Sakorn Sukkasemsakorn

Note:

I have covered Capstone Green Energy (NASDAQ:CGRN) previously, so investors should view this as an update to my earlier articles on the company.

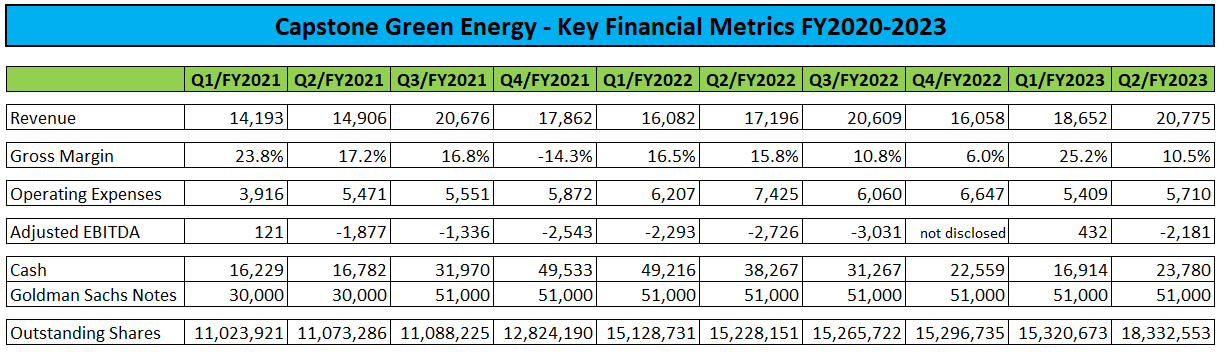

Two months ago, ailing microturbine manufacturer Capstone Green Energy (formerly Capstone Turbine) or “Capstone” reported another set of less-than-stellar quarterly results as supply chain issues impacted the company’s margin performance quite meaningfully:

Company Press Releases and SEC-Filings

As a result, gross margin was down by almost 1,500 basis points sequentially to just 10.5% thus causing Adjusted EBITDA to turn negative again.

On the flip side, Capstone managed to generate $0.2 million in free cash flow for the quarter which is in stark contrast to the massive cash outflows suffered in recent years.

The company also received $7.3 million in net proceeds from an underwritten public offering consisting of 2,934,498 shares of common stock and accompanying warrants to purchase up to 2,934,498 shares of common stock at a combined public offering price of $2.75 per share and accompanying warrant. The warrants have an exercise price of $2.75 per warrant, are exercisable immediately, and will expire five years following the date of issuance.

The offering was required to satisfy recently amended debt covenants governing an aggregate $51.0 million in senior secured notes (“the notes”) issued to a division of Goldman Sachs (GS) between 2019 and 2020.

That said, the company missed out on the October 1, 2022 refinancing deadline for the notes but in absence of any regulatory filings regarding the issue, it is fair to assume that Goldman Sachs has refrained from declaring an event of default for now.

In early September, Capstone engaged Greenhill & Co. or “Greenhill” (GHL) as financial advisor and investment banker in conjunction with the required “commercially reasonable best effort” of refinancing the notes.

On the Q3 conference call, management was optimistic regarding Greenhill’s ability to not only refinance the notes but also raise additional debt in the near future:

Couldn’t be happier with the job Greenhill & Company is doing for us. We looked at 12 different investment banks. Scott and I did the interview to see who can refinance Goldman for us. And they definitely came out on top and have not disappointed. And so look forward to them launching shortly and seeing what kind of pricing we can get for some additional debt and refinance the Goldman note that’s up in a little under a year.

But in the current environment and given the financial condition of the company, raising new debt won’t be an easy task and even if Greenhill manages to line up new creditors, interest rates are likely to eclipse 15%.

As a result, Capstone was required to include a going concern warning in the company’s most recent 10-Q (emphasis added by author):

(…) While the Company believes internally generated cash will adequately fund operating and investment activities over the next twelve months, there will not be sufficient internally generated cash, nor does the Company expect that it could obtain sufficient financing through underwritten public offerings, at-the-market offerings or other similar methods, to retire the outstanding debt. The Company has engaged Greenhill, a global investment banking firm, to assess financing alternatives related to the Note Payable as well as to raise incremental capital for general corporate purposes. As there is no guarantee that the Company will successfully complete these financing activities, these conditions raise substantial doubt about the Company’s ability to continue as a going concern for a period of one year from the date of the financial statements are issued.

That said, not all was bad in Capstone’s Q2/2023 report as the company managed to decrease days sales outstanding by more than 30% sequentially and almost 45% since the end of FY2022:

Our accounts receivable balance, net of allowances, was $19.3 million and $24.7 million as of September 30, 2022 and March 31, 2022, respectively. Days sales outstanding in accounts receivable (“DSO”) decreased by 65 days to 85 days as of September 30, 2022 compared to 150 days as of March 31, 2022, primarily due to an increase in accounts receivable collections as our Distributors saw improved cash flows as the COVID-19 pandemic subsides.

In addition, improved order intake resulted in product backlog to increase by 16.5% quarter-over-quarter to $28.9 million at the end of Q2/FY2023.

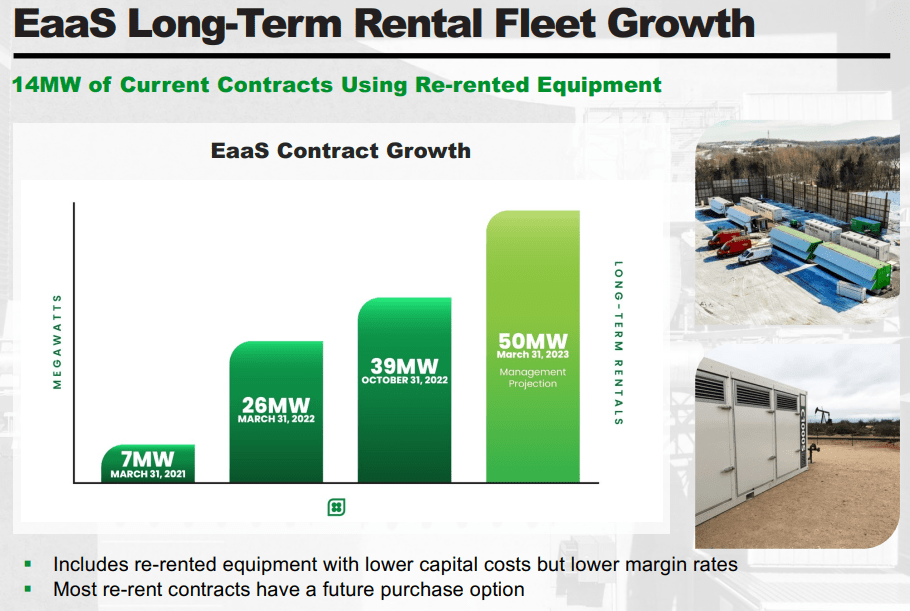

The company continues to focus on expanding its high-margin microturbine rental business which the company refers to as “Energy-as-a-Service” or “EaaS”:

Company Presentation

That said, building out the rental fleet has already required substantial cash investments and despite strong segment revenue growth, EaaS still accounts for less than 10% of Capstone’s quarterly revenue.

In an effort to lower capex requirements, the company has developed a “re-rent” strategy to add idle microturbines from existing customers to the rental fleet. At the end of October, approximately 35% of the fleet consisted of “re-rented” equipment with the resulting capex relief coming at the expense of lower margins.

On the conference call, management stated a 60% gross margin target for the EaaS segment which is actually down from the 72% recorded in Q2 as more re-rentals are expected to enter the fleet going forward.

More importantly, the company expects to become EBITDA positive and generate positive cash flow from operations once the 50MW target will be achieved.

But given management’s long history of over-promising and under-delivering, investors should take these projections with the usual grain of salt.

Bottom Line

Investors are still waiting for Capstone Green Energy to get a handle on its debt issues and future capital requirements for scaling its high-margin Energy-as-a-Service offering.

While Goldman Sachs has not yet declared an event of default under the company’s senior secured notes, refinancing the debt at reasonable terms might prove be a herculean task in the current interest environment.

On the flip side, with market participants chasing speculative stocks again and management projecting positive Adjusted EBITDA and cash flow from operations in FY2024, a successful refinancing would likely cause a major rally in Capstone’s beaten-down common shares.

While I would advise investors to remain on the sidelines until the fate of the company becomes more clear, I am upgrading shares to “Hold” from “Strong Sell“.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment