belterz

Introduction

Cadence Bank (NYSE:CADE) is one of the largest banks in Texas and the Southeast. Based on the total amount of assets, the bank ranks sixth, thanks to the completion of a series of acquisitions. This expands the bank’s footprint and asset base, but it also means it makes it difficult to compare the financial performance with previous years as the bank closed three mergers in Q2 and Q4 of last year, adding in excess of $20B in assets to the balance sheet.

A Decent Q1 Result, Despite Merger-Related Expenses

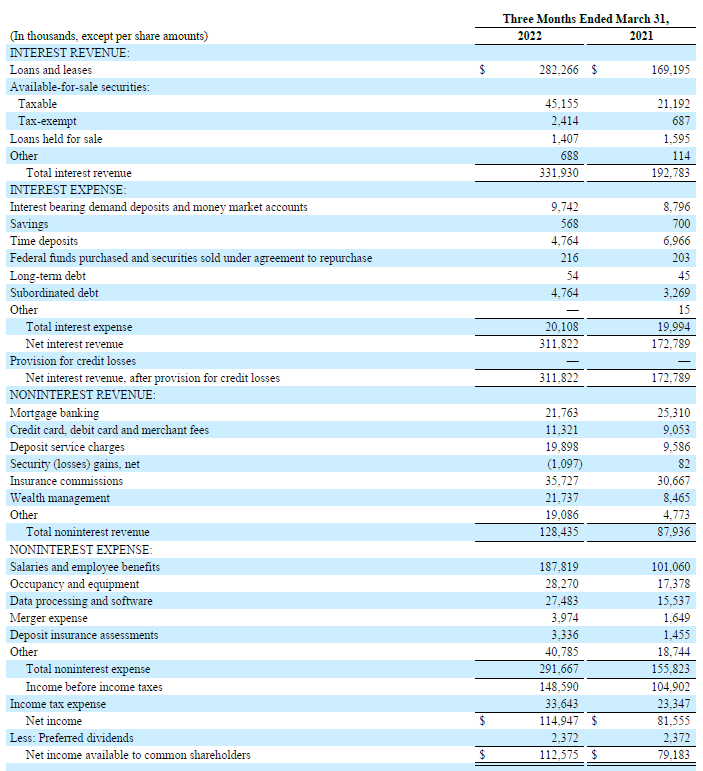

Thanks to the expanded asset base, the interest income increased to almost $332M, while the interest expenses barely increased (by 0.5%) to $20.8M. This means that even though the asset base almost doubled, the bank’s interest expenses barely moved as the cost of funding continued to decrease.

As there were no provisions for credit losses, the net interest income in the first quarter of the year was approximately $312M.

Cadence Bank Investor Relations

Thanks to the mergers, the non-interest income increased from $88M to $128.4M, but the non-interest expenses increased at a much faster pace and reached almost $292M. This includes in excess of $10M in merger-related expenses, while the first quarter is now more expense-intensive than before as that’s the quarter with the seasonally higher compensation costs including payroll taxes and the 401(k) matches.

The pre-tax income was just under $149M, resulting in a net income of $115M and about $112.6M after taking the preferred dividends into account. This means the EPS in the first quarter was just about $0.60, which is about 20% below the $0.77 in Q1 of last year.

Keep in mind, however, that once we exclude the merger-related expenses, the net income would have been closer to $0.65/share while the anticipated merger-related benefits are only starting to be unlocked, so we should cut the bank some slack as it moves to integrate the acquired companies. Also keep in mind, the EPS is based on an average share count of approximately 187 million shares. As Cadence has been buying back stock at a relatively fast pace, the current share count is much lower, at just around 183.5M shares. The reduced share count alone is already adding in excess of $0.01/share per quarter to the earnings tally.

The Book Value Declined Due To The Increasing Interest Rates

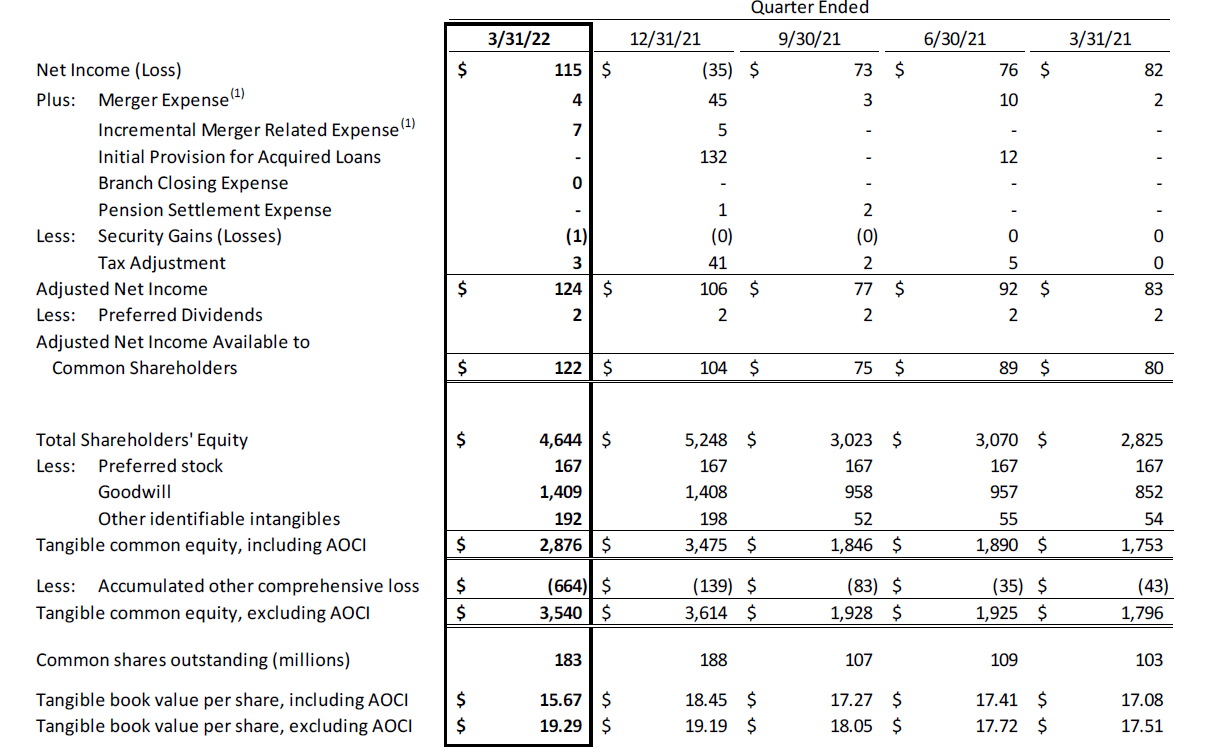

It’s not easy to compare book values, considering the company has seen massive changes in the past twelve months. However, there’s one important metric to talk about here, and that’s the tangible book value per share. This fell from $18.45 as of the end of December to just $15.67 as of the end of March, and this drop can be explained by the available for sales securities in the portfolio. According to the comprehensive income statement, there was a loss in excess of half a billion dollars on that portfolio and if we would look at the non-GAAP book value reconciliation, the tangible book value per share, excluding the AOCI, would have come in at $19.29/share.

Cadence Bank Investor Relations

That’s still only $0.10 higher than at the end of December, despite generating $0.60 in earnings while only paying out $0.22 as a quarterly dividend. One would have expected to see the TBV increase by $0.38 but as the bank has been buying back stock at a premium to the tangible book value, the TBV per remaining share is negatively impacted. Cadence repurchased 5.082 million shares for a total of $156.8M, indicating it paid on average $30.85/share, or just over 1.5 times the tangible book value at that time.

The total share repurchase authorization for 2020 was 10 million shares, which means that as of the end of Q1, the remaining authorization was good for 4.91M additional shares and at the current share price, this buyback could be completed at a much lower premium to the TBV which means the impact on the TBV/share will remain limited.

The main question is how fast Cadence will be willing to buy back stock as the fair value adjustment on the securities for sale reduced the CET1 ratio from 11.1% to 10.6% and while that’s still a decent position to be in, the experienced management may have hit the brake pedal a little bit.

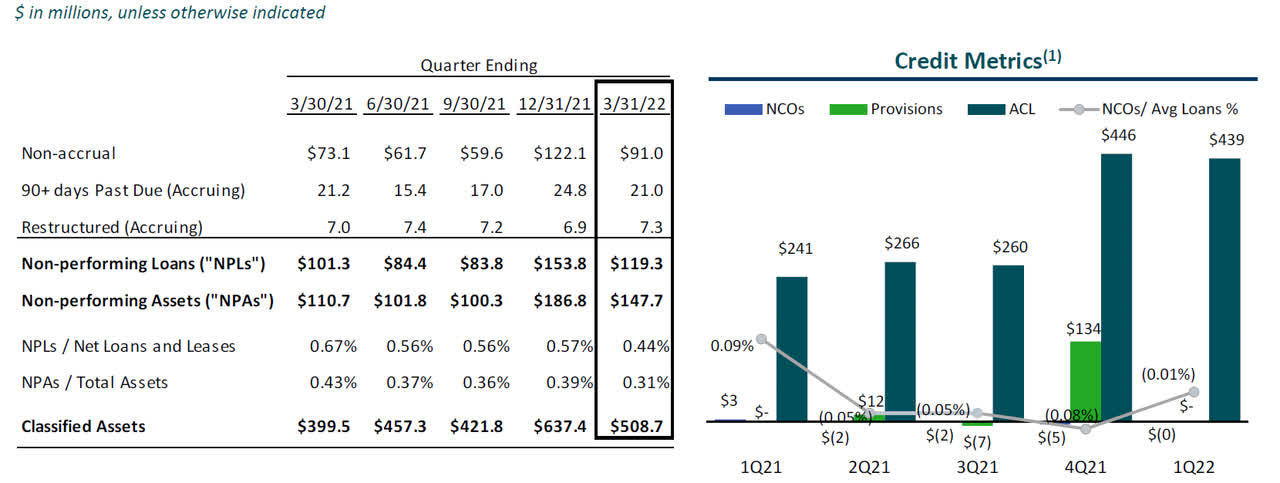

I expect the reported net income to remain strong as Cadence’s $27B+ loan book is very strong with just under $120M in loans classified as non-performing. That’s approximately 0.44% of the loans. Meanwhile, the total allowance for credit losses on that loan portfolio is approximately $438M, which is almost four times higher than the current amount of non-performing loans, so it’s not exactly surprising to see the bank not recording any additional loan loss provisions on the income statement.

Cadence Bank Investor Relations

Investment Thesis

Cadence Bank also has a non-cumulative preferred share outstanding trading as (NYSE:CADE.PA). This preferred share has a 5.50% preferred dividend and at the current price of $23.50, the yield has increased to 5.85%. Considering the preferred dividends require less than 2% of the net income and the $172M of preferred stock outstanding (6.9M shares) ranks senior to the $3B in tangible common equity, the preferred share could be a good option for an income-focused investor.

I currently have no position in Cadence Bank, but I think both the preferred share and the common shares have their merits. I likely won’t do anything until I see the Q2 results of the bank.

Be the first to comment