Daniel Boczarski/Getty Images Entertainment

The recent spin-off from the mothership Brookfield Corporation (BN) has been a difficult time for shareholders. The combined value of BN and the newly released entity Brookfield Asset Management Ltd. (BAM) have fallen sharply. While in general, analysts on and off Seeking Alpha remain rather bullish on the prospects of Brookfield entities, we have more reserved view. In a later article we will go over why we are not too fond of the flagship fund. But today, we look at two income opportunities from this group that appear attractive and why we prefer one over the other.

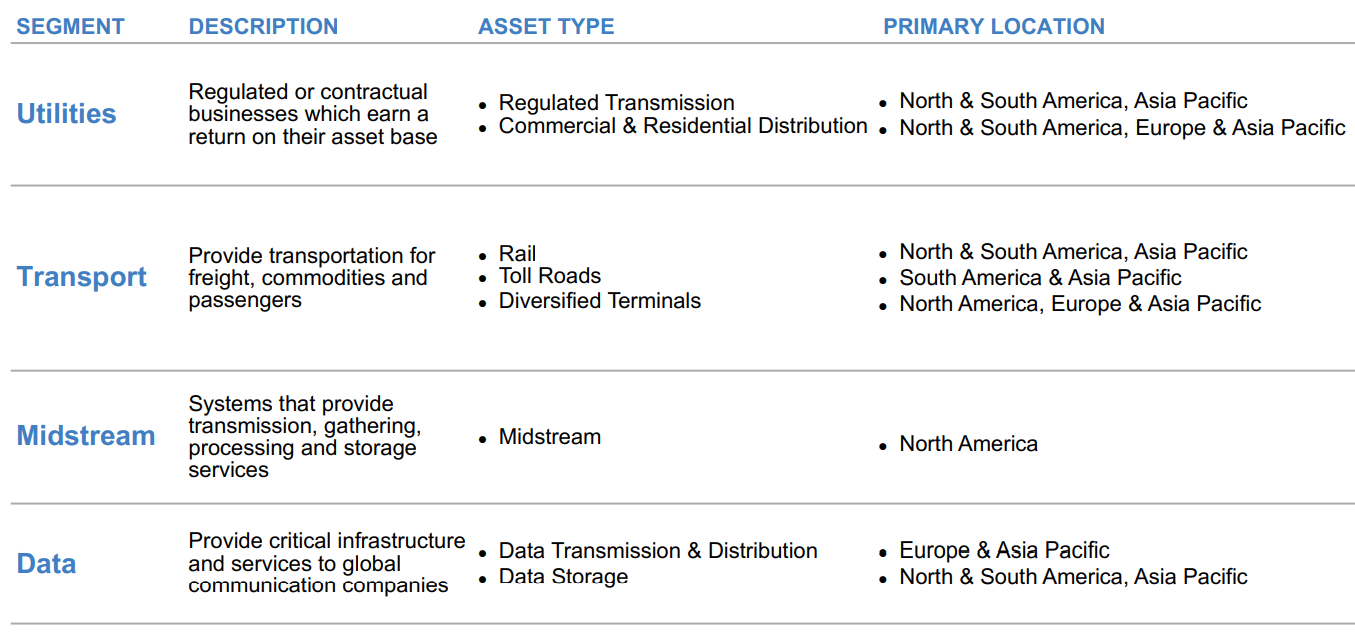

Brookfield Infrastructure Partners L.P. (NYSE:BIP) owns and operates a diversified portfolio of utilities, transportation, energy (midstream) and data infrastructure assets across the Americas, Asia Pacific and Europe.

Q3-2022 Supplemental

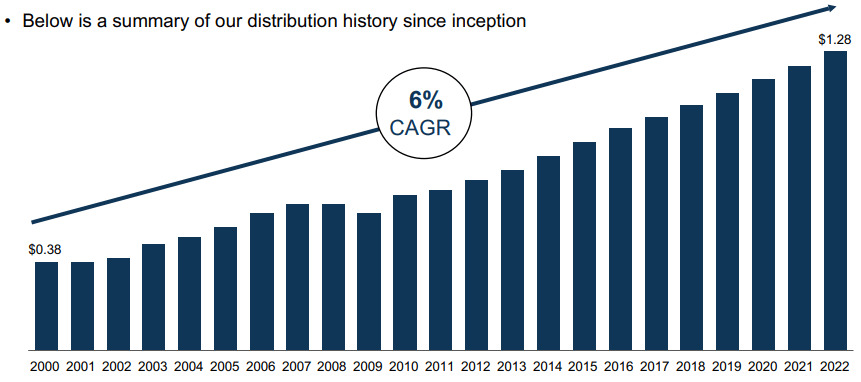

The company has had a steady dividend growth while maintaining a 60%-70% funds from operations or FFO payout.

Q3-2022 Supplemental

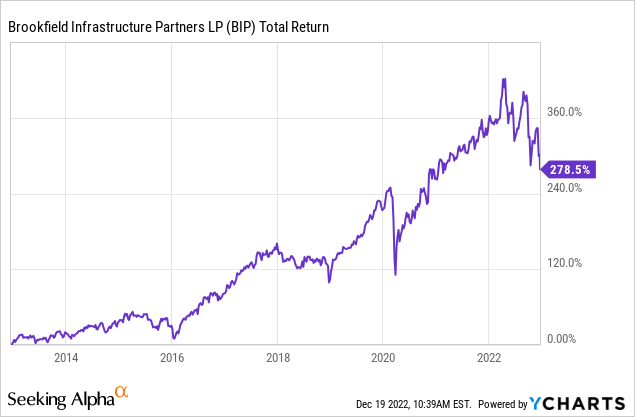

BIP has also done the Brookfield name proud with its total returns over the last decade.

We joined the coverage bandwagon for this company in January 2021 and have written on it a couple of times. Both times we were neutral on the stock and only became long for a short period as a result of Inter Pipeline acquisition. While we were not active buyers of this company, we still felt that the business deserved the premium multiple it traded at. It continued to execute its strategy with admirable efficiency, case in point its acquisition of Inter Pipeline Ltd under our fair value. On the flipside, we thought that BIP would not be able to continue delivering at this pace in the monetary environment we saw on the horizon.

Our neutral rating turned out to be justified for the time frame as all of the legendary returns came prior to that.

The second name we are going to talk about today is Brookfield Renewable Partners L.P. (NYSE:BEP). This one has been on our coverage list since April 2019. BEP owns and operates hydroelectric, wind, solar and storage facilities in the Americas, Asia Pacific and Europe.

Q3-2022 Supplemental

Unlike BIP, this business has a high dividend payout ratio that is somewhat mitigated by its investment grade balance sheet and predominantly long term, non-recourse debt. Riding on the renewable wave in the last couple of years, it has yielded under 5%. However, that has slowly started inching back up to the levels it has been for the bulk of the last decade i.e. over 5%. Like BIP, albeit to a lesser extent, BEP also boasts of a consistent dividend increase over the 10 year time frame.

Q3-2022 Supplemental

We have recommended staying on the sidelines with the common stock during the course of most of our coverage, never having found a compelling direct buy point.

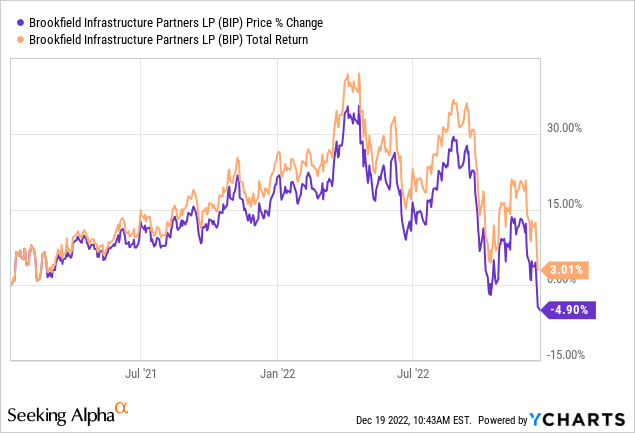

It has rewarded its investors handsomely since 2020, even though it has lost some ground since its highs. Despite staying out, we too had a couple of things going for us, which was nice. Firstly, we issued our sole sell rating in April 2022, warning our readers to take their profits. The stock is down 27% since then. Secondly, while we stayed out from an outright purchase of the common stock, we did trade covered calls on this. Those handily outperformed a buy and hold method.

In both BIP and BEP’s case, we have touted the preferred stock quite a few times in our writings. Today, we once again visit one of each and provide our preference.

1 ) Brookfield Infrastructure Partners L.P. 5.125 CL A PFD13 (NYSE:BIP.PA)

Brookfield entities have a ton of preferred shares listed on TSX, but there are far fewer of them this side of the border. This fixed rate issue is NYSE traded and currently has a stripped yield of 7.88% at a price of $16.21. These are perpetual unless redeemed at par by BIP on or after October 15, 2025. They also have the option to redeem it for $25.50 in case of a ratings event or at $25 in case of a tax law change, details of which can be consumed from the prospectus.

BIP Preferred Instruments

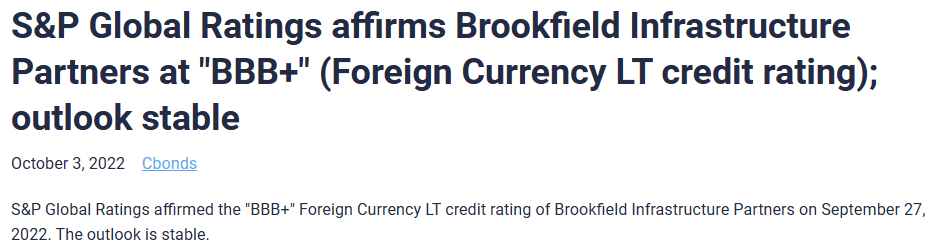

The corporation has an investment grade rating from S&P.

cbonds.com

The Preferred shares are also rated investment grade, although as expected, are two notches lower.

Quantum Online

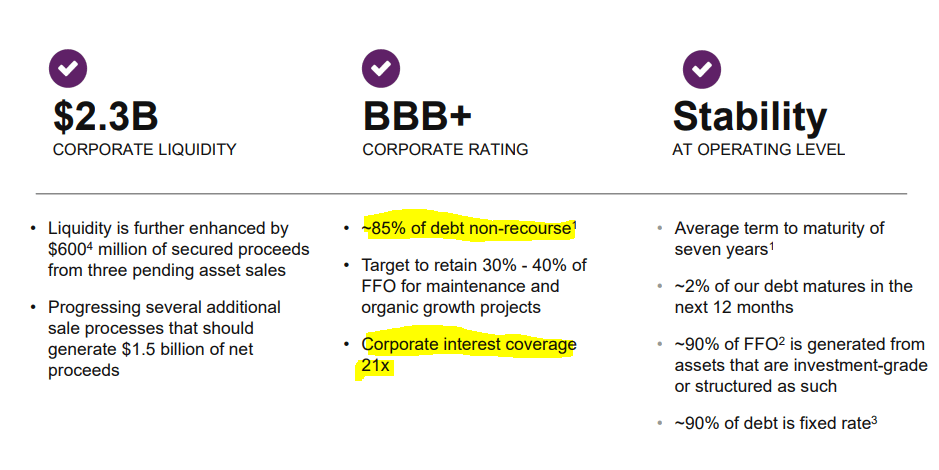

The key reason to love this issue, besides the investment grade nature, is the relatively tiny part it forms for the capital structure. At $1.283 billion par value, the shares are less than 5% of the total equity market cap outstanding. Equally importantly, they consume about 10% of the expected FFO for the company. BIP does run a moderately heavy debt structure, but 85% of that is at the asset level and corporate interest coverage is fantastic.

BIP Presentation

To us, this is one of the safest issues in the preferred space.

2) Brookfield Renewable Partners L.P. 5.25% PFD CL A (NYSE:BEP.PA)

This fixed rate issue is NYSE traded and currently has a stripped yield of 6.87% at a price of $19.11. These are perpetual unless redeemed at par by BEP on or after March 31, 2025. Just like BIP, BEP also has the option to redeem it for $25.50 in case of a ratings event or at $25 in case of a tax law change, details of which can be read in the prospectus.

BEP Preferred Instruments

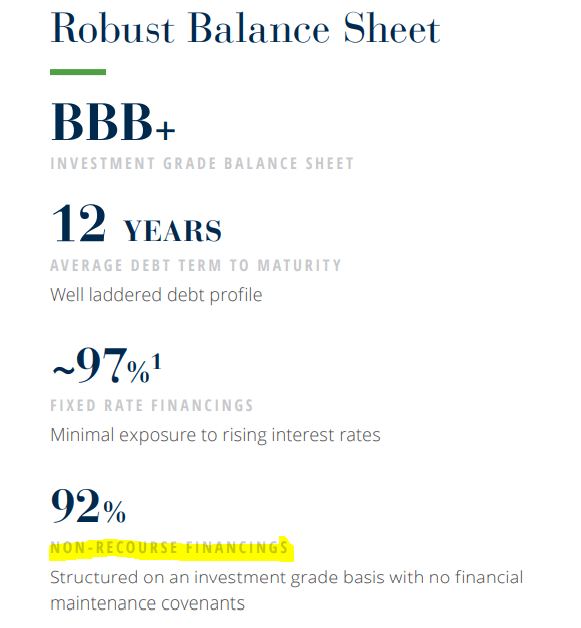

Noted in the Q3-2022 presentation, BEP is rated BBB+ by S&P, while the preferred issue comes in at BBB-.

Quantum Online

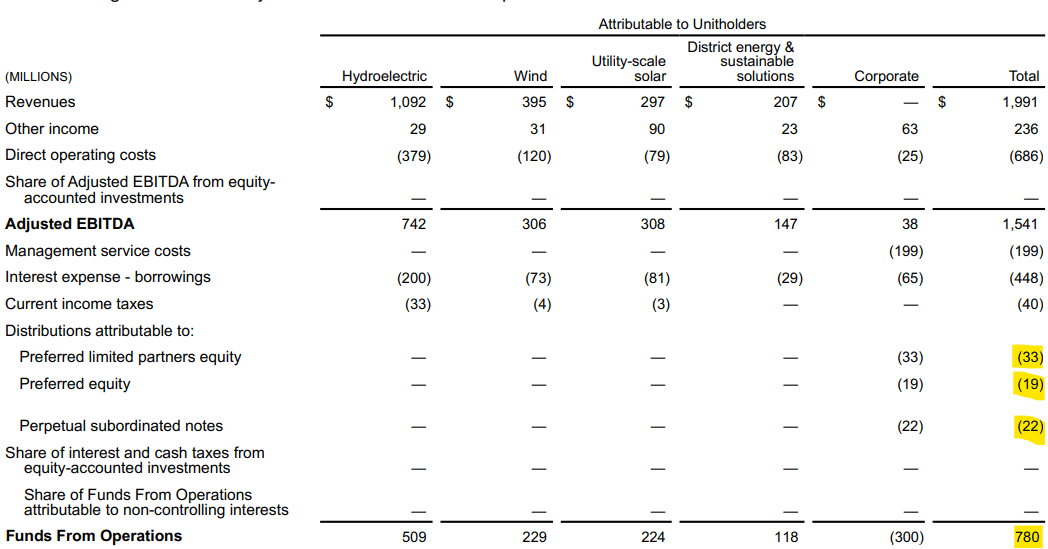

For the nine months ended September 30, BEP had more than 10X coverage for its preferred distributions.

Q3-2022 Supplemental

Just like BIP, BEP runs a moderately heavy debt structure but keeps its dangers limited by focusing on debt at the asset level.

BEP Presentation

Verdict

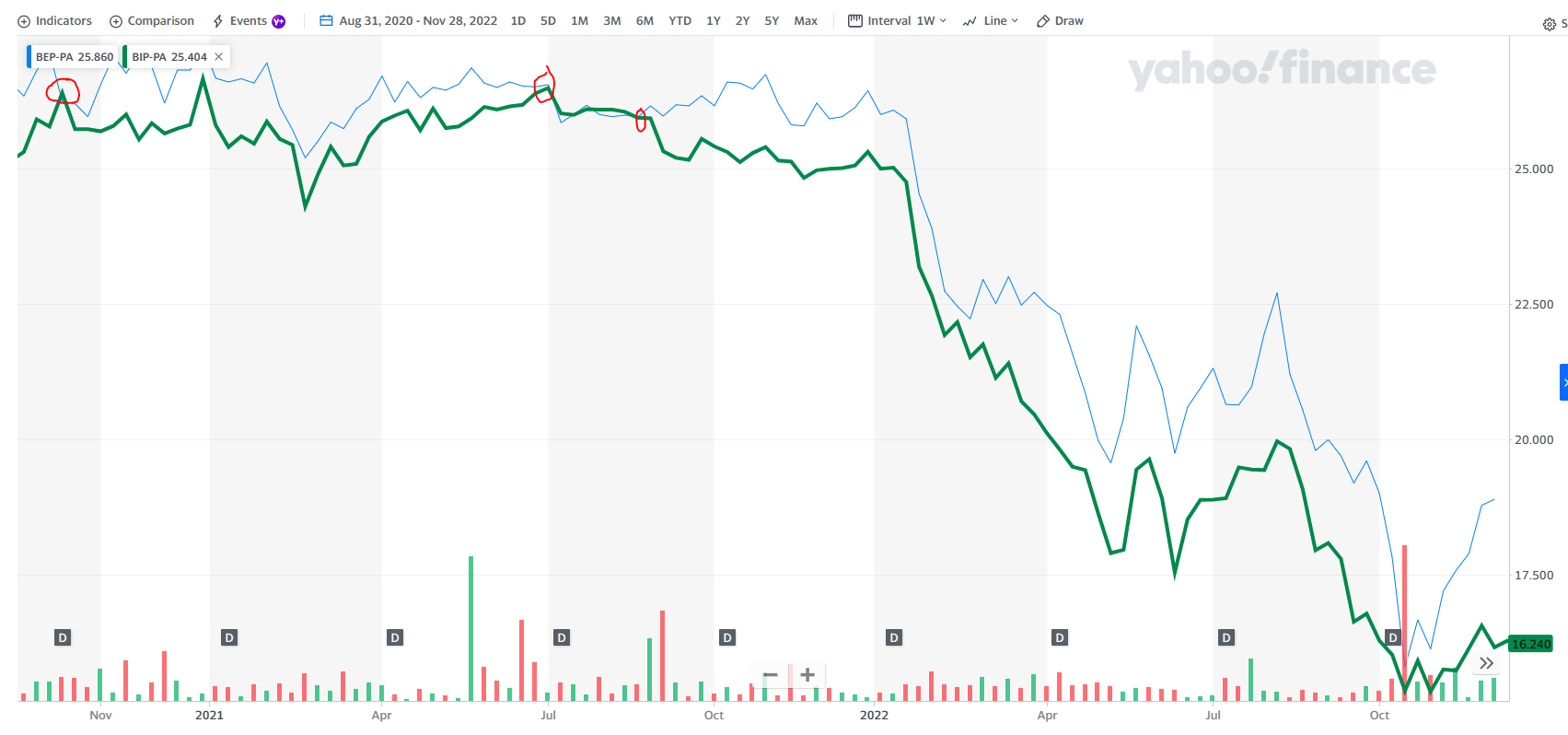

Both sets of preferred shares offer high current income with little risk. They also offer a far higher level of income than what BAM is going to dole out. Both come with relatively non-complicated K-1s and investors should read the information of the company websites (BEP Tax and BIP Tax). While they do sound like the MLP type stocks, they are quite different as both are based in Bermuda and there is a lack of UBTI. Both sets of dividends also have historically been qualified, although there can be no guarantee that this continues. For our money BIP is clearly the superior organization, with overall less leverage and a superior, more diversified business model. On top of that. BIP.PA offers the better yield. That is a clear preference for us. These shares have traded at the same price in the past as well and we don’t see why that would not happen again once people realize the relative value.

Yahoo Finance

That gives us a better upside for BIP.PA as well.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment