themotioncloud/iStock via Getty Images

When we started coverage of Broadridge Financial (NYSE:BR), we said that while we liked the company we still considered it a little bit expensive. Since then shares have lost approximately 10%, while the market is down only about 1%. We now believe shares to be trading very close to fair value, but we still have some concerns.

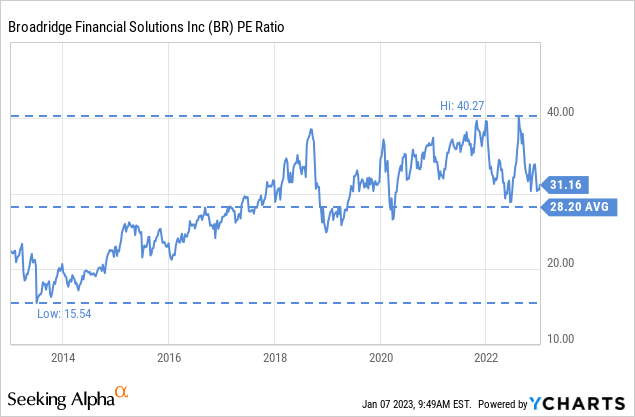

Seeking Alpha

As a reminder, Broadridge Financial Solutions is a market leader in the financial services industry, providing investor communications, proxy voting, and other services to banks, broker-dealers, mutual funds, and other financial institutions. In other words, it helps to power the critical infrastructure behind investing, governance, and communications

In particular, Broadridge has been the dominant proxy service provider for broker-dealers for decades, and this business is its crown jewel, as a disproportionate amount of the company’s earnings comes from this segment. Another segment that is also becoming increasingly important is its global technology and operations segment which generates ~30% of its fee revenue and profit, it provides securities processing solutions.

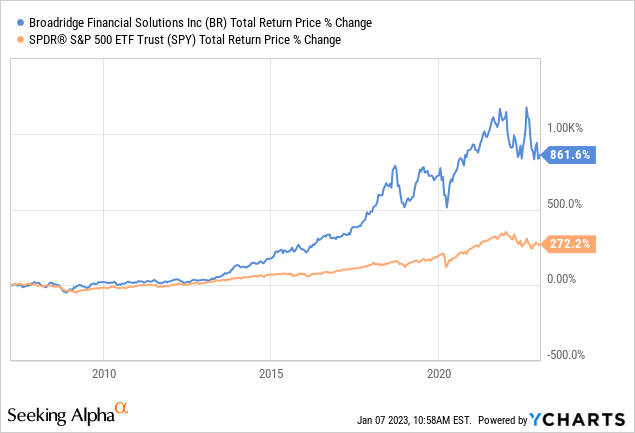

Since the company was spun-off from Automatic Data Processing (ADP) in March 2007, it has outperformed the S&P 500 index (SPY) by a wide margin.

Broadridge reported first quarter results with 9% recurring revenue growth in constant currency, and reaffirmed its fiscal year 2023 guidance. This guidance included 6% to 9% recurring revenue growth in constant currency and 7% to 11% Adjusted EPS growth.

Competitive Moat

One of the main reasons investors should consider Broadridge Financial for an investment is its competitive moat. We believe the company benefits from high switching costs for its customers, as its expensive and time-consuming for them to switch to an alternative service. Additionally, Broadridge has a large and established customer base, and a long track record of successful relationships, which makes it difficult for new entrants to compete with the company.

We believe the company also benefits from its scale, which gives it operating leverage and allows the company to operate profitably at price points that small competitors are probably unlikely to be able to match without incurring losses.

Financials

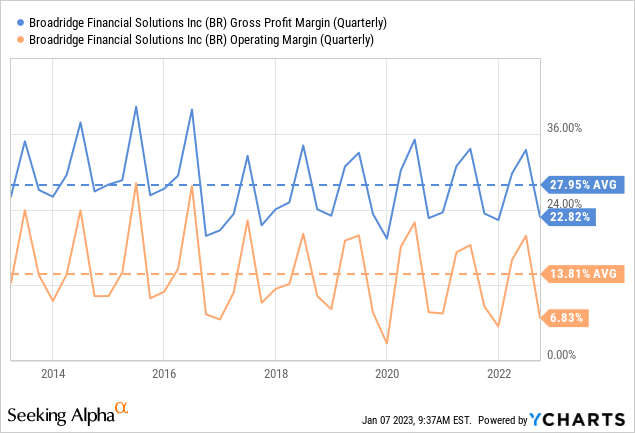

The company is quite seasonal, making most of its profits during proxy season, which coincides with the Broadridge’s fiscal third and fourth quarters. Its operating margin is quite healthy averaging ~13%, which reflects the company’s competitive moat.

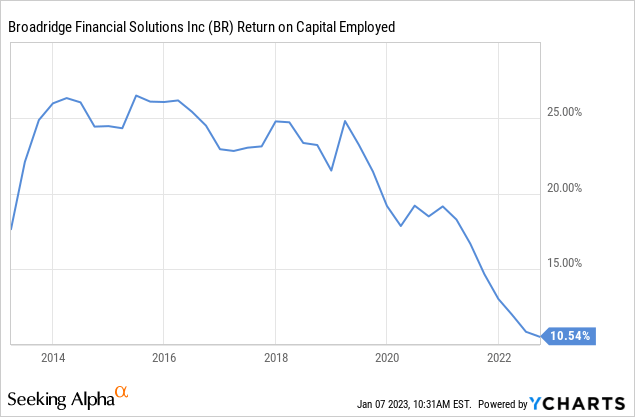

The company, however, is seeing its return on capital employed trend down. This is concerning as it means retained earnings won’t be able to generate as much value as they used to previously.

Growth

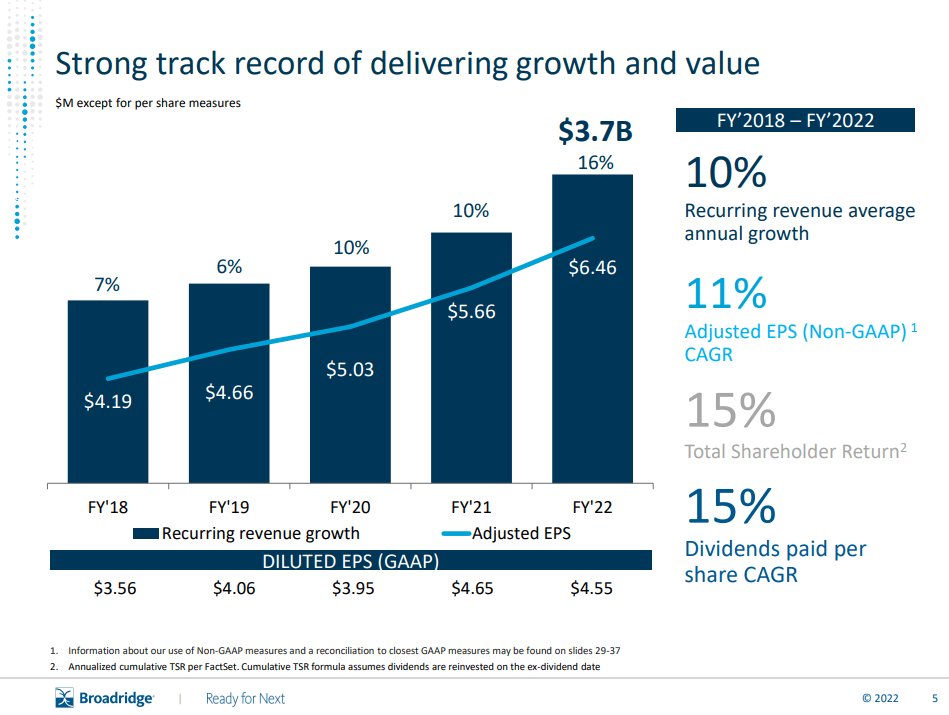

Broadridge has three strong growing franchises with $3.7 billion in combined recurring revenue. Recurring revenue has been growing on average at a ~10% rate, and earnings per share slightly faster at ~11%. The company has been complementing organic growth with some strategic acquisitions, such as Itiviti, which helped extend Broadridge’s capital markets franchise. The company is also driving growth through innovations, for example, it is launching AI-powered fixed income trading platform.

Broadridge Financial Investor Presentation

Balance Sheet

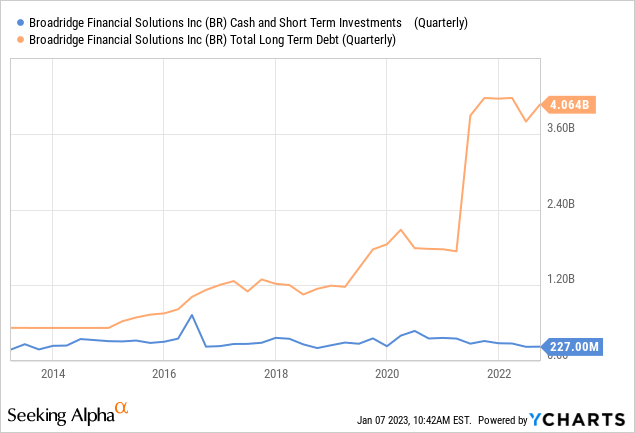

The acquisitions have not been cheap, however, and this has resulted in a significant increase in net debt. As can be seen below, the company now carries about four billion dollars in debt, while holding only ~$227 million in cash and short-term investments.

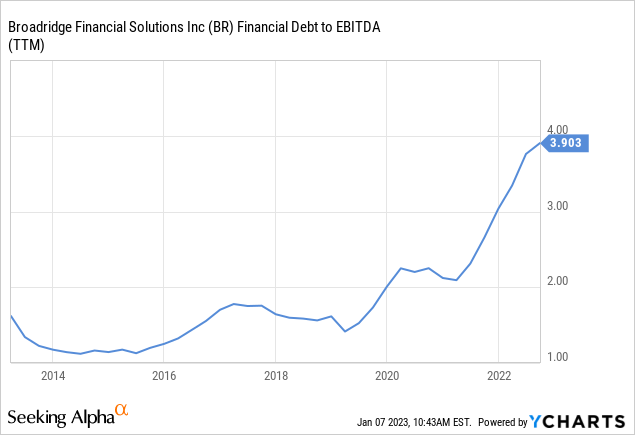

This has resulted in increased leverage, with financial debt to EBITDA now reaching ~3.9x. This is higher than what we consider to be reasonable for the company, and hope they start deleveraging the balance sheet soon.

Valuation

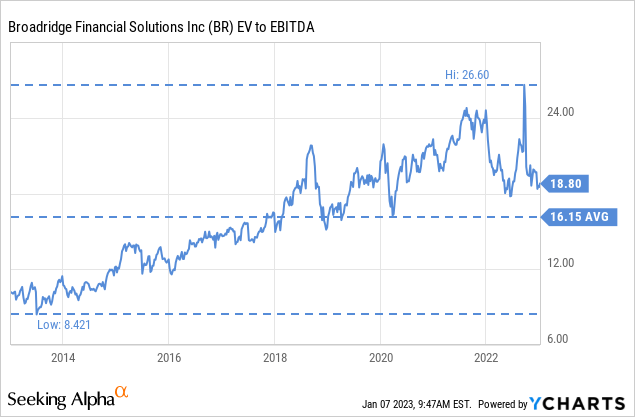

The valuation ten years ago was arguably too low, and it is probably why the shares have performed so well since then. Given the company’s competitive advantages we do believe it deserves to trade at a premium multiple. We therefore consider the current EV/EBITDA multiple around 18.8x to be reasonable, but far from a bargain.

Similarly with the p/e ratio at ~31x, we believe it to be justified given the low double digits earnings growth rate, and the company’s competitive moat, but do not consider it cheap.

Using analyst earnings per share estimates for the next three years and ~8% earnings growth until 2033, we estimate the fair value for the shares at ~$130. This is very close to the current price at which shares are trading, leading us to believe that shares are fairly valued.

| EPS | Discounted @ 10% | |

| FY 23E | 6.94 | 6.31 |

| FY 24E | 7.54 | 5.74 |

| FY 25E | 8.32 | 5.66 |

| FY 26E | 8.99 | 5.68 |

| FY 27E | 9.70 | 5.58 |

| FY 28E | 10.48 | 5.48 |

| FY 29E | 11.32 | 5.38 |

| FY 30E | 12.22 | 5.28 |

| FY 31E | 13.20 | 5.18 |

| FY 32E | 14.26 | 5.09 |

| FY 33E | 15.40 | 5.00 |

| Terminal Value @ 3% terminal growth | 220.00 | 70.10 |

| NPV | $130.48 |

Risks

As we discussed above, there are a few things we find concerning. First, the returns on invested capital have been trending down. Second, the company has been increasing its financial leverage. Third, the shares appear fully valued, meaning that there is not much in terms of margin of safety in the share price.

Conclusion

Broadridge Financial has a history of outperforming the market, and we certainly believe that it is a company with strong competitive advantages. Shares are now trading very close to our estimated fair value, but we do have some concerns, including the deteriorating returns on invested capital, and the increasing debt levels. Overall we continue to rate shares a ‘Hold’ until there is some margin of safety in the valuation.

Be the first to comment