Caesarstone Ltd. (NASDAQ:CSTE), manufacturer and marketer of engineered quartz, is delivering promising performance outside the United States. Even considering the recent decrease in revenue guidance for 2022 and other risks, CSTE looks quite undervalued. Further development of the company’s digital platforms in different languages, successful integration of recent acquisition targets, and successful R&D will likely bring more free cash flow (“FCF”) than expected. Future free cash flow would justify, in my view, higher stock price marks than what the market currently indicates.

Caesarstone

Caesarstone Ltd develops high-end engineered surfaces for both interior and exterior environments in residential and commercial buildings.

In addition to its work on stone, the company offers pieces of other material such as porcelain or graphite. In my view, one of the biggest bets from Caesarstone is the commercialization of quartz, which it has been introducing into the market since 1999. Specifically, the company has included the work of quartz, which it promotes as a material of high quality and durability that still maintains affordable costs for its acquisition and trade in the market.

By the year 2020, the installation of quartz in its key markets exceeds two figures, 20% in the U.S. market and a whopping 80% in the Israel market. Its clients include direct buyers as well as indirect buyers through distribution subsidiaries, with currently active operations in more than 50 countries.

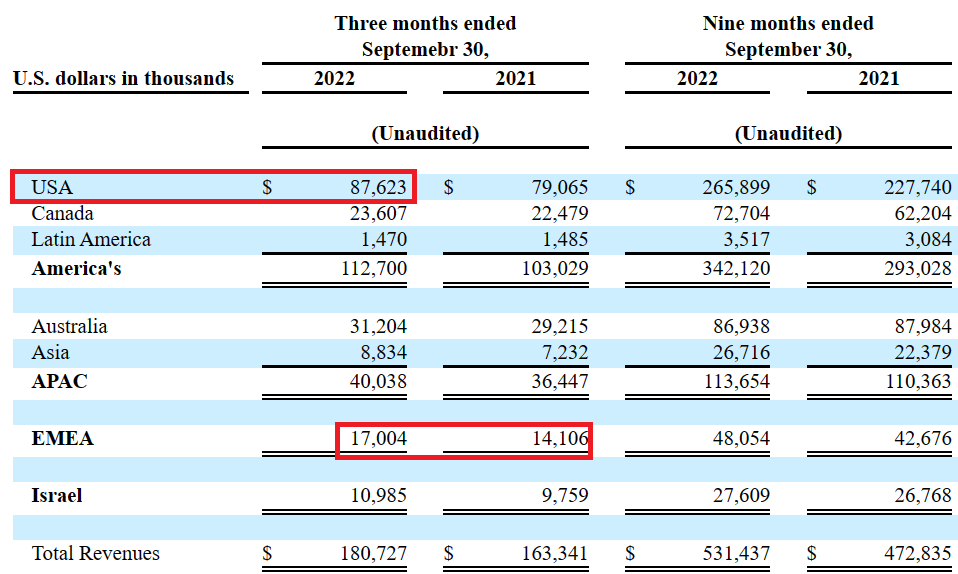

Caesarstone’s strategy outside the United States appears to be working pretty well. For instance, the company’s marketing strategies in Europe in 2022 resulted in a considerable increase in revenue. Considering the improvement in the EMEA region in 2022, I am quite optimistic about the future of Caesarstone’s global business model.

Source: Quarterly Report

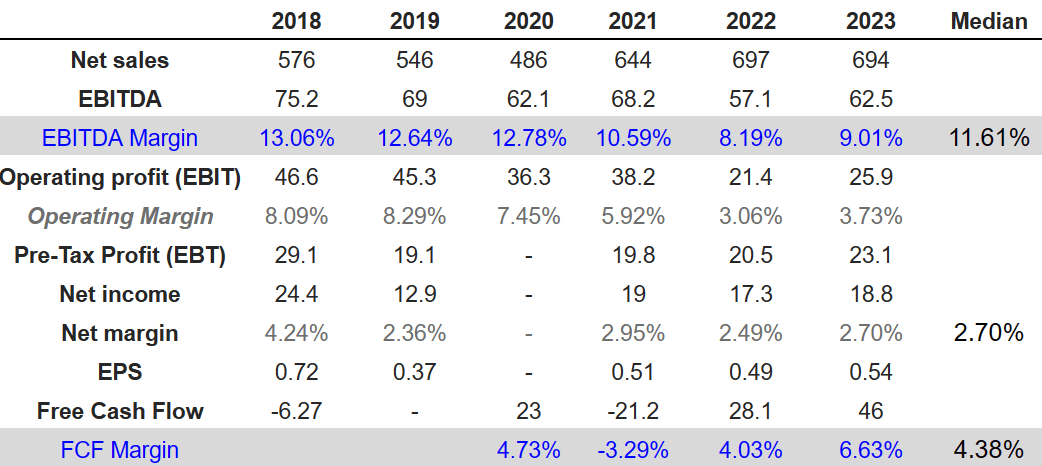

Analysts Are Expecting Growing Free Cash Flow Margin In 2022 And 2023

Analysts are expecting 2023 sales close to $694 million and an EBITDA of $62.5 million together with an EBITDA margin of 9.01%. 2023 operating profit will likely be close to $25.9 million with operating margin of 3.73%. 2023 pre tax profit would be close to $23.1 million, with net income of $18.8 million and a net margin of 2.70%. Finally, EPS would stand at close to $0.54, with 2023 FCF of $46 million and free cash flow margin of 6.63%. In my financial models, I tried to use numbers that were not very far from previous figures of Caesarstone. Hence, I believe that readers may want to have a look at the company’s figures from 2018 to 2021.

Source: marketscreener.com

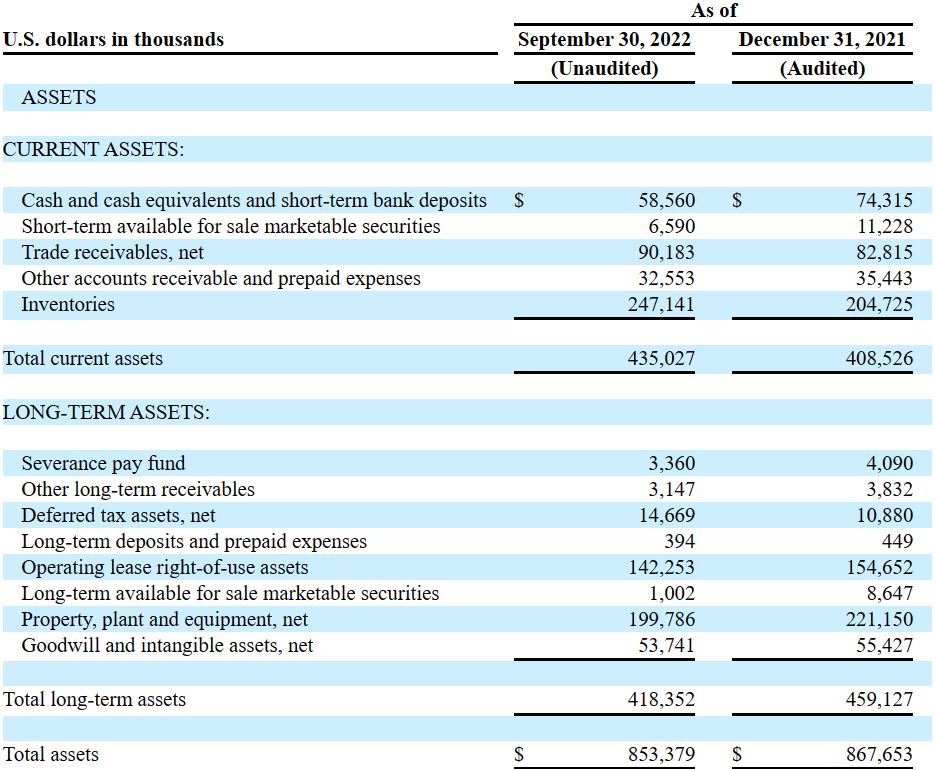

Solid Balance Sheet

The balance sheet as of September 30, 2022 includes cash of $58.560 million and trade receivables of $90.183 million in addition to other accounts around $32.553 million. Total current assets stand at $435.027 million, close to 2x the total amount of current liabilities. I don’t see any liquidity issue coming any time soon.

Deferred tax assets stand at $14.669 million with operating lease rights of use assets worth $142.253 million, property of $199.786 million, and goodwill of $53.741 million. Finally, total long term assets stand at $418.352 million with total assets worth $853.379 million. I believe that the balance sheet stands in a good position.

Source: Quarterly Report

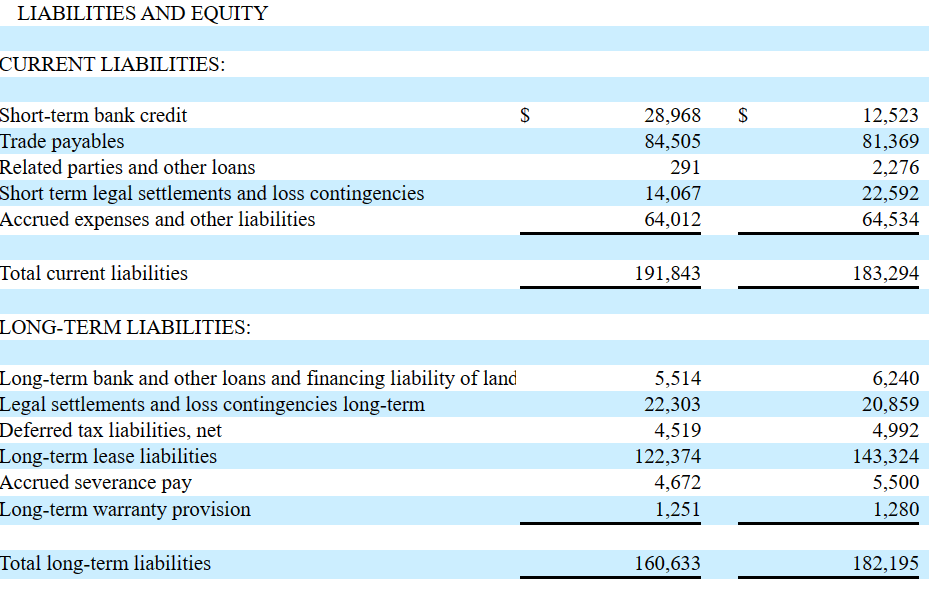

Regarding the liabilities, Caesarstone Ltd. reported short-term bank credit worth $28.968 million, trade payables of $84.505 million, accrued expenses worth $64 million, and total current liabilities of $191.843 million. Besides, the legal settlements were $22.303 million, with a long-term lease liability of $122.374 million and total long-term liabilities of $160.633 million.

Source: Quarterly Report

Case 1: Under Normal Conditions, I Would Expect A Fair Price Of $11 Per Share

Most of Caesarstone’s marketing strategy is given through its website and social networks, where it shows the designs and benefits of working with this type of stone. In addition, as clarified in its reports, it develops regional marketing strategies to have better results in each of the local markets. I am quite optimistic about the work developed by Caesarstone’s website designers. In my view, the gallery on the website offers a significant amount of information for clients. Under this scenario, I assumed that the website would enhance future revenue growth.

Our websites enable our business partners, customers and end-consumers to view currently available designs, photo galleries of installations of our products in a wide range of settings, instructions with respect to the correct usage of our products and offer an innovative cutting-edge experience with rich content and interactive tools to empower and guide consumers at any stage of their renovation journey. Source: 20-F

Source: Company’s Website

I also believe that Caesarstone’s acquisitions from third-party engineered stone and ceramic OEMs from China, Spain, and Italy could be very beneficial. Under this case, I assumed that Caesarstone’s new business partners will likely help the company grow its production capacity and bring economies of scale. As a result, we would likely see FCF margin growth.

In order to optimize our production capabilities, meet market demands and adjust to changes in market dynamics, we accelerated our strategy to acquire certain basic product models from third-party engineered stone and ceramic OEMs, primarily from China, Spain and Italy. We anticipate further increasing this activity. Source: 20-F

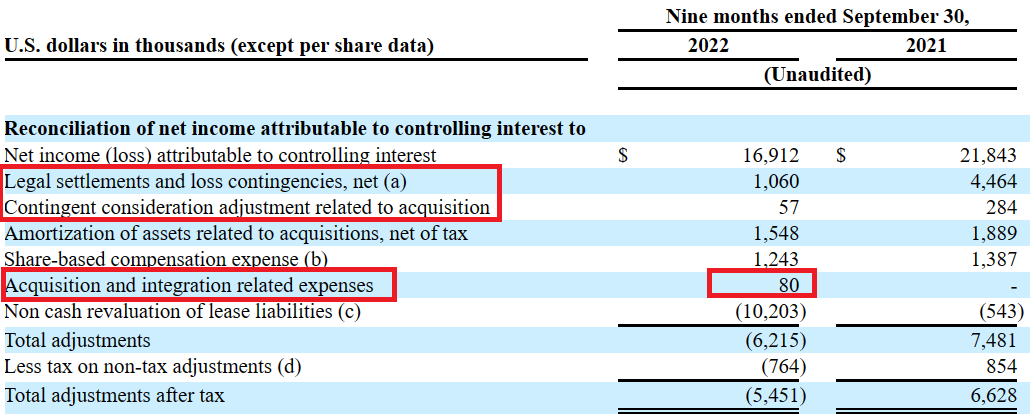

Besides, I am expecting free cash flow margin increases as a result of the company’s recent acquisitions and the expansion of Caesarstone’s digital platforms. According to the last quarterly report, Caesarstone Ltd. is investing some money in the integration of targets, and some contingent considerations may have affected the company’s results in 2022. Under this scenario, I assumed that the acquisitions would be successful, and would serve as catalyst for FCF generation.

Source: Quarterly Report

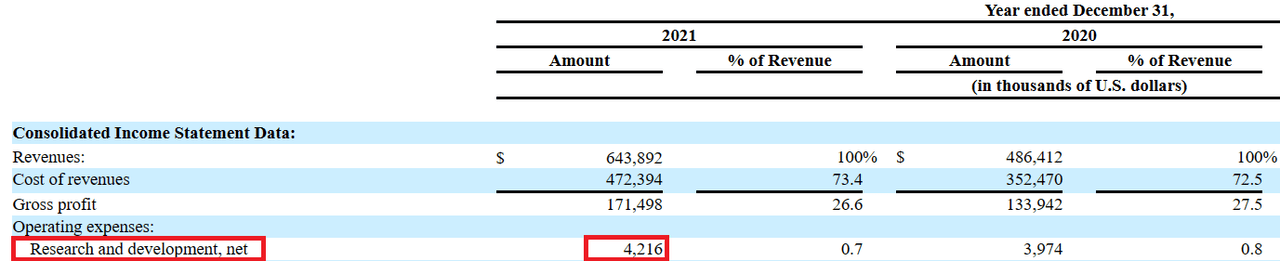

Finally, I would also expect improvements in quality and new product generation since Caesarstone yearly invests a significant amount of dollars in research and development. In 2021, R&D expenses increased to up to $4 million, a bit more than that in 2020.

The strategic mission of our R&D team is to develop and maintain innovative and leading technologies and top-quality designs, develop new and innovative products according to our marketing department’s roadmap. Source: 20-F

Source: 20-F

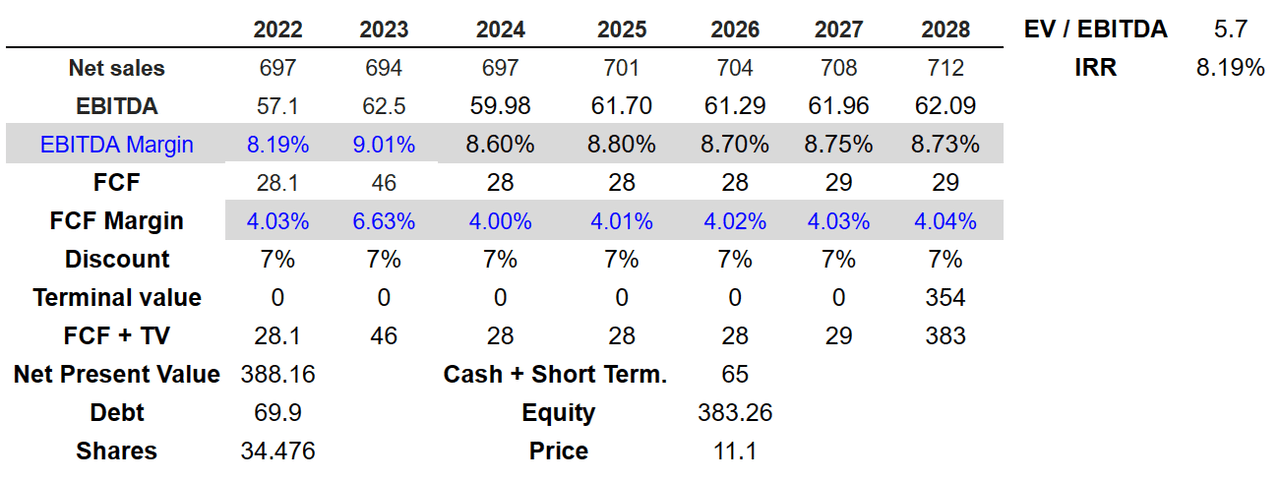

My forecast for 2028 included net sales of $712 million, EBITDA of $62.09 million, and an EBITDA margin of 8.73%. In addition, I expect 2028 FCF close to $29 million with a FCF margin of 4.04%.

With a discount of 7% and an EV/EBITDA multiple of 5.7x, the net present value of future FCF would be close to $383 million. With debt of $69.9 million and cash and short term investments of $65 million, equity would stand at $383.26 million, and the fair price would be $11.1 per share. Finally, I believe that the internal rate of return would stand at 8.1%.

Source: Bersit’s DCF Model

Case 2: Lower Guidance, Inflation, And Dependency On the United States May Bring The Stock Price Down To $5 Per Share

Under bearish conditions, I assumed that Caesarstone may continue to lower its guidance for the year 2022. I also assumed that 2023 and the future years may not be much better than 2022. In line with these thoughts, let’s note that the company lowered its target revenue, for 2022, to $690 million. Besides, higher interest rates and inflation could affect the company’s volume growth in the near future.

The Company revises its expectation for 2022 revenue to be in the range of $690 million to $700 million, compared to a prior range of $710 million to $725 million. Additionally, the Company has moderated its volume expectations for the year due to softening economic conditions as higher interest rates and inflation have continued to pressure renovation and new construction activity, particularly in the U.S. Source: Quarterly Report

In relation to the risks that Caesarstone experiences, we can first name the exhaustion of the resources with which it works. This means that you constantly have to be weaving strategies in relation to the use, sale, commercialization, and distribution of these resources, since they are limited, and the profits must be managed intelligently. More in particular, if free cash flow margin decreases, less investors may give financing to Caesarstone. As a result, cash in hand may diminish, which may bring Caesarstone’s fair price down.

Currently, as we pointed out, almost half of its business concentration is in the USA, which on the one hand is beneficial because it demonstrates the efficiency in its migration from Israel to international markets, but at the same time it indicates a weakness in its diversification, which can jeopardize the plans of the company in the event of a recession in the North American economies.

Besides, Caesarstone depends directly on the regulations and restrictions on the exploitation of land. Considering the radical change of mentality that global markets are having in relation to environmental care and the fulfillment of goals in this regard, such as the reduction of the carbon footprint or the ecological management of waste from production chains, the company is strongly exposed.

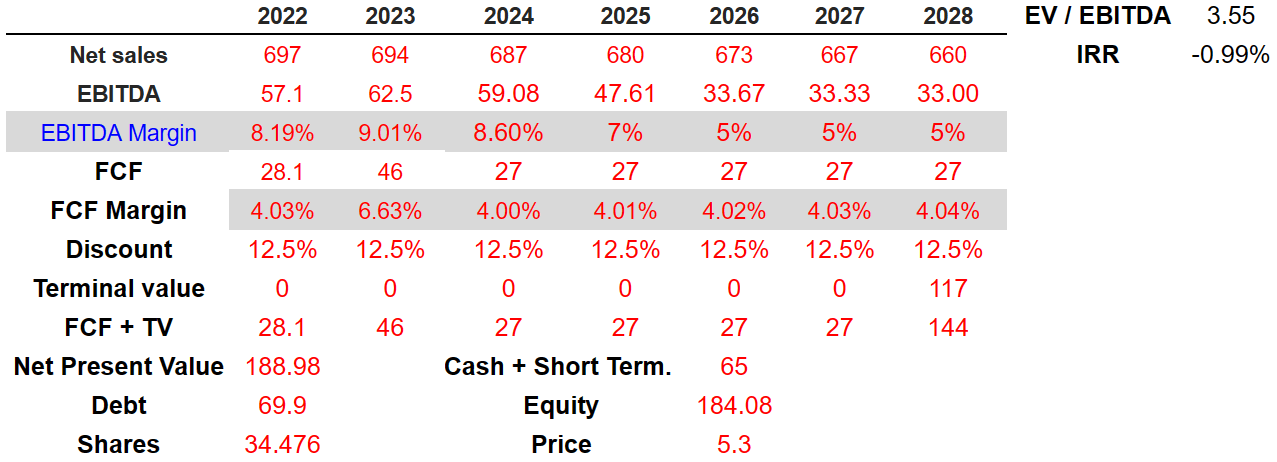

The results for the year 2028 that I am expecting include net sales of $660 million, EBITDA of $33 million, and an EBITDA margin of 5%. 2028 FCF would be close to $27 million with FCF margin of 4.04%.

Source: Bersit’s DCF Model

If we also assume a discount of 12.5% and an EV/EBITDA multiple of 3.55x, the implied enterprise value would be $144 million. Besides, if we subtract the debt, and add cash, the equity valuation would be close to $184.08 million. Finally, the fair price would be close to $5 per share with an IRR of -0.99%.

My Takeaway

Further successful commercialization of quartz and other materials outside the United States and successful integration of recent acquisitions could bring free cash flow generation. I also believe that more development of the company’s digital platforms in different languages and for more regions could bring revenue growth. In my view, risks from new regulations and restrictions on the exploitation of land, inflation, and dependency on the United States market may diminish FCF generation. With that, I believe that Caesarstone Ltd. appears significantly undervalued at its current price mark.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment