PeopleImages/iStock via Getty Images

Co-produced by Austin Rogers

The saying “Buy when there’s blood in the streets” is much older than many people think.

It would be natural to assume that this saying originated during the fearsome stock market crash of 1929.

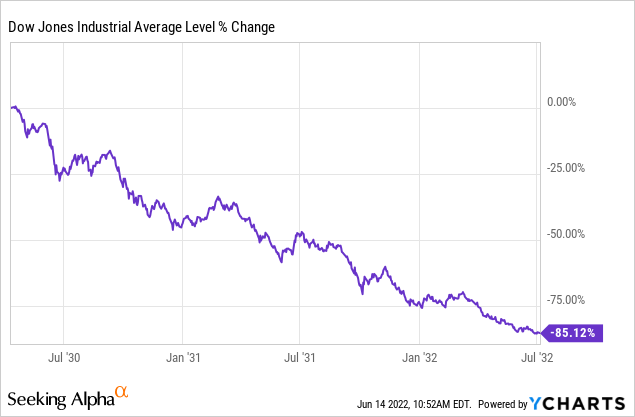

The Dow Jones Industrial Average (DJI) chart from YCharts does not go further back than 1930, so this chart below begins in April 1930, after the stock index had recovered about 60% of its losses during the brutal 1929 crash.

Dow crashes 85% (YCHART)

The DJIA peaked in September 1929 at 381.17 after sextupling (increasing sixfold) over the previous eight-year bull market. Then, over the next three years, the index shed some 89% of its value to bottom at about 43.50.

Imagine pouring your life savings into the stock market, never imagining that the massive wealth creation of the 1920s could turn into the massive wealth destruction of the 1930s, only to see 90% of your money go up in smoke. Or, if you were one of the many people buying stocks on margin back then, perhaps you would’ve lost everything.

There are stories of stockbrokers reading the tape from the ticker machine and then hurling themselves out their office windows to their deaths.

Some might think this is where “blood in the streets” comes from. But the saying is even older than that.

In fact, it originates from Baron Nathan Rothschild, an English-German financier and second-generation member of the famous Rothschild banking family. In the widespread panic and uncertainty following the news of Napoleon’s loss at the Battle of Waterloo in 1815, Baron Rothschild is said to have made a great fortune by buying the dip.

You might say that Rothschild was greedy when others were fearful. And it dramatically increased his wealth in the long run.

The Bear Market Is Upon Us

Today, investors have the opportunity to take after Baron Rothschild and buy when there’s (metaphorical) blood in the streets.

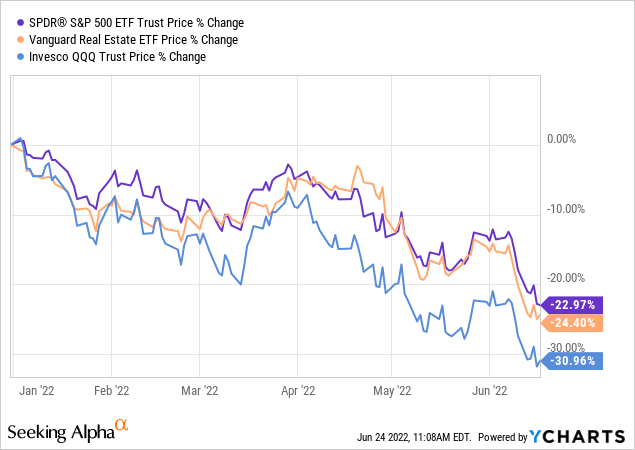

Recently, the S&P 500 (SPY) and Vanguard Real Estate ETF (VNQ) dipped into bear market territory by falling more than 20% from their high, and the tech-heavy Nasdaq (QQQ) reached a 30% decline from its high.

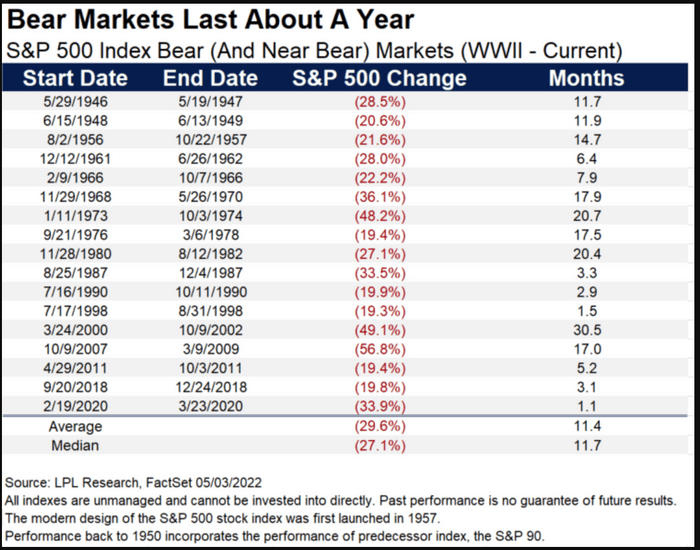

Since the end of World War II, the average decline of the S&P 500 during bear markets has been about 30%, and the average duration of bear markets has been a little over 11 months.

Bear markets last about one year (LPL Research)

Of course, a lot of variance is hidden in those averages.

During bear markets, stocks have declined as little as 20% and as much as 57% during the financial crisis of 2008-2009. Likewise, the peak to trough period has been as short as slightly over one month (at the beginning of the COVID-19 crisis) and as long as 30.5 months in the wake of the dot com bubble crash of 2000.

Bear markets are like snowflakes. Each one is unique and runs its course differently from all the others.

How do we keep calm and, like Baron Rothschild, “buy when there’s blood in the streets”? We do so by investing with the mindset of a landlord rather than a short-term trader.

That is, we pay close attention to the fundamentals of the businesses we own, and we do not like the fluctuations of the price affect us emotionally. They say knowledge is power, and in this case, it is absolutely true. Knowledge of the operational fundamentals of the businesses and real estate we own provides us with the power of will and mental fortitude to hold through the volatility and even to keep buying.

Three Reasons To Buy REITs Right Now

In particular, we believe bear markets are a fabulous time to accumulate real estate investment trusts (“REITs”) into a diversified stock portfolio.

This may go against some commonly held misbeliefs about real estate during periods of rising interest rates and economic weakness. So, here are three reasons why we believe now is a great time to buy REITs:

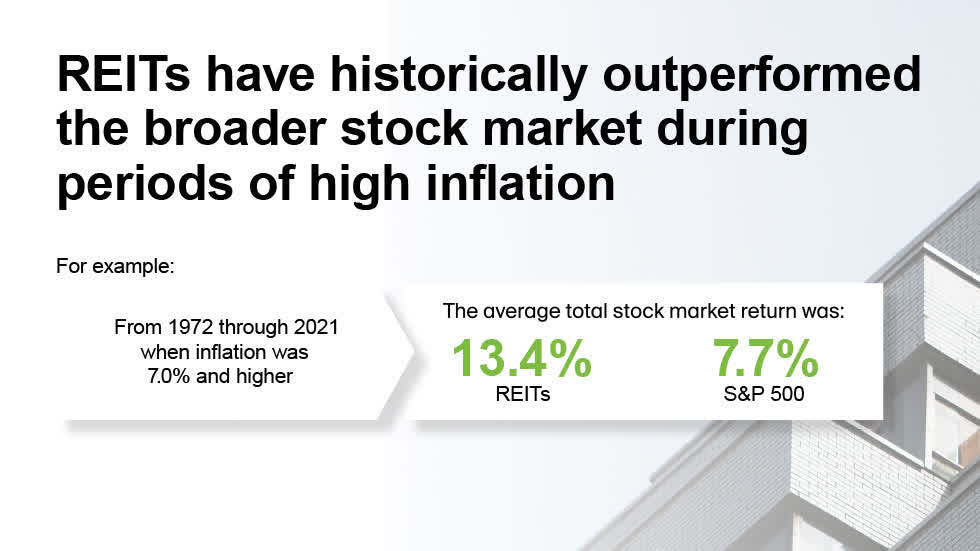

1. REITs historically outperform during periods of high inflation. Real estate values and rent rates rise along with general prices.

REITs outperform inflation is high (NAREIT)

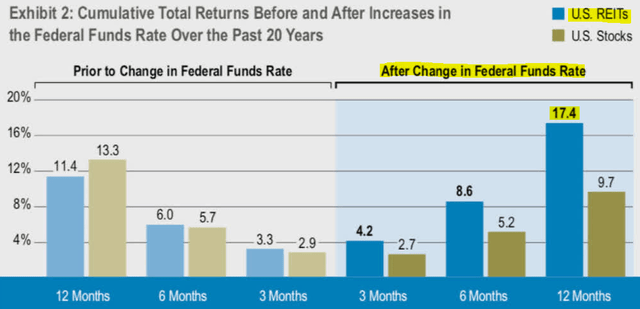

2. REITs historically outperform in the 3, 6, and 12 months after increases in the Federal Funds rate. Rent growth during these periods more than offsets any headwind of rising borrowing costs.

REITs outperform during times of rising interest rates (Cohen & Steers)

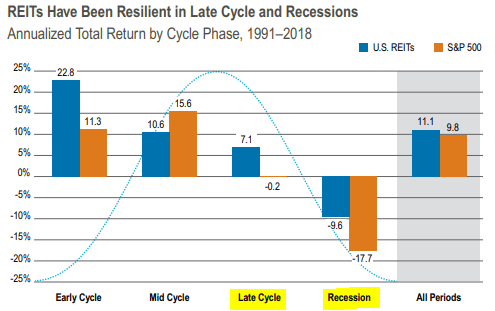

3. REITs historically outperform during late cycle periods and recessions. Most tenants do not want to give up their real estate locations by defaulting on their lease unless they absolutely have to.

REITs outperform during recessions (Cohen & Steers)

Most of the real estate that businesses lease is mission-critical, meaning that it is necessary to carry out the core functioning of the business model. As such, REITs’ rental revenue tends to be more stable during recessions than the average non-real estate company. Moreover, during periods of elevated inflation, businesses agree to pay higher rent rates so as to continue the use of their valued real estate infrastructure.

With that said, here are three REITs that we are particularly bullish on right now.

1. Agree Realty Corporation (ADC)

ADC is a $5 billion market cap triple net lease REIT that owns a rapidly growing portfolio of high-quality, e-commerce-insulated and recession-resistant retail real estate. Two-thirds of its rental revenue comes from investment grade credit-rated tenants, with Walmart (WMT) as its largest tenant by revenue at over 6%.

Triple net lease properties (Agree Realty Corporation)

As the REIT has dramatically ramped up its pace of acquisitions in the last few years, the portfolio quality has only increased. The percentage of investment grade retailers has increased around 500 basis points from two years ago, and that momentum continued in Q1 2022 with 74% of rents acquired coming from IG retailers.

Why this relentless focus on the nation’s largest and strongest retailers? After all, cap rates for these properties tend to be lower amid high investor demand for safe cash flows.

Well, ADC’s strongly shareholder-aligned management team is forward-thinking, and it is their view that single-tenant buildings are the ideal format for retailers to thrive in the face of rising e-commerce sales.

Triple net lease properties in a digitized world (Agree Realty)

Of course, these retailers need to be well-capitalized and have strong balance sheets in order to invest in an omnichannel future wherein customers have many ways of ordering and receiving goods. Hence the emphasis on IG retailers like Walmart, Home Depot (HD), Tractor Supply Co. (TSCO), and T.J. Maxx (TJX).

With a BBB credit rating, net debt to EBITDA of only 5.0x, virtually no debt maturities until 2025, and a recent forward equity raise of 5 million shares at $68.65 apiece, ADC looks well prepared to continue its acquisition spree through the volatility this year.

ADC’s 4.2%-yielding dividend has been growing in the high single-digits and likely will continue to do so in the years to come.

2. Crown Castle International Corp. (CCI)

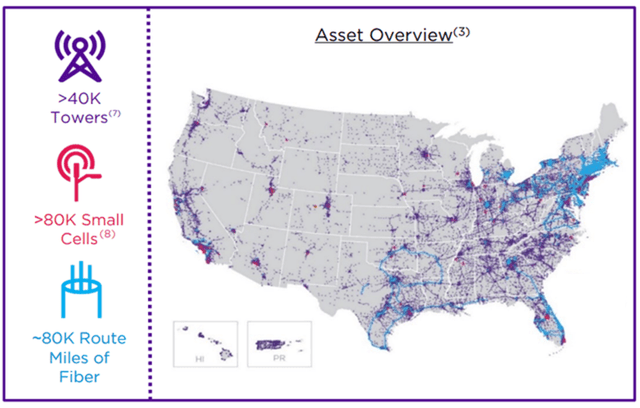

Focused on its core market in the United States, CCI is the nation’s largest owner/operator of telecommunications infrastructure, including both towers and small cell nodes scattered across the country.

Crown Castle International asset overview (Crown Castle International)

While it is difficult to discern how much the 5G revolution will benefit the major carriers like AT&T (T), Verizon (VZ), and T-Mobile (TMUS) because of the massive amount of capital these telecom providers need to invest in its rollout, it is undeniable that the 5G rollout is hugely beneficial to CCI.

CCI’s portfolio of over 40,000 cell towers, 80,000 small cell nodes, and 80,000 route miles of fiber play a mission-critical role in the provision of 5G services as well as the increasing consumer demand for fiber internet. The small cells, which are basically mini communications relays placed in dense, urban areas to boost the signal, should become especially valuable the more 5G investment the major carriers make.

Surely there will be ebbs and flows in the level of demand from cell carriers, but overall CCI’s business model should continue to provide recession-resistant growth of both cash flows and dividends, continuing its impressive streak since conversion into a REIT in 2014.

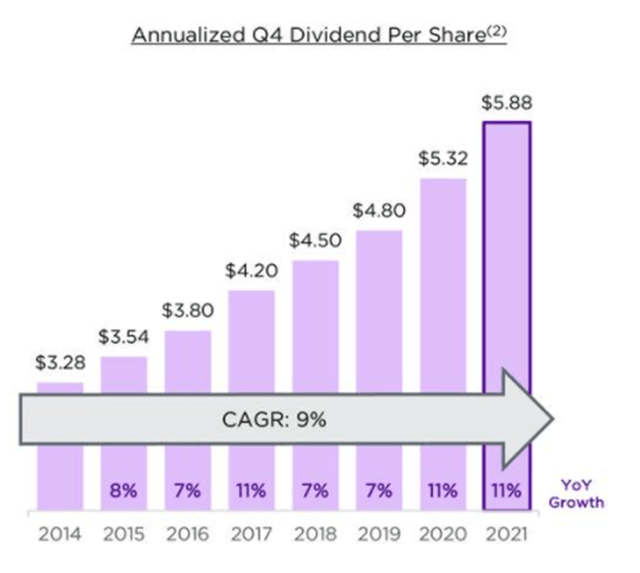

Crown Castle International dividend growth (Crown Castle International)

CCI’s strong balance sheet and BBB credit rating should serve the REIT well amid rising interest rates, and its revenues should remain steady as consumers will likely keep paying their cell phone bills even through a recession.

CCI’s 9% average annual dividend growth since 2014 should continue for the foreseeable future.

3. Medical Properties Trust, Inc. (MPW)

MPW owns a portfolio of 440 hospitals and other healthcare facilities across 10 countries such as the 384-bed general hospital, St. Francis Medical Center, in Lynwood, California:

Hospital property investment (Medical Properties Trust)

MPW’s basic business model is to perform sale-leasebacks with large health systems, in which the REIT buys real estate on the books of healthcare operators and immediately enters into a long-term lease with that operator to continue occupying the property.

MPW’s leases are triple-net, which put tenants in charge of all property maintenance, insurance, and taxes. On top of that, the vast majority of leases contain CPI-based rent escalations that provide rent bumps up to 5% per year, which operators can typically handle because insurance reimbursement rates have historically risen faster than the CPI.

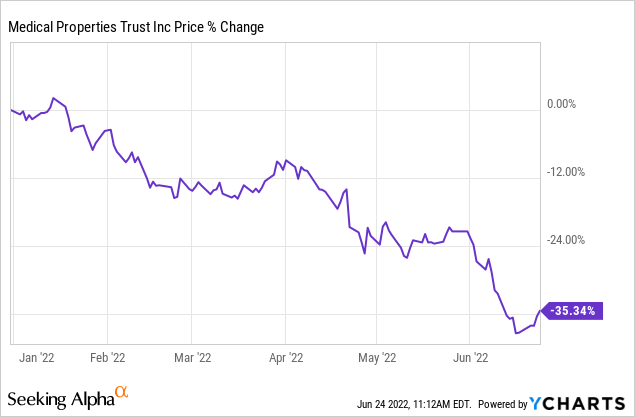

Lately, MPW has endured a 35% selloff, in part over fears of tenant weakness. After all, hospital revenue has taken a hit the last few years from reduced elective surgeries during the pandemic.

Recently, MPW reported that rent coverage for its largest tenant, Steward Health, remains over 3x. The same goes for most of its other tenants.

Also, MPW has multiple layers of protection even in the case of a tenant default or bankruptcy.

First, it enjoys master leases that cover multiple properties under a cross-default provision. This prevents tenants from simply defaulting and handing over the keys to MPW for any single property. In the case of a single default, MPW has the right to retake all properties covered under a master lease, which incentivizes the tenant to prioritize rent payment.

Second, MPW’s leases are crafted specifically to withstand any scrutiny during bankruptcy proceedings. In other words, they are designed to prevent the tenant from renegotiating lower rent in bankruptcy court.

Third, MPW has established strong relationships with all of the nation’s largest and strongest health systems. If a tenant-operator did need to vacate a property in the worst-case scenario, MPW would have multiple potential suitors to take over operations at that property.

MPW’s 7.8% dividend yield now looks extraordinarily attractive from a risk-adjusted perspective.

Bottom Line

The most important thing to do in a bear market is to prevent yourself from panicking and making rash decisions with your money. Do not feel that you need to lock in unrealized losses in order to prevent further losses.

Instead, take on the mindset of a landlord. Ignore the digital red ink and focus on the operations of the businesses and real estate that you own. Only consider selling if you are sure that the business model is permanently impaired and likely to go to zero. Those are rare cases.

Like Baron Rothschild, we advise using your available cash to take advantage of widespread panic and “buy when there’s blood in the streets.”

Be the first to comment