John Blottman

Investment Thesis – The Risk Is Growing

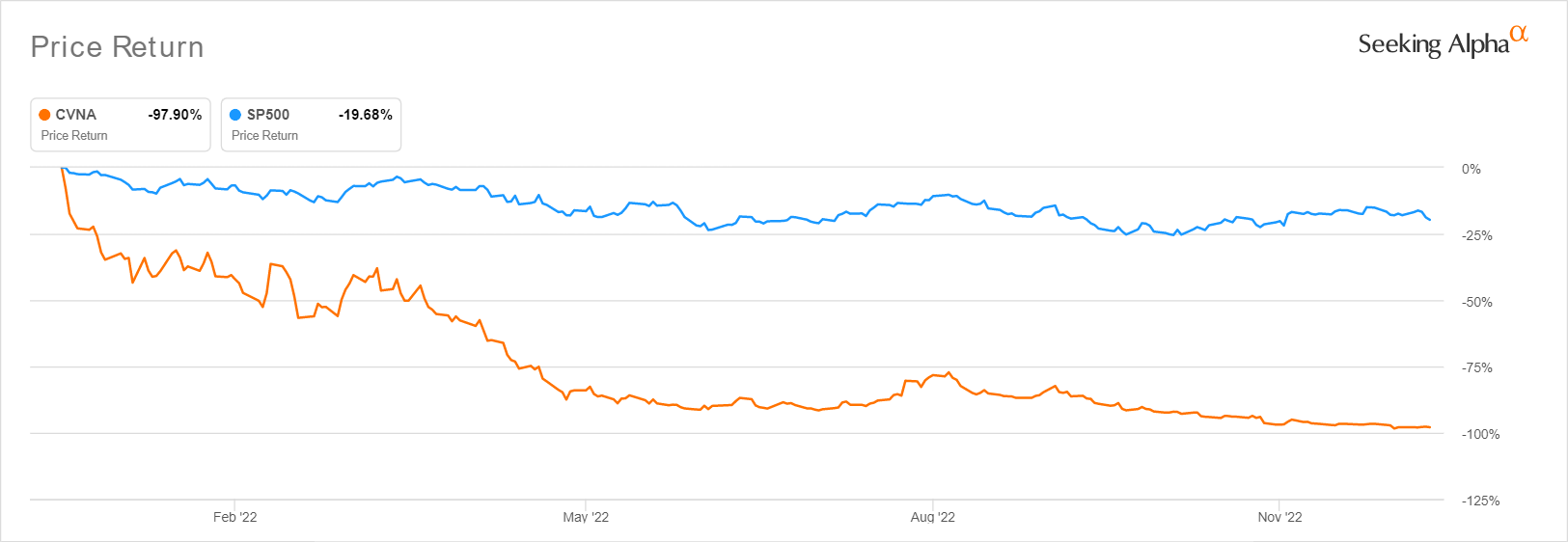

CVNA YTD Stock Price

Seeking Alpha

Carvana Co (NYSE:CVNA) has had the rollercoaster ride of a lifetime indeed, given the peak stock price of $361.25 in August 2021, before crashing catastrophically by -98.60% to reach $5.03. The fact that the stock has climbed by 41.69% since 07 December’s $3.55 is more than impressive indeed. However, here is where the good news ends.

Consumer demand for used autos has been falling, with the November CPI report highlighting a slowing index for used cars and trucks by -2.8% sequentially and -3.3% YoY. These continued the downtrend since the cooling of auto markets by mid-2022. The Manheim Used Vehicle Value Index reports a pricing decline of -16% since January 2022 as well, with analysts expecting prices to further normalize by up to -33%, due to the grossly inflated prices in 2021.

This is naturally a bane for CVNA, since the company still reports elevated inventory levels of $2.5B, on top of its long-term debts of $6.25B. Much of the former is accumulated when used auto prices are at record highs. As a result, it is no surprise that there have been expanded depreciation rates of -$488M by FQ3’22, compared to FQ3’21 levels of -$259M and FQ3’20 levels of -$146.24M. Any attempts to rapidly sell off its existing inventories may result in further margin compression, increasing its losses simultaneously.

Even peers, such as CarMax (KMX), have been severely impacted in FQ2’22 with reduced retail used units sold and compressed gross margins, due to consumer affordability issues from elevated interest rates. These point to more uncertainties ahead indeed.

Mr. Market Expects CVNA To Underperform Ahead

For its upcoming FQ4’22 earnings call, CVNA is expected to report revenues of $3.17B and EPS of -$2.36, indicating little improvements QoQ and YoY. These are worsened by the rising inflationary pressure, further compressing its gross margins by -4.5 percentage points YoY in FQ3’22. Its operating expenses have also been growing aggressively in the latest quarter, by 19.74% YoY and 318.16% from FQ3’19 levels. These impacted its EBIT margins by -8.2 percentage points simultaneously. The company has also been generating negative Free Cash Flow [FCF], due to its high capital expenditure of $618M over the last twelve months, growing by 28.75% sequentially and 268.06% from FY2019 levels.

In addition, CVNA may likely underperform in the intermediate term, due to the recent ADESA acquisition for $2.2B. ADESA may have brought in $1.96B of revenues in FY2021. However, despite the massive sales, the latter reported net losses of -$58.9M then. By the first three quarters of 2022, the car auction business has been severely impacted by the worsening macroeconomics, with declining revenues of $301M and net losses of -$57M. In addition to the higher average selling price of 17.77% compared to FY2021 levels, the net losses narrowed temporarily, due to the moderated SG&A expenses by -7% and a $13M contribution from the ADESA acquisition. Combined with the reversing consumer trend, there is a reason why market analysts are increasingly concerned about the company’s potential bankruptcy.

Therefore, it is no surprise that CVNA has notably increased its reliance on SBC expenses thus far. By the last twelve months, the company reported $68M of SBC expenses, increasing by 74.35% compared to FY2021 levels of $39M and by 209.09% from FY2019 levels of $33M. Combined with its capital raises in early 2022, long-term investors would also have witnessed an eye-watering share dilution of 226.24% since FQ3’19. While its SBC expenses may slow due to the strategic job cuts ahead, it remains to be seen when we can see a successful turnabout.

Despite CVNA’s well-laddered debts through 2030, the company is also looking at elevated quarterly interest expenses of $153M in FQ3’22. The growth is primarily attributed to the additional senior notes issued in March 2021, August 2021, and May 2022, on top of the leaseback financing since September 2021. Seeing how the company has been reporting -$1.12B of operating losses over the last twelve months, it is unclear how these expenses may be sustainable in the long term. There is still an outstanding liability of $483M for its property and equipment through various sale/leaseback transactions in the latest quarter, although with initial monthly payment terms split between the next 20 to 25 years. Depending on how the base rent increases throughout the whole term, we expect to see a continued impact on CVNA’s EBT and net income profitability ahead.

Beyond the annus horribilis in 2021 and 2022, there are few catalysts for CVNA’s short and long-term recovery. Even if the company meets analyst expectations of sales growth of 15.8%, the company may remain unprofitable over the next few years, significantly attributed to the highly volatile market funding environment. Bonds are trading at a 20% yield adding material risk to its outlook since CVNA relied on loan sales. YTD, the company reported earnings of $361M from auto loan sales, representing a decline of -31.75% from FY2021 levels. These may indicate its difficulty in competing with larger banks in these elevated interest conditions, before the Feds pivot by speculatively 2024. Even then, it is likely that interest rates will remain elevated for a while longer, due to the slower normalization effect.

While CVNA may report positive margins by speculatively FY2026, it is diminutive at best, with projected EBIT margins of 3.4% and FCF margins of 2.8%. These may potentially fuel its growing reliance on debt leveraging, Stock-Based Compensation expenses, and share dilution in the intermediate term. In the meantime, we encourage you to read our previous article, which would help you better understand its position and market opportunities.

- Carvana: Value Trap – Still Not A Buy During This Auto Bubble

So, Is CVNA Stock A Buy, Sell, Or Hold?

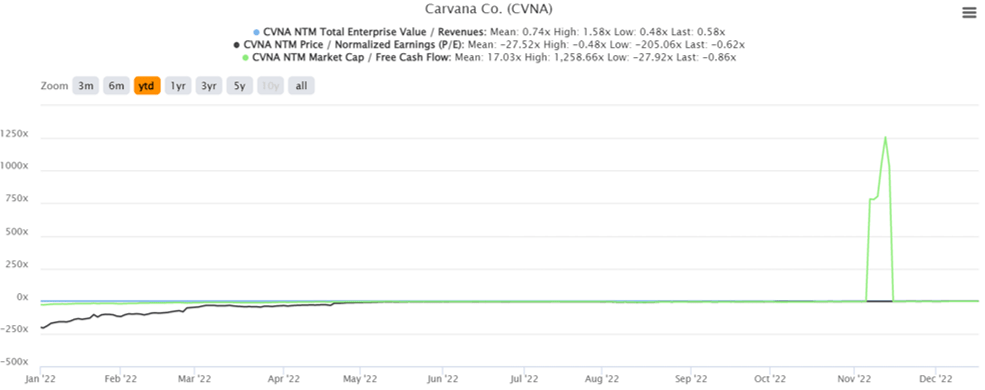

CVNA YTD Valuations

S&P Capital IQ

CVNA is currently trading at an EV/NTM Revenue of 0.58x, NTM P/E of -0.62x, and NTM Market Cap/FCF of -0.86x, lower than its 5Y mean of 1.31x, -84.82x, and -9.59x, respectively. Otherwise, it is tragically moderated from its YTD mean of 0.74x, -27.52x, and 17.03x, respectively. Due to its lack of meaningful projected profitability over the next few years, it is naturally hard to place a supposed price target on the stock. Based on market analysts’ $20.50, CVNA is currently trading with an ambitious 363.80% upside.

However, those numbers are too optimistic, especially given the Fed’s continued hikes through 2023, uncertain financing markets through 2024, and the normalization of used auto markets. Combined with the pessimistic financial projections through FY2026, we do not recommend anyone add the underperforming CVNA stock to their portfolios. Naturally, we believe that those still holding on to this stock should take the $5 and run, as similarly mentioned by a fellow contributor. Do not wait any longer.

Be the first to comment