Sunan Wongsa-nga

REIT Rankings: Cannabis

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on December 28th.

Hoya Capital

Cannabis REITs have been slammed this year amid concern over defaults from their cannabis cultivator tenants, which have been smoked by plunging wholesale cannabis prices, setbacks on federal legalization, and a broader re-pricing of risk across financial markets. Within the Hoya Capital Cannabis REIT Index, we track the three cannabis equity REITs – Innovative Industrial (IIPR), NewLake Capital (OTCQX:NLCP), and Power REIT (PW) – along with the two mortgage REITs – AFC Gamma (AFCG) and Chicago Atlantic (REFI). Combined, cannabis REITs account for roughly $4B in market value.

Hoya Capital

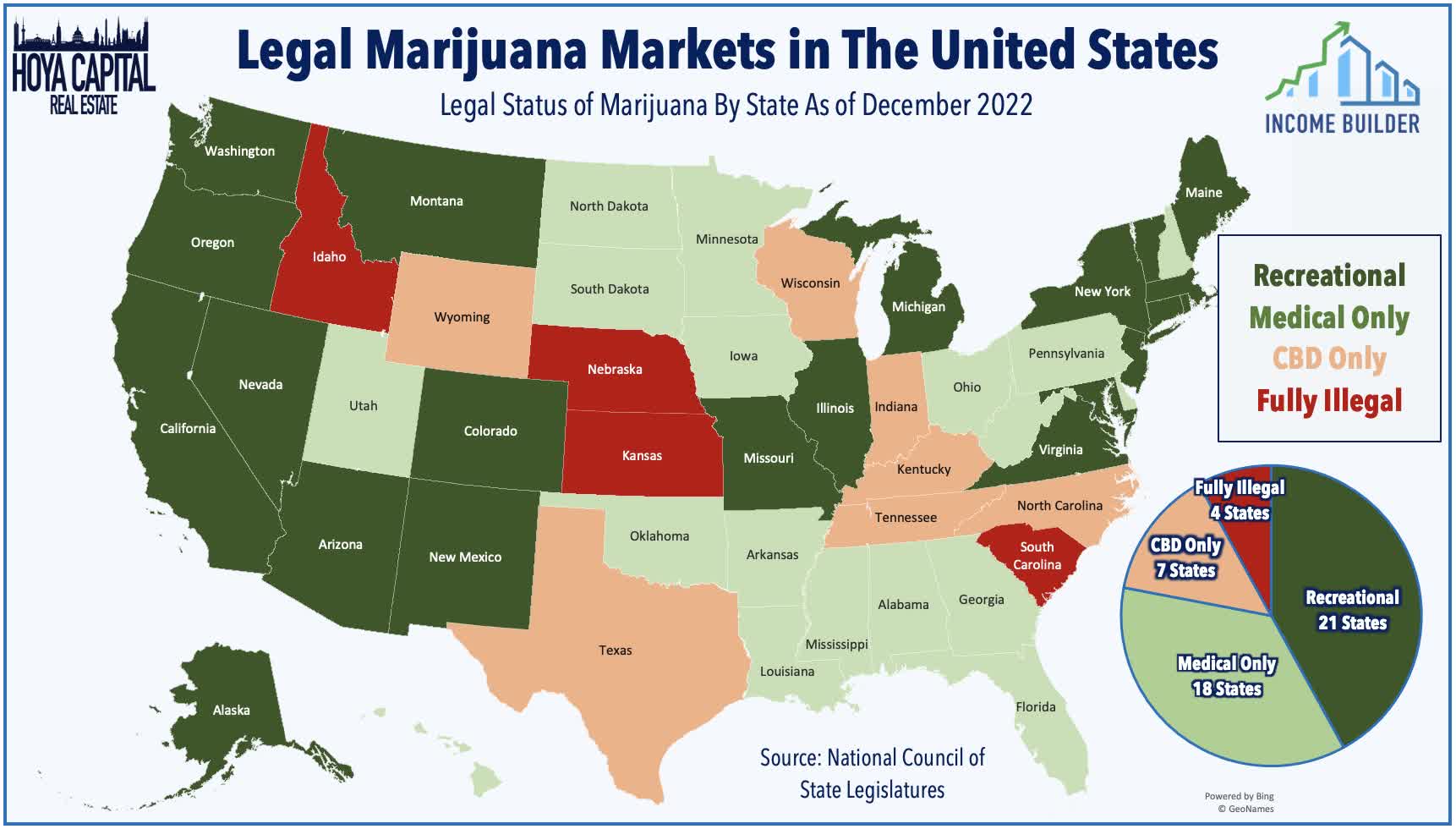

Existing in a legal “grey area” in which federal, state, and local laws often contradict, cannabis has been federally restricted since the 1930s, but medical usage is now legal in 38 states while recreational usage is legal in 21 states following a wave of successful ballot measures over the past half-decade. Just four U.S. states currently maintain a full prohibition of any cannabis-based product, but even within these states, cannabis possession and production has been incrementally decriminalized over the past decade. More than two-thirds of the U.S. population now support marijuana legalization, up from roughly 15% in the 1970s and 35% in the early 2000s while roughly 1-in-8 Americans consume cannabis regularly. Marking a major milestone in 2018, the FDA approved the first cannabis-derived medication – Epidiolex (cannabidiol) – for the treatment of seizures associated with two rare forms of epilepsy.

Hoya Capital

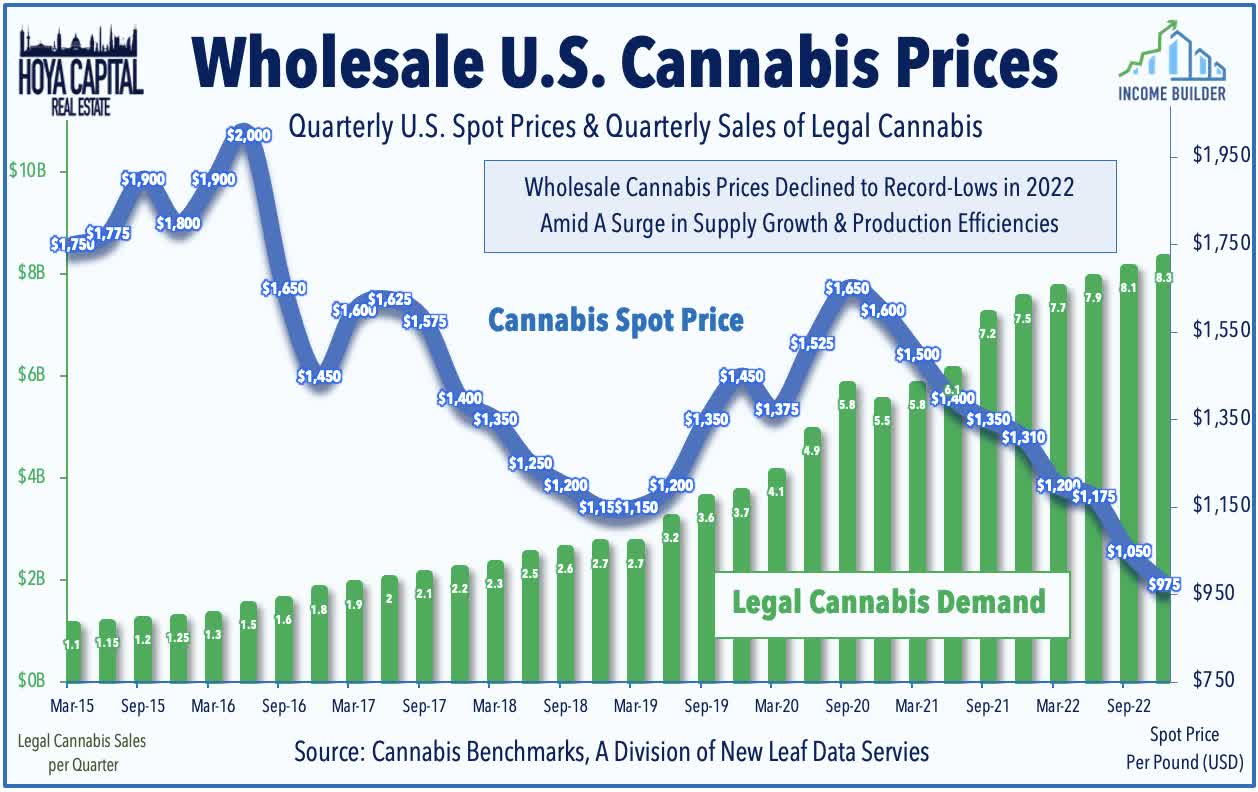

Getting high is getting cheaper – and that’s becoming a problem. Aggravating the already-challenging macroeconomic environment, cannabis cultivators and retailers have been pressured by a weak pricing environment amid a wave of new entrants to the cannabis retail and cultivation industry and as institutional capital to multi-state operators has driven production efficiencies. Reflecting trends seen nationwide, data from the Colorado Department of Revenue showed that wholesale marijuana prices dipped to record lows at just $658 per pound – down more than 50% from a year ago. The cost of production is estimated to be $800-$900 per pound in Colorado. The U.S. Cannabis Spot Index – the aggregate national price for the 18 legal cannabis markets covered by Cannabis Benchmarks – has also set a series of record lows this year with the national average declining to $956 per pound last week – roughly 35% below the average price over the prior five years and more than 50% below the average price in 2015 amid the initial wave of state legalization.

Hoya Capital

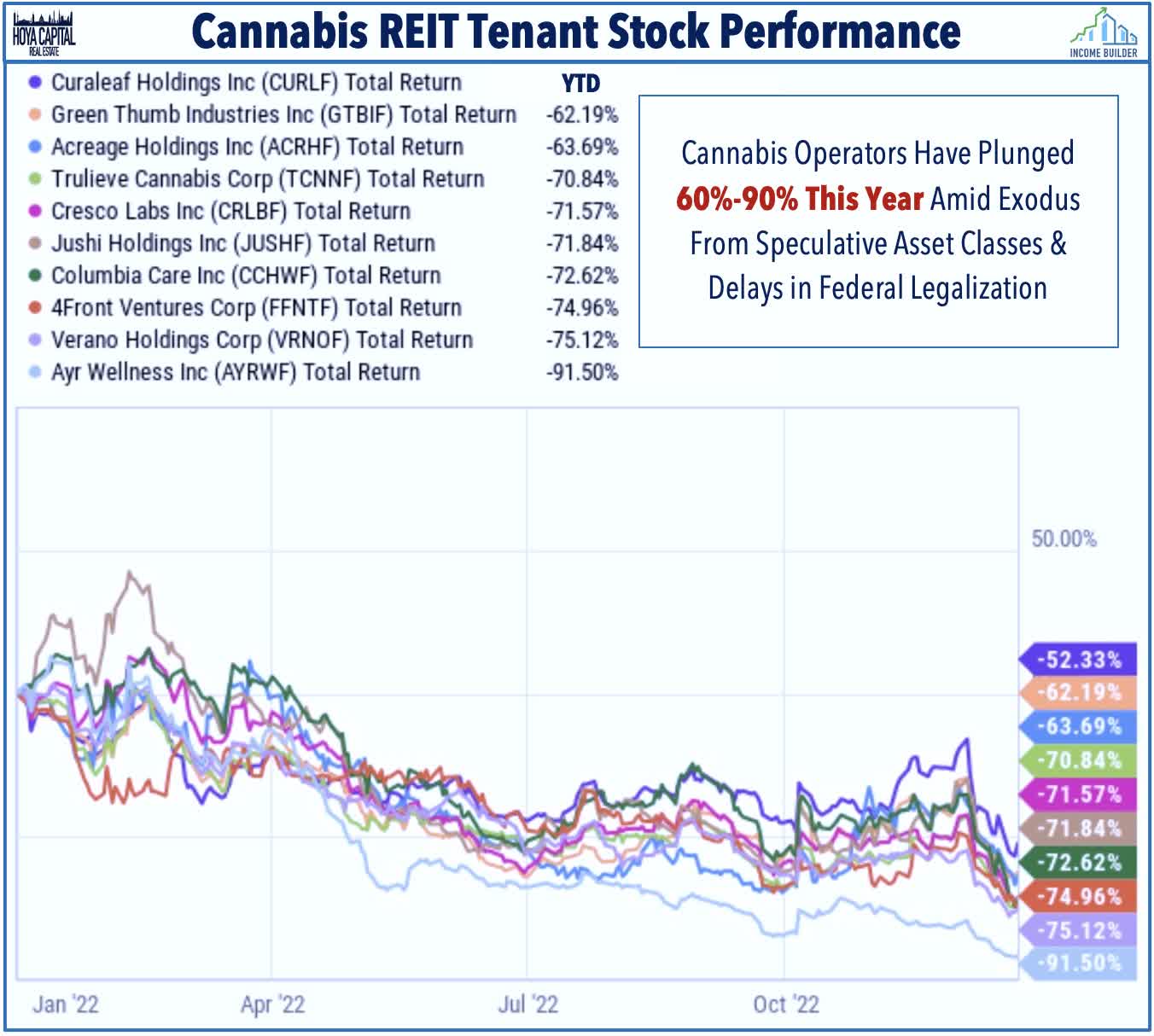

Cannabis REITs – which entered 2022 with the strongest five-year total returns, dividend growth, and FFO growth of any property sector – have been unable to escape the seemingly relentless downward pressure on the broader cannabis industry this year. Owning the “Pharmland” – the physical real estate behind the cannabis cultivation industry – had been one of the few cannabis-related investments that was working during a half-decade-long stretch of poor performance from the broader cannabis industry, but concerns over tenant financial health have bled over onto the REITs themselves after a handful of tenant defaults among smaller single-state operators. Rent collection and loan performance concerns have mounted as the ten public-traded REIT tenants have plunged between 60-90% over the past year and the struggles among smaller non-public operators are likely even more acute.

Hoya Capital

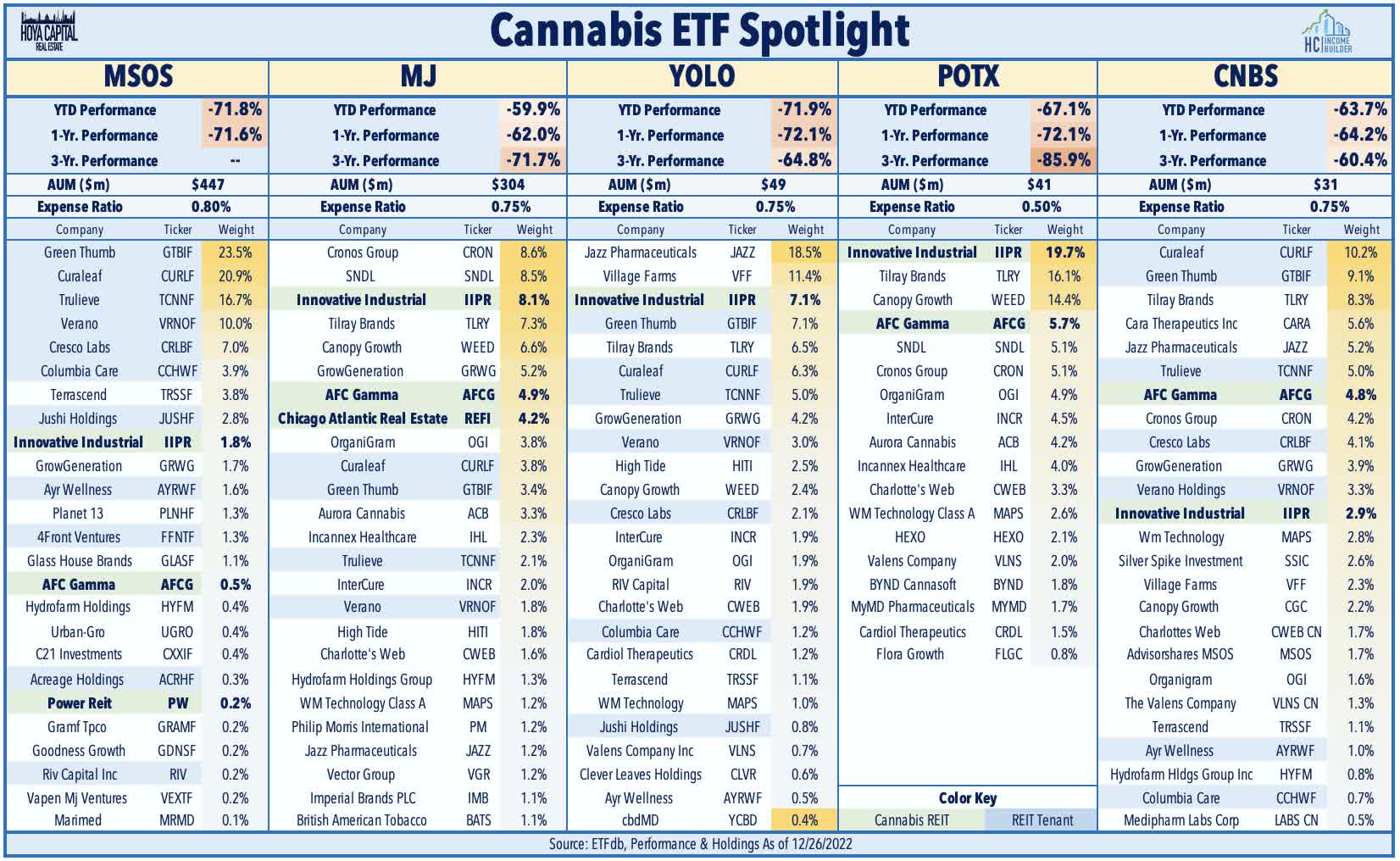

Underscoring the persistent struggles of the broader cannabis industry, since its launch in late 2015, the ETFMG Alternative Harvest ETF (MJ) – the oldest cannabis ETF – has produced average annual total returns -19.14%, woefully underperforming the S&P 500’s 10.95% annual returns during this time, and being “left in the dust” by the two cannabis REITs. Other broad cannabis ETFs have seen similarly weak performance since their respective inceptions including (MSOS), (YOLO), (POTX), and (CNBS) which are all lower by at least 60% this year. Cannabis REITs represent less than 10% of these ETFs, on average, as these ETFs primarily hold cannabis operators and retailers including most of these publicly-traded cannabis REIT tenants.

Hoya Capital

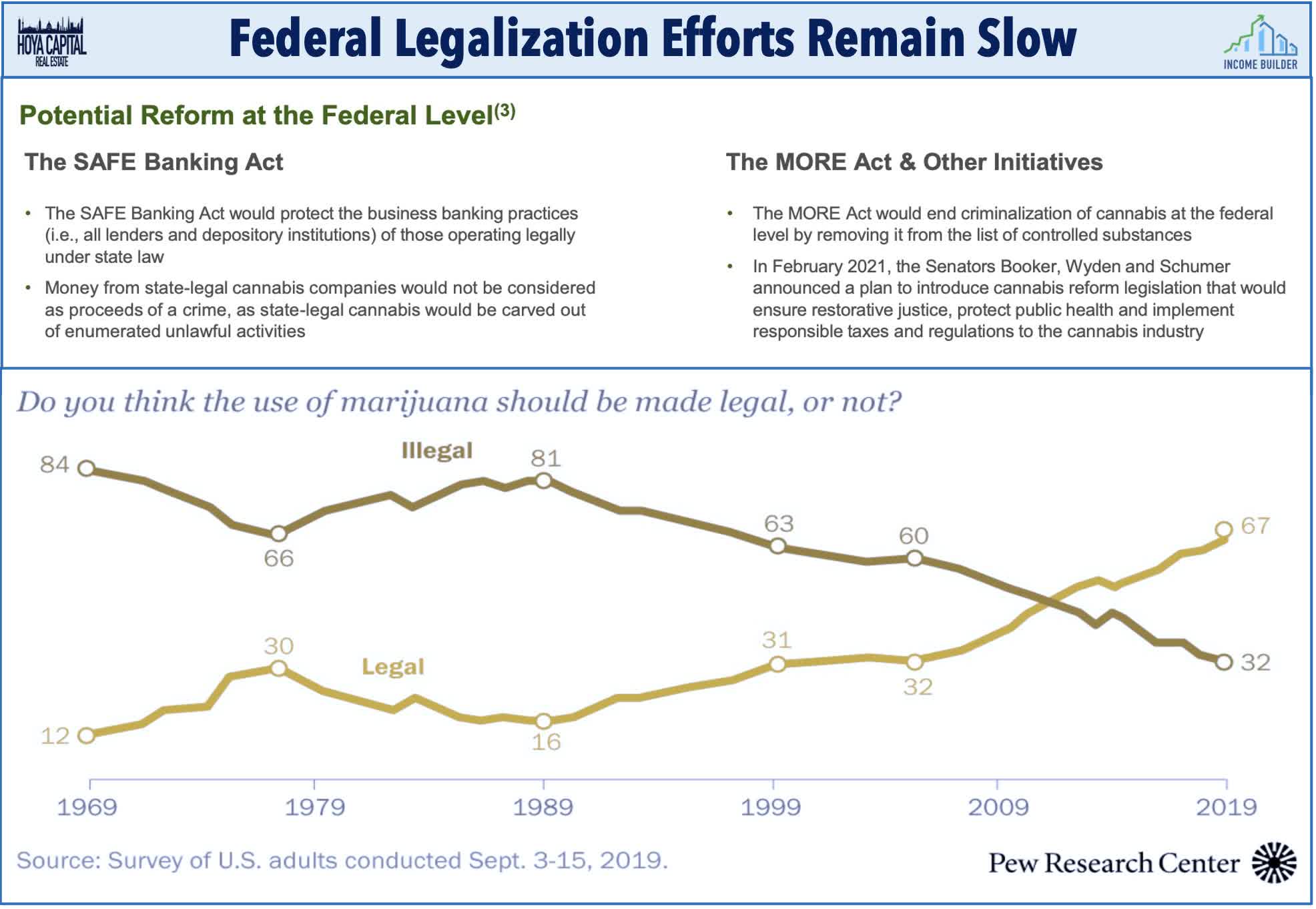

Adding insult to injury, stalled progress on federal legalization – which is typically the first investment case “bullet point” of cannabis businesses – has made a challenging operating environment enough tougher. The exclusion of the SAFE Banking Act from the omnibus federal spending package in late 2022 dimmed hopes that any major federal marijuana legislation will be passed during the Biden Presidency. The Secure and Fair Enforcement (“SAFE”) Banking Act was designed to protect financial institutions from penalties for providing services to legitimate cannabis businesses that operate legally under state law. After the 2020 elections in which Democrats won “trifecta” control of the federal government, investors had widely expected the passage of several “low-hanging fruit” pieces of incremental legislation that garner bipartisan support including this SAFE Banking Act or the MORE Act even if the more long-shot comprehensive efforts came up short.

Hoya Capital

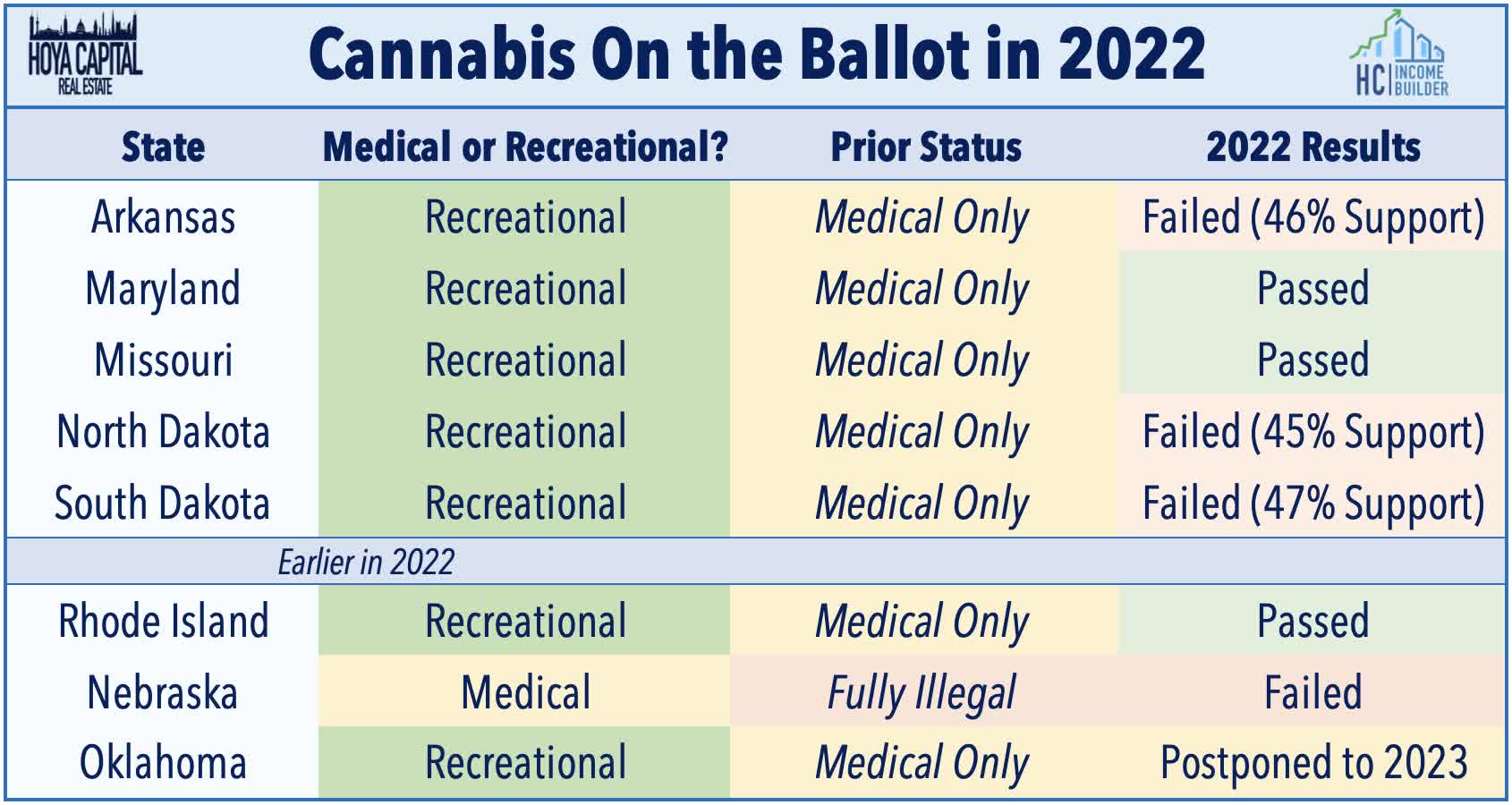

While federal reform efforts have yielded minimal tangible progress outside of one-off pardons and marijuana research funding, the cannabis industry has continued to score incremental “wins” at the state level. Two additional states approved recreational marijuana usage in the 2022 elections – Maryland and Missouri – while legalization narrowly failed in three states – Arkansas, North Dakota, and South Dakota. These two states join six other states that approved recreational usage from 2021-2022 including Rhode Island, New Jersey, New York, Virginia, New Mexico, and Connecticut. With the approvals in Maryland and Missouri, a key threshold was reached as more than 50% of the U.S. adult population now has access to recreational marijuana.

Hoya Capital

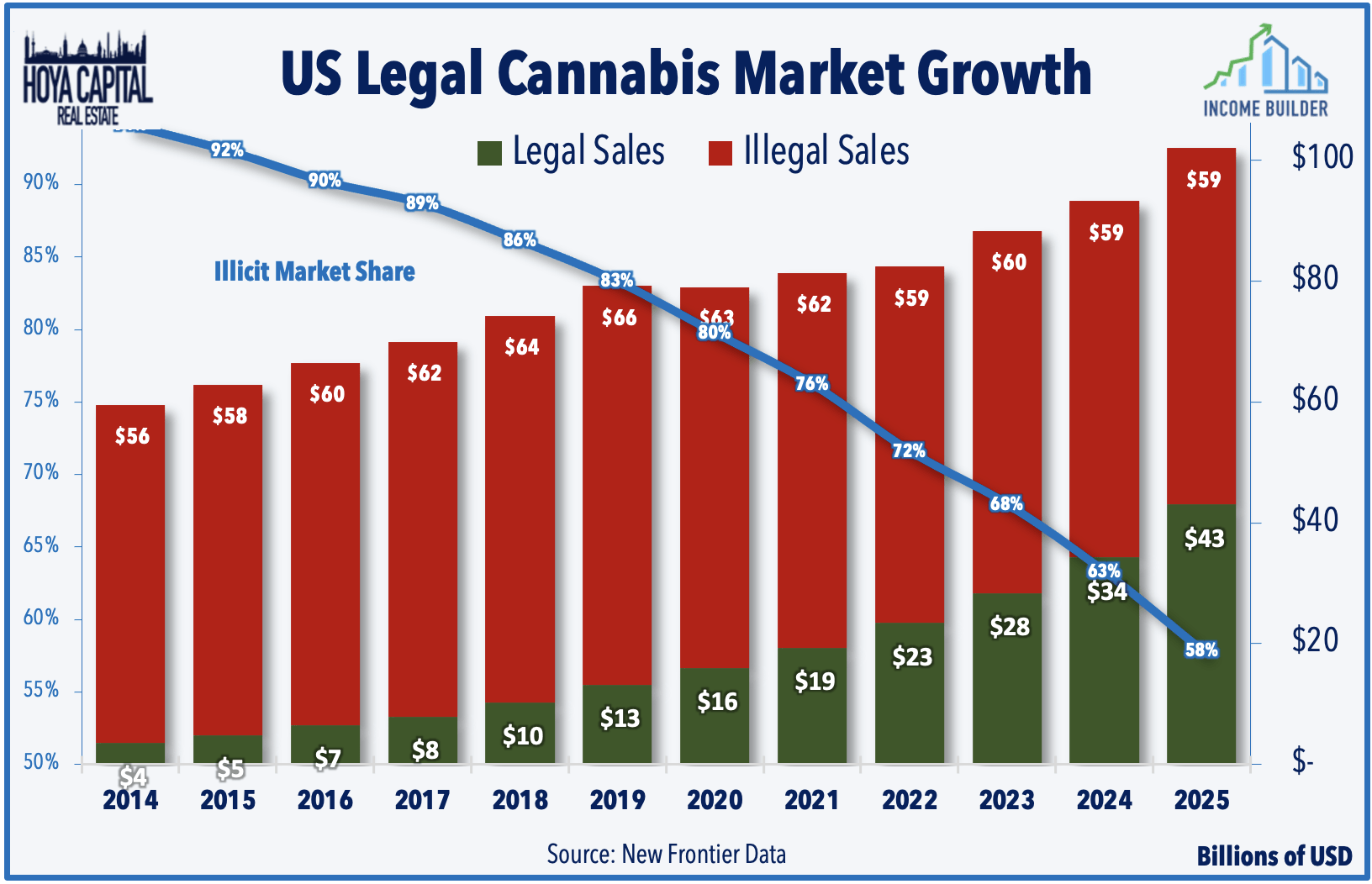

New Frontier Data – a leading cannabis research firm – identified 15 additional states that are likely to enact legalization measures by 2030 which, if successful, would expand access to legal recreational marijuana to two-thirds of the U.S. population. Fueled by this expanded access, the legal cannabis market is expected to more than triple in size during the 2020s, from roughly $16 billion in 2020 to nearly $72 billion in 2030. Per New Frontier, an estimated 27% of U.S. cannabis sales in 2021 were through legal channels, but by 2030, 47% of total annual U.S. demand will expectedly be met by the legal market. If all of the potential markets legalize within their respective expected timelines, the legal market capture could reach nearly 60% by 2030.

Hoya Capital

Cannabis REIT Fundamentals

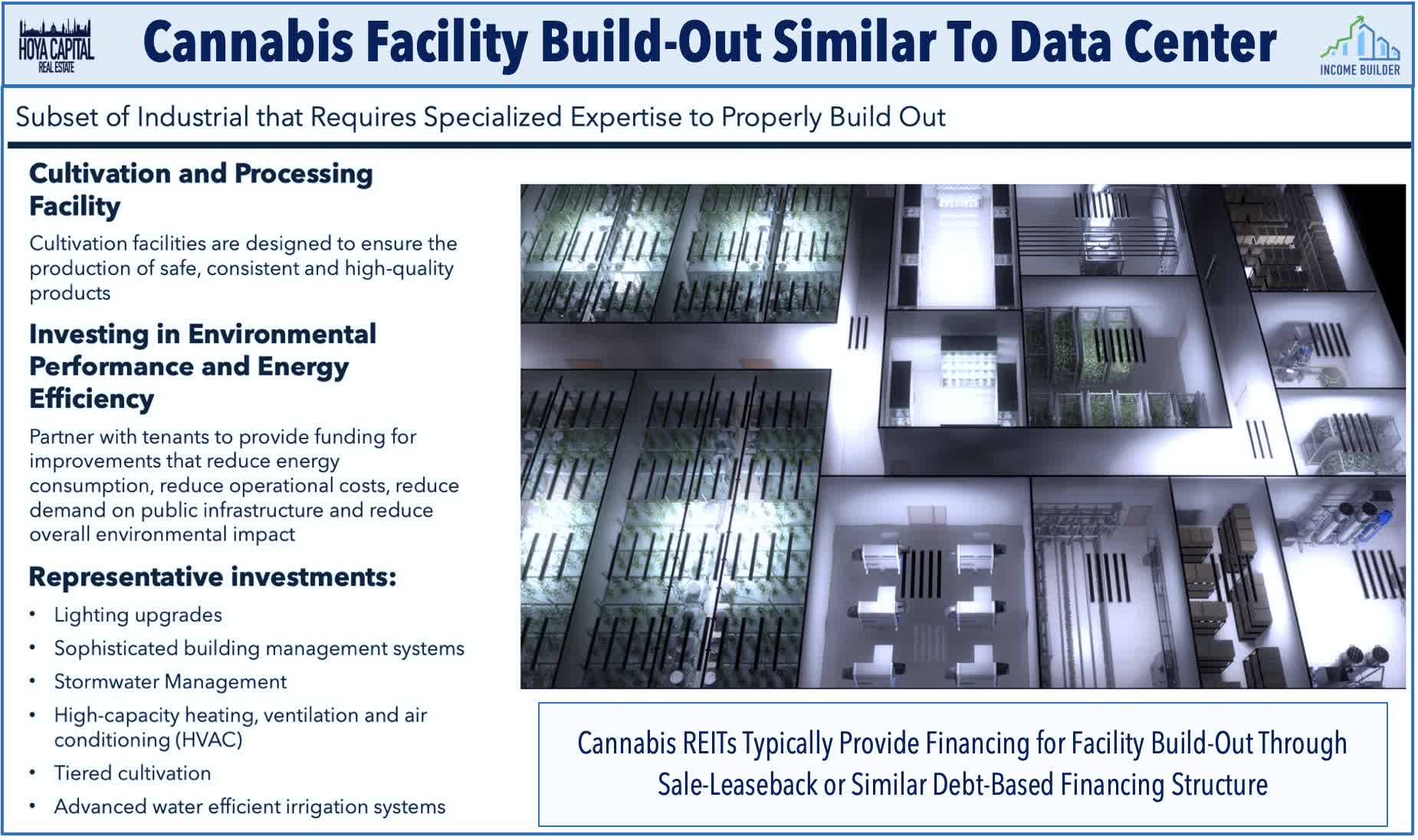

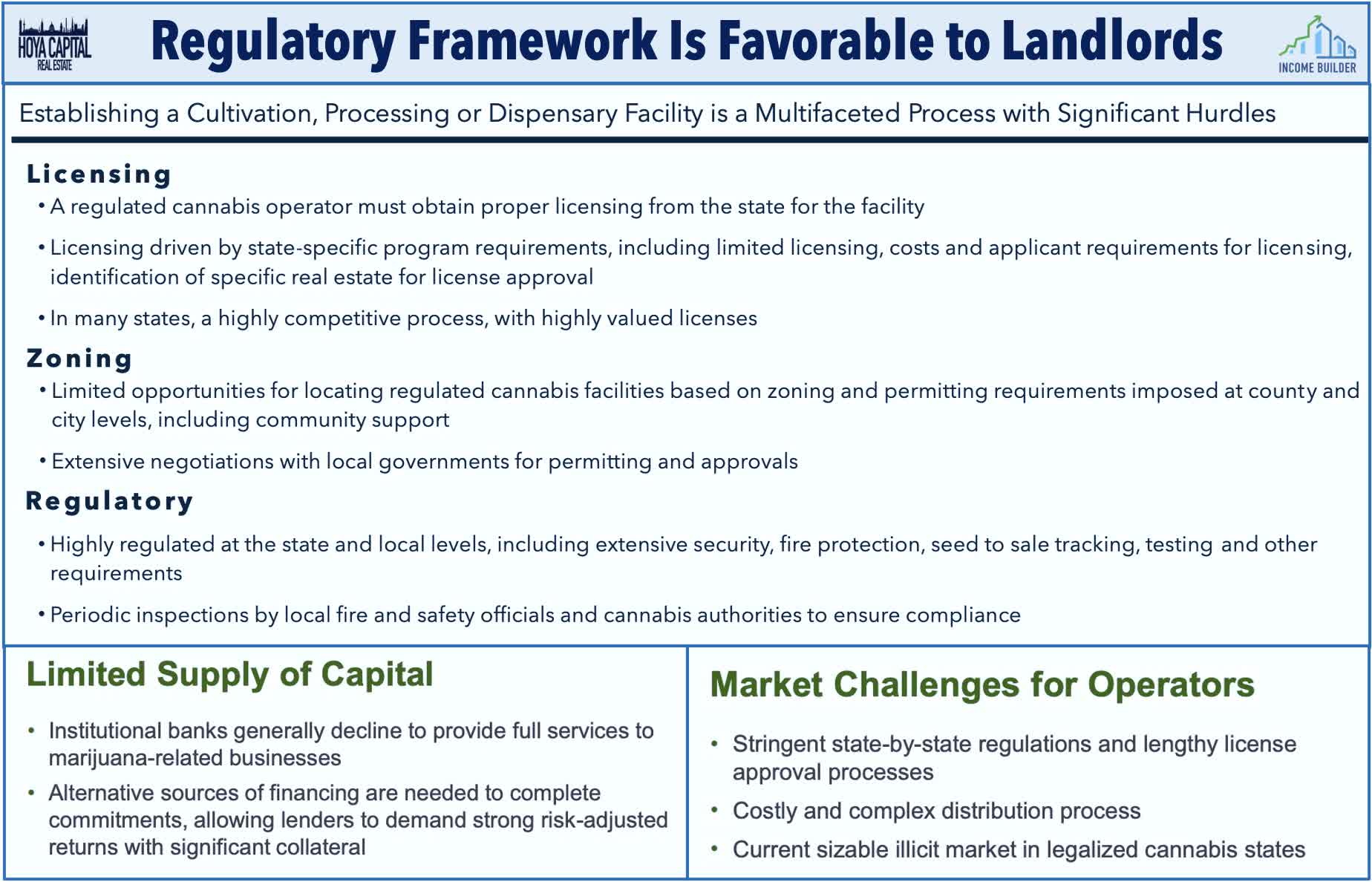

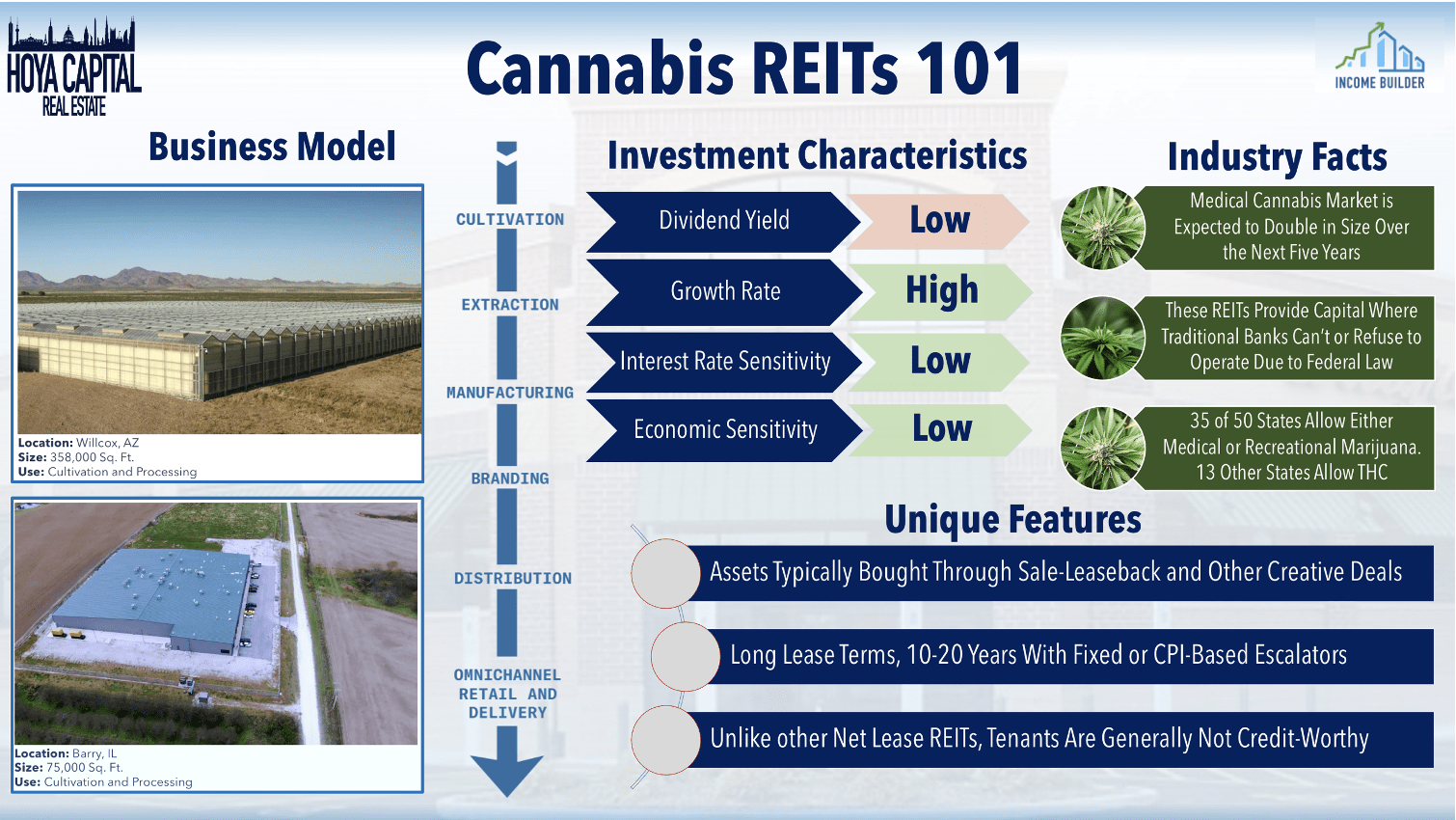

The ongoing federal prohibition – and the resulting limit on access to traditional banking – has forced cultivators and retailers to turn to alternative sources for capital. These REITs effectively serve as “non-bank” lenders to state-licensed cannabis cultivators who often are shut out from access to traditional lending from federally-regulated banks. For equity REITs, assets are typically acquired through sale-leasebacks of cultivation, processing, and retail properties and lease are typically structured as triple-net leases with lease terms of 15-20 years. Cannabis mortgage REITs, on the other hand, typically originate 5-10 year loans collateralized by the underlying real estate, which stays on the balance sheet of the borrower. In either case, the capital provided by the REIT is typically then used by the operator to build-out a new facility or expand an existing cultivation facility, which are typically industrial-type facilities with specialized HVAC, lighting, and irrigation systems.

Hoya Capital

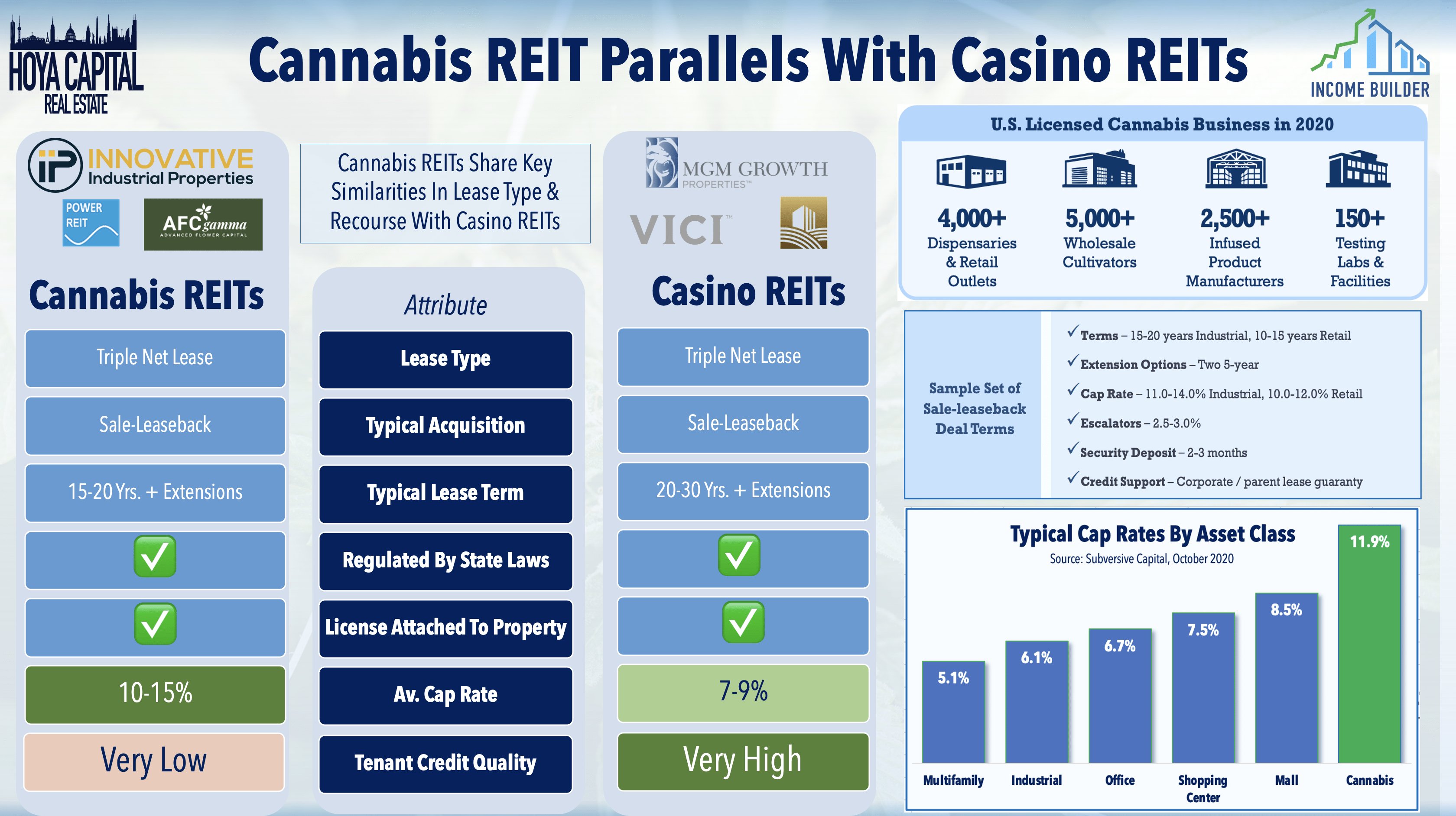

More states have adopted a limit-license framework in which licenses are effectively tied to the property – much like casino gaming licenses – which provides protection for real estate owners and the ability to quickly relet space. In a report on the linkage of cannabis businesses with an underlying real estate asset within state legal frameworks, Hoban Law Group notes, “In many cases, state marijuana statutes and regulations are closely tied to real estate laws.” In Colorado, for example, the marijuana license is attached to the physical premises and stays with the property in the event of default. This ideal legal framework effectively puts the real estate asset at the center of the business and grants the landlord significant protection from tenant non-payment while also serving as a barrier to entry to new supply growth.

Hoya Capital

Under this framework of limited licenses controlled by the state – which is increasingly the “default” structure of newly-legalized states – suggests that REITs could continue to be a primary capital provider even with expanded access to traditional financing sources in the event of full federal legalization. While still early in the evolution of the industry, we continue to see emerging parallels with the casino industry where REITs have carved out a profitable and attractive niche with a sustainable competitive advantage. Reflecting the effects of this legal framework – along with the lack of available capital sources – demand for suitable cannabis real estate properties has outstripped the supply, particularly for large cultivation facilities that are housed in industrial facilities, a property sector that is already in short supply.

Hoya Capital

Leases are also generally subject to parent company guarantees covering operations throughout the United States and, critically, regulated cannabis operators typically must obtain licensing from the state for the facility which typically requires identification of specific real estate for license approval. Given that there’s no shortage of potential tenants in grow facilities and no shortage of demand for cannabis products – but there is a lack of ‘high-quality’ tenants with diversified business operations – we believe that the institutionalization of the cannabis cultivation industry is a net positive for these cannabis REITs over the long-term. For Cannabis REITs – which have concentrated leasing and lending efforts on larger multi-state operators (“MSOs”) and publicly-traded firms in recent years – tenant default issues have remained limited to a handful of smaller single-state operators.

Hoya Capital

Deeper Dive: Innovative Industrial

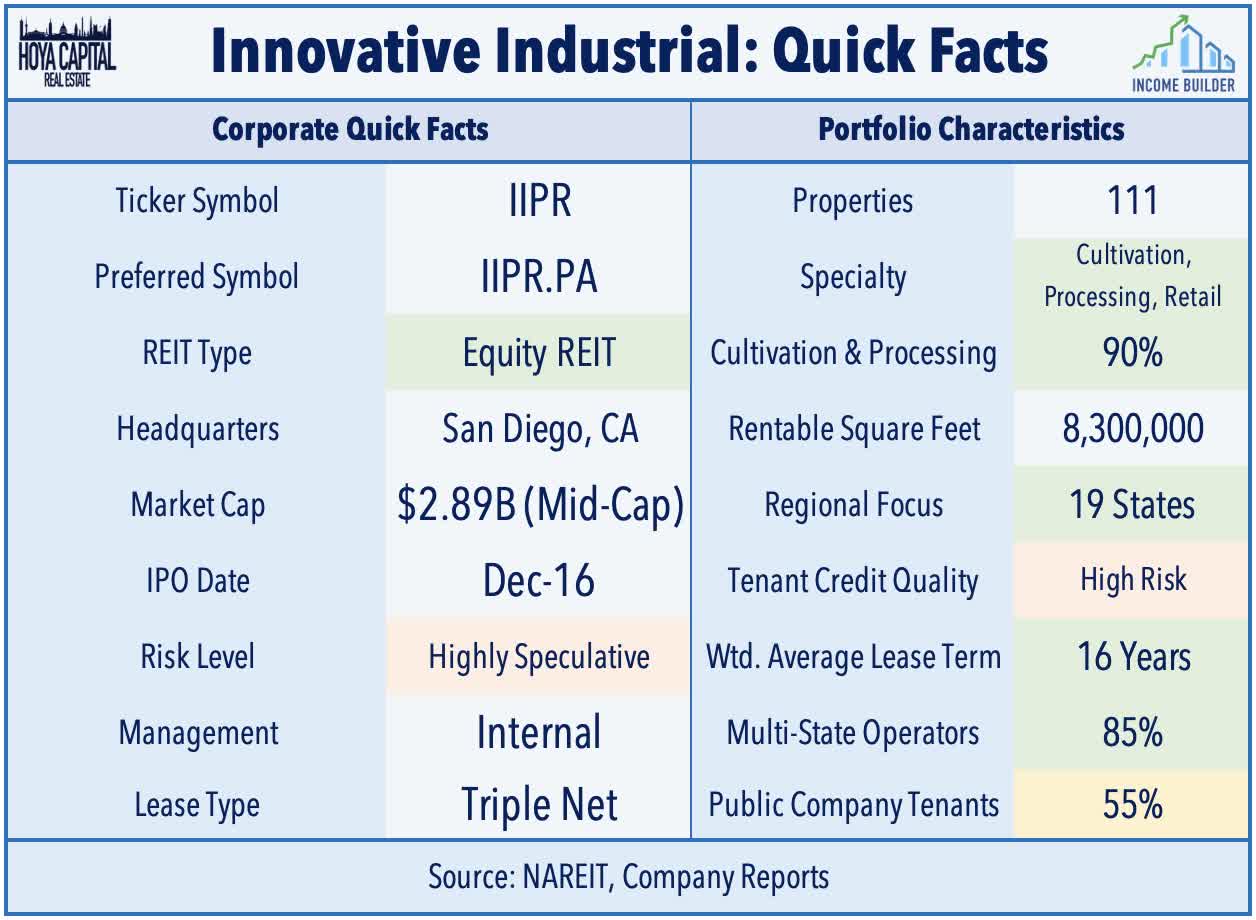

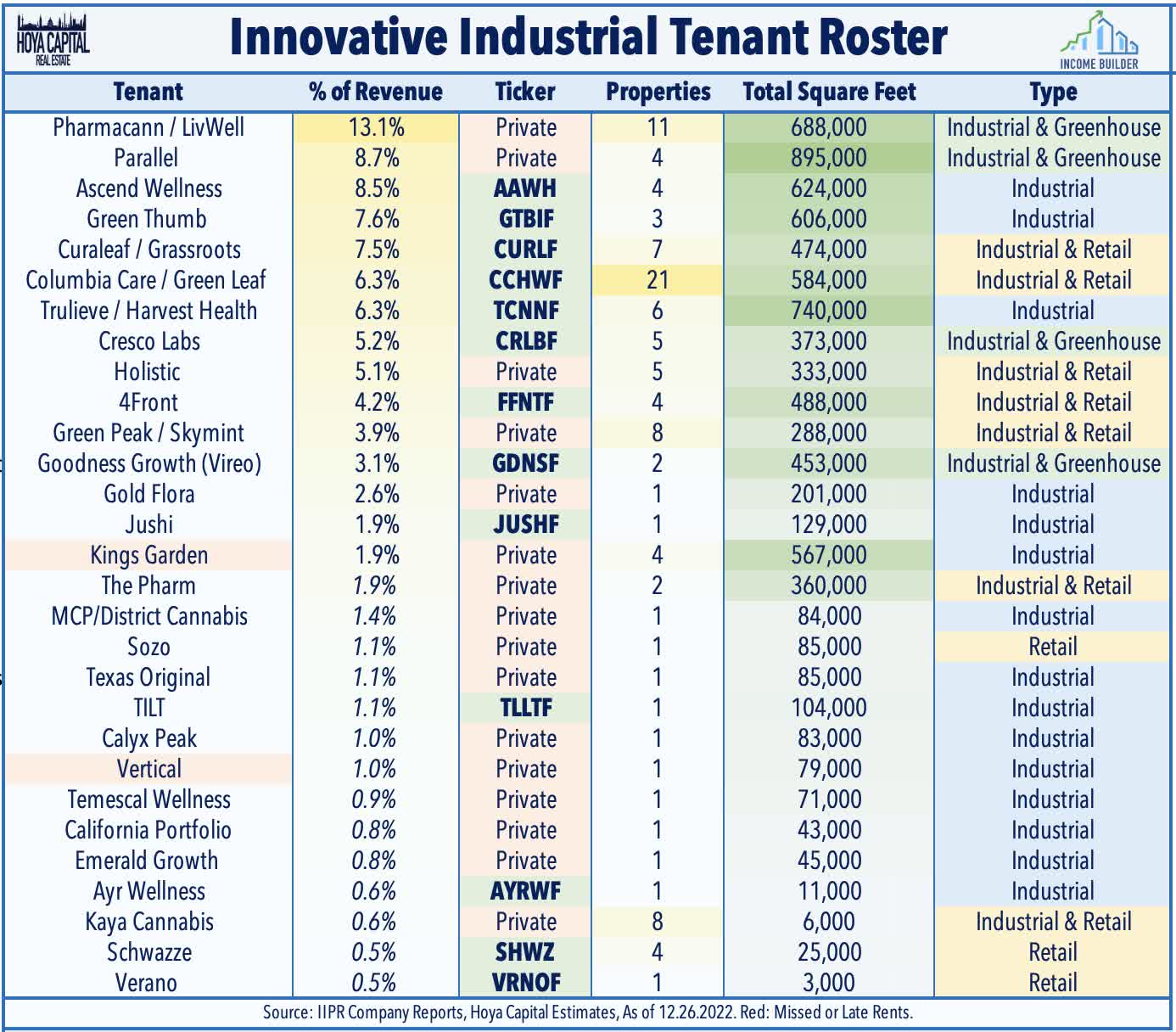

San Diego-based Innovative Industrial Properties (IIPR) was founded in 2016 with just a single property but has been on a continuous acquisition spree over the last five years, expanding its portfolio to 111 properties spanning 19 states and 8.3M square feet. Straddling the classification line between Industrial REIT and Net Lease REIT, IIPR was the first publicly traded REIT to pursue this cannabis-focused strategy. IIPR is now included in the S&P Small-Cap 600 Index and has a listed Preferred (IIPR.PA).

Hoya Capital

IIPR reported last month that rent collection issues remain limited to two troubled tenants – Kings Garden and Vertical. IIPR noted that it has collected 97% of its rent so far this year with the Kings Garden defaults in July responsible for the majority of that 3% of uncollected rent. Encouragingly, IIPR reported that it signed a Letter of Intent for a long-term lease at one of the properties that was formerly leased to Kings Garden in “just over a month of marketing the property.” IIPR now derives 85% of its revenues from multi-state operators and 55% of its revenues from publicly-traded companies.

Hoya Capital

Deeper Dive: New Lake Capital

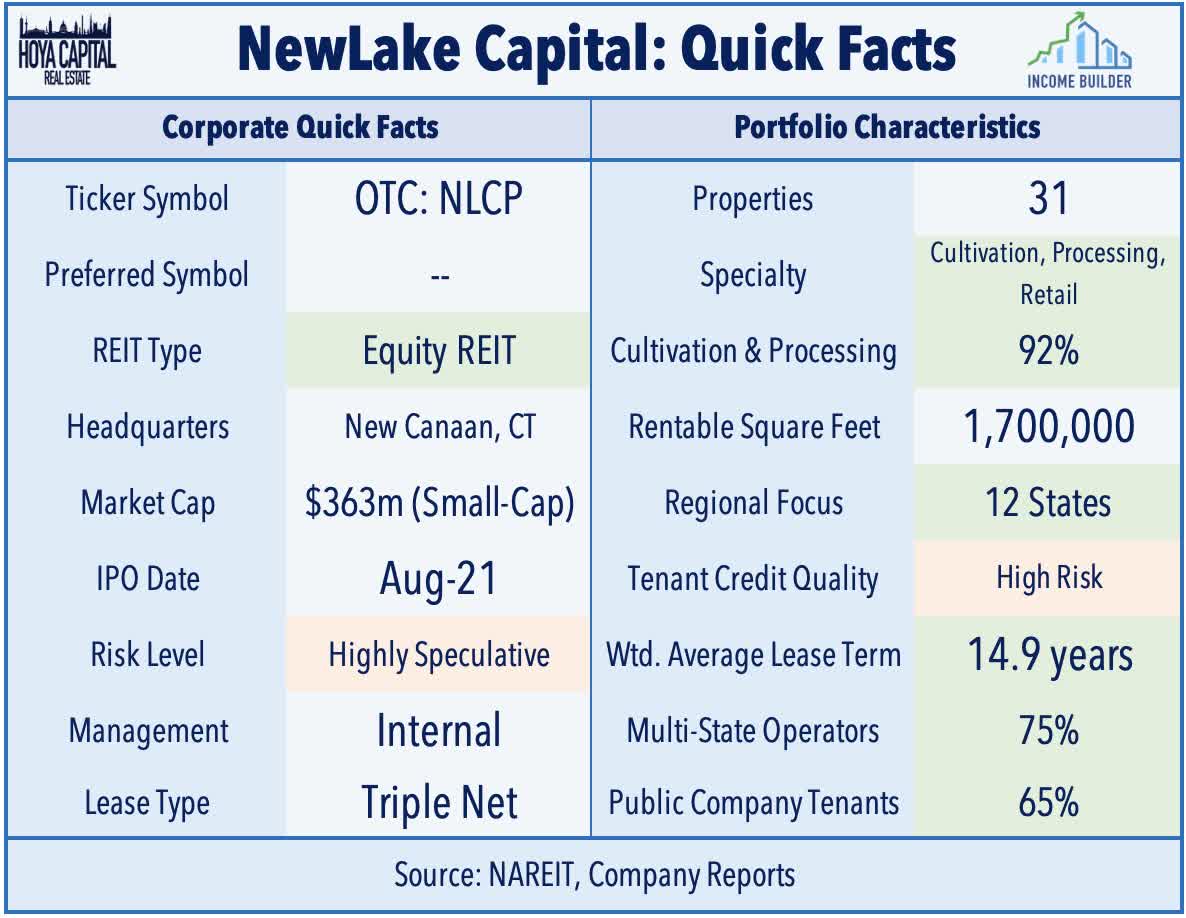

Connecticut-based NewLake Capital Partners began trading on the OTC Market last August following a $102M public offering. NLCP is an internally managed triple-net lease equity REIT that purchases properties leased to state-licensed U.S. cannabis operators. Despite its “OTC-status,” NLCP is the second-largest cannabis REIT by market capitalization and on its recent earnings call, the company noted that it is still exploring an exchange listing on the NASDAQ, but noted that it does “not expect an uplift to occur without regulatory relief or a change in the legal status of cannabis.”

Hoya Capital

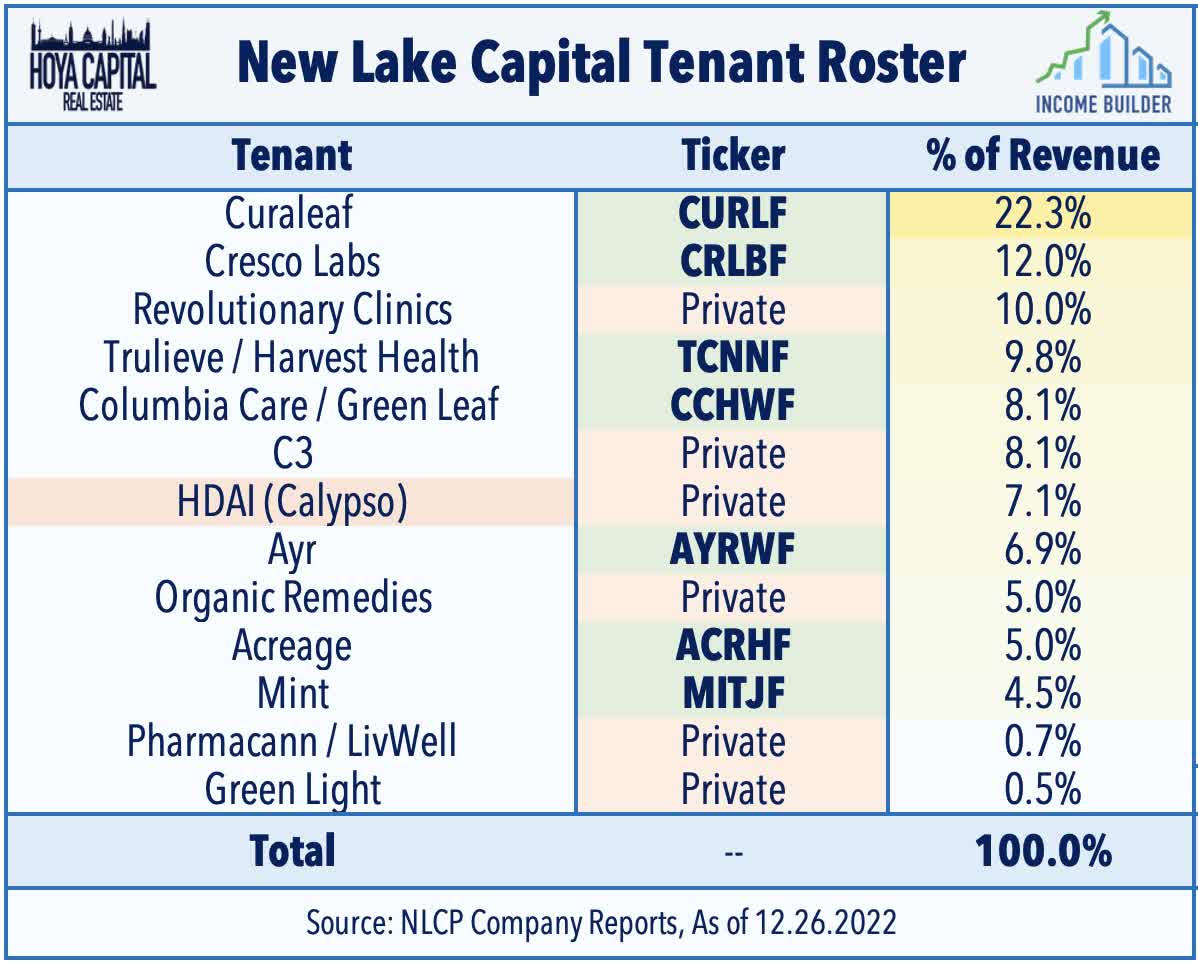

Similar to its larger peer, NLCP has concentrated recent leasing efforts on these larger multi-state operators and now derives roughly 75% of its rental revenues from MSOs and 65% of revenues from public companies – a list that includes several of the same tenants as IIPR including Curaleaf (OTCPK:CURLF), Cresco Labs (OTCQX:CRLBF), Trulieve (OTCQX:TCNNF), and Columbia Care (OTCQX:CCHWF). NLCP noted that it has collected 100% of its rents to date but did comment in its second-quarter call that it’s “just a matter of time until we have a tenant issue to focus on.”

Hoya Capital

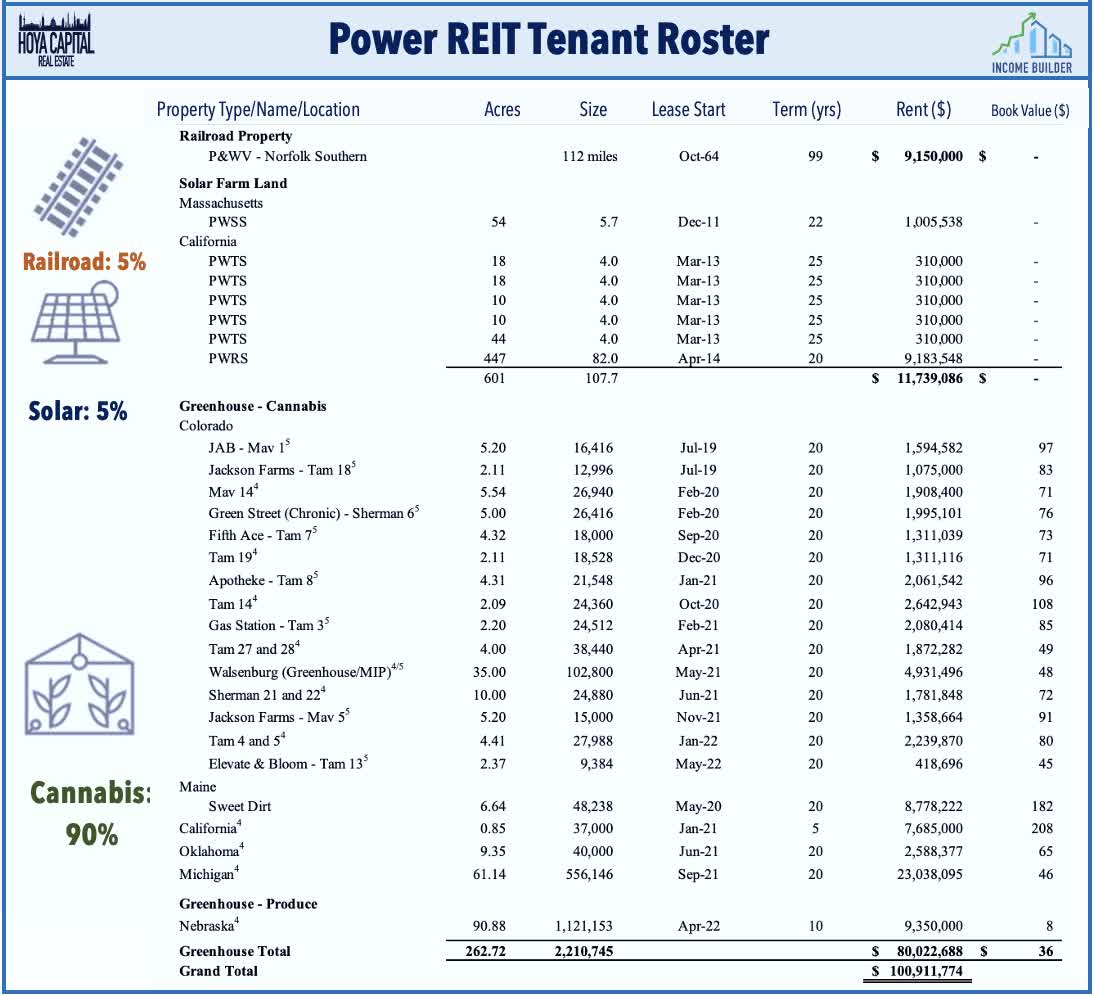

Deeper Dive: Power REIT

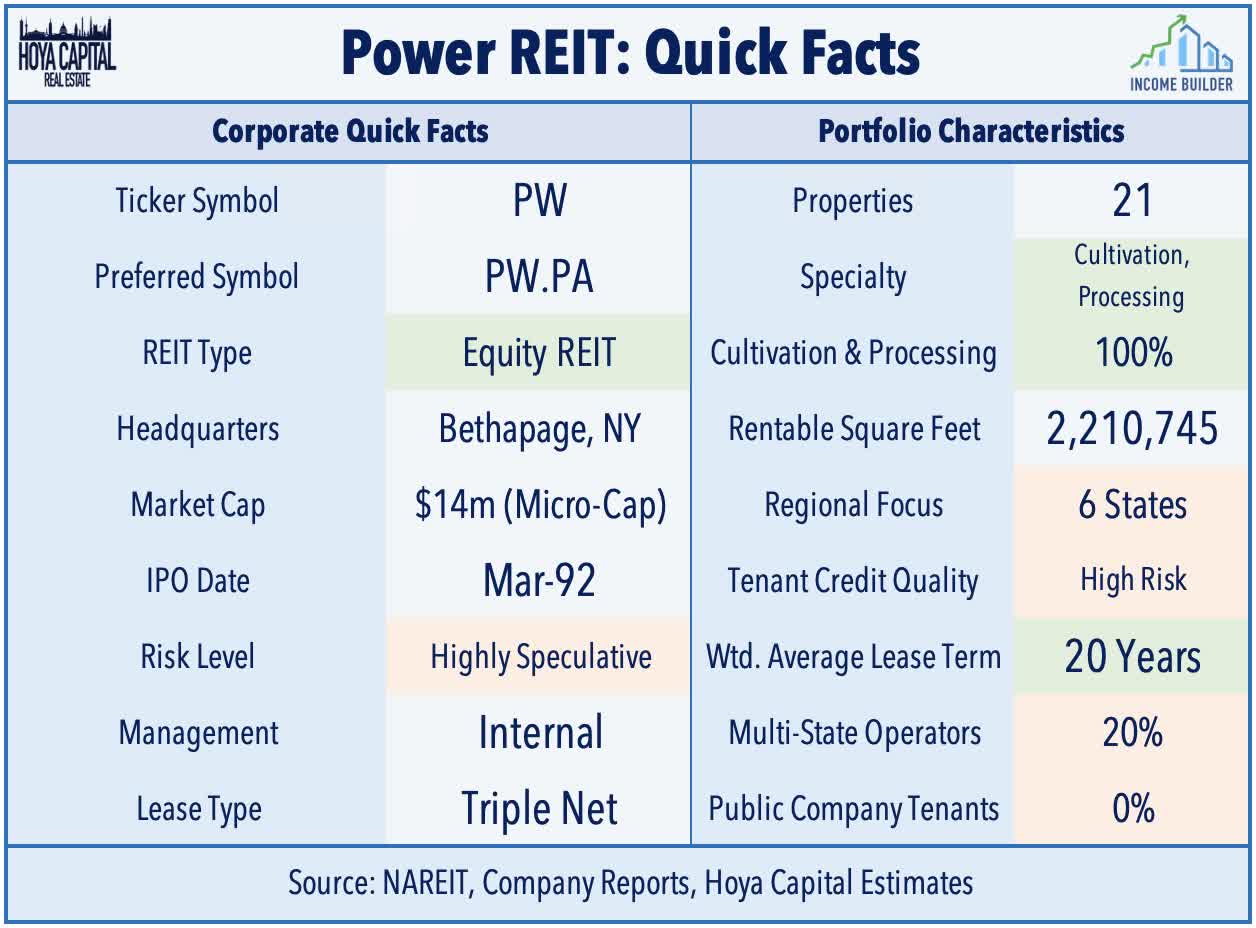

New York-based Power REIT has a more complex operating history, emerging in its current form in 2011 as the successor company to Pittsburgh & West Virginia Railroad. Until it began a strategy shift in 2018 towards a focus on cannabis real estate, the firm was focused on the ownership, development, and management of transportation and energy infrastructure-related real estate. PW is a small-cap REIT and also has a listed Preferred (PW.PA).

Hoya Capital

Power REIT is currently diversified into 3 industries: Controlled Environment Agriculture (greenhouses), Solar Farm Land, and Transportation. Power REIT announced in 2019 that it intends to focus primarily on expanding its real estate portfolio of Controlled Environment Agriculture greenhouse. Power REIT owns 21 CEA properties across six states – Colorado, Maine, and Oklahoma, Michigan, California, and Nebraska – comprised of 2.21M square feet of greenhouse and processing space. Notably, unlike its larger peers, PW’s tenant roster is less “institutional” with the majority of its revenues derived from smaller single-state operators that are not publicly traded.

Hoya Capital

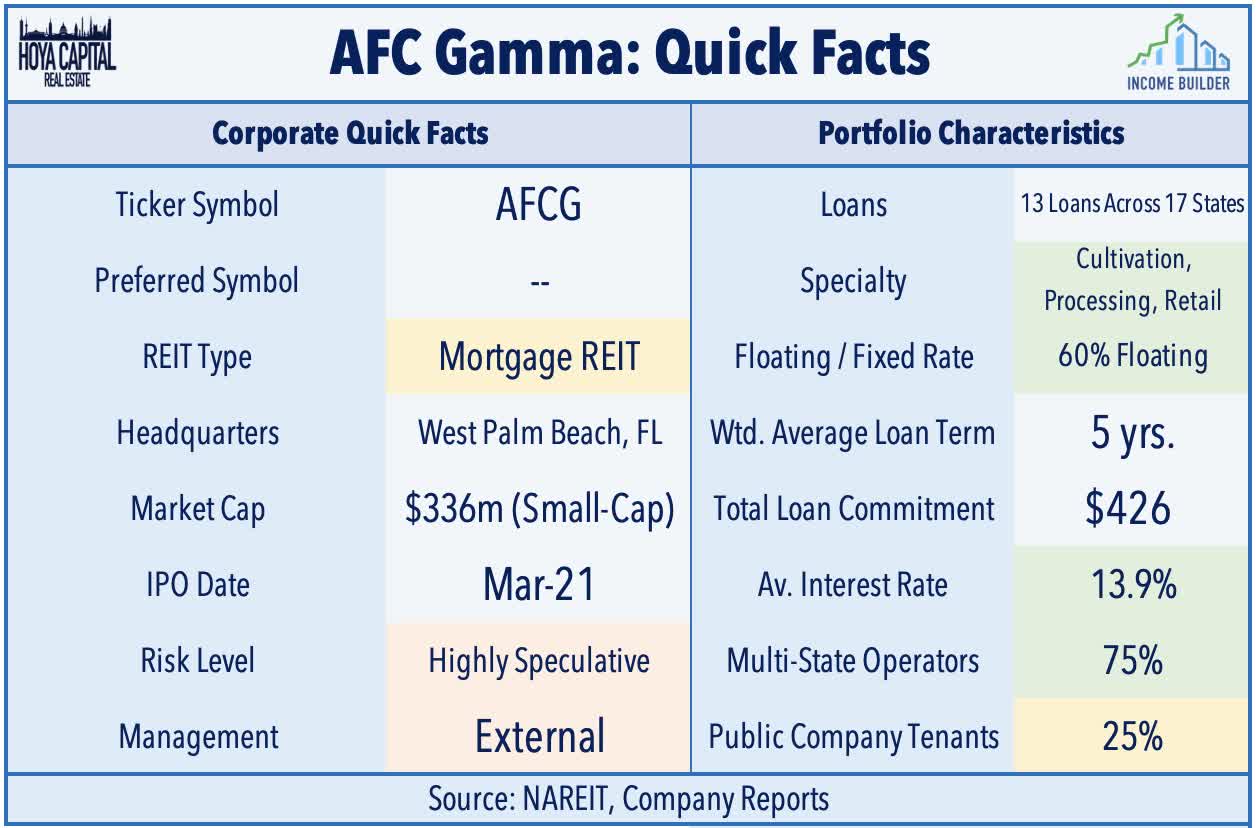

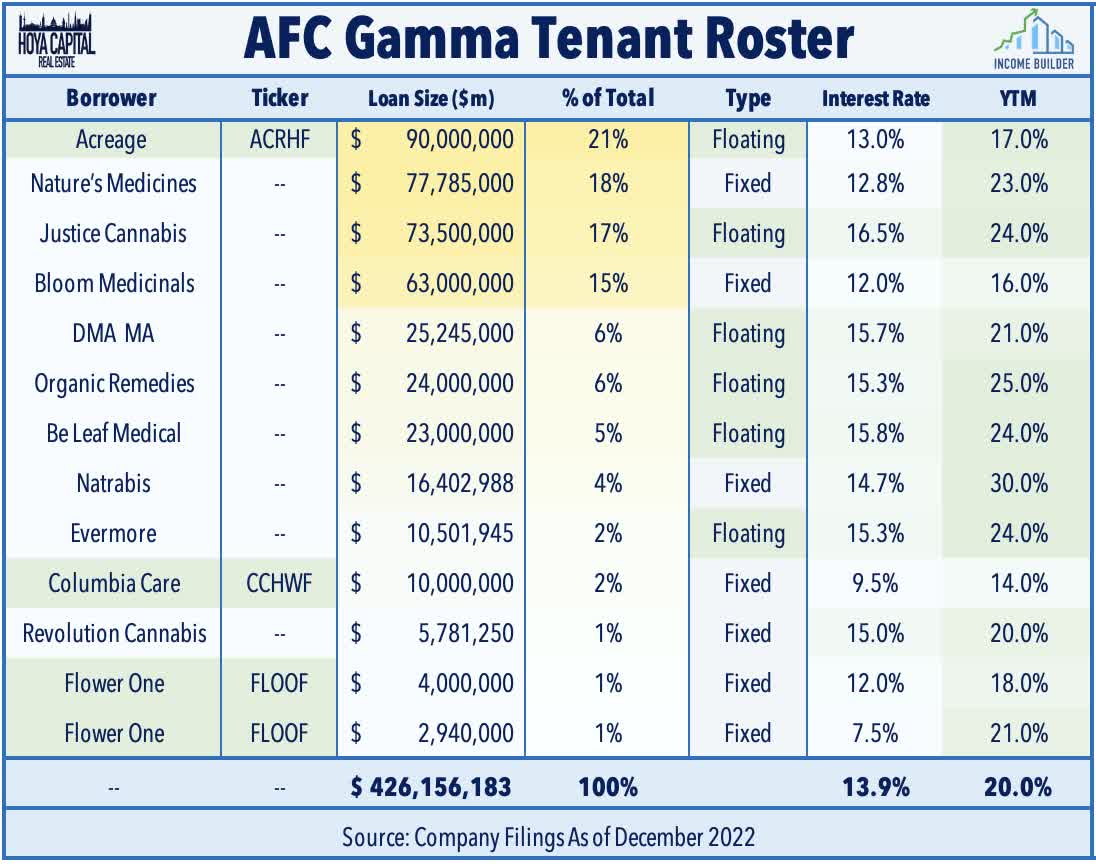

Deeper Dive: AFC Gamma

Florida-based AFC Gamma is one of the two newer publicly-listed cannabis REITs following its $115m IPO last March. Prior to its public listing on the Nasdaq, AFC Gamma operated as a non-traded REIT under the name Advanced Flower Capital and is led by Leonard Tannenbaum, who previously founded the asset management firm Fifth Street Finance. Unlike IIPR, NCLP PW which are both equity REITs, AFCG operates as an externally-managed mortgage REIT, originating and managing real estate-backed loans for cannabis companies. As of September 30, 2022, the weighted average yield to maturity of the portfolio was approximately 20%.

Hoya Capital

AFCG’s portfolio is comprised of loans to eleven different borrowers across roughly 50 individual properties, totaling approximately $426 million in total principal amount. Its loan portfolio has an average cash interest rate of 13.9% and its loans typically have up to a five-year maturity, secured by a lien on the real estate. Roughly 60% of AFCG’s loans are floating-rate and the company noted that all of its loans remain current and performing. Roughly 75% of AFCG’s loans are to multi-state operators.

Hoya Capital

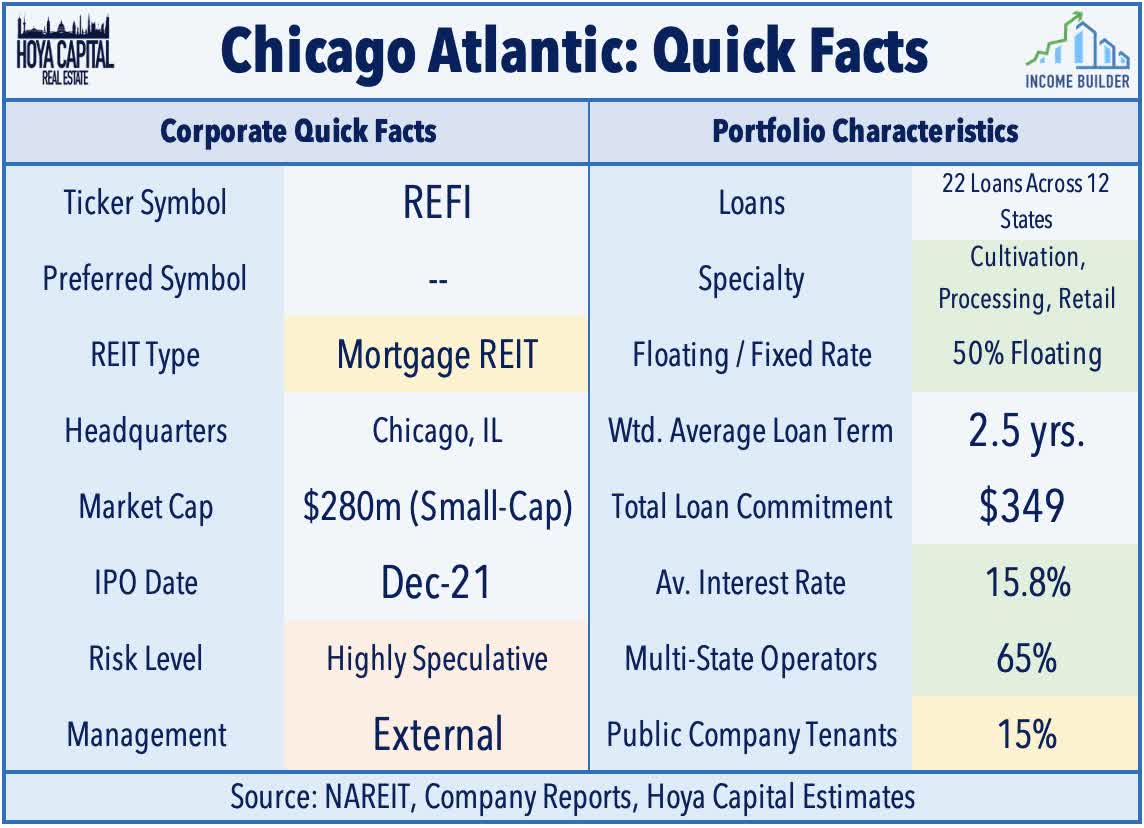

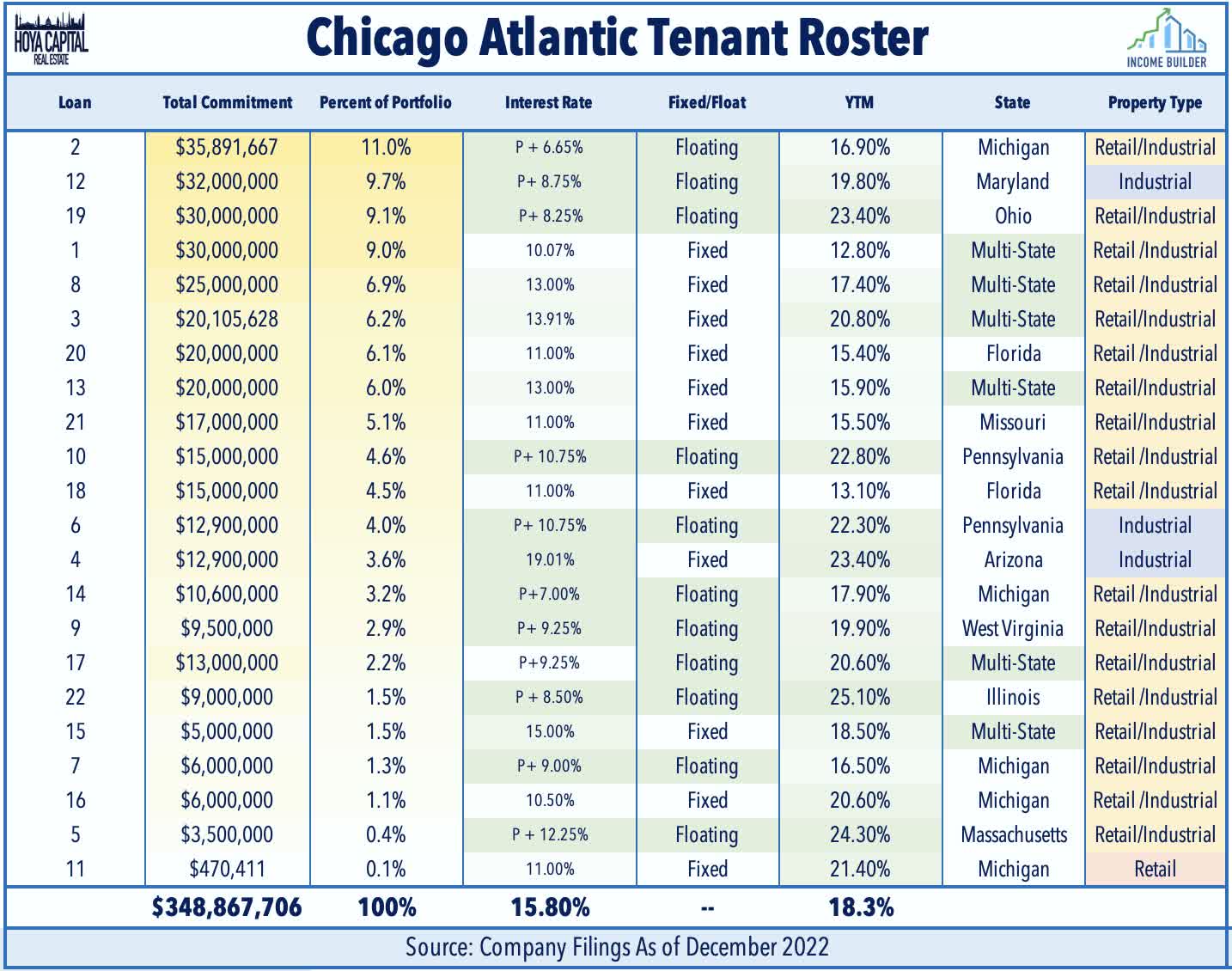

Deeper Dive: Chicago Atlantic

Joining these four REITs, Chicago Atlantic Real Estate Finance (REFI) joined the “pot party” last year. Like AFCG, Chicago Atlantic is a mortgage REIT that is externally managed by Chicago Atlantic REIT. REFI’s loan book consists of $349m in committed capital across 22 loans with an average interest rate of 15.3% and an estimated yield to maturity of 18.3%.

Hoya Capital

Roughly 50% of REFI’s loans are floating-rate and, like AFCG, the company also noted that all of its loans remain current and performing with 65% of its loans made to multi-state operators. REFI notes that its portfolio has a 1.8x real estate collateral coverage and that its loans are typically secured by additional collateral including personal guarantees or by cultivation equipment.

Hoya Capital

Cannabis REIT Dividend Yield

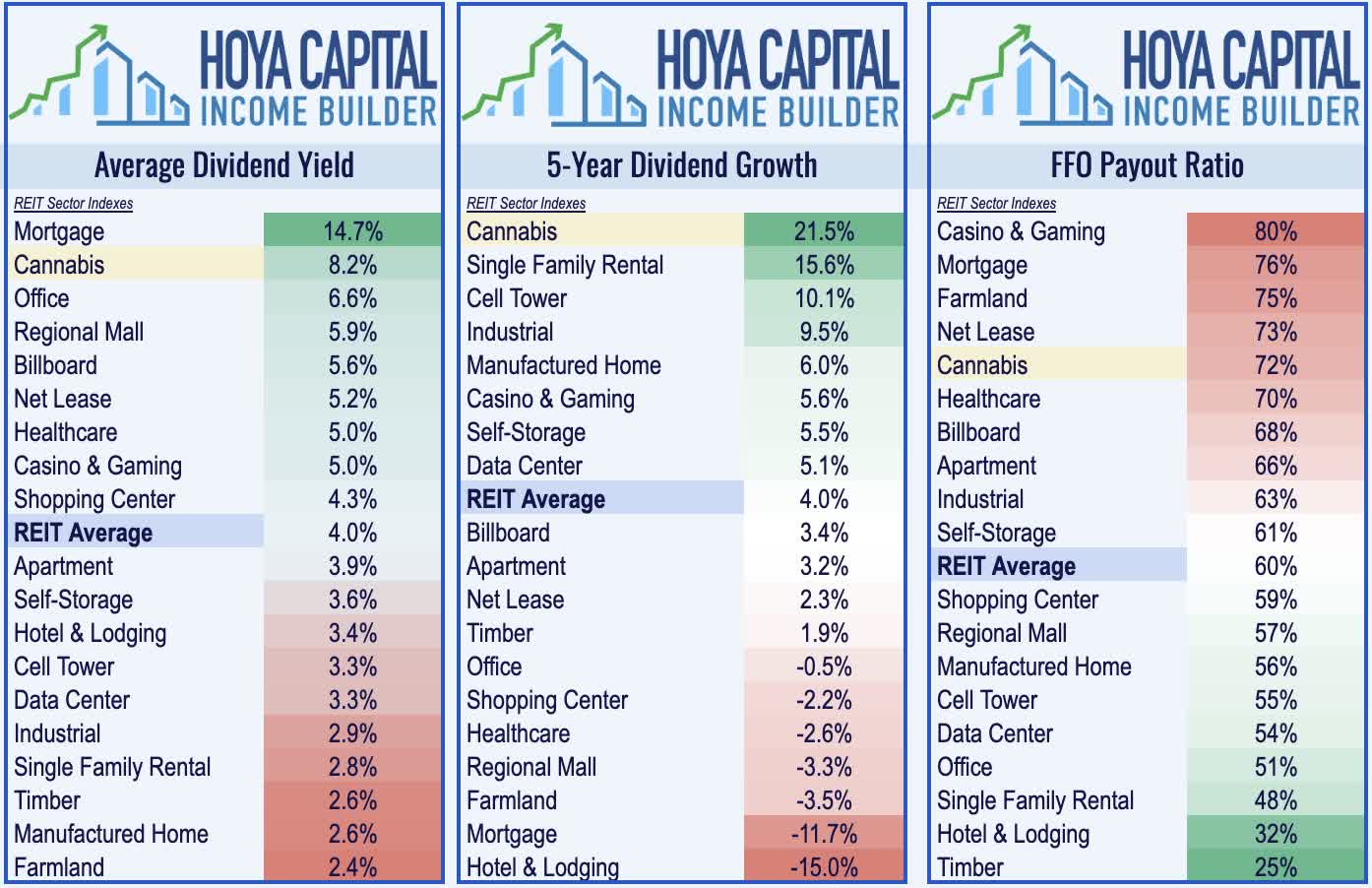

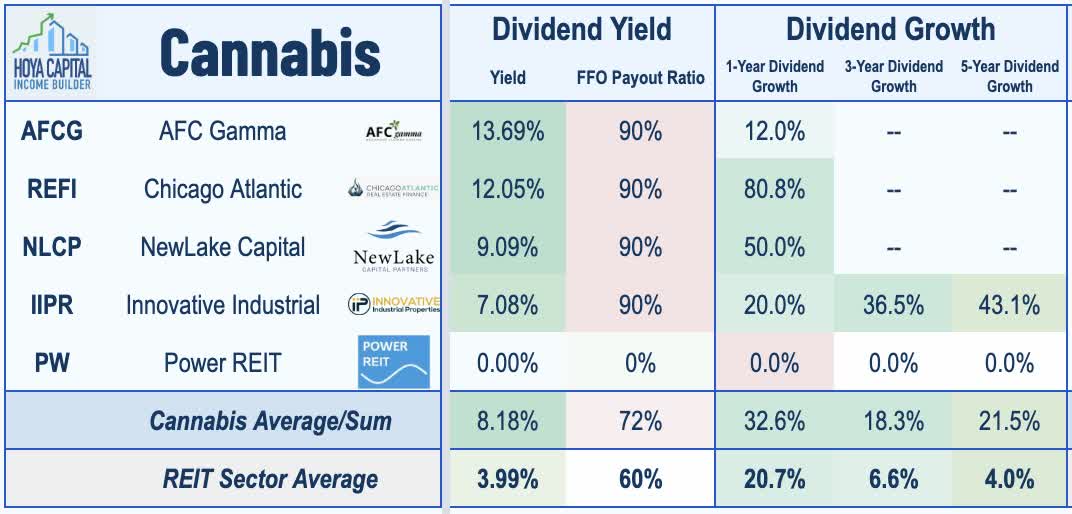

Buoyed by the two higher-yielding mortgage REITs and by another wave of dividend hikes this year, cannabis REITs pay an average dividend of 8.2%, which is well above the REIT market-cap-weighted average of 4.0%. Cannabis REITs have delivered the strongest dividend growth over the past five years, averaging more than 20% per year. Cannabis REITs pay out roughly 70% of their available FFO, however, higher than the REIT sector average.

Hoya Capital

Four of the five cannabis REITs hiked their dividends in 2022. Innovative Industrial hiked its quarterly dividend twice this year to a current rate of $1.80/share which is 20% above its dividend rate in the prior year. NewLake Capital hiked its dividend four times this year to $0.39/share rate – up 26% from the prior year. AFC Gamma raised its quarterly payouts twice to a rate of $0.56/share, which is roughly 12% above last year’s rate. Chicago Atlantic held its dividend steady throughout the year but declared a special cash dividend of $0.29 per share last month. Power REIT, however, has not paid a dividend since 2013.

Hoya Capital

Takeaways: Weeding Out The Weak

Cannabis REITs have been slammed this year amid concern over defaults from their cannabis cultivator tenants, which have been smoked by plunging wholesale cannabis prices and setbacks on federal legalization. Production efficiencies fueled by industry consolidation and the “institutionalization” of cannabis supply chains have pushed wholesale prices down 60% from 2020, which has begun to “weed out” some smaller operators. For Cannabis REITs – which have concentrated leasing and lending efforts on larger multi-state operators (“MSOs”) and publicly-traded firms in recent years – tenant default issues have remained limited to a handful of smaller single-state operators. While still inherently speculative and volatile, valuations of Innovative Industrial (IIPR) appear particularly compelling as we believe that Cannabis REITs have carved out a legitimate competitive niche as primary capital providers to a maturing industry on an undeniable secular growth trajectory.

Hoya Capital

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Centers, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, and Mortgage.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment