blackdovfx

By Rob Isbitts

Strategy

There’s a reason I’m issuing a rare Strong Buy on the Core Alternative ETF (NYSEARCA:CCOR). It might be the best ETF on the market for investors who prioritize risk-management, as well as those who are concerned about bonds no longer being the long-term sidekick to equities in their portfolios.

CCOR invests about 90% of its assets in a portfolio of Large Cap equities. But importantly, it uses the remaining 10% to both hedge that equity exposure, hedge macro-market risk, and attempt to enhance portfolio returns.

Proprietary ETF Grades

-

Offense/Defense: Offense

-

Segment: Tactical

-

Sub-Segment: Option-Enhanced

-

Correlation (vs. S&P 500): Very Low

-

Expected Volatility (vs. S&P 500): Very Low

Holding Analysis

CCOR’ equity portfolio comprises just over 40 stocks. These are Blue-chip names, dividend payers, and spread across 10 of the 11 S&P 500 sectors (only REITs are absent). It has a strong technology exposure (15%) but that is not so high as to get it into the type of trouble that Nasdaq-oriented ETFs are dealing with in the current market climate.

The key to CCOR’s stability is its options holdings. Currently there are 5 calls and 5 puts, all with the S&P 500 as the underlying security. Importantly, both the calls and puts are “long” option positions. The calls are not covered calls.

This means that the options act more like long and short positions around the core stock portfolio. In a moderate-to-highly volatile market, the calls may go up enough to offset the loss on the puts, or vice-versa. The puts are “tail risk” protection for the total CCOR portfolio, while the calls act as a way to “put the pedal to the metal” and try to drive higher gains than the hedged stock portfolio can do on its own.

Strengths

Pound for pound, For someone like me, who is a self-proclaimed “tough grader” on ETFs and stocks, especially in the financial era we live in, I can’t deliver higher praise for an ETF. At least, none I’ve seen so far. But rest assured, looking for outstanding ETFs to write about and consider investing in myself is a full-time job for me.

I say this after managing money professionally for about 30 years, and researching, stress-testing, buying and selling hundreds of ETFs over that time. I’ve been researching ETFs since, well, since there were ETFs. So, what’s so special about CCOR?

The biggest reason I like CCOR is because it is the closest thing to how I have managed money professional for about the past 20 years. During that time, the goal has always been simple, though challenging. Namely, to achieve:

1. Avoidance of big losses (ABL). “Big” varies by investor, but for me and for the investors I managed money for before selling my practice in 2020, that typically meant that in a given 12-month period, the goal was to keep the maximum loss to as close to 5% as possible, or 10% in an “Armageddon” type of market.

2. Make as much as you possibly can.

3. ABL comes first!

The goal has been to replace what bonds used to do but no longer do for investors, with the same confidence behind it. The nature of bond investing has changed for a while, at least. And the stock market is not helping. That should prompt many investors to look for other ways to allocate. That’s why I focus my ETF coverage on a mix of long, inverse and cash-like ETFs. Then, there are some, like CCOR, that provide a lot of that in one neat ETF package.

Weaknesses

The basic tenet of investing is, take more risk to get more return. That is not true in mixed market cycles. However, you can see that CCOR’s tight risk-management process will put it well behind the S&P 500 Index in sustained up markets.

Opportunities

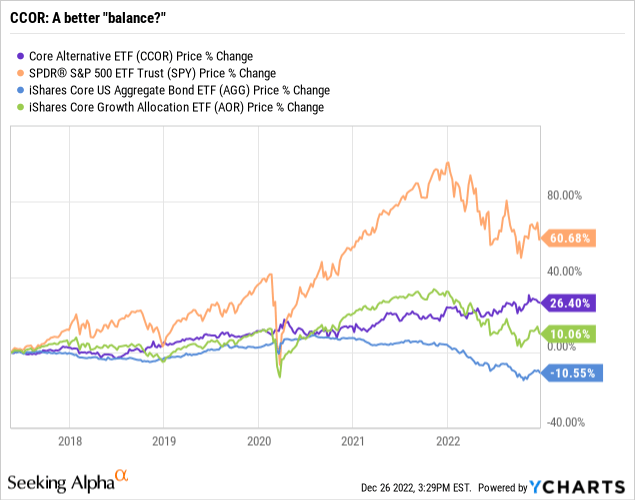

However, that is not what we have currently, and no one knows when we will again. As that chart above shows, the past 5 years have seen CCOR produce a steady path of returns, while a 60/40 “balanced” ETF rocketed higher, then fell back to earth, with CCOR ultimately outperforming by a wide margin. And, as compared to the standard bond market benchmark, it is simply no contest. So until rates are crashing lower at the same time stocks are rising, CCOR would seem to offer a superior risk-adjusted method of doing what “balanced” strategies did for so long. That is at the “Core” (pun intended) of my very favorable opinion here.

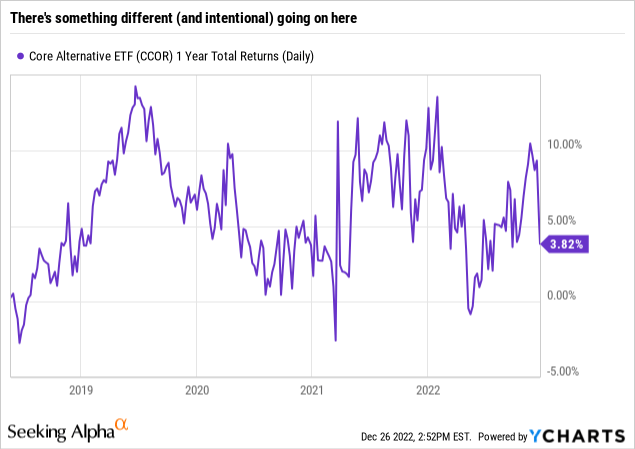

The stress-test I apply to any ETF’s past performance is something I think most serious investors would appreciate: I look at every 1-year return period, to see its best and worst, and everything in between. Here’s what that looks like for CCOR.

That is a return range over any 1-year period of between +14% and -3%. When I ran these years ago, before 2018, they were less meaningful than they are today. That’s because the equity and fixed income markets had not been stress-tested. Since that time, we’ve had at least 3 key stress tests.

There was the quick dip in late 2018 (which I likened to the current climate in this article) 2018 vs 2022 Article By MII

Then we had the 2020 debacle: 5 weeks, 33% drop in the S&P 500, albeit with a lightning-fast recovery.

Most recently we had the entirely of 2022. This time, we could stress-test any ETF in a headwind for both stocks and bonds.

In each period, CCOR has not only survived, but thrived.

CCOR is one if the least-followed ETFs in the entire Seeking Alpha coverage universe. It should not be. Thus, my reporting on it here for the first time since its 2017 debut, and feeling I understand its approach as well as any outsider could, makes this a unique ETF profile among a sea of mediocre or downright dangerous funds.

Threats

As is often the case, when I write about the “threat” of an ETF, I am often referring to the threat that investors will misuse it, and not see it for what it is. In the case of CCOR, the “risk” is predominantly that it is not likely to deliver a gigantic return in an uber-bullish stock market environment. The put option positions cap the upside. This is not to a specific upper level, but the fact is, put option exposure is a drag on returns in up markets, just as call options and stocks are a drag on what the puts do in down markets.

Investing is a constant tradeoff if your objective is to pursue a steadier ride in an era where the nature of markets makes that darn near impossible. Just be clear that in the next roaring bull market, if investors want to grab a big piece of that bull, they’ll need some un-hedged equity exposure to get there.

The other threat is a period of extremely low volatility. This can cause the put and call options to erode in value.

Proprietary Technical Ratings

-

Short-Term Rating (next 3 months): Hold

-

Long-Term Rating (next 12 months): Hold

Conclusions

ETF Quality Opinion

Not knowing the managers of CCOR personally, I feel like I do, because their approach is literally the only thing out there that reminds me of, well, me. They manage an ETF and I don’t (I did manage this type of strategy in a mutual fund on 2 occasions in my younger days). So, finding that this approach is available to any investor is a true “find” for me, and hopefully for others.

ETF Investment Opinion

Keep in mind that this opinion is fully based on the role of this ETF as a portfolio stabilizer, a “Core” position around which other investment biases can be owned. Note that my own proprietary technical ratings are “hold” for both 3-month and 12-month time frames. That makes sense because CCOR is about as poor a “trading” candidate as you will find among ETFs. It is full of self-balancing/hedging mechanisms that make it a potential portfolio anchor, rather than a trading/tactical piece that an industry or sector ETF might be.

I note this because I fear retail investors have poured so much money into the “set it and forget it,” ETFs (that’s what the statistics show, with a small number of the 3,000+ ETFs attractive the vast majority of investor assets).

Thus, they have invested relatively little into the type of ETFs that could better-navigate the next decade for them, so I think we need to lift the veil on more of the former type of ETF. That’s the mission for Modern Income Investor in 2023 and beyond. I aim to be a tough grader, so take this rave review of CCOR, and my Strong Buy rating, in that context. It isn’t sexy, unless you consider a much smaller range of possible outcomes to have sex appeal. I do.

Be the first to comment