z1b

Earlier this month, I shared 2 REITs that I would sell before going into 2023.

These are Global Net Lease (GNL) and Tanger Factory Outlet (SKT):

GNL is poorly managed, it is heavily exposed to single-tenant office buildings, and its dividend isn’t sustainable.

SKT is a great REIT, but I fear that its outlet center business will experience some difficulties going forward and its valuation remains excessive relative to some peers like Simon Property Group (SPG).

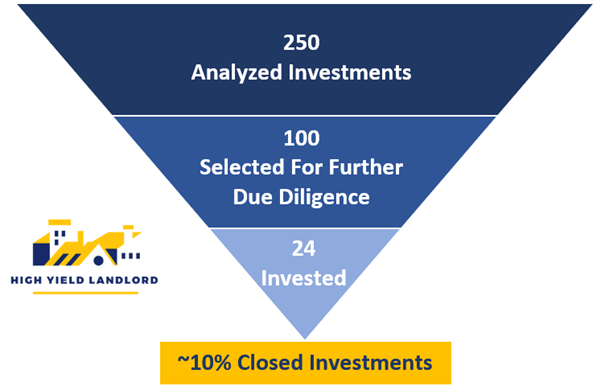

These are just 2 examples of REITs that I wouldn’t buy today, but there are many others. We are very selective at High Yield Landlord and only invest in the REITs that offer the best combination of yield, growth, value, and safety.

This results in us investing in only one REIT out of ten on average:

High Yield Landlord

It is when you get the right mix of yield, growth, value, and safety that your investment results improve materially.

GNL yields a lot and it is cheap, but its growth is negative on a per-share basis and its asset base is very risky.

SKT has grown rapidly in the past, but it is expensive and risks are on the rise.

Therefore, they don’t belong to our short list of Top REIT buying opportunities for 2023, which includes around 25 REITs at the moment.

Below, we highlight two of them for you so that you get a sense of what we are buying as we head into the new year:

Healthcare Realty (HR)

Over the past weeks, most REITs surged to higher levels as they released strong quarterly results.

But one REIT failed to recover and continues to trade at an exceptionally low valuation.

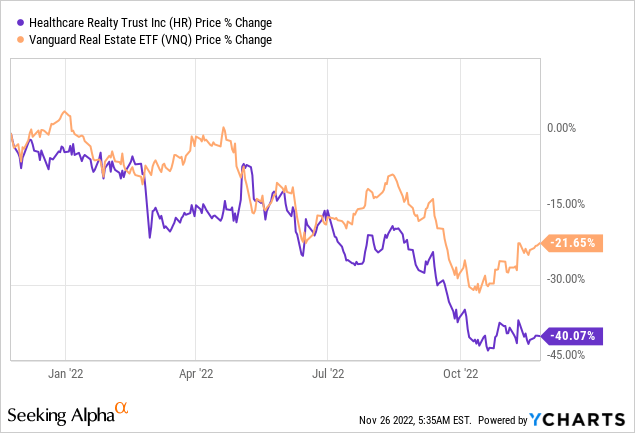

That is Healthcare Realty:

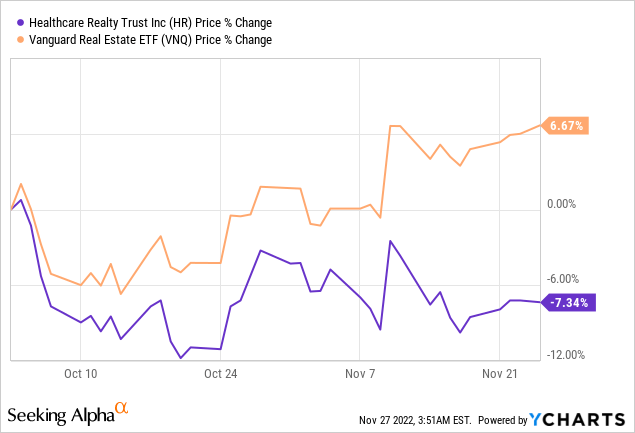

YCHARTS

It is down nearly twice as much as the Vanguard Real Estate ETF (VNQ) at the moment.

This is especially intriguing when you consider that HR is what you would typically describe as a high-quality REIT. It owns a defensive portfolio of medical office buildings, it has a good balance sheet, a strong track record, and it has guided for this steady 5-7% FAD per share growth in the years ahead.

That’s despite all the uncertainty:

Healthcare Realty

Healthcare Realty Healthcare Realty Healthcare Realty

So if anything, you would expect a REIT like HR to outperform in today’s environment given that it is more resilient than your average REIT.

The CEO of Physicians Realty (DOC), a close peer of HR, has previously described medical office buildings as the safest segment of the entire real estate market. They are largely non-cyclical assets that generate consistent and predictable cash flow that grows slowly, but very steadily through economic cycles. That’s precisely what you would want to own as we potentially head into a recession.

Why is it down so much then?

And why has it kept underperforming in recent weeks?

YCHARTS

I suspect that HR’s recent merger with HTA, another medical office REIT, has caused its share price to underperform because of two reasons:

Firstly, many former shareholders of HTA simply aren’t interested in owning HR and therefore, they have decided to exit, causing a steady stream of investors to sell their positions. They never bought HR in the first place and so they aren’t as attached to it.

Secondly, the merger caused some uncertainty because HR expected to sell some of HTA’s assets outright or via JVs to raise some cash. But shortly after the merger closed, interest rates surged and the transaction market cooled down. As a result, the market worries that HR won’t be able to execute its plan, at least not at the cap rate level that it intended, leading to some dilution.

But HR just reported that they have actually had good success, despite all the uncertainty:

“Associated with the merger, the Company has closed $922 million in joint ventures and asset sale transactions at a weighted average cap rate of 4.6%. Transactions totaling $105 million are under contract and expected to close in November. In December, the Company expects to complete the remaining sales that will bring the total to over $1.1 billion at an expected weighted average cap rate of 4.8%.”

Source: HR Q3 report

“I’d like to commend my colleagues who worked tirelessly to accomplish this remarkable outcome in the current market environment. Moving forward, we can afford to be more patient. We currently have a lot of lines in the water. You’ll see us sell assets selectively where it makes sense strategically and financially.”

Source: HR CEO Todd Meredith, Earnings Call

The plan was to execute the sales at an average cap rate of 4.8%, but so far, they have gotten even higher sales proceeds, selling assets and JV partnerships at a 4.6% cap rate.

A lot of these assets were sold when interest rates were a bit lower so it may get a bit more difficult going forward, but they have already achieved the bulk of their expected sales, which gives them more flexibility.

It shows that there is still a lot of demand for medical office buildings and that’s not surprising since they provide highly defensive, long-dated, inflation-protected cash flow in an uncertain world.

So ultimately, I believe that the recent underperformance is caused by temporary factors that will eventually lead to a delayed recovery in HR’s share price and valuation.

HR actually reported strong quarterly results with accelerating same-property NOI growth, now reaching nearly 3%. The G&A synergies of its merger are also well ahead of schedule. And the company has attractive investment opportunities to redeploy the capital of its recent capital recycling.

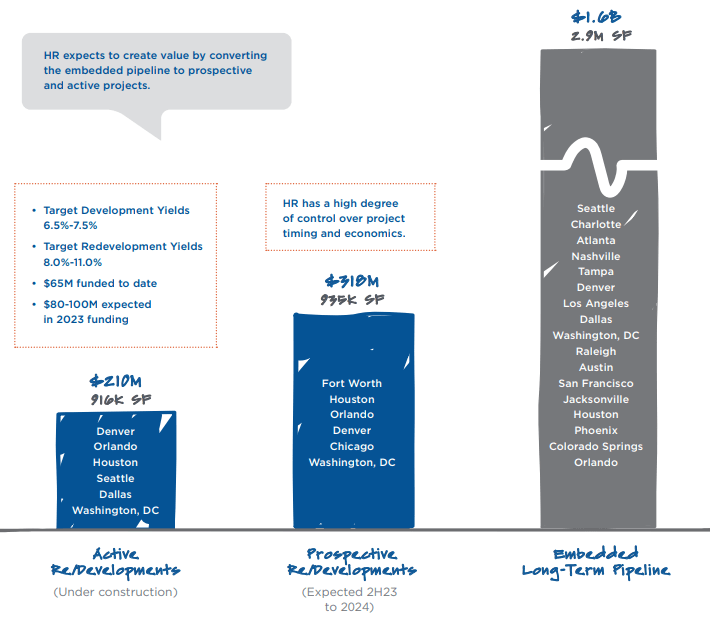

It has a pipeline of development opportunities with a ~7% projected initial yield and redevelopment opportunities with yields even greater than that:

Healthcare Realty

All in all, the 5-7% FAD per share long-term growth target seems quite doable given the accelerating same property NOI growth and the attractive external growth opportunities.

That’s a strong growth rate for a defensive REIT and in most cases, investors would reward such a REIT with a healthy FFO multiple and a small premium to NAV.

But because of the 2022 crash and the recent merger, HR is now priced at a 35% discount to NAV, 12x FFO, and it pays a 6.4% dividend yield with a conservative 75% payout ratio.

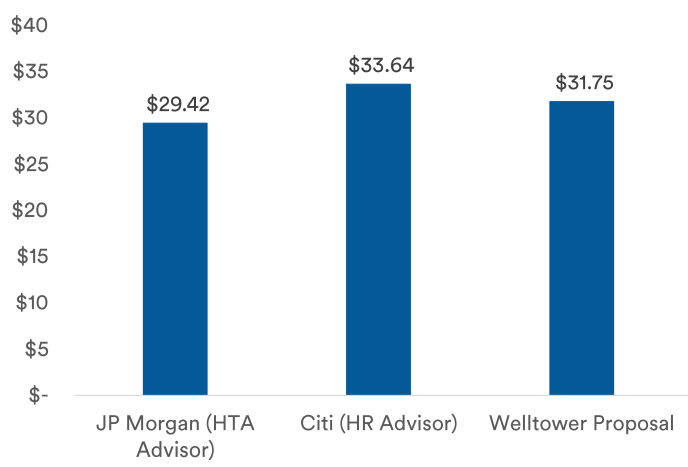

Welltower actually offered to buy out HR last year at $31.75 per share and the fairness opinion of various advisors put HR’s fair value at around $31 so we have real evidence that its NAV is materially higher than its current share price of $19:

Healthcare Realty

HR’s board of directors recently also announced a $500 million buyback program which they expect to implement in the coming quarters.

All in all, HR appears to be a great opportunity for more conservative income-seeking investors.

We think that HR is likely to generate double-digit total returns for shareholders from its 6.4% dividend yield and its 5-7% FAD per share growth prospects, and in addition to that, it has up to 50% upside potential as it eventually reprices near its NAV.

It offers a great combination of yield, growth, value, and safety. Exactly what we like to target at High Yield Landlord.

Here is another example:

EPR Properties Series G Preferred Shares (EPR.PG)

A lot of REIT investors only look at common shares and forget that there are plenty of REIT preferred shares that are also opportunistic.

EPR Properties (EPR) is a good example of that.

We think that both, its common and preferred equity, are opportunistic at today’s levels, but the preferred equity is especially attractive for more conservative investors because they are heavily discounted due to reasons that shouldn’t affect them.

Put simply, investors fear EPR because it is a net lease REIT that specializes in experiential properties and about 1/3 of its portfolio (measured by NAV) is invested in movie theaters.

EPR Properties

I think that the fears are overblown because:

- 2/3 of the portfolio is doing exceptionally well with rent coverage ratios at 2.8x, up from 2.2x prior to the pandemic.

- EPR’s theaters are some of the most productive megaplex theaters in the nation. Netflix (NFLX) may cause some lower-quality theaters to close down, but the highest-quality theaters may benefit from this.

- Today, the box office is still much lower than prior to covid but the rent coverage of its theaters is already positive at 1.3x.

- The box office is expected to recover higher with a strong movie slate for 2023. Even Amazon (AMZN) recently said that they plan to invest $1 billion a year on theatrical film releases going forward.

- EPR has 14-year-long leases with 1.5 -2% annual contractual rent increases.

- It has an investment-grade-rated balance sheet with a net debt to EBITDA of 5.2x, no maturities until 2024, no secured debt, and $1 billion available on its revolver.

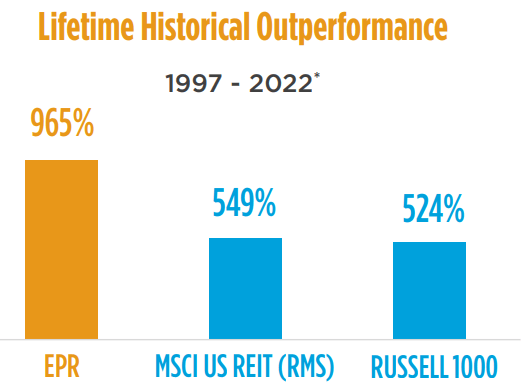

- Finally, they have an exceptionally strong track record and even survived the pandemic, which was the worst possible crisis for the company:

EPR Properties

So I am bullish on the common equity and own a good position.

But even then, I can understand why some people are reluctant to buy it given that some of its top tenants include AMC (AMC), Cinemark (CNK), and Regal, whose parent company Cineworld (OTCPK:CNNWQ), is currently in bankruptcy.

But the preferred equity is still a lot safer than the common equity, and it makes even less sense for the market to discount it so heavily.

The preferred equity is only a small fraction of the balance sheet and the common equity offers significant buffer even in case of troubles:

EPR Properties

Today, the payout ratio is only 68% for the common equity and EPR even hiked the dividend in 2022. That also tells you a lot about the safety of the preferred dividend, which comes ahead of the common.

And yet, the preferred equity is today priced at just $17.50, representing a 30% discount to its par value, and it trades at an 8.2% dividend yield.

We think that the preferred dividend would be sustainable, even if EPR suffered some big setbacks, and eventually, the share price will return to par, unlocking ~40% of the upside for shareholders.

As such, the preferred equity of EPR offers a nice combination of yield, growth, value, and safety.

Bottom Line

There are lots of opportunities in the REIT sector right now because valuations are at a historical low. But it is still important to be selective if you want to beat the sector averages (VNQ).

Be the first to comment