satsitt/iStock via Getty Images

Thesis

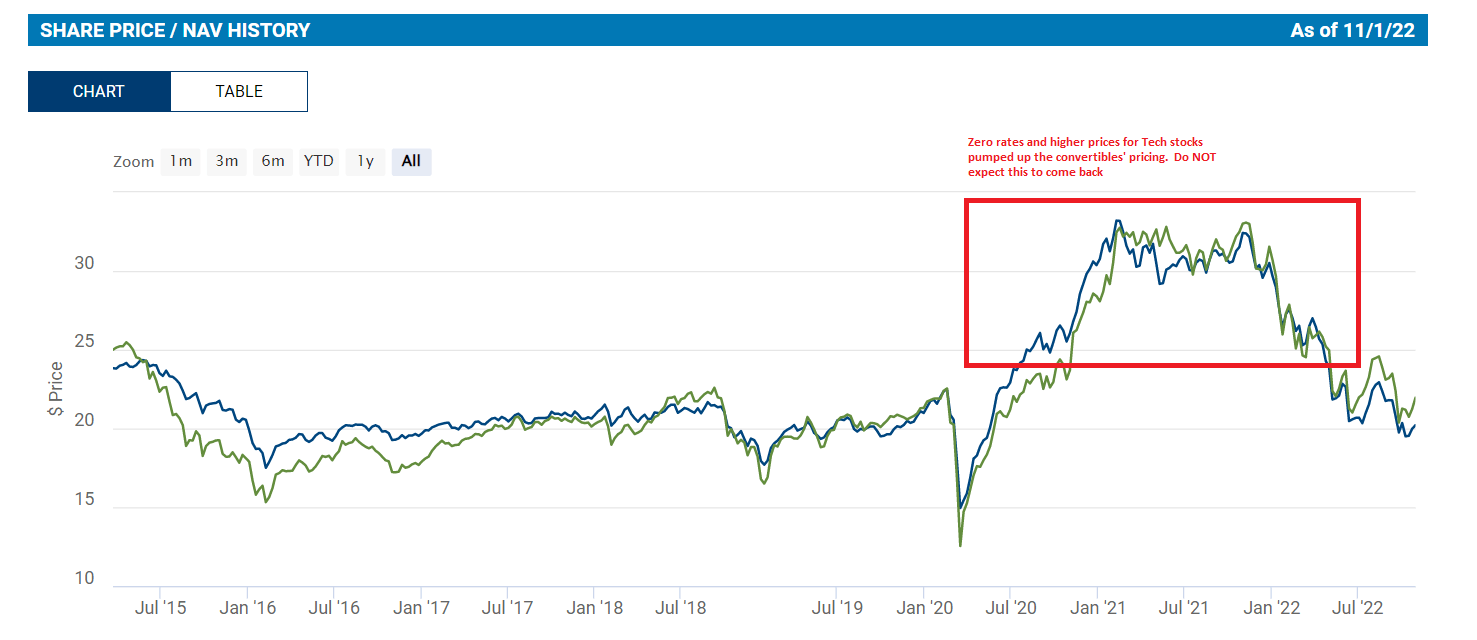

Calamos Dynamic Convertible and Income Fund (NASDAQ:CCD) is a closed end fund focused on convertible securities. The vehicle is overweight convertible securities, which currently account for over 78% of the fund. The CEF has had an outstanding performance during the 2020/2021 zero rates environment, but has returned to a more normalized NAV level as higher rates have taken their toll on equity prices:

CCD NAV (Fund)

Let us have a step back and better understand what a convertible security is:

A convertible bond gives the holder the option to exchange (convert) the bond for a specified number of shares in the underlying company. The number of shares for which the bond can be exchanged is given by the conversion ratio, which is usually stated at bond issuance. While the investor holds the bond and does not exercise their option to convert, they will receive periodic payments at the stated coupon level. In essence, a convertible bond can be thought of as a regular bond with an embedded equity call option. Convertible bonds can also be issued with other embedded features such as time varying issuer calls and investor puts. As the underlying share price increases, the bond will behave more like an option.

Source: FINCAD

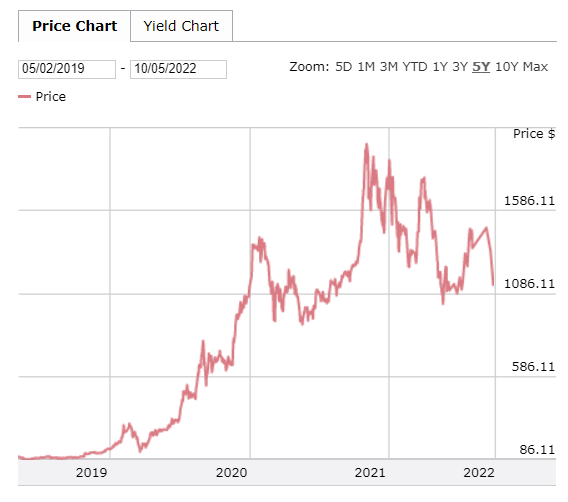

As tech stocks soared in 2020 / 2021 and the market was experiencing historic gamma squeezes, convertible securities benefited from the meteoric rise in prices through their embedded equity call option leverage. Just think about a simple example such as Tesla – the company originally sold convertible securities because they contained a cheaper outright cost of funds (i.e. fewer actual dollars out the door). As the Tesla share price went up, the convertible bonds gained on the grounds that the fixed income instrument was actually going to convert into equity, which had rallied past the conversion price. The convertibles started to behave like pure equity after a certain pricing point:

Tesla Bond Price (Fidelity)

Step back into 2022 and the exact opposite is happening – equity prices are collapsing, especially in the tech space. The fund is balanced, with overweight positions in Tech and Healthcare, which have cushioned the overall fall. CCD is down only -25% on a total return basis this year, which is a fairly good performance considering the fall in prices in some tech stocks.

We expect the rest of 2022 to be challenging for CCD as we embark on another leg down in the current bear market. The fund’s collateral is more equity than bond like given its conversion factors, and has benefited from the increase in overall market volatility (higher volatility makes an option command a higher premium). We feel next year will be a much brighter one for CCD, but we do not expect to see the outsized returns of the 2020/2021 period which were driven by zero rates and gamma squeezes. Expect a regime change here with annualized total returns for the fund to fall back to the 10% range.

Tesla 2% 15-May-2024 Bond Study Case

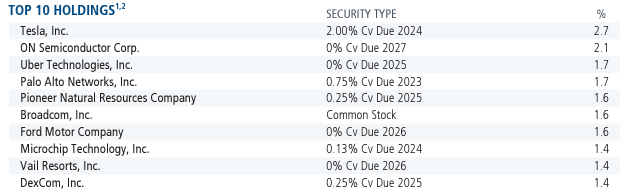

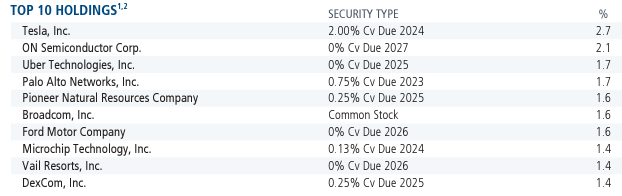

One of the top holdings in the fund is the 2% Tesla bond that matures in May 2024:

Top Holdings (Fund)

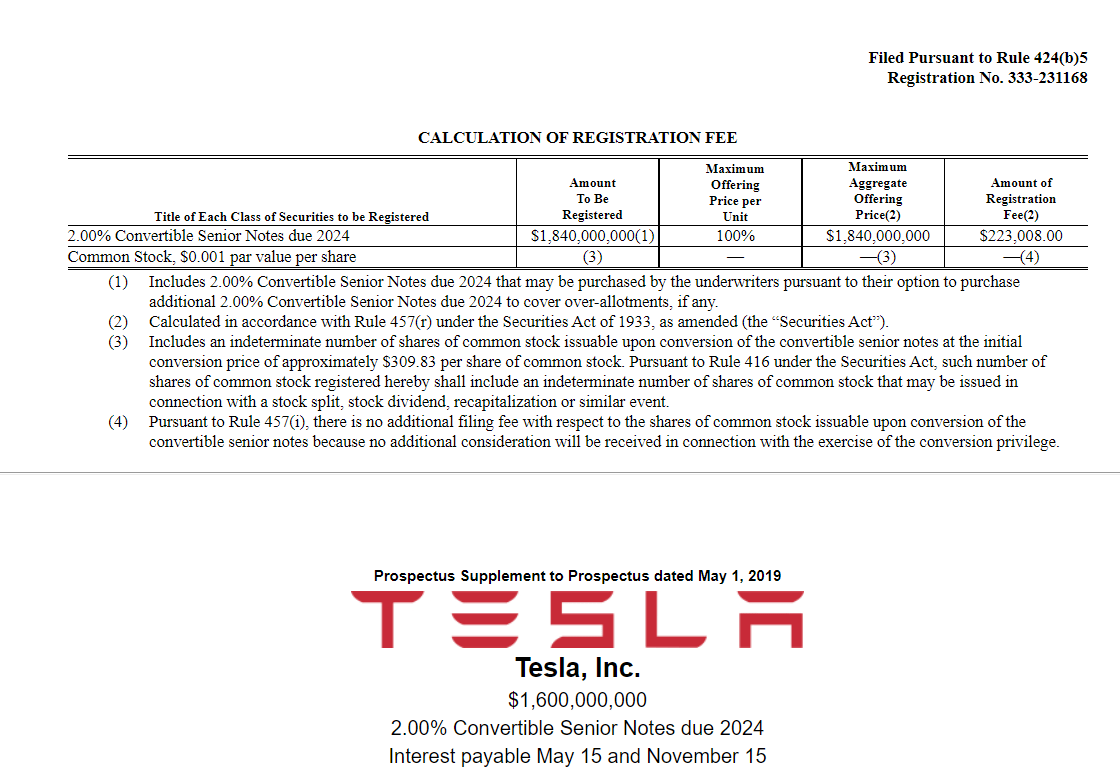

Let us have a closer look at this bond since it gives us a better flavor for how the collateral in this CEF performs. Firstly, the bond was issued back in 2019:

Tesla Bond Prospectus (the SEC )

The key aspect to remember about this bond is the fact that it pays a 2% rate and it gives a holder the option to convert into equity:

The conversion rate with respect to the notes will initially be 3.2276 shares of common stock per $1,000 principal amount of notes (equivalent to an initial conversion price of approximately $309.83 per share of common stock). The conversion rate will be subject to adjustment in some events but will not be adjusted for any accrued and unpaid interest. In addition, following certain corporate events that occur prior to the maturity date, we will increase the conversion rate for a holder who elects to convert its notes in connection with such a corporate event in certain circumstances.

A savvy investor needs to keep in mind that this year we had a 3 for 1 reverse split for the Tesla shares back in August, hence the above conversion price is now 309.83 divided by 3, or roughly $103/share. So the security is significantly “in-the-money” as its price graph also shows:

Tesla Bond Price (Fidelity)

The bond price started off in 2019 at around par, and then as the Tesla stock became more valuable it increased in price substantially. The fixed component is virtually ignored by the current pricing, due to the value of the option embedded in the bond. This bond is more equity-like now rather than a fixed income instrument.

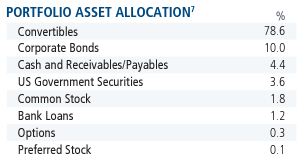

Holdings

The fund overwhelmingly holds convertible securities:

Assets (Fund)

We can see from the above split that over 78% of the fund is convertibles, followed by a 10% bond bucket and cash and cash like instruments.

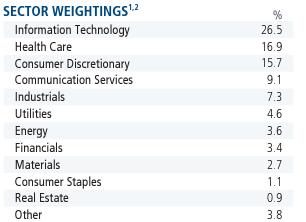

On the converts side Information Technology is the largest allocation:

Sectors (Fund)

We have Tech as the highest allocation, followed by Health Care (a defensive sector). Consumer Discretionary is third at 15.7%.

What is interesting to me when looking at the top holdings is the fact that most names are equity like:

Top Holdings (Fund)

What do I mean by that? They have a 0% coupon. This means the bond does not pay any cash, and the return to be expected is from the performance of the equity price versus the conversion level.

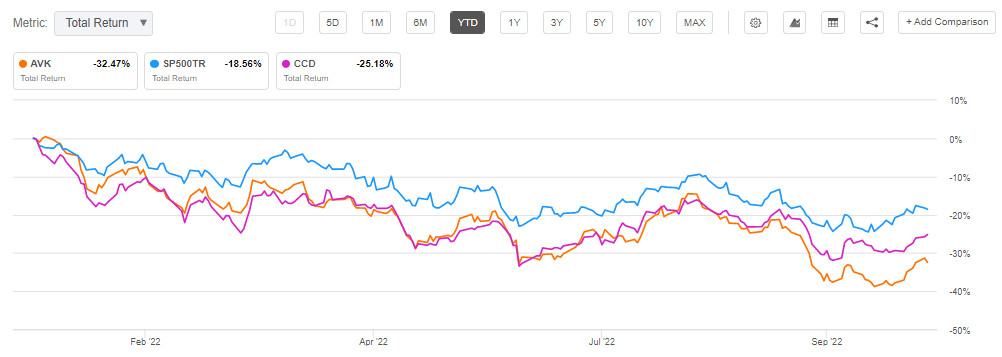

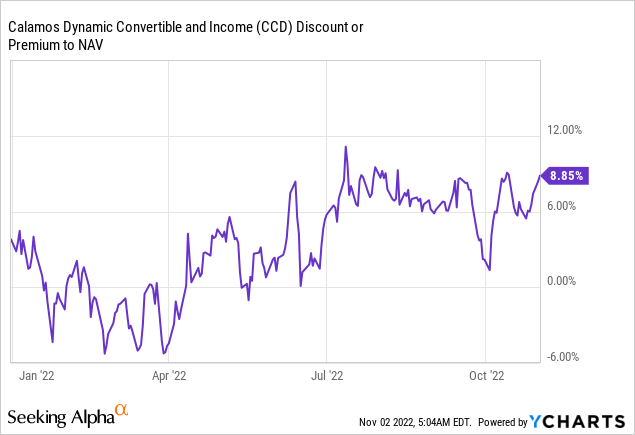

Performance

The fund is down over -25% on a year-to-date basis:

YTD Total Return (Seeking Alpha)

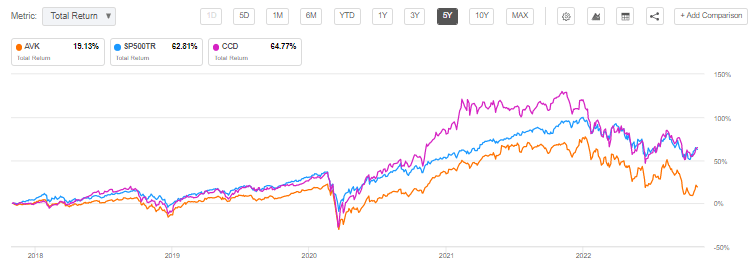

The fund is still substantially up on a 5-year basis and outperforming the S&P 500:

5Y Total Return (Seeking Alpha)

CCD has posted a fairly impressive performance here, with an outperformance during the zero rates environment, but a pull to a normalized performance in the past year.

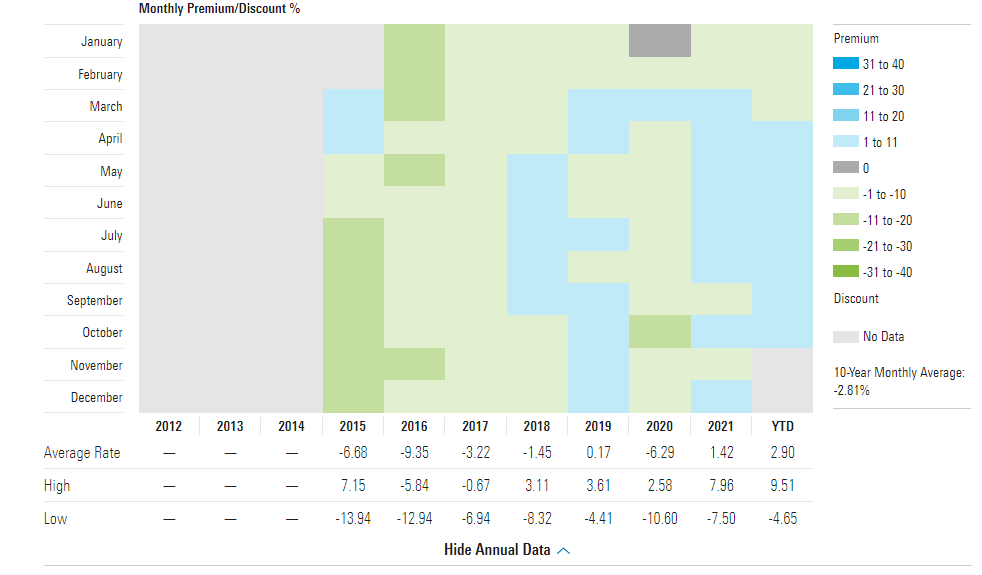

Premium / Discount to NAV

The fund has traded at flat levels versus net asset value in the past decade:

Premium/Discount to NAV (Morningstar)

We can see the CEF has a narrow, well contained range for its discount and premiums to NAV. Interestingly, on a year-to-date basis the CEF has seen premiums:

We think this is due to the optionality embedded in the fund’s assets – even though equity prices have come down, volatility is higher, which makes the option levels in the converts valuable.

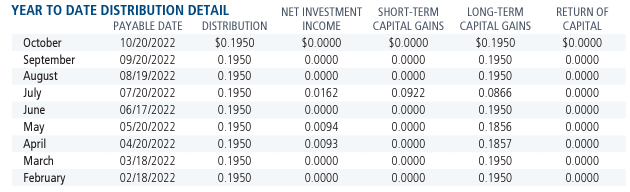

Distributions

The fund is not using any ROC in 2022, despite the underperformance in the underlying collateral:

Distributions (Fund)

We surmise this is the case given the fund’s distribution policy, and the fact that it did not disburse all crystalized gains from the past years. This is the flag of a great management team that does not get greedy when times are good. There is a lot to be admired here. There are numerous equity CEFs that in 2022 have most of their dividends coming from ROC. Not for CCD.

Conclusion

CCD is a closed end fund focused on convertible securities. The fund holds more than 78% in convertible bonds, 10% in high yield debt and the rest in cash and government bonds. The CEF posted extraordinary annual returns in the 2019-2021 period, with average annualized total returns exceeding 30%. The fund has a great management team that has been able to cover the fund’s distributions in 2022 via the crystallization of capital gains from past years and a steady dividend policy. Most of the securities in the portfolio derive their values from the equity option component, with many of the bonds having 0% coupons. Down -25% year to date, the fund has not been able to escape the equity carnage driven by higher rates. We expect the rest of this year to be challenging for CCD, with the next leg down of this bear market coming in shortly. Next year we expect a positive performance for the fund, albeit a more “normalized” one as the tech stocks’ performance will be subdued when compared with the height of the market in 2020/2021.

Be the first to comment