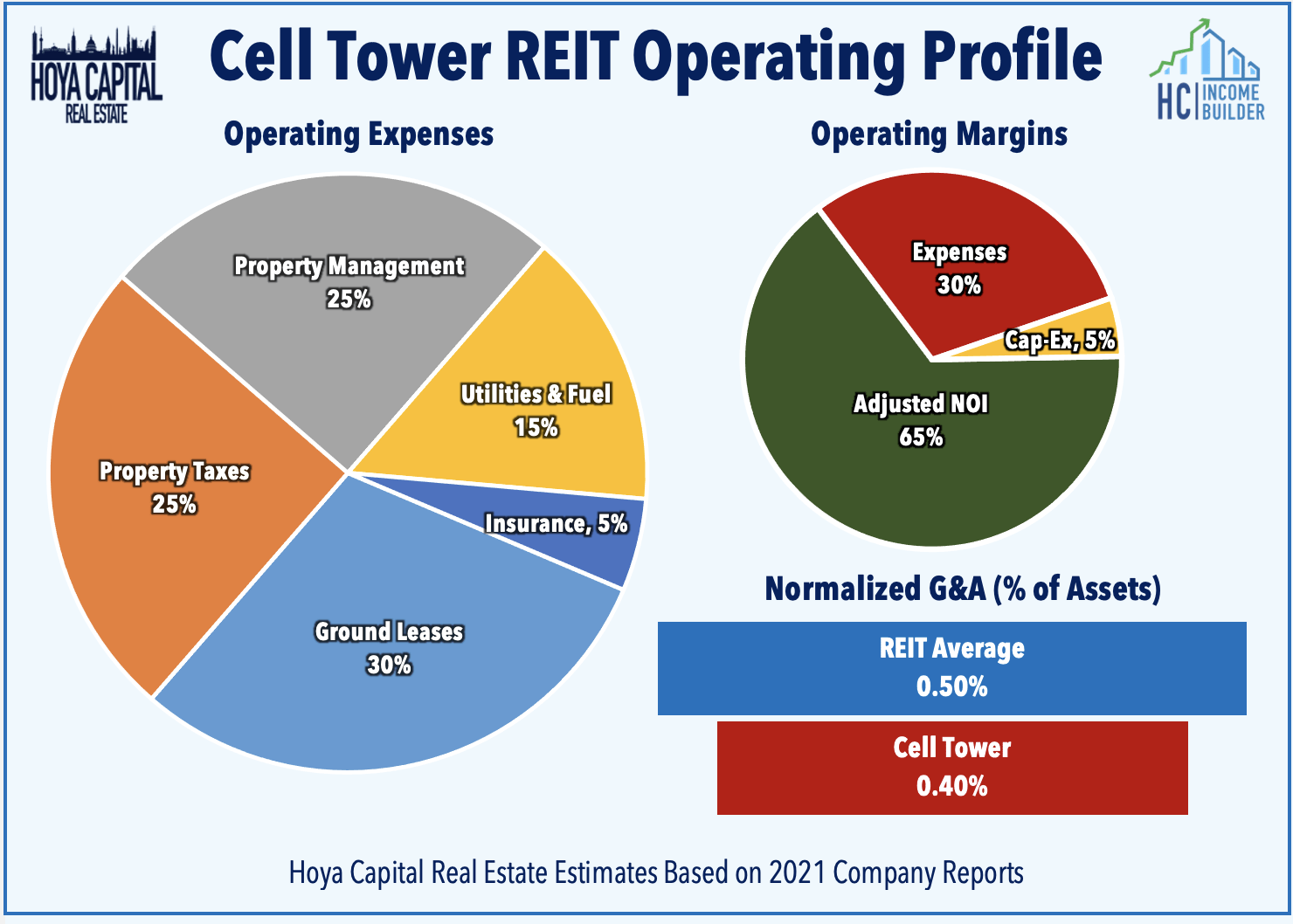

The typical cell tower operates equipment from multiple carriers and rental rates based on property location and the amount of equipment on the tower or on the ground site below. Cell tower leases are typically 5-10 years with annual fixed-rate escalators with multiple renewal options. Cell Tower REITs, however, only own about one-third of the land under the towers and control the rest through long-term ground leases, a source of potential long-term risk. EBITDA margins typically average around 60-65% for the Cell Tower REIT sector, towards the higher end of the real estate universe, with minimal ongoing cap-ex required relative to other REIT sectors.

Hoya Capital

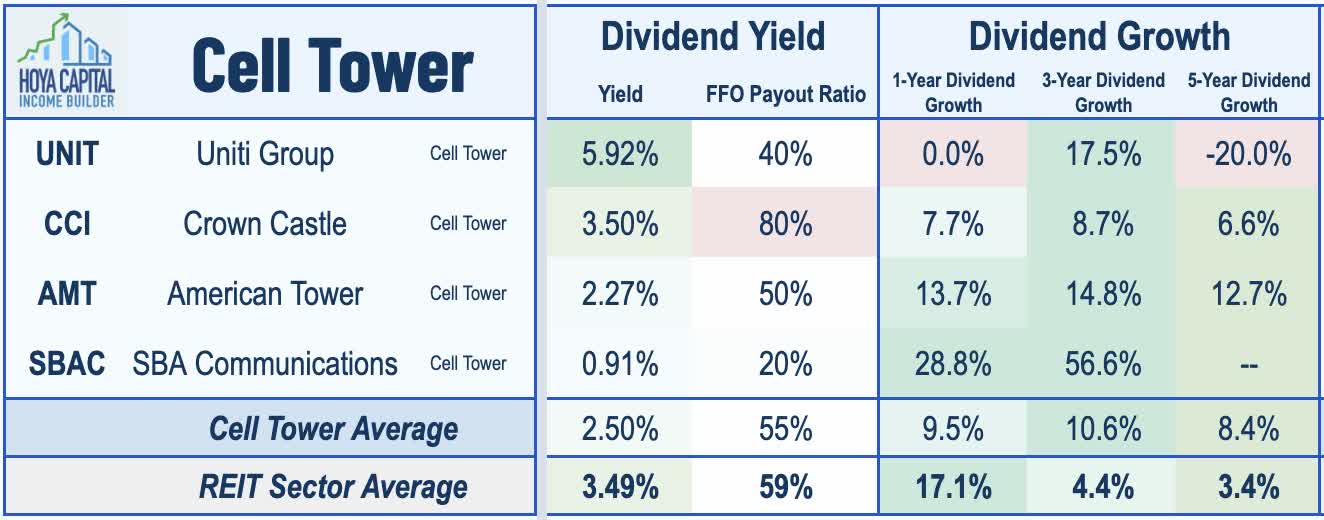

Cell Tower REIT Dividend Yields

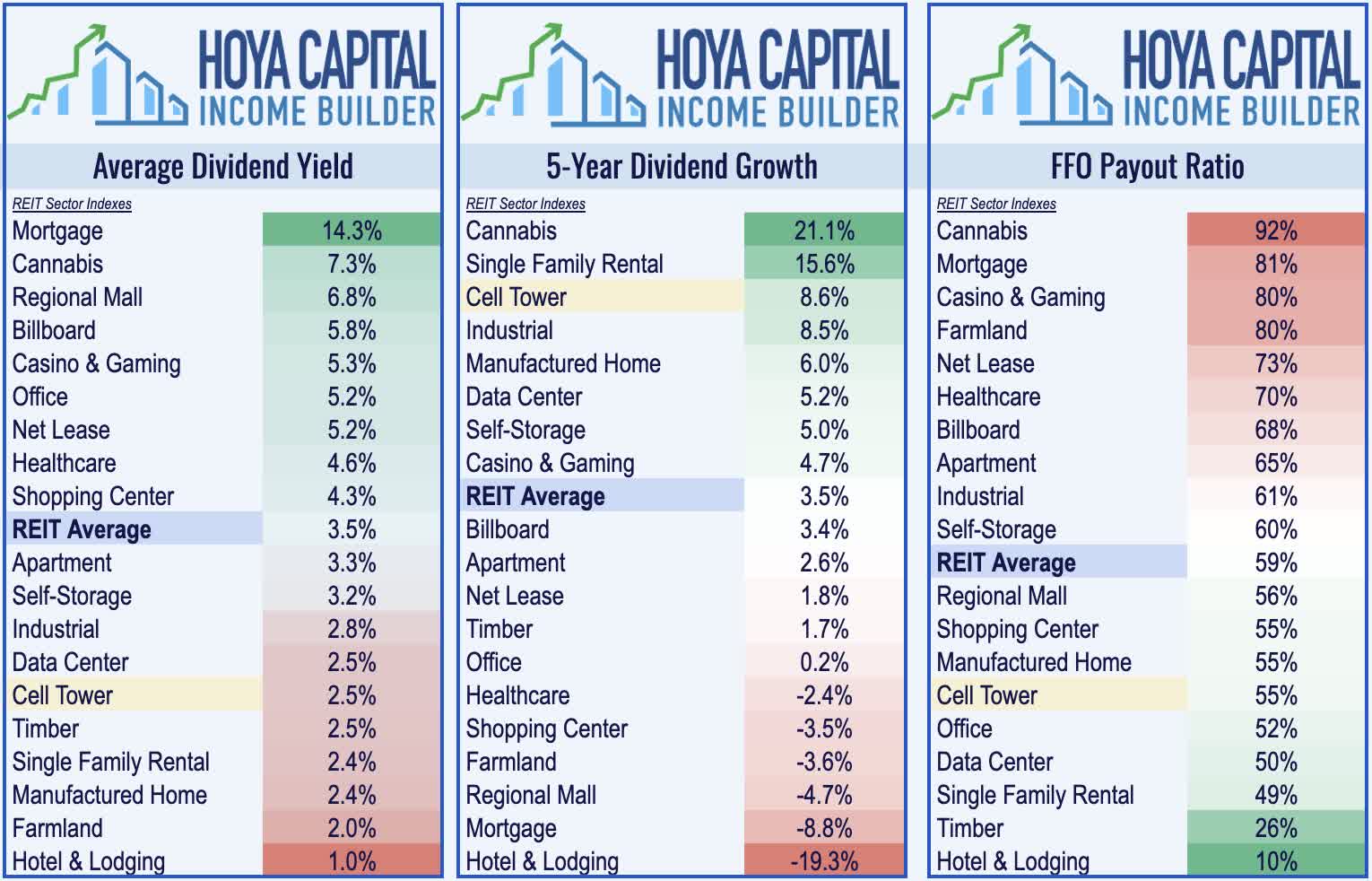

Cell Tower REITs pay an average dividend yield of 2.5%, below the market-cap-weighted REIT sector average of roughly 3.5%, but have been among the leaders in dividend growth throughout their history. Cell towers were one of the few property sectors that were untouched by the wave of dividend cuts and suspensions that hit the REIT sector in 2020 and have delivered robust annual dividend growth averaging over 8% over the past five years. Cell Tower REITs retain roughly half of their free cash flow leaving ample free cash flow for external growth and additional dividend growth.

Hoya Capital

Among the three larger cell tower REITs, we note that only Crown Castle acts like a “typical REIT” when it comes to distributions, paying a relatively healthy 3.5% dividend yield, which is roughly 80% of its available cash flow. American Tower, meanwhile, pays a relatively low 2.27% yield, while SBA Communications pays a yield of just 0.91%. Fiber-focused Uniti Group pays a yield of 5.92%, but has lagged its peers when it comes to dividend growth.

Hoya Capital

Takeaways: For 5G, 4 Carriers Beats 3

After uncharacteristically lagging for most of the year, Cell Tower REITs have been the best-performing property sector over the past quarter, benefiting from favorable macro shifts and positive industry-specific catalysts. DISH Network commercially launched its 5G network, becoming the fourth national wireless carrier alongside AT&T, Verizon, and T-Mobile. Given the industry skepticism over DISH’s viability, any level of success is incremental for tower REITs. We foresee DISH partnering with a major technology firm – possibly a Low Earth Orbit satellite provider – to create a competitive connectivity offering. While there is some risk of disintermediation to towers if the mobility of satellite connections improves, we see a higher likelihood that LEO networks will be “customers” rather than “competitors” to tower REITs, utilizing ground-based sites for network backhaul and supplemental network coverage.

Hoya Capital

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Mortgage, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital

Be the first to comment