phive2015

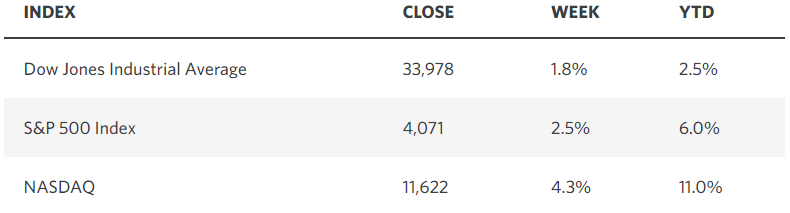

John Templeton said “bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria.” I’d say we are still in the pessimistic stage after a more than 16% rally in the S&P 500 from its October bear-market low. The certainty with which the bearish consensus is convinced that the market will retest last year’s low, if not fall below it, is what makes me think it won’t happen. Despite mixed earnings news, stocks soared last week, as investors welcomed another decline in inflation measures that was accompanied by a slower but still positive rate of economic growth in the fourth quarter of last year. At the same time, the labor market remains strong with weekly unemployment claims falling to just 186,000. We are on track for one of the best Januarys in more than twenty years, which bodes well for the rest of the year, as a gain in January has led to a gain for the year two-thirds of the time over the past five decades.

Edward Jones

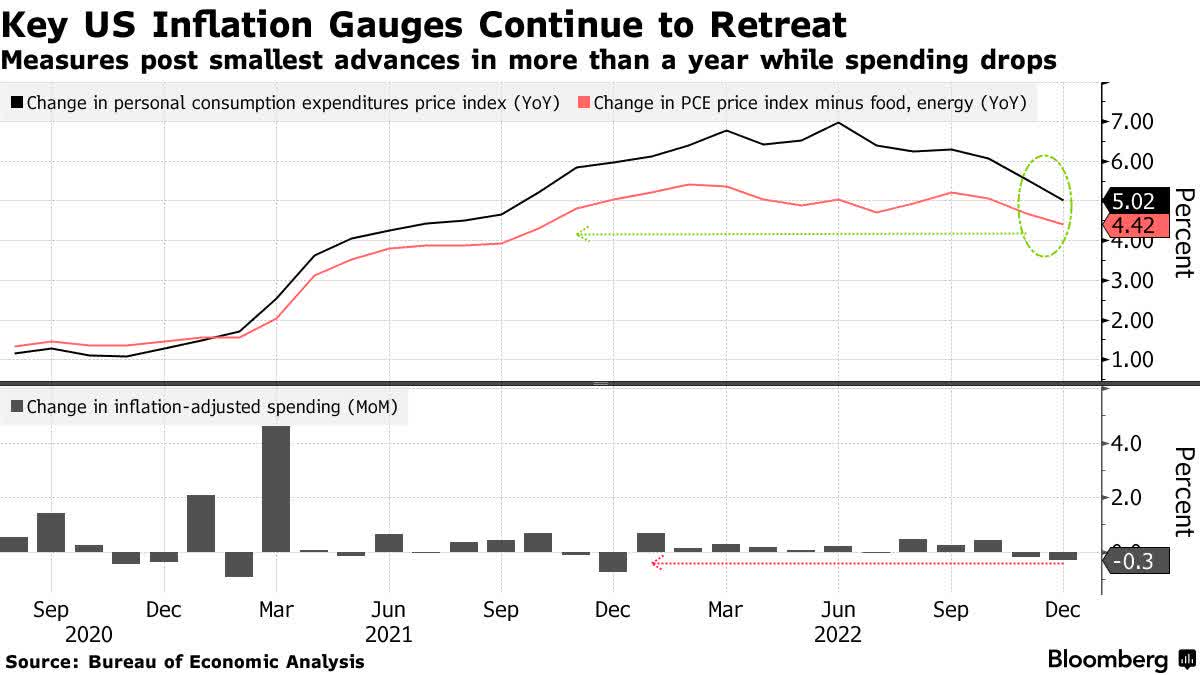

The Fed’s preferred measure of inflation being the personal consumption expenditures price index (PCE) fell to 5% in December, while the core rate that excludes food and energy fell to 4.4%. These are the lowest rates we have seen since late 2021, and they are coming down without significant job losses that most feared would undermine the current economic expansion. This is why more and more investors are warming to the idea of a soft landing in 2023. It is also why consumer sentiment is gradually recovering.

Bloomberg

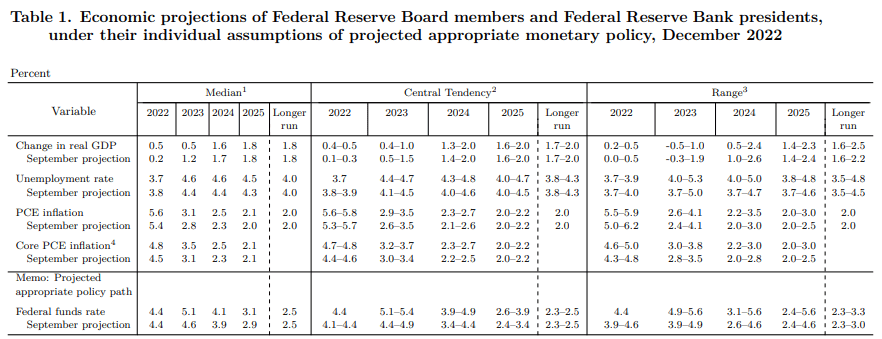

At the Fed’s last meeting in December it increased its forecast for where the rate of inflation would finish the year from 5.4% to 5.6% for the PCE and from 4.5% to 4.8% for the core PCE. They should have been lowering the numbers. Still, the latest data should result in reaching their year-end targets much sooner for 2023, and I suspect this will be reflected in the next update to their Summary of Economic Projections.

Federal Reserve

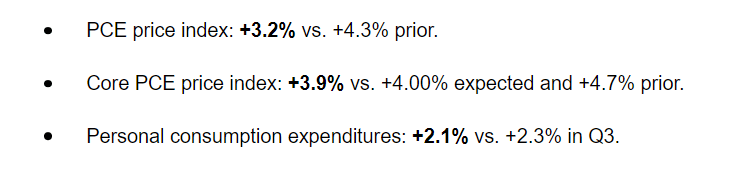

The annualized rate of inflation in the fourth quarter of last year fell to 3.2% from what was 4.3% in the third quarter, while the core rate fell from 4.7% to 3.9%. I think both will be within a 2-3% range by the end of this year.

SeekingAlpha

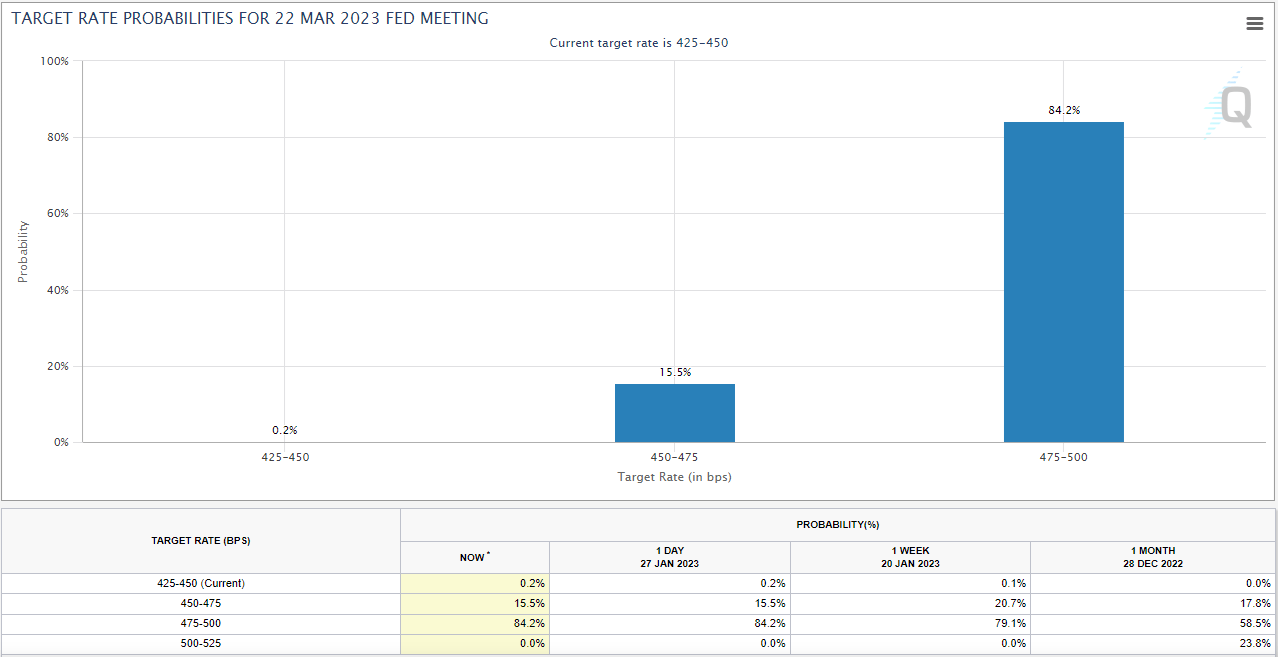

While the Fed will most assuredly raise rates by a quarter point this week, there should be enough evidence of disinflation by the next meeting in March to end the rate-hike cycle with a terminal rate of 4.5-4.75%. The chances of that have hovered between 15-20% over the past month in the Fed funds futures market, but they were practically zero a few months ago. As this probability increases, it should be supportive of risk asset prices.

CME Group

These positive developments on the inflation and interest rate fronts explain why the stock market has recovered over the past three months. The rates of change are improving, which is what matters most to markets.

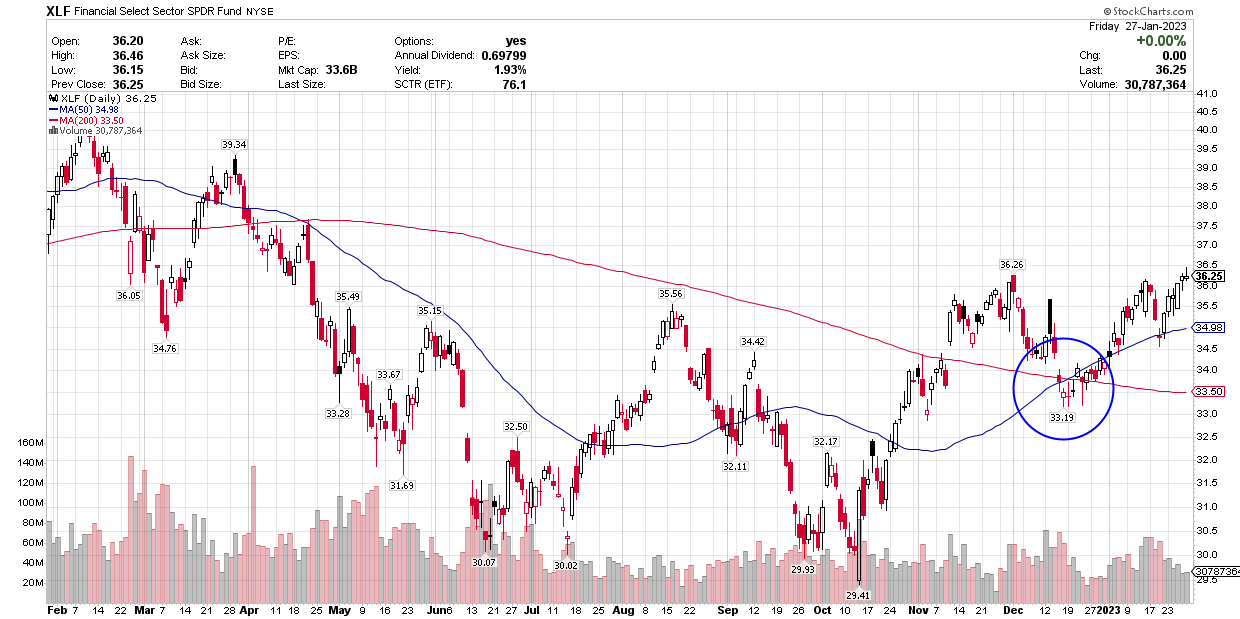

Now we are starting to see extremely positive technical developments in the major market averages that are turning downtrends into new uptrends. The Nasdaq Composite has finally climbed above its 200-day moving average. Market breadth has been exceptionally strong. Last week saw four S&P 500 sectors complete golden crosses, which occur when the 50-day moving average climbs above the 200-day. The fact that these four were financials, industrials, materials, and energy is also a positive, as that kind of leadership is not indicative of a recession being on the horizon.

Stockscharts

While the outlook for the year continues to brighten, we are bound to see an increase in volatility this week with the Fed’s rate decision and the commentary that will follow from Chairman Powell. He will likely attempt to cap further gains in stock prices with hawkish rhetoric, so as to limit a further loosening in financial conditions. Additionally, some short-term technical measures are moving into extended territory, which makes the market ripe for a pullback. Yet a healthy pullback that results in a higher bottom in price is the glue that makes the uptrend stick.

Be the first to comment