ogichobanov/iStock via Getty Images

Critical crack spreads and a management update confirm that Calumet Specialty Products (NASDAQ:CLMT) continues to perform at the same high level as in previous quarters. The news is stunningly consistent, thus continuing to offer investors a unique vision into December’s performance and insights into future quarters. The two timely indicators appearing recently almost forced us to write an article. Through consistently strong results comes investing confidence.

Crack Spreads

With the quarter ending, data for two key crack spreads WTI/WCS and the Gulf Coast 2-1-1 are available. The following table summarizes the results.

| Spreads * | Oct | Nov | Dec | Average | ** June/September Qtr |

| WCS | $22 | $21 | $22 | $22 | $15 |

| GC 2-1-1 | $50.5 | $38 | $30 | $40 | $39 |

* Generated using our data set gathered from the EIA and OilPrice.

** WCS uses the June quarter for the December quarter comparison with Great Falls being down for most of the September quarter. The GC comparison uses the September quarter average.

The Great Falls asphalt refinery operated at half rates during December with the other half being filled with Montana Renewables (MRL) feed.

The above table shows that the December quarter and September quarter will be very similar in financial performance.

Management’s Press Release

With the stock price lagging miserably near $12 after reaching into the $20 just a few weeks prior, management issued a press release updating December operational performance, which drastically positively lifted the stock. A bulleted summary follows:

- Montana Renewables and Montana Refining

- The 12,000 bpd specialty asphalt refinery is operating at full rates on Canadian heavy crude.

- Started up the RND hydro-cracker on Nov. 5 operating at 6,000 barrels per day.

- With the commissioning of the renewable hydrogen, SAF, and feedstock pre-treater in the 1st quarter, rates will be lifted to 12,000 barrels per day.

- Preliminary engineering and procurement is beginning for the expected 2024 expansion including an option to maximize SAF yield to 85%.

- Montana Renewables recently acquired the second reactor needed for its MAX SAF option.

- Specialty News

- Shreveport experienced a week plus of unscheduled downtime due to cold weather.

- Demand continues to be healthy considering routine seasonal volume patterns.

- Expect soft winter season margins for asphalt.

- Specialty margins remain strong.

Financial Performance Estimate

With the above data, a reasonable estimate is possible. But, an additional bit of information is also helpful. During the December quarter North American refineries operated at abnormally high rates compared with past seasonal weakness. EIA report data has the rate near full; last week it was at 92% when normally it is the middle 80’s this time of the year. We expect volumes in December to be similar to September in the fuels business, minus a week shutdown. Asphalt margins will be thinner.

In the past, December quarter specialty volumes tend to be lower from peaks in June and September. Past performance suggests a $10-$20 million lighter report.

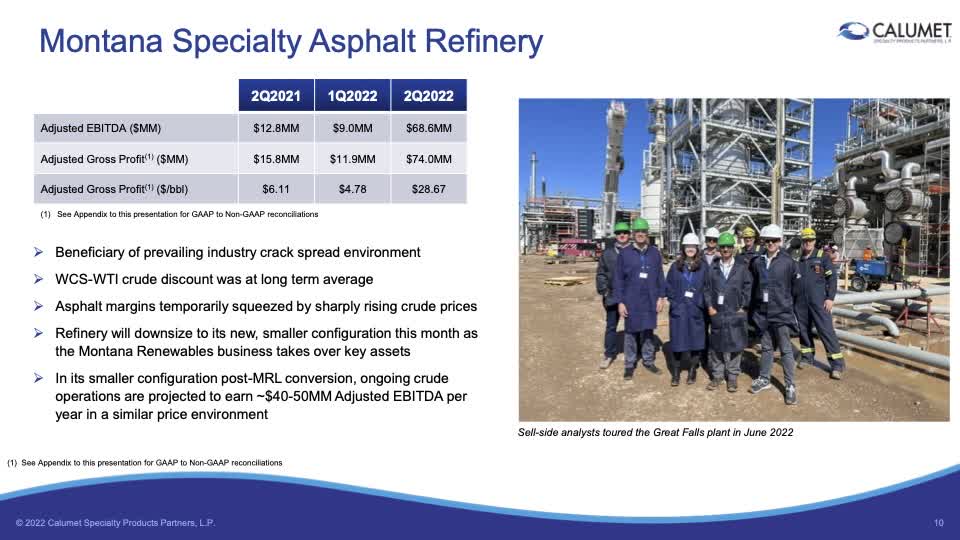

The Great Falls refinery now operates at half rates compared to the past. In the June quarter, the business produced $70 million in EBITDA shown in the next slide.

Calumet Specialty Products

With similar base margins plus significantly higher WCS spreads mixed in with seasonal weaker asphalt margins, a valid estimate might be half of the second quarter performance or $35 million in EBITDA.

With minimal operation of the MRL portion of the refinery, an estimate at $0 is in order. Management noted at the last conference that a minimum volume level would be needed before significant the plant would generate meaningful levels of EBITDA.

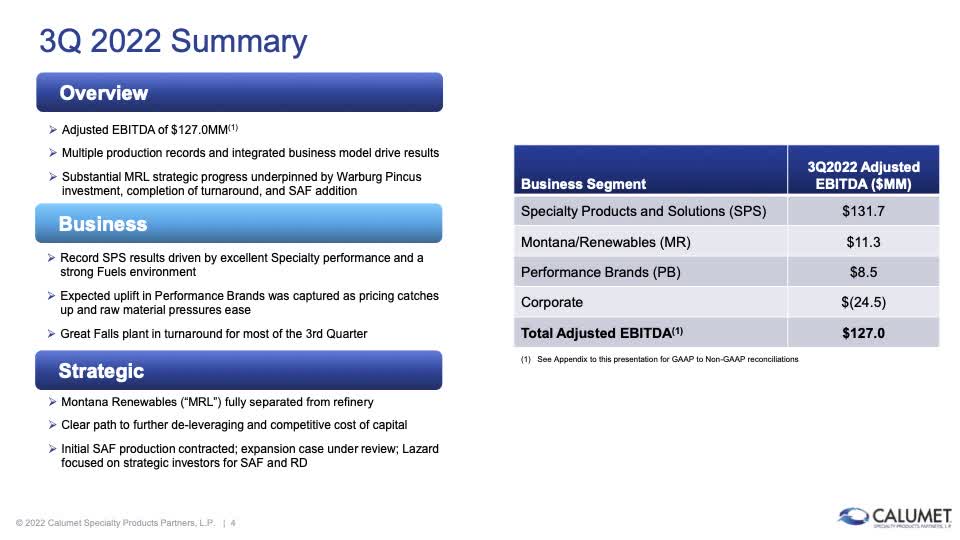

A final piece for the estimate is the specialty performance for September. The next slide summarizes the result for September.

Calumet Specialty Products

Specialty generated $130 million with Performance Brands generating $9 million. Performance has been lagging in its financial achievements mainly due to the short cycle production routines required to catch up lost production from a year ago. Again, management noted at the third quarter conference that this issue was resolving itself. A following table summarizes our estimate for December:

|

Dec. EBITDA Estimate (Millions) |

Specialty | Performance | Great Falls | MRL | Corp. Overhead | Total |

|

June |

$70 | $0 | ||||

| September | $130 | $9 | $11 | $0 | $25 | $128 |

| December Estimate | $100 * | $12 | $35 ** | $0 | $25 | $120 |

* Seasonal asphalt margin reduction plus slightly seasonal weaker sales volumes.

** Improved WCS margin offsets all or most of the asphalt weaker margin.

Our qualitative estimate suggests that December will be the same or similar to the September quarter. Our guess suggests that $120 million plus or minus $15 will result. But investors must not forget the importance of the coming significant revenue from MRL. With its full startup coming in the March quarter, total EBITDA will most likely be significantly higher.

What Does This Mean?

The company, without MRL, is obligated to pay out approximately $30 million a quarter in interest and $20-$30 million a quarter in capital. Generating $100 million plus in EBITDA ensures those payments plus much more are possible. The $50-$70 million extra each quarter can be used to reduce debt or increase capital for essential needs. For example: Calumet has $200 million in debt due in 2024. At $70 million a quarter above cash needs, three quarters might be enough to pay that debt.

Risks

In our view, Calumet’s primary risk resides with a limit number of refineries, that being two. Should either one shut down for lengthy periods of time, Calumet’s performance suffers significantly. Also, future fuel’s spread performance may be at risk. Before 2020, crack spreads ranged in the $15-$20. Since early 2021, with demand returning, cracks jumped $20 on average. Our stance: this increase isn’t short-term in natural. Owners shuttered capacity during the pandemic and since. “U.S. refining capacity has fallen by 5.4%, or 1.03 million bpd to 17.9 million bpd since it peaked in 2019 at 18.98 million bpd. Capacity in 2021 dropped 4.5% to 18.13 million bpd.” In the most favorable light, supply is tight. In the least favorable, it is insufficient.

Of most importance for investors, this December quarter, though a generally seasonal weaker financial quarter, reflects the low side for future performance of the business without MRL. It isn’t small. In the next two years or so, Calumet will likely delever its balance sheet and began to invest in growth capital projects. With MRL coming on stream, the future is very bright. Unit prices under $20 suggest cheap valuations. We continue to recommend a buy on the stock, a strong buy on weakness.

Be the first to comment