SweetBunFactory

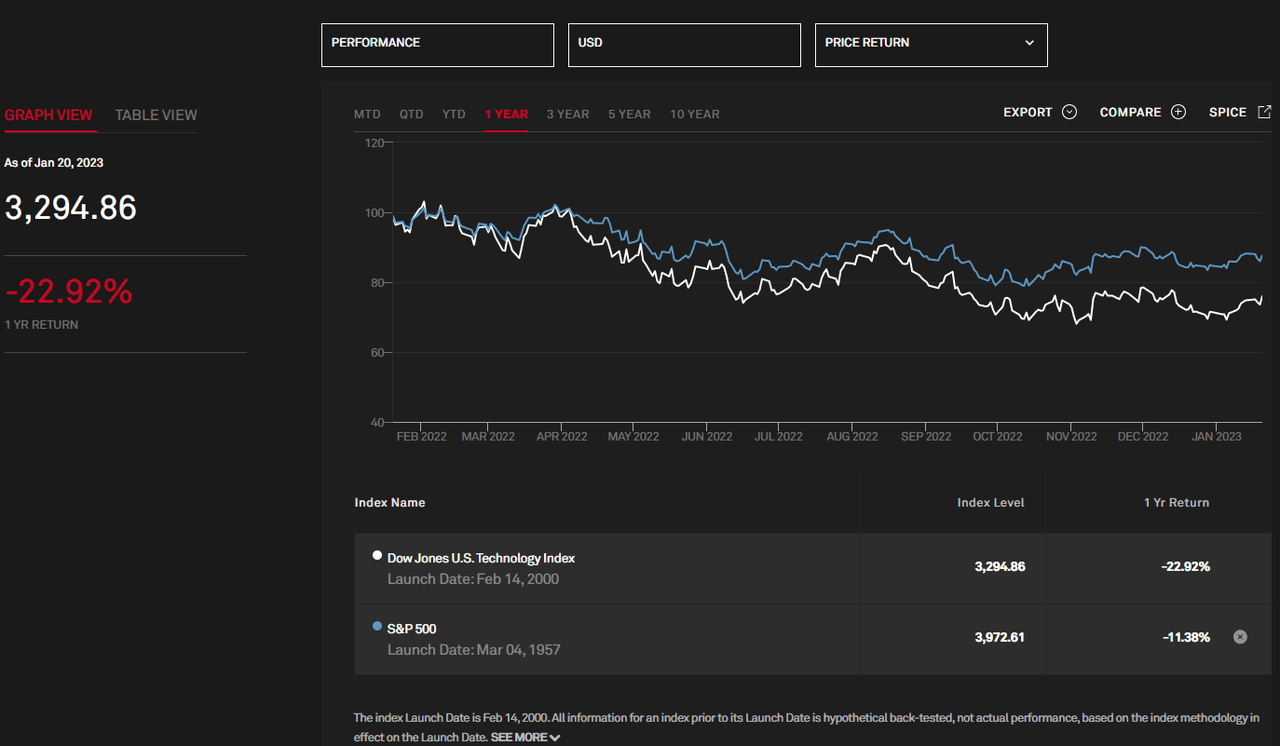

The tech sector has faced significant challenges in the last year, with layoffs approaching levels seen at the start of the 2020 pandemic. This is reflected in the underperformance of tech companies compared to the S&P500, with the market seeing a significant selloff in the last 2 months alone. However, there may be opportunities for investors to find value within the sector as the market adjusts to news of layoffs.

The Tech Index Vs S&P500 (spglobal.com)

Despite the industry’s struggles, by analyzing data and conducting a comparison pricing analysis, we aim to identify firms in the market that may be undervalued or overlooked in the current environment.

We will be comparing Celestica Inc. (NYSE:CLS) to the “Top Tech Stocks” screener on Seeking Alpha, which includes 663 of the top-rated tech firms on the market. We’ll also use the “All Us Stocks” screener as a basis for assessing the wider market.

Celestica Inc. has a long list of offerings in the advanced tech space, as summarised from their website below:

Celestica Inc.

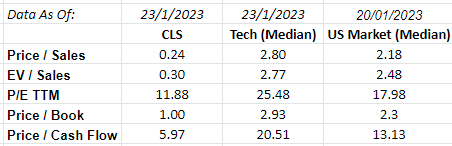

(Data & prices correct as of pre-market 23rd January 2023)

The Financials: Anything Noteworthy?

We will take a quick glance at the financials of CLS to ensure that there are no major concerns, and while we won’t be dwelling on this side of the analysis for long, it pays to have a picture in mind of the health of the firm.

Author

Largely speaking the firm is in good health, with moderate debt and average margins, though I note there are some concerns on the “acid test” with only 54% coverage of liabilities in a worst-case scenario.

Author

A cursory glance at the obligations structure and we see some small worries about coverage ratio (5 is considered low for the tech sector, as seen in the 22% percentile), while the current ratio of 1.43 shows the firm has some cushioning against any softening in revenue, but management won’t want to rely on it for long.

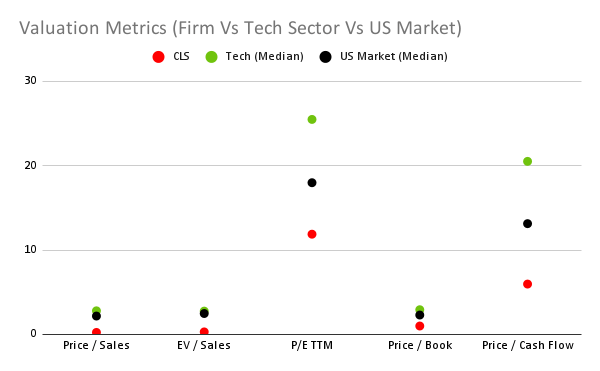

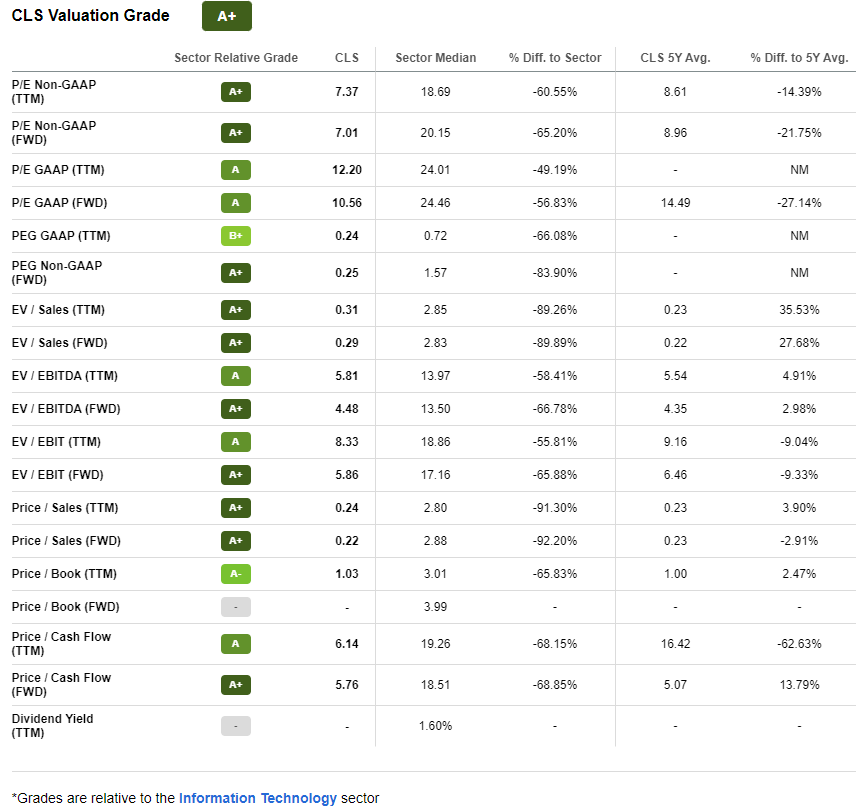

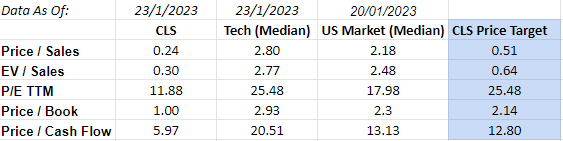

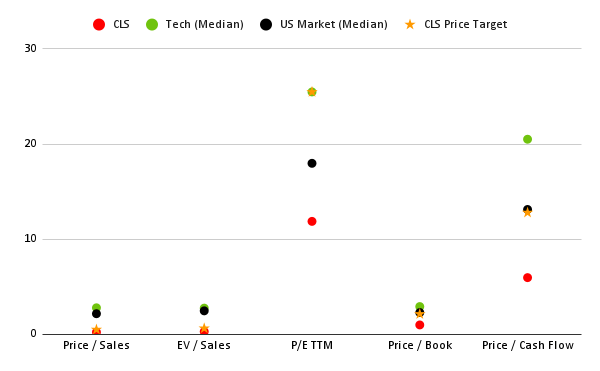

Celestica Inc. Vs The Market

We will examine how CLS‘ current pricing compares to the tech sector and the broader US market by analyzing key valuation metrics and visualising these ratios. This will provide insight into the relative value of the company and give us a starting point.

Author Author

Overall we see the firm sits well-below on all valuation fronts compared to both the US market and the tech sector, despite a reasonably healthy balance sheet. Profits and free cash flow per share are also generated far more efficiently for an investor’s dollar compared to the wider market.

Lastly, we’ll take a look at the top-line price attractiveness of the firm and get a sense of if it’s worth continuing our investigation.

Author

A weighted score of 89% indicates that there is plenty of overlooked value in CLS, so we’ll move on to exploring a pricing mechanism for the firm.

Finding An Appropriate Pricing Mechanism For Celestica Inc.

If you’re new to my analysis approach, I suggest checking out a previous article of mine where I detail my methodology in more depth. For those already familiar with my method, we’ll proceed with finding an appropriate pricing mechanism for the company.

Author

Ordinarily, I put a lot of trust into this pricing mechanism but given the wildly low valuation metrics compared to the IT market, we may need to dig a little deeper as a 300% upside price needs significant justification.

Firstly, we check Seeking Alpha’s valuation recommendation, which largely agrees with an argument for a Strong Buy.

Seeking Alpha

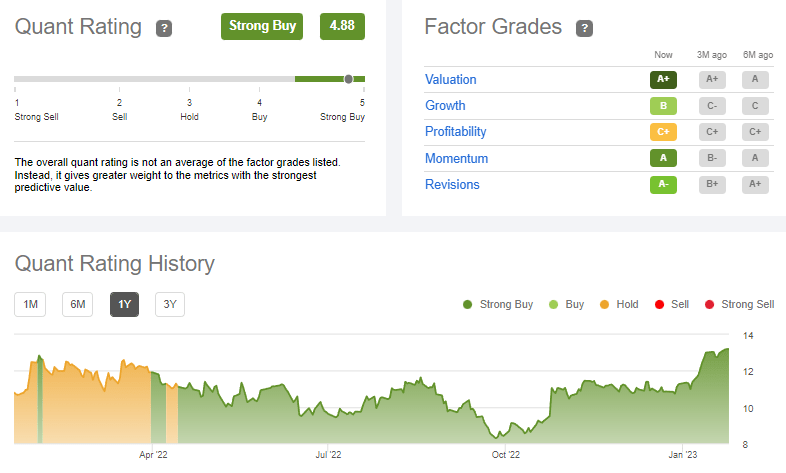

Next, we check The Quant, which also agrees strongly, noting they see weakness in CLS’ profitability, which I would also agree with (recall 45th percentile for EBITDA).

Seeking Alpha

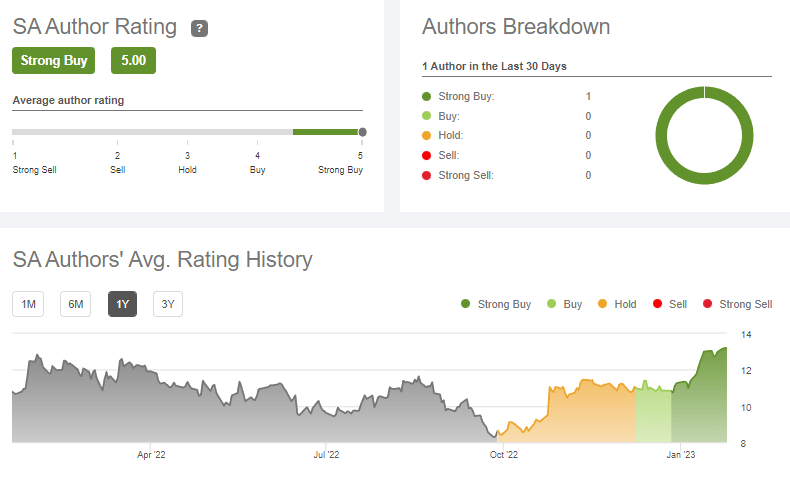

Seeking Alpha analysis is light on coverage, but we see a positive history here.

Seeking Alpha

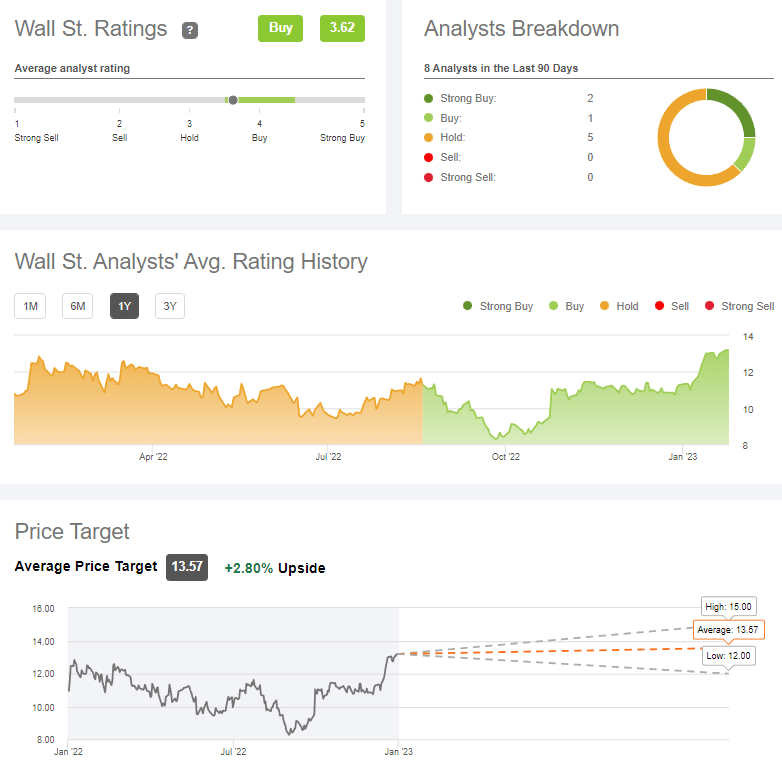

Lastly, we check the pulse of the street, who are rating CLS as a buy as a whole.

Seeking Alpha

Price targets amongst these groups are a long way from our pricing mechanism’s $52 target, and I date say we probably need to lean more heavily on the P/E pricing comparison rather than other metrics, which leads us to a conclusion that CLS has value up to the $27 mark (114% upside).

That said, I note some downside risks that could materially change the picture for CLS.

Visualising this price target and recalculated valuation metrics appears as so:

Author Author

Downside Risks

There exists some large risks for CLS, with the forecasted decline in global semiconductor revenue for 2023, as predicted by Gartner. This decline in revenue could negatively demand for the firm, while the oversupply in the semiconductor market could lead to increased competition and pressure on margins.

Further, an assessment of the balance sheet reveals 2,325m in inventor which has been rising rapidly over the last few years (up 2.8X since 2017), and makes up 43% of total assets, suggesting a slowdown in sales, confirmed by seeing fairly steady revenue (2% growth over 5 years).

Closing Remarks

Celestica Inc. stands out as a company with potential for growth, with a healthy balance sheet, efficient profit, cash flow generation, and a pricing attractiveness score indicating significant value in the stock.

A buy recommendation with a price target of at least $27 is appropriate for the stock, though monitor demand and inventory levels closely to revise the target.

Be the first to comment