Kiran Ridley/Getty Images News

Introduction

2022 is over, and what a year it has been! The stock market entered a bear market, the Federal Reserve started one of the most hawkish hiking cycles in modern history, and a lot of fast-growing tech stocks got hammered. The good news is that there were a lot of places that provided shelter for conservative dividend (growth) investors like myself. One of these places is Northrop Grumman (NYSE:NOC), one of America’s leading defense contractors. While the stock has a subdued dividend yield, I believe that the stock is a must-have in every dividend growth portfolio. The company is well-positioned to benefit from emerging defense requirements like hypersonics, space, and missile defense. Furthermore, the company is now benefiting from accelerating war-related defense budget hikes, fading supply chain problems, and its ability to protect investors against high inflation.

This article will discuss all of this and assess the company’s risk/reward after the NOC ticker added more than 40% in capital gains last year.

So, let’s get to it!

NOC Stands For Stability & Low-Volatility Outperformance

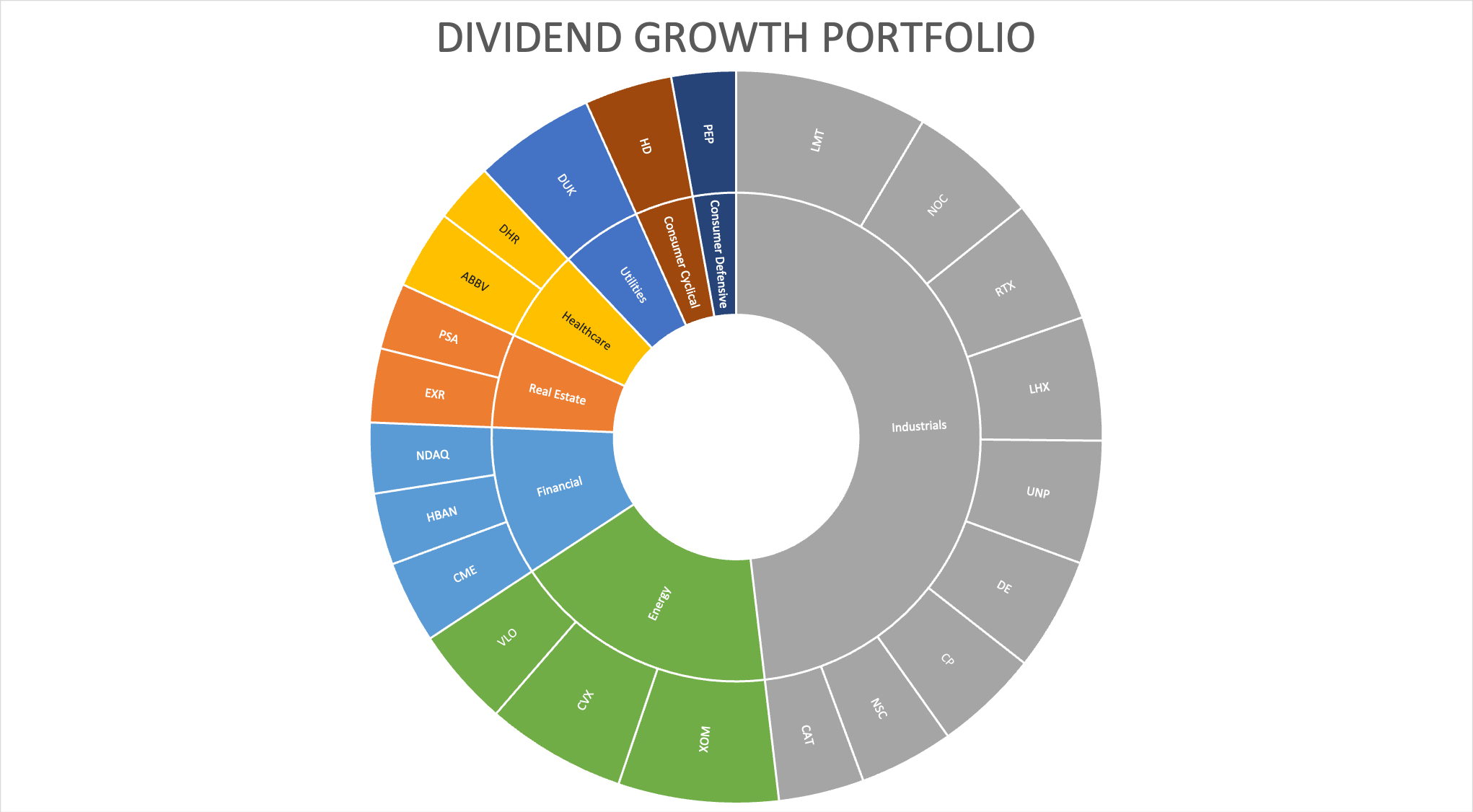

The chart below shows the past performance of my dividend growth portfolio. However, it is important to mention that it shows the past performance of the current portfolio composition. For example, if I added a new stock to my portfolio in 2022, the chart believes that I owned that stock when the measurement began in 2021. In other words, if anything, it is a way to track the past performance of my current portfolio composition. Also, my portfolio started in the first half of 2020, not in 2021.

Author

We see above that the portfolio added roughly 6% in the challenging year of 2022. The portfolio completely ignored the somewhat steep downtrend of the S&P 500, as I have limited exposure to high-growth industries.

I have 18% energy exposure and 25% defense exposure. Both did very well in 2022. After going from 24 to 22 individual stocks (purely based on reducing complexity), I now have four defense stocks that make up a big chunk of my industrial exposure.

Author

In this case, I decided to go overweight energy and defense well before they turned out to be no-brainers in 2022. After all, I wanted reliable income and high-quality dividend growth.

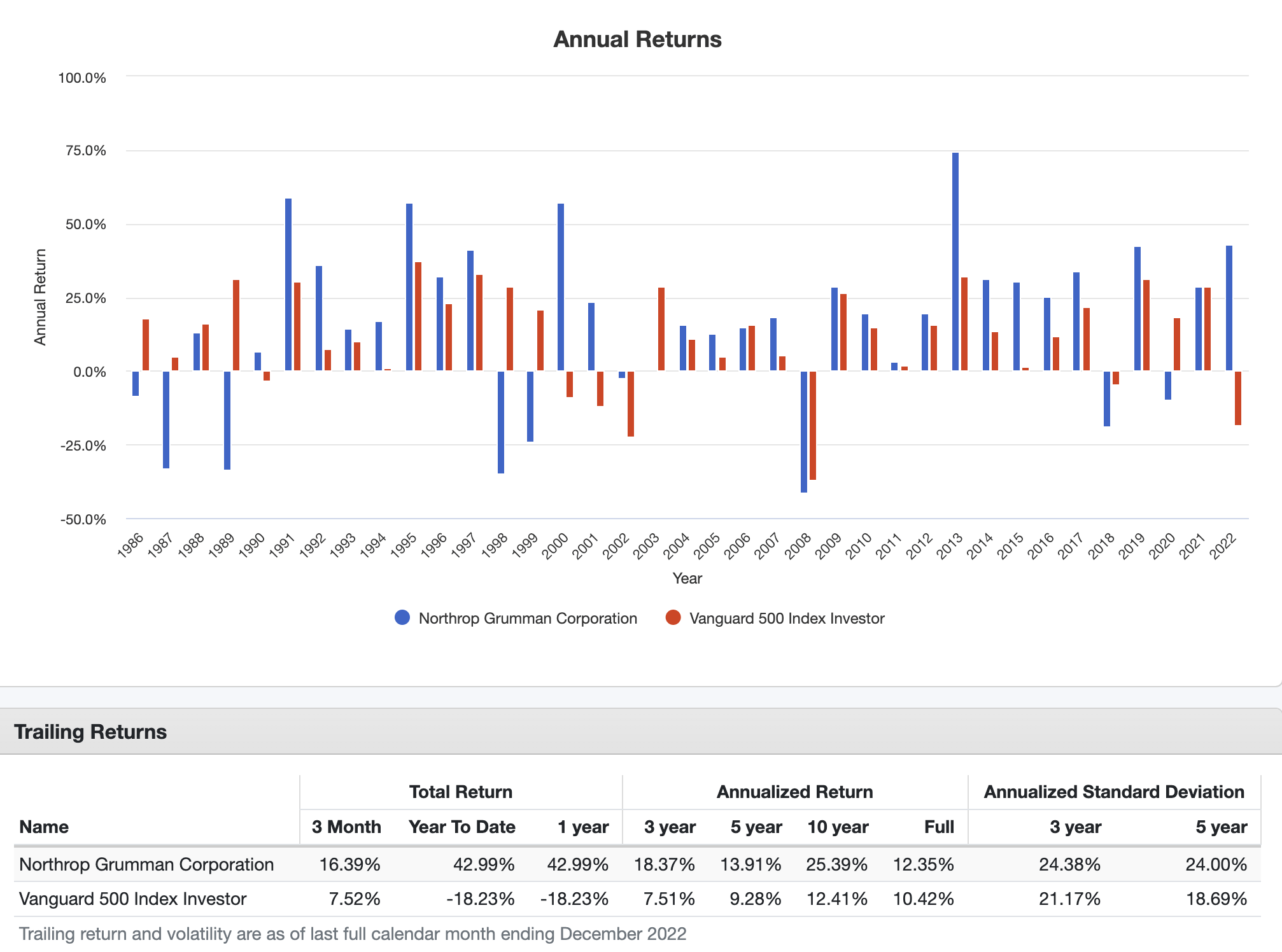

In the case of Northrop Grumman, the Virginia-based defense contractor has returned 12.4% per year since 1986. That is a stellar performance, beating the market by almost 200 basis points per year. As the table below shows, the stock has outperformed the market very consistently. Even more important, the standard deviation was subdued at less than 25.0%.

Portfolio Visualizer

Also, the bar chart above shows that NOC is doing well during uncertain economic times when people rush to buy bonds and safe dividend stocks.

To visualize this a bit better, we can take a look at the ratio between the NOC share price and the S&P 500 (excluding dividends). Over the past 22 years, the stock outperformed the market after the Dot-com crash, between 2013 and 2018, and again starting in 4Q21.

TradingView (NOC/SPX Ratio)

While NOC is a consistent performer, it does best when the market becomes less risk-tolerant. It tends to underperform in times when growth stocks do well. At that point, the market loses interest in conservative value stocks like Northrop Grumman. The best example is the pandemic of 2020 and the first quarter of 2021.

With that being said, let’s dive a bit further into the longer-term bull case.

Fast Growth Thanks To Great Products

In January of last year, I wrote an article dedicated to the two biggest reasons to buy Northrop Grumman. As Russia hadn’t set foot in Ukraine, reason one was not the war that would start in February. No, reason one is Northrop’s high-tech defense exposure.

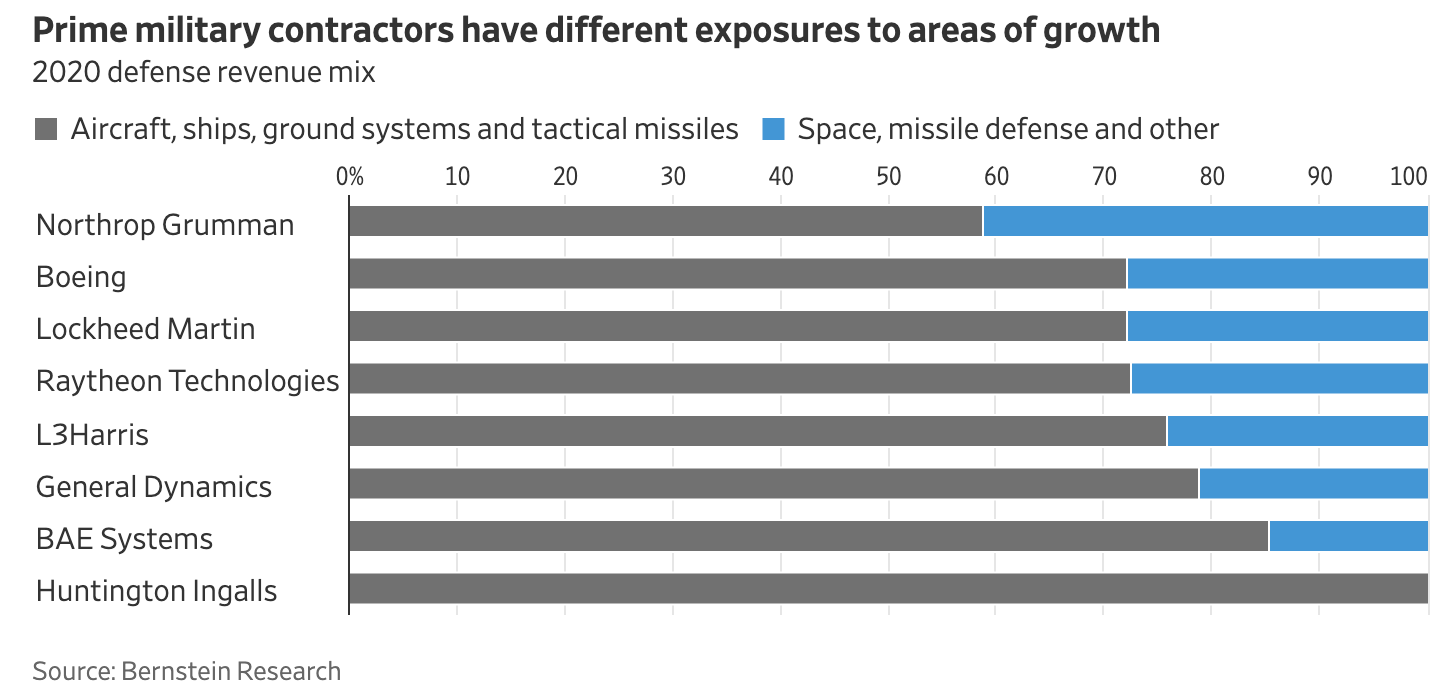

Back then, the Wall Street Journal wrote an article dedicated to changing defense needs. The timing could not have been better as the Ukraine war shows that Russia did not achieve its desired results, despite owning a LOT of hardware like tanks and other armored vehicles.

The overview below shows that Northrop Grumman has the highest non-traditional defense portfolio among major defense contractors. More than 40% of its 2020 revenues came from space, missile defense, and others.

Wall Street Journal

This was – and still is – a major reason why I own Northrop Grumman, in addition to other defense companies. While its yield is below average (more on that in this article), the company is more focused on growth.

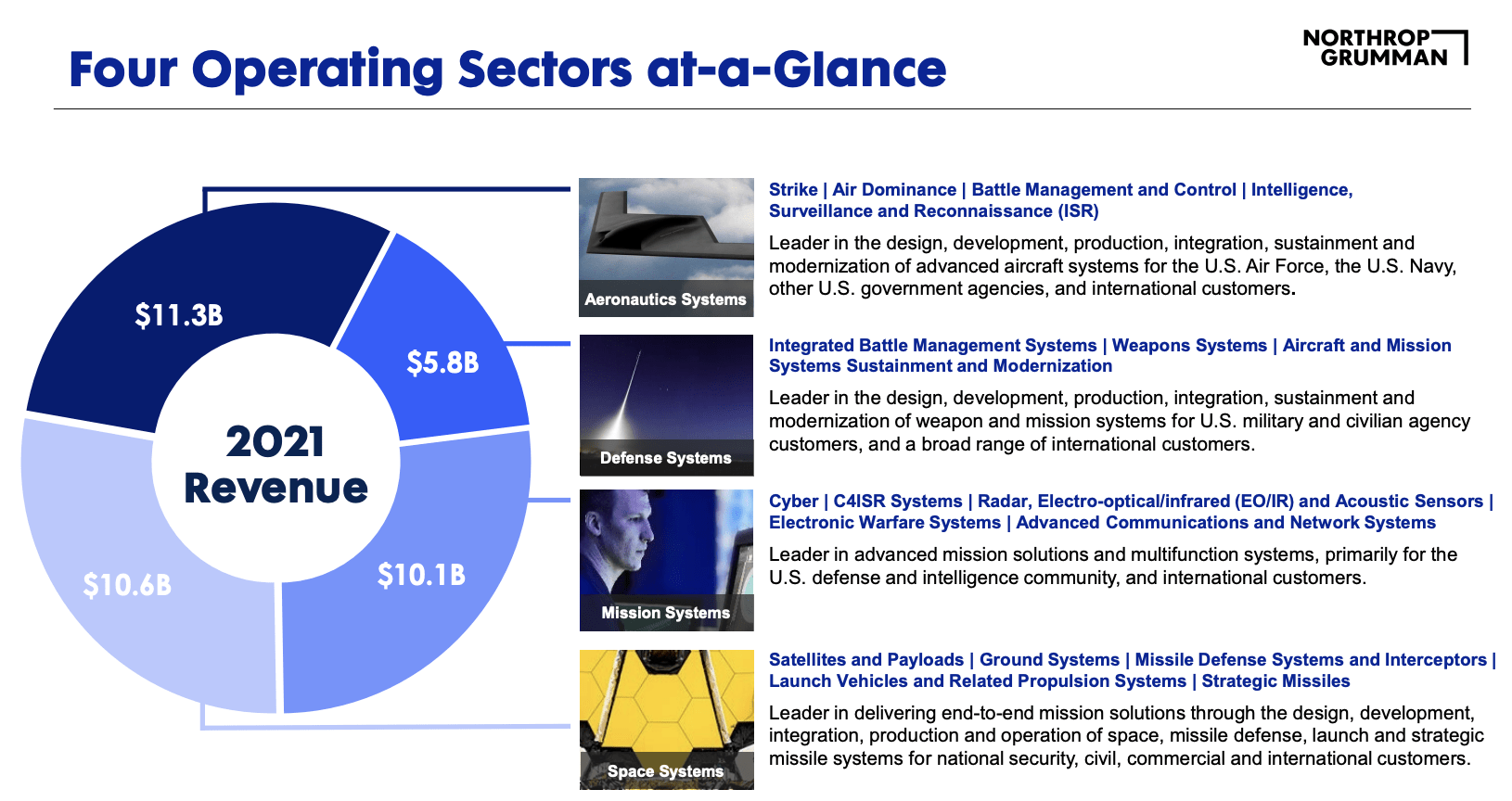

Unlike Lockheed Martin (LMT), the company is not dependent on a major program like the F-35. While the company produces the fuselages and other parts for that advanced jet, it has a highly diversified product portfolio. The fast-growing space segment alone accounts for more than 25% of FY2021 revenue.

Northrop Grumman

Moreover, half of all contracts are on a cost-type basis, meaning inflation is taken directly into account. While the other half is based on fixed prices, the company isn’t taking a huge risk as inflation is a major concern in government budgeting. After all, almost 100% of revenues come from government agencies.

Concerning the aforementioned capabilities, in its third quarter, Northrop commented on its capabilities in light of changing defense needs:

[…] it’s clear that Northrop Grumman’s portfolio continues to be extremely well aligned with the requirements outlined in the National Security Strategy. This is reflected in the administration’s fiscal year 2023 budget request which showed alignment with these priorities and strong support for many of our key programs.

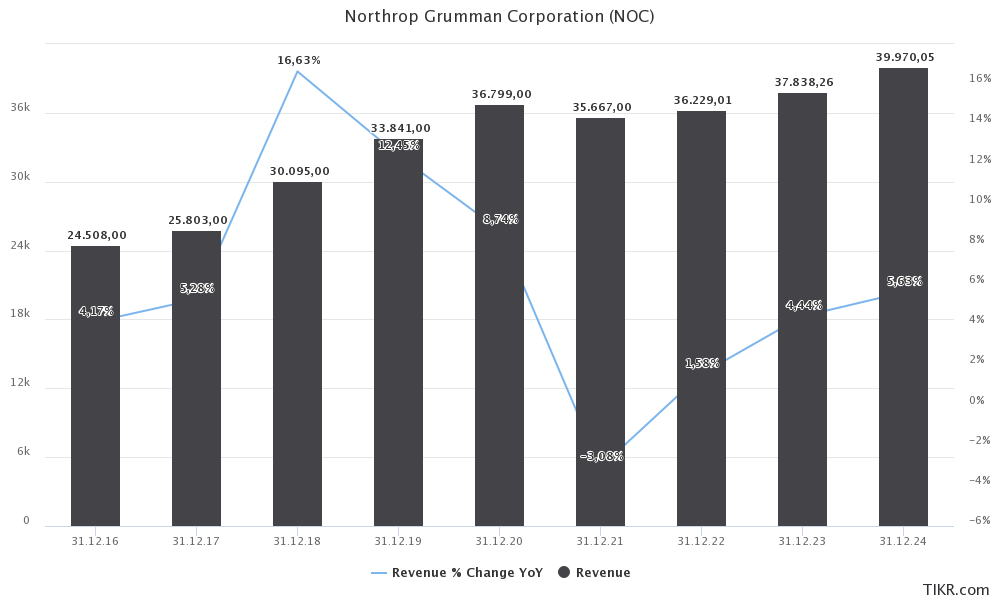

With that said, in 2023, Northrop expects to grow its revenues by 4% to 5%. Analysts are in the middle of that, expecting 4.4% revenue growth (as seen in the chart below).

TIKR.com

Based on these numbers, it’s both important and interesting to assess where growth is coming from. First of all, Northrop Grumman is operating in a highly favorable macro environment. As everyone has noticed by now, global spending on defense is rising. NATO is slowly turning its 2% spending target into a floor instead of a goal, the United States is ramping up defense spending and support for Ukraine, and APAC nations are accelerating spending as China continues to threaten the peace in that area.

Moreover, in December, President Biden signed the National Defense Authorization Act into law, approving $858 billion, including $816.7 billion for the Department of Defense. It’s $45 billion more than Mr. Biden initially asked for and a great step in the right direction for defense contractors.

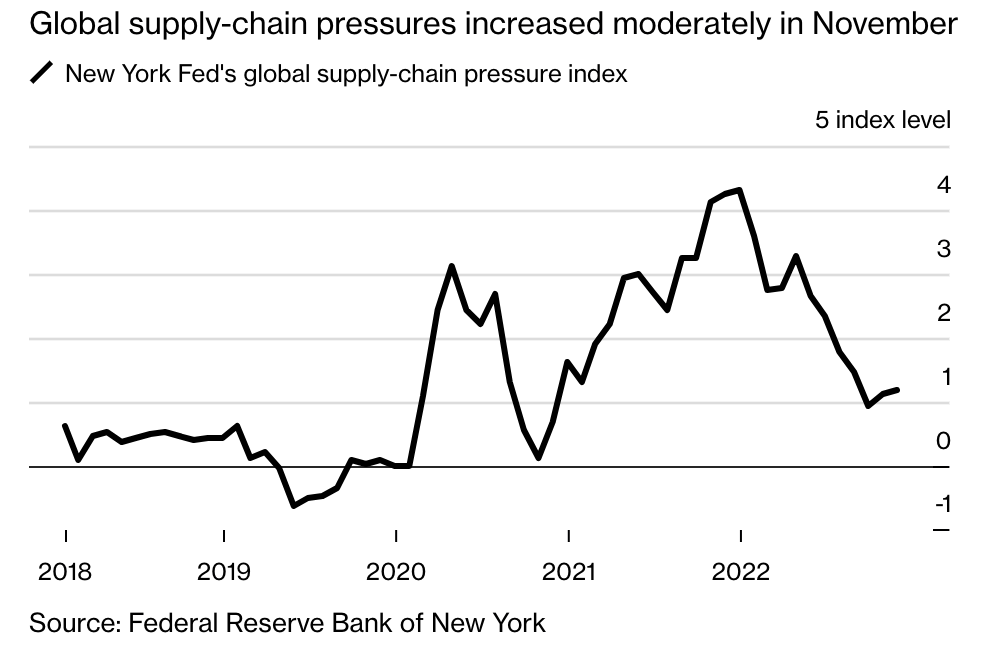

Moreover, demand tailwinds are now accompanied by easing supply chain problems. Since 2020, defense companies had tremendous problems turning orders into finished products. Companies like Northrop are highly dependent on skilled labor, high-tech components, and several other input products that saw significant shortages.

While these problems will last in 2023 as well, it’s getting less severe. I even believe that a recession this year could be bullish for the defense supply chain. If we assume that cyclical companies will order fewer products, defense companies will have more access to materials and labor. After all, defense sales are anti-cyclical.

For example, we’re already starting to see easing supply chain pressure. The New York Fed global supply chain pressure index below is a good example.

Federal Reserve Bank of New York (Via Bloomberg)

It also needs to be said that Northrop is often praised as the most efficient supply chain operator in the industry. Not only is the company efficiently dealing with thousands of suppliers, but it is also a major supplier itself, which makes it easier to gain experience and use past lessons to avoid future mistakes.

When it comes to micro factors (on a company level), the company praises its space program, which is outperforming its other segments:

[…] when we look at our businesses, the opportunity exists for our Space business to continue to be our fastest-growing business over the next couple of years. Its backlog growth has been tremendous. The market is growing rapidly in the space domain, and I think we’re gaining share in that market, really across mission areas, across domains and across customer sets between our National Security customer set and on the civilian and even in pockets of the commercial market as well. You noted we’ve projected that our Aeronautics business will return to growth in 2024. Opportunities exist for growth in all of our sectors in 2024.

Again, note that these comments include strength in all segments. In 3Q22, the company won awards worth $8.7 billion, resulting in a book-to-bill ratio of 1.14. This means that the company is winning orders faster than it can turn them into finished products. That is indicative of higher future growth. Also, the book-to-bill ratio is above 1 in every segment.

With that said, I’m going to combine the valuation and dividend discussions in this article.

The Risk/Reward For Dividend Investors

2022 was a terrific year for Northrop Grumman. Not only that, but the next few years will be great as well. However, we need to be realistic. The bull case has become widely known, resulting in a return of more than 40% in 2022. In other words, we are not dealing with an undervalued gem.

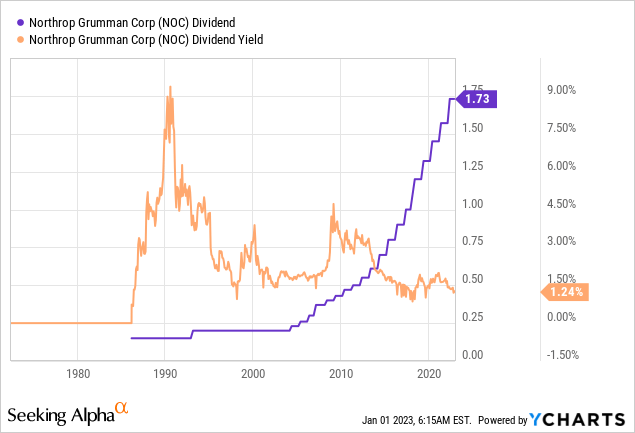

It also means that the dividend yield has come down. The company currently pays a $1.73 per quarter per share dividend. This translates to a yield of 1.3%.

This is one of the lowest yields in the company’s recent history as capital gains have outperformed dividend growth by a rather wide margin.

However, that’s where the bad news stops. The company has terrific dividend fundamentals. For example, over the past ten years, the average annual dividend growth rate was 12.1%. Over the past five years, that number is still 11.6%.

While the number one priority for its capital is obviously capital investments to remain competitive, Northrop’s second priority is the dividend. Once the dividend has been taken care of, excess cash is used for buybacks. Between 2012 and 2021, the company repurchased 38% of shares outstanding. This contributed a lot to the share price outperformance we discussed in the first half of this article.

Northrop Grumman

This year, the company is committed to returning 100% of its free cash flow to its shareholders through buybacks and dividends, which means the years of subdued buybacks are over.

In this case, drivers are not just higher growth, but also the fact that the company has a healthy balance sheet. The company has a sub-2x leverage ratio and a BBB+ credit rating. There is no need for NOC to prioritize debt reduction over buybacks.

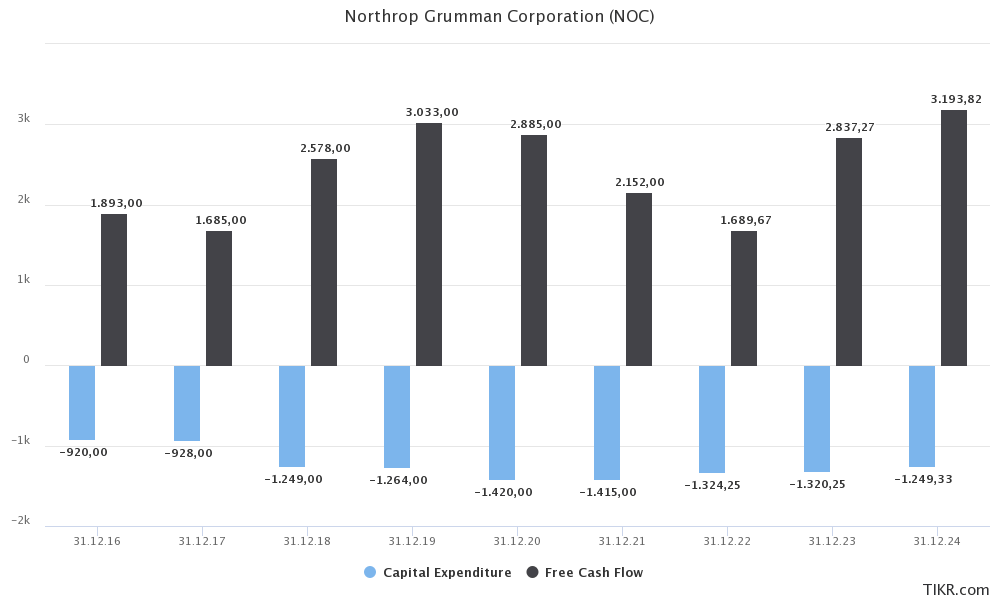

With that said, the chart below shows free cash flow and capital expenditures. Note that free cash flow already excludes CapEx (the company’s investment needs). Higher demand, easing supply chain issues, and stable CapEx spending is expected to trigger the return of high free cash flow.

TIKR.com

This means high dividend growth and buybacks are almost a certainty.

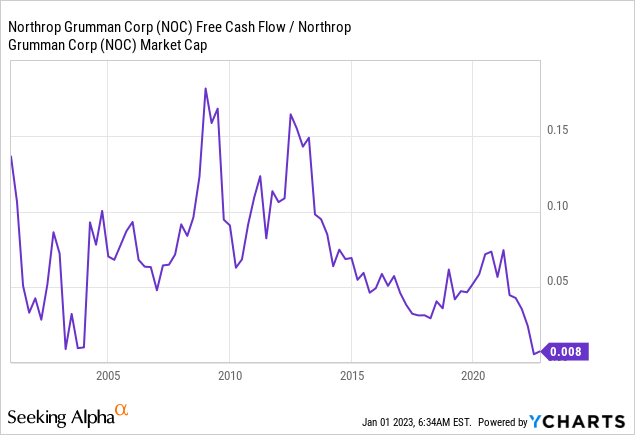

However, the valuation isn’t attractive. After all, we can put a price on free cash flow. In 2024, NOC is expected to generate $3.2 billion in free cash flow. Northrop’s current market cap is $84.0 billion. This translates to a 3.8% 2024E free cash flow yield.

This is an important part of the valuation as there is a huge difference between repurchasing shares with a market cap of $84 billion or 10-20% lower.

This implied free cash flow yield is rather low as it used to hover close to 5% prior to the birth of the new defense bull case.

Based on this number alone, I would be a buyer of NOC shares at prices 15% below the current share price.

The same goes for the EV/EBITDA multiple, which takes net debt and pension liabilities into account. Using the $84.0 billion market cap, $9.4 billion in 2023E net debt, and $2.4 billion in pension liabilities, we get an enterprise value of $95.8 billion. That is 18.8x 2023E EBITDA of $5.1 billion.

While NOC’s valuation has looked lofty for more than five years, we’re now at really lofty levels. Even if we incorporate 2024E EBITDA of $5.5 billion, we’re dealing with a forward multiple of 17.4x.

TIKR.com

Hence, just like my comment on its free cash flow, I believe that these numbers warrant an investment the moment the stock drops 15%.

That said, I was lucky to buy all of my defense shares last year on weakness. Like its peers, NOC was prone to regular sell-offs of more than 10%. This was often caused by earnings, which included supply-chain comments, or analyst downgrades as a result of high inflation and pressure on margins (also supply-chain related).

Now, here’s my takeaway.

Takeaway

Northrop Grumman protected my portfolio against mayhem last year. While the company benefited from global defense uncertainties and an accelerating need for funding, it has been a source of value and safety for decades, which is why I bought the stock in the first place.

I highly recommend NOC shares to dividend growth investors. Despite its low yield, the company brings something to the table that not a lot of companies can compete with. It has an anti-cyclical business portfolio, high exposure in fast-growing defense segments, and the ability to protect its investors against high inflation and supply chain problems.

Going forward, I expect sales growth to accelerate, providing the company with high annual free cash flow growth, used to maintain high dividend growth and buybacks.

Unfortunately, the valuation has become lofty. Hence, the single-best way to deal with NOC is to keep a close eye on the ticker. Regardless of whether you’re a NOC shareholder looking to buy more or a new investor, I would start buying as soon as NOC shares drop 10-15%. At that point, I believe the long-term risk/reward is much more attractive.

Other than that, there isn’t much more to it than buying weakness and enjoying the safety and growth potential this company brings to the table.

(Dis)agree? Let me know in the comments!

Be the first to comment