z1b

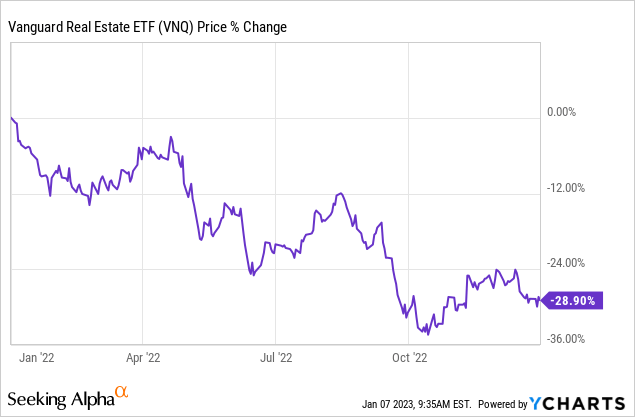

Right now, REITs are priced at their lowest valuation in years.

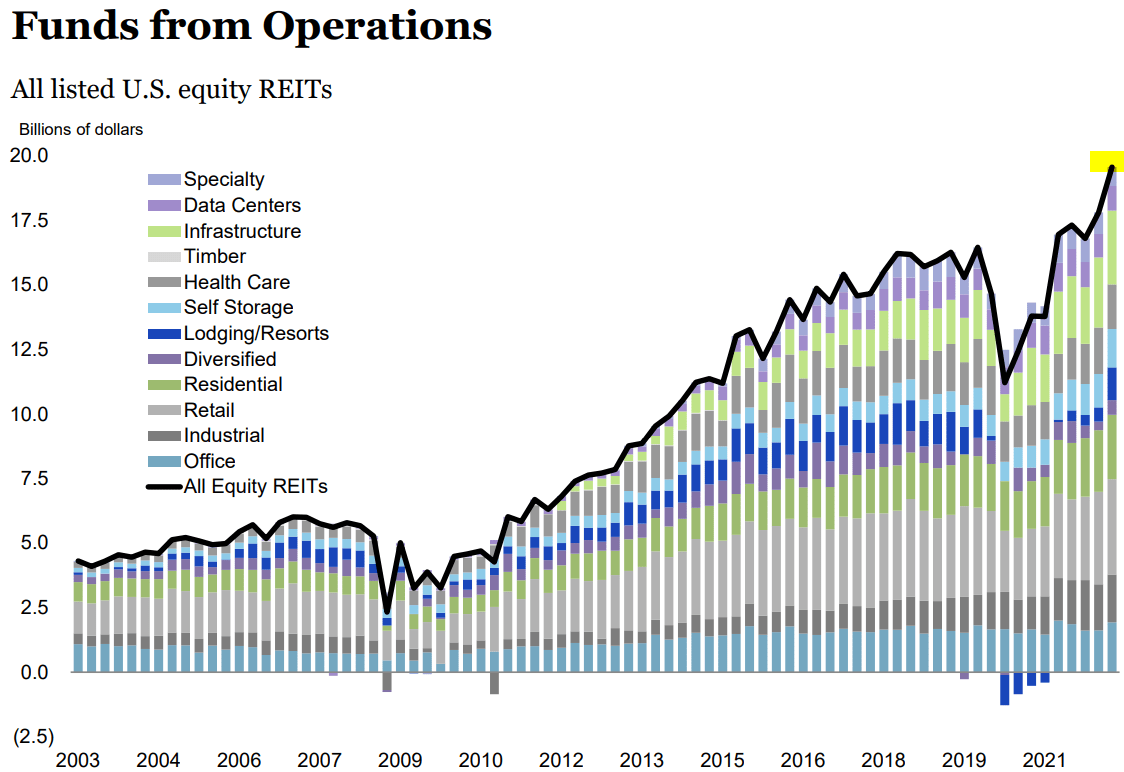

They dropped by 30% on average in 2022 even as their cash flow rose significantly, and as a result, valuations have been cut in half in many cases.

Take a look at the contrast between cash flow and valuation growth:

NAREIT

I believe that this disparity between fundamental and share price performance is an opportunity for long-term-oriented investors.

Of course, we cannot predict how REITs or any other stocks will perform in the short run, but over long time periods, it has always been a good idea to buy good real estate when it has been deeply discounted, and that’s the case today.

There are a number of rapidly growing, recession-resistant REITs that are priced at pennies on the dollar. We are today accumulating many of them for our Portfolio at High Yield Landlord, and in today’s article, I will highlight two particular REITs that are priced at exceptionally large discounts at the moment.

The first REIT that I want to highlight is BSR REIT.

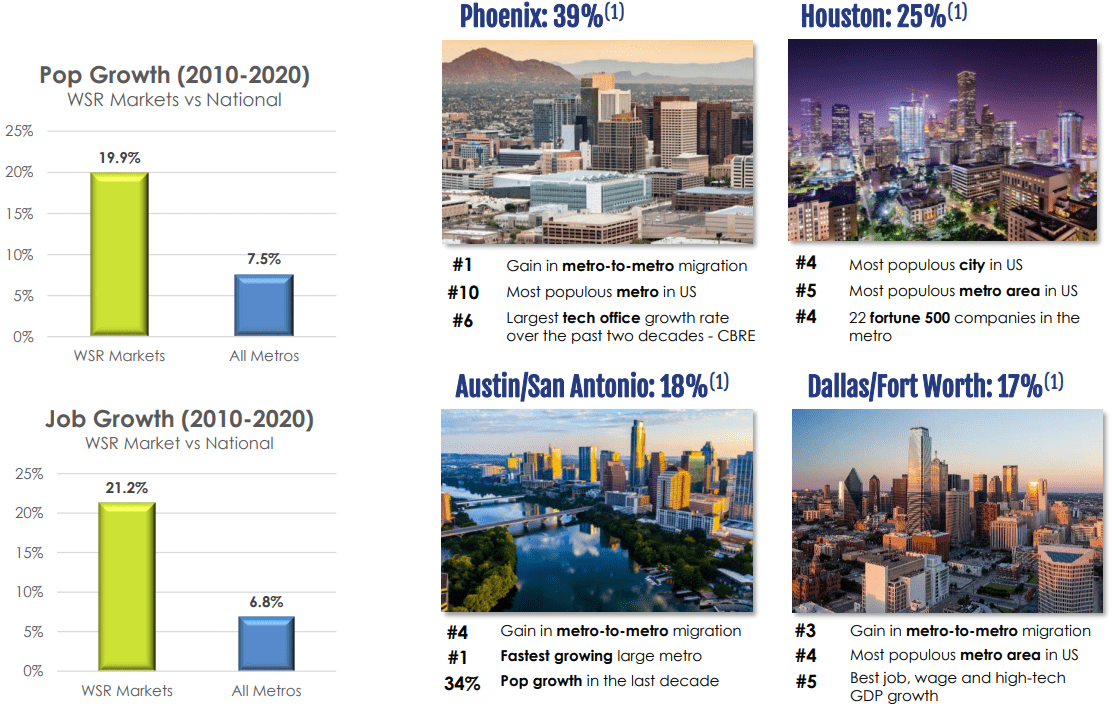

BSR is an apartment REIT that specializes in rapidly growing Texan markets like Dallas, Austin, and Houston:

BSR REIT

BSR REIT

This sets it apart from other apartment REITs like AvalonBay (AVB), Equity Residential (EQR), and Essex (ESS) because these Texan markets are today experiencing very rapid growth.

Lots of companies are moving to these states to benefit from their lower costs, good access to talent, and lack of state income tax. Tesla (TSLA) was one of them to make the move, but there have been many others.

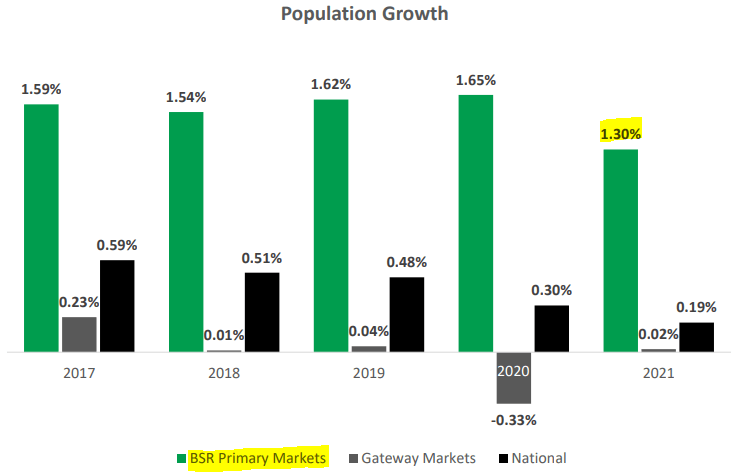

These companies then bring jobs with them, and people tend to follow jobs. This has historically led to rapid population growth, and this growth is expected to continue:

BSR REIT

You can easily imagine how this would benefit a REIT like BSR that owns affordable, well-located apartment communities.

It increases the demand for its apartments and since this increase in demand hasn’t been matched with enough new supply, rents are going up.

And they are not going up by a few percentage points… they are going up very significantly.

BSR has not reported its 4th quarter results yet, but it is predicted to grow its same property NOI by 12-14% in 2022 alone.

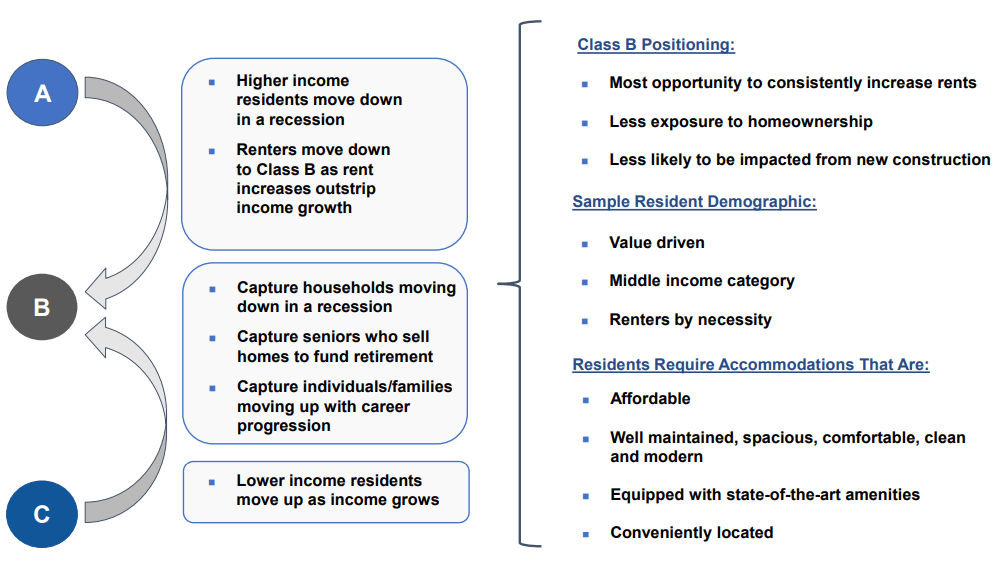

This growth will likely slowdown in 2023, but even today, its rents remain below market at just $1,460 and represent only 20% of its resident’s income, which is about 2x lower than in gateway coastal markets, where it is commonly closer to 40%:

BSR REIT

So on one hand, there is more room for strong rent growth, and on the other hand, BSR should also be relatively resilient to a future recession because its rents are below market and only represent a small portion of its resident’s income. If anything, you would expect people to downgrade from expensive Class A communities to BSR’s affordable Class B communities in a recession, leading to even more demand.

Independence Realty Trust

So BSR owns very attractive assets, and this is the type of REIT that would typically trade at an expensive valuation.

But against all odds, it is today priced at a 40% discount to its net asset value.

Is it maybe overleveraged? No, it isn’t. The LTV is just around 35%, and most of its debt is fixed rate or hedged. It has no maturities in 2023. And it has a low payout ratio of around 67%, which would leave ample cash flow to pay off debt if they wanted to.

So if it is not overleveraged, what else could justify this low valuation? Could it be poorly managed?

Again, that’s not the case. BSR’s management is very well aligned with shareholders because they own about 40% of the equity themselves, and as such, they have a lot of skin in the game. The value of their equity and its growth is far more important to them than their salaries. Further proof of good alignment is that they are today buying back shares, and they also hiked the dividend in 2022.

In a recent exclusive interview that we did for High Yield Landlord, the CEO explained that they expect to buy back shares for as long as they remain heavily discounted relative to the street value of their assets because it offers them the best risk-to-reward.

So to recap, here you have a high-quality REIT that owns desirable assets, has a good balance sheet, and a shareholder-friendly management team, and yet, it is priced at just 60 cents on the dollar. That’s a pretty attractive value proposition if you ask me.

Just to return to its NAV (where it traded in 2022), it would need to rise by 70%, and while you wait, you also earn a 4% dividend yield, and the management keeps buying back shares and hiking rents to create further value for shareholders.

For these reasons, BSR represents 7% of our Core Portfolio at the moment.

Whitestone REIT (WSR)

The second REIT that I want to highlight is WSR.

WSR is similar to BSR in that it is a fairly small REIT. It is also heavily discounted. And it is mainly invested in rapidly growing sunbelt markets.

But unlike BSR, WSR invests mainly in service-oriented strip centers instead of apartment communities.

Think about the local grocery store that you visit weekly. It probably also has a gym attached to it. Maybe a barbershop. A few quick service restaurants, etc. Examples of typical tenants include Whole Foods (AMZN), Chipotle (CMG), and Planet Fitness (PLNT):

Whitestone REIT

I like these properties for three reasons:

-

They are e-commerce resistant for the most part. Even Amazon invests in such properties via Whole Foods because you cannot easily get these services online.

-

They are largely recession resistant. People still need to eat and get essential services during recessions. Moreover, WSR is a landlord so its rent checks are quite steady.

-

They are located in rapidly growing sunbelt markets. WSR’s biggest markets are Phoenix and Austin, both of which have been among the fastest-growing cities in recent years.

Whitestone REIT

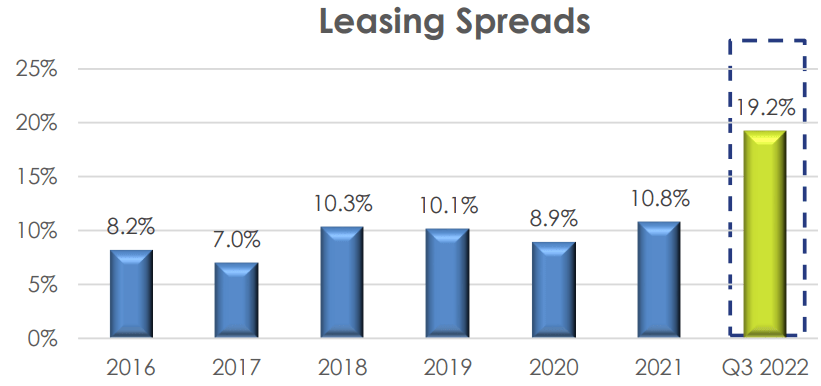

As a result, rents are growing rapidly. In the most recent quarter, the company’s releasing spreads reached 19%! And today, lots of leases still haven’t been adjusted higher, so we can expect this strong growth to continue in 2023:

Whitestone REIT

Despite that, just like BSR, WSR is also priced at a huge discount on its net asset value. We estimate that the discount is right around 40%, but according to its most recent asset sales, the discount could be as large as 50%.

That’s rather unusual for assets of this quality.

So this leads us to wonder again: is the company overleveraged? Not really. The leverage is a bit high, but the management is focused on deleveraging the balance sheet and the plan is to be below 7x Debt/EBITDA within a year.

Is the company poorly managed? It isn’t, but it used to be, and this is probably why WSR is so heavily discounted. Long story short, WSR used to be poorly managed, and the managers were grossly overpaid. But the board fired the previous CEO for a cause, and now the company has new leadership that’s laser-focused on creating shareholder value. I have talked with them a few times over the phone, and I am convinced that the company is now headed in the right direction.

It will probably take some time for them to build a track record and regain the trust of the market, but they are now well on their way to achieving that, and you can still buy shares at a steep discount.

Just like BSR, WSR would also need to appreciate by about 70% to reach its net asset value, and while you wait, you also earn a 5% dividend yield. It is hard to beat that coming from a relatively defensive and growthy real estate investment.

Bottom Line

One of our competitive advantages at High Yield Landlord is that we get to regularly talk to management teams because we have a following on Seeking Alpha and REIT managers want to get their message out.

This often allows us to identify small-cap REIT opportunities like BSR and WSR, which we currently own in our Core Portfolio. They essentially allow us to buy real estate at 60 cents on the dollar, and we then get the added benefits of professional management, diversification, liquidity, and limited liability on top of that for free.

This is why most of my capital is going into these REITs at the moment. I think that, priced as they are, they offer some of the best risk-to-reward in today’s market.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment