franckreporter

Numbers are in Canadian dollars unless otherwise indicated

Dear readers/followers,

Recently, I wanted to diversify my exposure within REITs outside of the US. I’ve looked at a number of companies in Europe and also in Canada. In this article I want to highlight the state of the Canadian Real Estate market, look at a major player within the Canadian residential REIT sector – Canadian Apartment Properties REIT (TSX:CAR.UN:CA) and argue that in order to invest in Canada and given the elevated risks, investors should demand an additional discount and should be very cautious when evaluating potential investments.

Canadian Real Estate market

The Canadian residential market has been on a steep, bubble-like trajectory for some time. The question is whether (and if so when) the bubble is going to pop. Let’s examine some key data points to try to determine this.

- The Federal Reserve’s Q2 2022 index of real home prices shows that home prices (adjusted for inflation) have risen faster in Canada than anywhere else in the developed world, rising by almost 400% since 2000 (compared to only 100% or so in the US).

US Federal Reserve Bank of Dallas

2. More importantly, it is clear that this steep rise has not been fueled by fundamentals as home prices in Canada completely lost touch with real disposable earnings. The chart below actually tells two stories – Canada might be in a bubble and the US surprisingly seems fairly priced.

US Federal Reserve Bank of Dallas

3. One of the drivers of this insane growth (especially during the pandemic) has been unprecedented demand for single family homes with simply not enough homes built. The chart below shows this to be especially true for large metropolitan areas (Toronto, Montreal, Vancouver) where the vast majority of space delivered to the market between 2011 and 2020 was multifamily, while demand has clearly favored single family homes in 2020 (and likely onwards). Understandably this caused a surge in single family prices.

Statistics Canada and Canadian Real Estate Association

4. This high demand came from two places. Firstly, Canada has a steadily growing population with a CAGR of 1.3% over the last 7 years. This growth has been largely fuelled by immigration which the Canadian government is very fond of and plans to continue supporting. With the Immigration Plan calling for about 500,000 new immigrants per year going forward the population and consequently demand for housing is likely to grow at rates similar to those in the past.

Created by Author using data from Statistics Canada

5. Secondly the demand has been fueled by foreign investment, lots of foreign investment. This has been an ongoing pattern, especially in Vancouver, where many foreign investors from Asia (mainly China) like to invest. Recently the Canadian Government has issued a new law, in an effort to improve the affordability of Real Estate for Canadians, which prohibits some foreign investors from investing into Canadian Real Estate. The effect of this is yet to be seen.

6. On the flip-side, higher real estate prices are likely leading to a higher portion of people renting (simply out of necessity) which can be positive for some players (such as multifamily oriented REITs) as it leads to higher demand and potentially higher rents.

To sum-up. It is clear that the market has been out of balance. That doesn’t necessarily mean that the bubble has to pop tomorrow. Investors were surely contemplating the same thing in 2008 and those who didn’t invest would have missed out. With the current ban on foreign investment and Central banks increasing interest rates at an unprecedented pace, it’s clear that the next two years might be difficult for real estate prices.

Does that mean that we shouldn’t invest in REITs that hold properties in Canada? I’d argue that not necessarily. If we can find a REIT that trades well below net asset value, thus providing a large margin of safety and essentially pricing in a significant decline of say 30% in Canadian property prices, it can still make for a good investment. But one should definitely be more cautious and picky when selecting Canadian REITs as the US market seems to be much more in line with fundamentals.

Basics

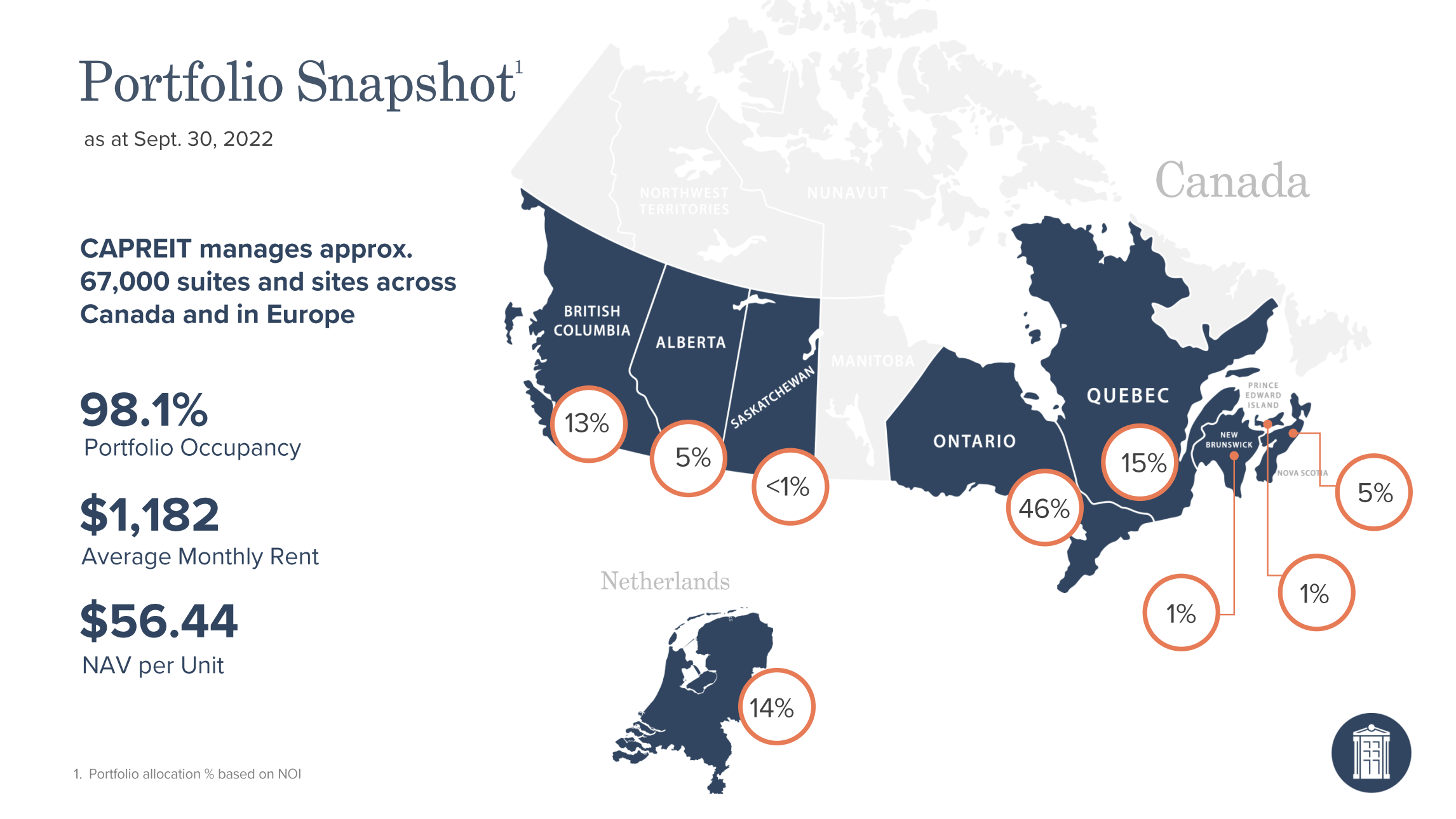

Canadian Apartment Properties REIT or CAPREIT for short is an experienced player which has been on the market for 25 years. They own and operate a diversified portfolio of well-located, residential apartment suites, townhomes and land lease community sites across Canada (86%) and in the Netherlands (14%). The European Exposure is through majority interest held in European Residential Real Estate Investment Trust (ERE.UN:CA)

CAPREIT Investor Presentation

Compared to other major residential REITs such as:

- HOM.UN – a Canadian REIT with properties in the Sunbelt

- Essex Property Trust (ESS) – a US REIT with properties in the West Coast

- AvalonBay (AVB) – a US REIT with properties in the East Coast

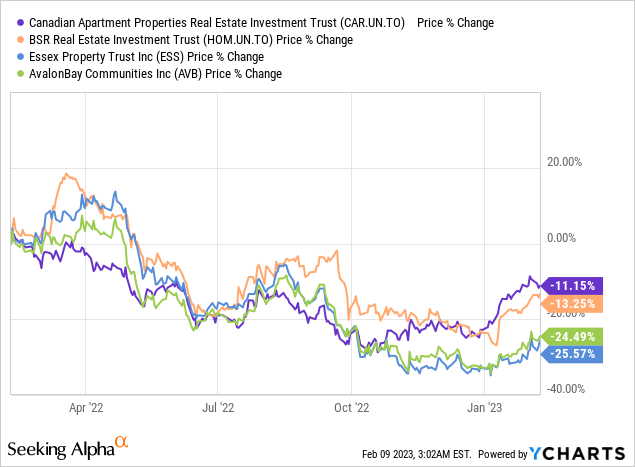

CAPREIT’s price has been quite resilient over the last 12 months. Frankly the comparison is a bit skewed because of the effect of FX as the Canadian dollar weakened against the US dollar by about 5%. Meaning that in USD terms, the securities quoted in CAD below (CAR.UN in purple and HOM.U in orange) have actually done 5% worse than indicated. Still the Canadian REIT performed as much as 9-10% better than its US peers (FX adjusted).

Operations

Some provinces in Canada have strict regulation on rent increase, in particular Ontario and British Columbia cap rent growth for 2023 at 2.5% and 2.0%, respectively. Without the cap, the rental guideline increase would have been calculated to be 5.3% and 5.4%, respectively, based on the Ontario and British Columbia Consumer Price Indices. This is important as it applies to 59% of the company’s portfolio.

Q3 2022 Report

In this regulated environment the company was able to generate same property NOI growth of 0.7% as of Q3 2022. Overall NOI increased by an impressive 5.4% in the same period mainly due to recent acquisitions. The REIT also has a very stable occupancy, which has been around 98% over the past three years.

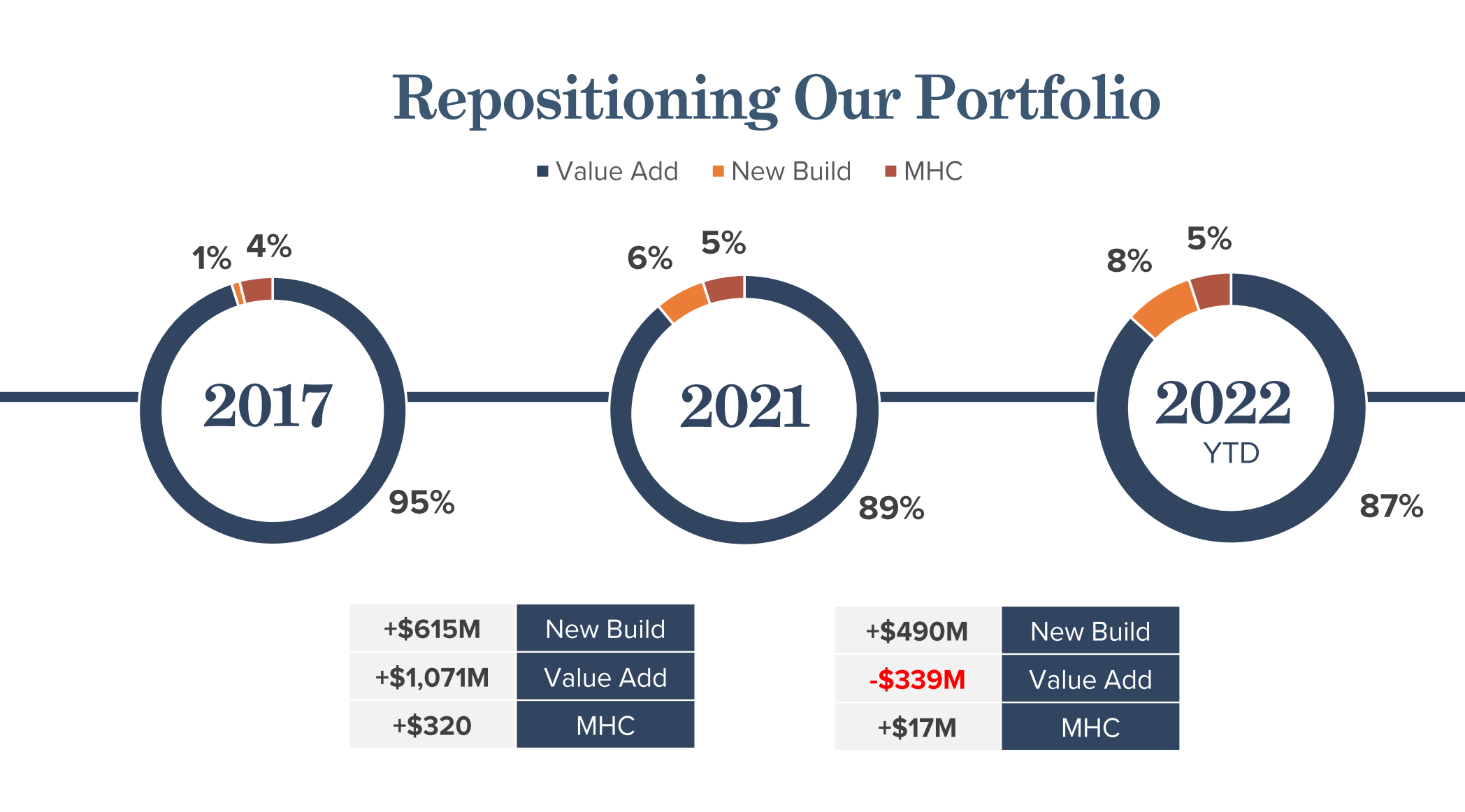

The company has remained active on the acquisition front even in 2022, acquiring about $500 Million of new build assets in BC and QC. Management stated their focus on acquiring new build properties in an effort to enhance portfolio quality and diversification. Their disposal have been in line with this statement as they sold around $340 Million worth of older assets (mostly built in 1960s and 1970s). I like this approach as new build properties are more likely to attract tenants and generate higher rents – but arguably the company has work to do on this front as the vast majority of space is still quite old.

CAPREIT Investor Presentation

Financials

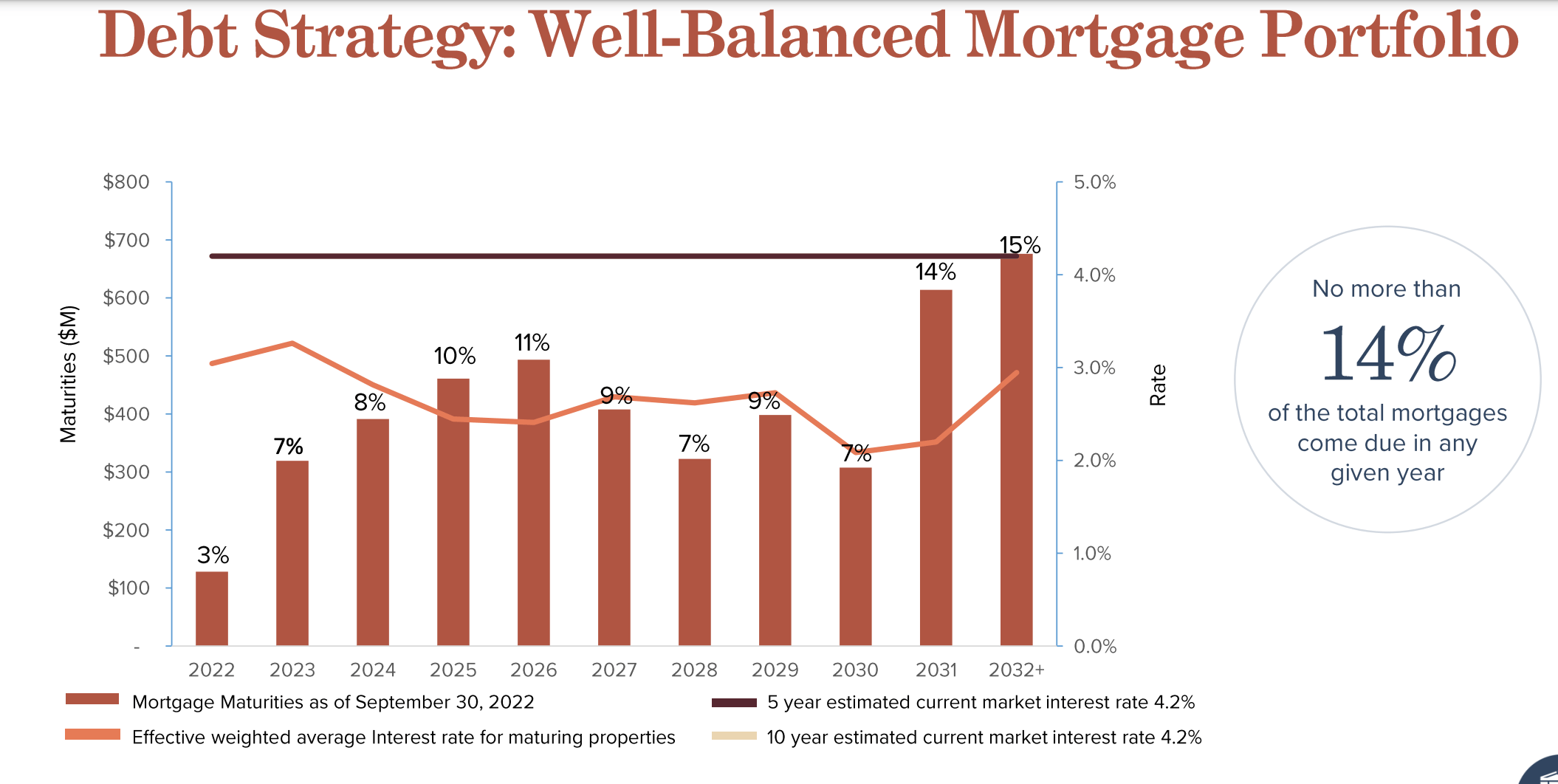

The company has $6.8 Billion of debt outstanding, 99% of which has a fixed interest rate. Debt maturities are spread over time with 7% and 8% due in 2023 and 2024, respectively. This means that the REIT will have to repay/refinance about $500-$550 million of debt in each of the next years. In the current difficult macroeconomic environment, I frankly prefer REITs that have little or no maturities until at least late 2024 as I consider this a potential risk for the company. With about $400 Million in FFO in 2023 and about $100 Million in cash, the company will likely not be able to repay this debt in full from cash from operations. It could therefore be forced to refinance (likely at a higher rate).

CAPREIT Investor Presentation

Valuation

Finally let’s consider valuation. The shares currently trade at $49.00 which translates into 21x FFO. This is actually above the long-term historical average of 18-20x FFO depending on the timeframe. It is also above the multiple of its peers with ESS trading as low as 16.2xFFO.

Created by Author using data from Fast graphs

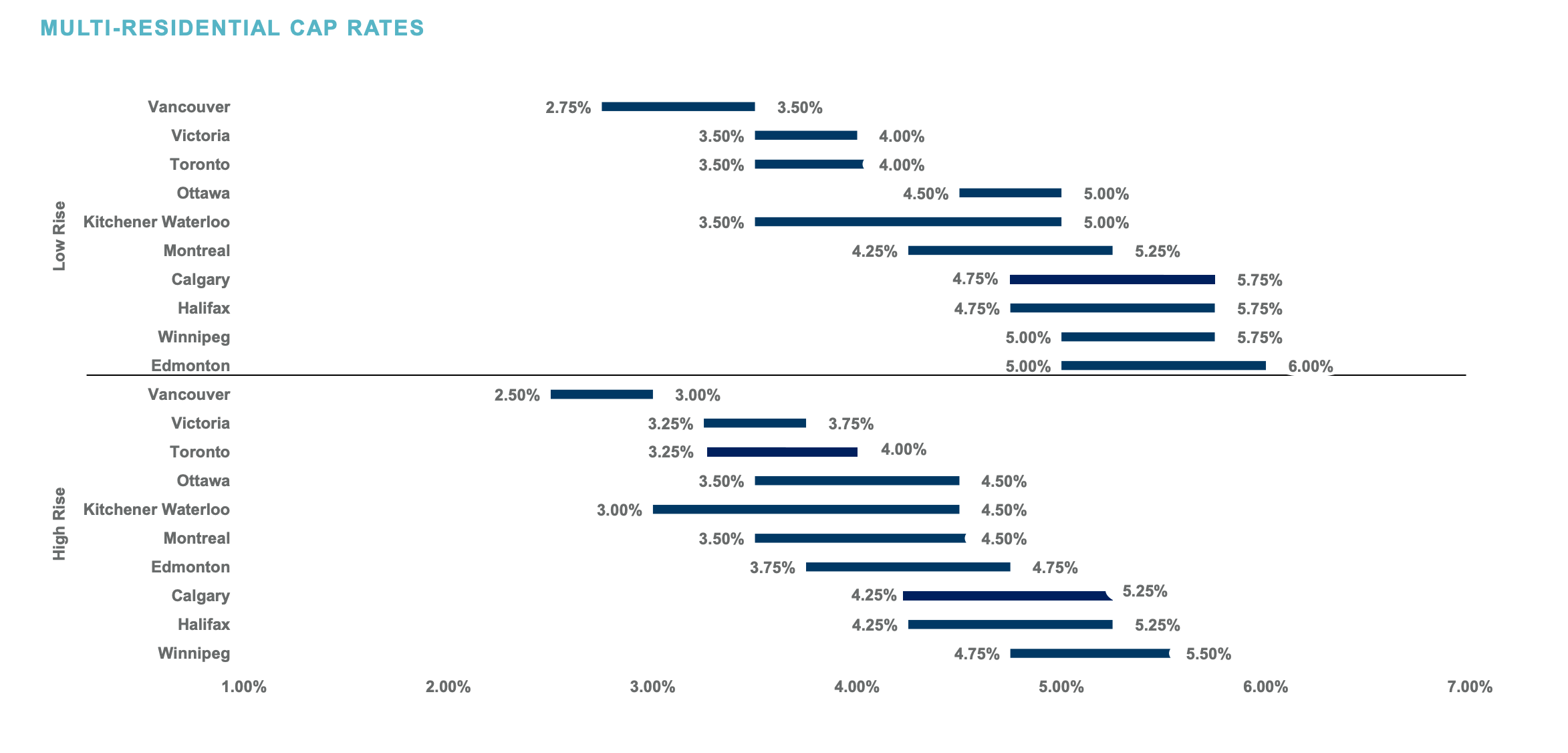

On a NAV basis, the company reports its asset at a book value of $17 Billion corresponding to a yield/cap rate of 3.68%. Cushman&Wakefield report the following market cap rates. Since most of CAPREIT’s properties are in low-rise older buildings it’s easy to see that the reported cap rate of 3.68% is way too aggressive. I’d argue that a fair cap rate, based on the table below, for the company’s assets would be at least 4-4.25%.

Cushman&Wakefield report

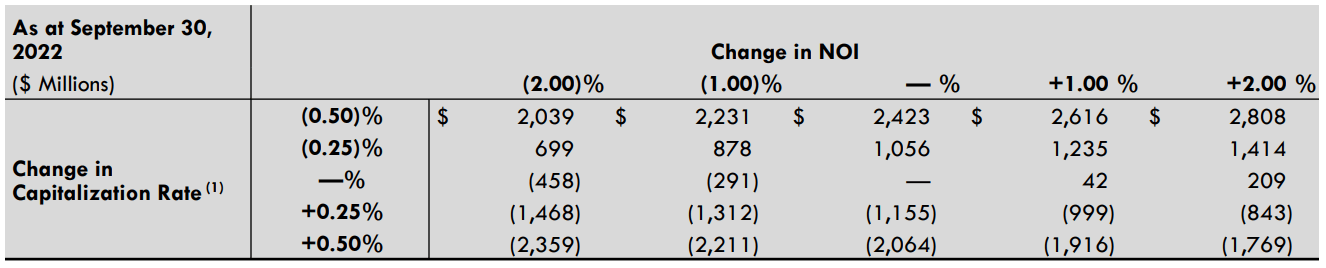

Canadian Apartment Properties was nice enough to provide a sensitivity analysis for the cap rate. If we assume a 50 bps increase in rate (3.68%+0.5%=4.18%), the asset fair value would actually be $2.36 Billion lower. Deducting this from the original $17 Billion we get $14.6 Billion.

Q3 2022 Report

With total debt at $6.8 Billion we get NAV of $7.8 Billion. This is slightly below the market cap of $8.3 Billion that the company currently trades at. This paints a very similar picture to the relative valuation method above. The company is simply slightly overvalued here at $49.00.

Investor Takeaway

It might be tempting to diversify one’s REIT exposure into another country and indeed Canada might seem like a good option. The problem is that the Real Estate market up north has experienced an unprecedented boom fueled by immigration and foreign investment and has become completely detached from fundamentals. Now with a new law passed, which prohibits foreign investment for the next two years, one of the major drivers of price increases is gone. Add to this the tight monetary policy of Central Banks with increasing rates and you get a potential for a major correction in the market. Of course this correction will not happen overnight and might not happen at all, but it is an increased risk that investors should reflect in their decision making.

Any investment into Canadian real estate should therefore be thoroughly analyzed to make sure that the margin of safety / discount is large enough to protect the investor in case of a larger market correction. Canadian Apartment Properties REIT seemed like a potential candidate, but our analysis revealed that although it’s doing very well on an operational level, it is not worth the risk as it has significant debt maturities in the following two years and most notably it is not undervalued. CAP.UN trades at fair value here at $49.00 and therefore deserves a “HOLD”. I would only consider this REIT if the price were to fall at least by 20-25%.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment