niphon

Investment Thesis

Single-family home starts are beginning to decline following the strong last two years of residential demand. Since Builders FirstSource, Inc. (NYSE:BLDR) derives 74% of its revenue from the single-family housing market, the company is expected to report a significant decline in revenue as well as margins in FY23. According to the consensus estimate, BLDR should post a ~30% drop in revenue and a ~65% drop in EPS for FY2023.

From a long-term perspective, we believe the supply-demand dynamics in the housing market are favorable which should act as a tailwind for the overall industry and BLDR. Additionally, the company’s tuck-in acquisition strategy should help the revenue growth. On the margin front, the company continues to execute productivity initiatives such as automation, footprint optimization, and the use of new technologies. Moreover, the synergy benefits from acquisitions should also help margins, looking forward.

Revenue Outlook

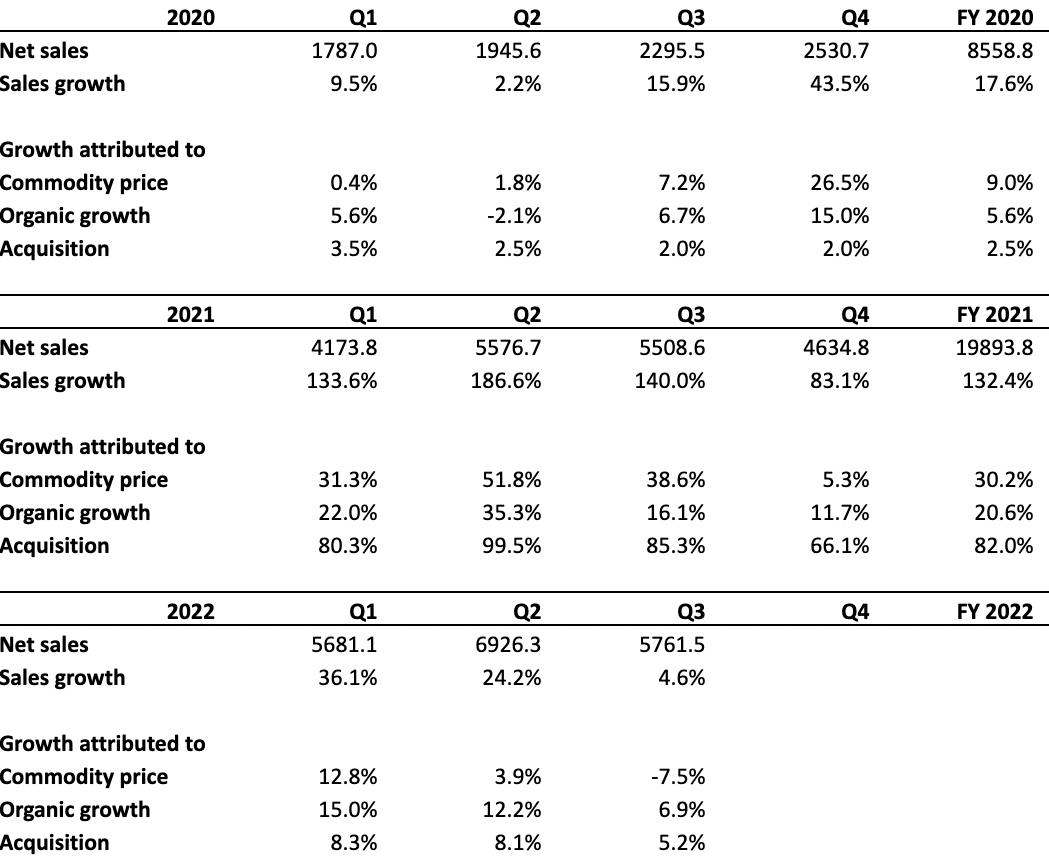

BLDR has seen strong growth over the last couple of years driven by mergers and acquisitions (primarily the BMC merger), commodity price inflation (primarily lumber), and a strong new residential construction market. The company’s revenue grew from $7.2 billion in 2019 to $19.9 billion in 2021 and BLDR is expected to post $22.68 billion in revenue in 2022.

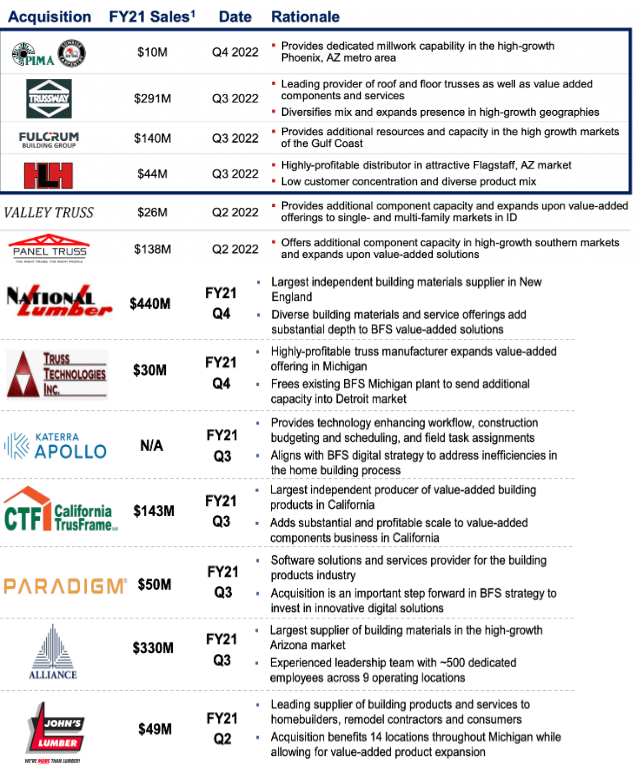

The company has completed the BMC merger and several other small and mid-sized acquisitions in recent years. In January 2021, BLDR announced the completion of its all-stock merger with BMC Stock Holding Inc (BMC) which had net sales of $4.22 billion in 2020. The BMC merger helped BLDR report revenue growth of 132.4% Y/Y in FY21 of which 82% growth was contributed by the BMC merger. In addition, the company had spent a total of $2 billion in acquisitions post-BMC merger. Some of the major acquisitions include National Lumber, Alliance, Trussway, and Fulcrum.

BLDR’s recent acquisitions (Investor Presentations)

The company also benefited from the rise in commodity prices in recent years. As BLDR primarily sells lumber products, fluctuation in lumber prices greatly affects BLDR’s revenues. Due to the sudden rise in demand for lumber in 2020 and 2021, lumber prices (LB1:COM) increased ~4-5 folds from bottom to peak. The increased lumber price benefited the company helping revenue growth. During 2020 the company’s revenue benefitted 9% from commodity price inflation and this number was 30.2% in 2021. However, due to the recent retracement in lumber prices, the company’s revenue was negatively affected by commodity price deflation which resulted in a 7.5% revenue headwind for Q3 2022.

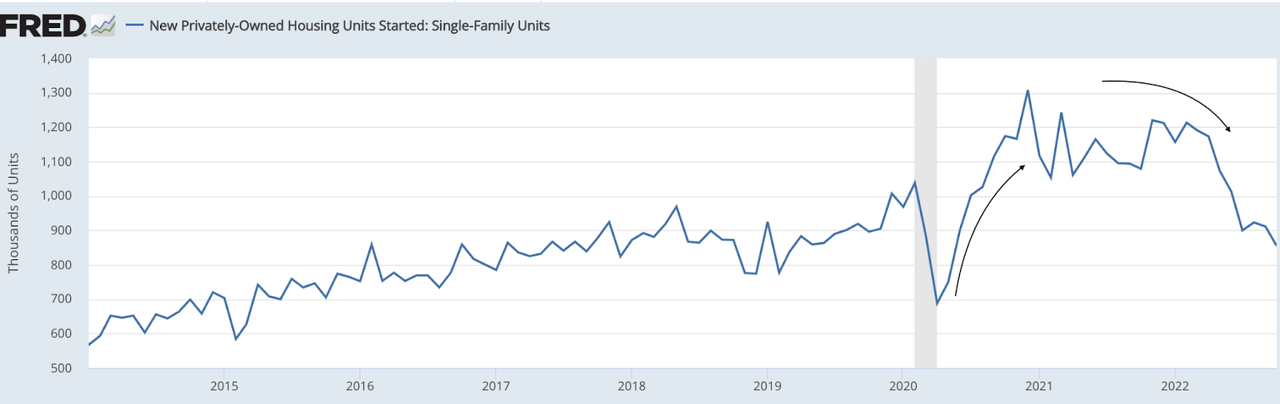

Lastly, the strong residential market which accounts for ~74% of BLDR revenues contributed to core organic revenue growth. Before the pandemic, annualized single-family home starts were in the range of 800-900 thousand in 2019. However, it jumped to a peak at ~1.3 million level in 2021 and remained meaningfully higher than pre-pandemic levels from late 2020 to early 2022. The increased home starts benefited BLDR’s revenue growth. The company reported core organic revenue growth of 5.6% in 2020, 20.6% in 2021, and 11.4% for the first nine months of 2022.

New single-family housing starts (FRED)

In recent months annualized home starts have been plummeting due to a significant and swift rise in the 30Y mortgage rate. The annualized single-family home starts dropped from ~1.21 million in February 2022 to ~828 thousand in November 2022. This resulted in the company’s core organic sales growth slowing down to 6.9% in Q3 2022.

Revenue growth breakup (Company data, GS Analytics research)

Looking forward, the single-family home should continue to decline due to higher mortgage rates and falling consumer confidence, negatively impacting BLDR’s sales. Most public homebuilders are expecting a 30-40% decline in order rate on average indicating a steep correction. Of late, there is some relief from moderating inflation and a slightly less hawkish stance of the Fed, but the near-term outlook for the home building industry and single-family home start still remains very negative.

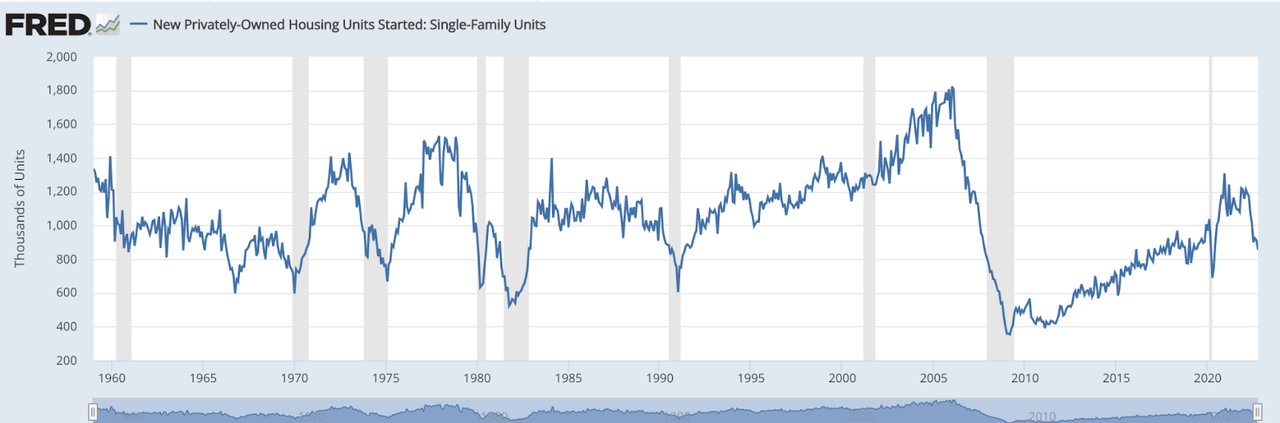

However, in the long run, housing demand should benefit from a structural shortage of homes. Since the great recession of 2008, housing starts have lagged their long-term average for over a decade. Even if we account for the strong last couple of years, from 2008 to now, the annual single-family home starts have averaged ~733 thousand which is much below the long-term average of ~1.01 million single-family starts. This meaningful undersupply over the last decade and a half bodes well for future starts as they need to average above historical levels to compensate for the undersupply. I have discussed this dynamic in detail in a prior article. While the rising interest rates should negatively impact the housing starts for the next couple of years, once inflation is under control and the Federal Reserve starts easing, the demand should quickly rebound.

Annualized single-family home starts (FRED)

Meanwhile, while the market is still slow, management plans to continue its acquisition spree and benefit from a largely fragmented market. For a potential tuck-in acquisition, BLDR searches for entities that can assist the business in gaining market leadership in particular geographic areas, enhancing value-added capability, or providing technological advancement. The company has a target base of 1100 small-mid size entities with $15-$100 million in revenue which in total represents $26 billion in revenue. Management plans to wait patiently for the correct time/valuation for acquiring entities from this large target base. The company plans to spend ~$500 million every year on M&A in the coming years, boosting the company’s inorganic revenue growth.

While no doubt that FY23 is going to be a rough year, I believe we will see a sharp rebound in the market once the Federal Reserve reverses its stance. Additionally, the company plans to use the near-term industry headwinds as an opportunity to acquire several small to medium-sized entities at attractive valuations. This bodes well for long-term growth and shareholder value creation.

Margin Outlook

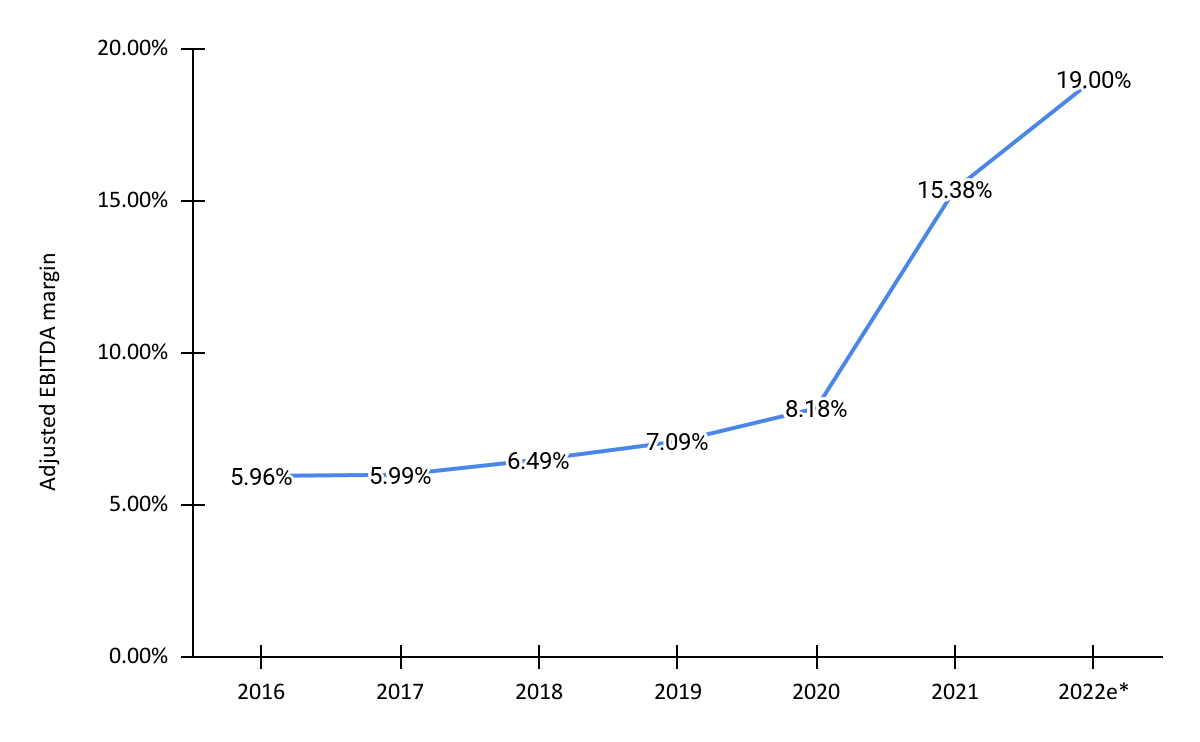

The company saw a significant margin expansion post-Covid due to a favorable demand environment, rising lumber prices, productivity improvements, and synergy benefits from the BMC merger. The company reported 8.2% and 15.4% adjusted EBITDA margins for 2020 and 2021 respectively. For 2022 management expects the company’s adjusted EBITDA to be 19% (at the midpoint).

BLDR Yearly adjusted EBITDA margin (Company data, GS Analytics Research, 2022e EBITDA is midpoint of management guidance)

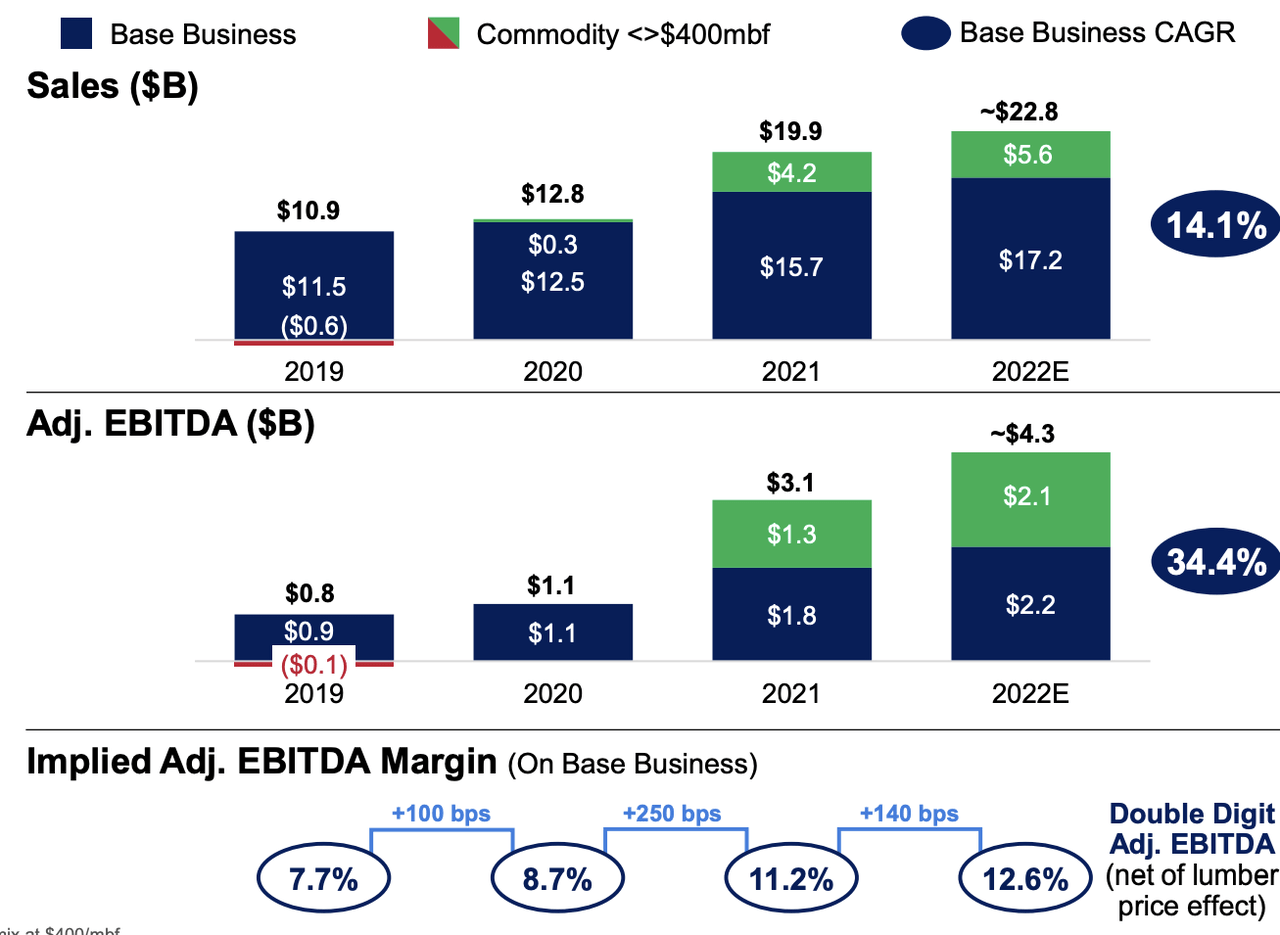

If we look at individual components, lumber price added 420bps to the adjusted EBITDA margin in FY21. On a constant lumber price basis, the company’s adjusted margin for the year would have been 11.2% in FY21. Similarly for FY22 management’s guidance for adjusted EBITDA margin is 19% at the midpoint. However, excluding the lumber price effect, the base business is expected to post 12.6% adjusted EBITDA margins.

Adjusted EBITDA chart net of lumber price. (Investor presentation.)

Excluding lumber prices, the improvement in EBITDA was due to synergy and productivity benefits. After the BMC merger, the management aimed for $140 million in run rate synergy benefits in the next 2-3 years. However, due to more than expected leverage benefits, direct spend benefits and saving from footprint consolidation, the company achieved the target within 12 months. According to the latest update by management, the company is on track to achieve $160 million of run rate synergy benefits by the end of 2022.

Apart from synergy benefits, the company is also focusing on productivity initiatives to drive margin growth. The initiative includes training and development of employees in lean operations. Almost 20% of the staff working for BLDR is lean-certified and the company is targeting a 3% to 5% annual productivity improvement. The company is using automation and robotics in manufacturing to increase productivity. A good example of this is the READY-FRAME solution in which the company uses machines to precisely pre-cut lumber sticks for a house. The use of machines in cutting and sawing results in less waste of lumber and reduces labor costs. So far the company achieved a 20% improvement in board foot (a measurement of the volume of lumber) per hour and increased 13% capacity in Truss assembly. Moreover, Millwork witnessed a 6% improvement in doors per hour and a 16% increase in capacity.

During the Q3 earnings call, management mentioned that in a scenario where single-family home starts drop to 800k, the company will still be able to post a double-digit adjusted EBITDA margin for the base business. Note that the last time single-family home starts were below 800k was in 2017. BLDR at that time had an adjusted EBITDA margin of ~6%. This indicates a ~400 bps improvement in margins vs. 2017 due to structural cost reductions. Moreover, the company expects its productivity and synergy benefit to add 300-500 bps to the adjusted EBITDA margin in the long run. So, while margins will see some hit from volume deleverage next year, I am positive about long-term margin expansion prospects especially once the housing market turns up.

Valuation and Conclusion

The stock is currently trading at 10.10x P/E for the FY23 consensus EPS estimate of $6.29, which is in line with its five-year average forward P/E of 10.10x. While FY23 is going to be a tough year, the company has good long-term revenue and margin opportunity. Additionally, the company’s tuck-in acquisition strategy might work well during a slowdown as valuations of target company contracts. Also, the company has recently boosted its stock repurchase plan by $1 billion which should provide some downside support. I believe the current weakness in the housing market provides a good opportunity to go long BLDR, especially for long-term investors who can wait till the housing market turns back up.

Be the first to comment