Leon Neal

Introduction

Following a bumpy ride during 2020 and 2021, the middle of 2022 saw BP (NYSE:BP) back on track and as my previous article discussed, I was expecting more big dividend increases. Much to my enjoyment as a shareholder, this was proven apt with their recently released fourth quarter of 2022 enclosed with a gift, namely a surprise big dividend increase of around 10% that came only half a year after the last one. When looking ahead into 2023 and beyond, I now feel that we as shareholders are on the road to a $50+ share price as management unlocks the hidden value of their massive free cash flow.

Coverage Summary & Ratings

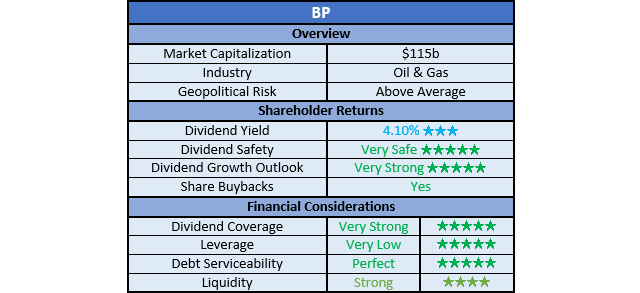

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

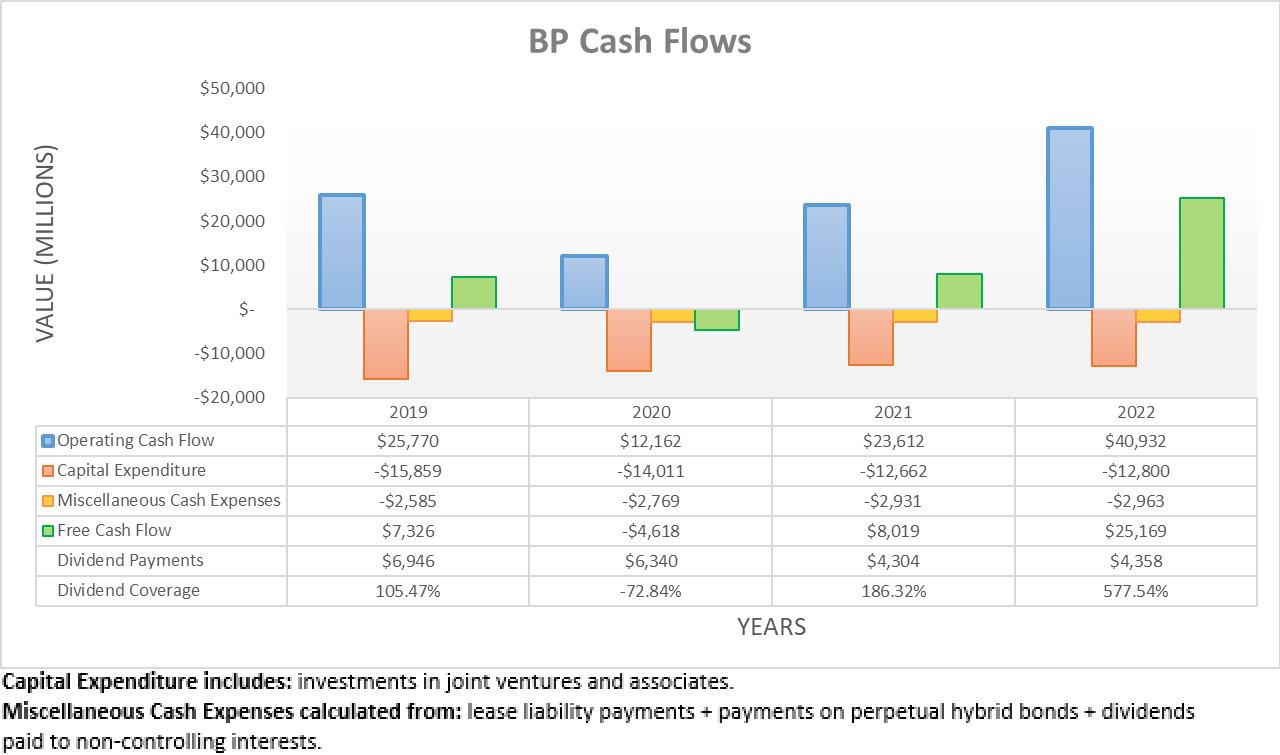

The booming oil and gas prices seen during the first half of 2022 as Russia invaded Ukraine softened during the second half as economic concerns weighed heavily, although their cash flow performance still posted massive results. To this point, their operating cash flow recorded a result of $40.932b for the full year that is slightly more than double what they generated during the first half, which was $19.073b. Naturally, it was also far above their previous result of $23.612b during 2021, despite being weighed down by material working capital movements.

Author

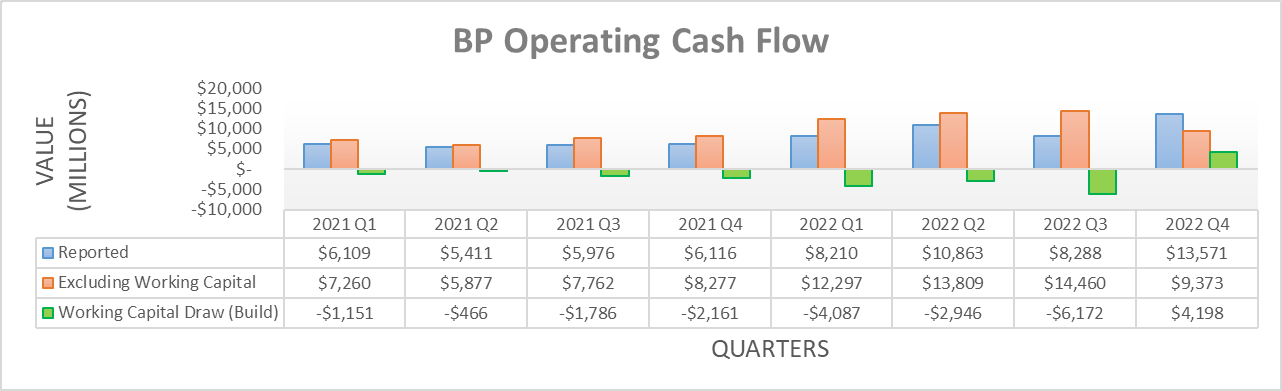

When looking at their quarterly operating cash flow, the fourth quarter of 2022 saw a significant boost from a $4.198b working capital draw. That said, it pales in comparison to their builds during the preceding three quarters, which totaled a massive $13.205b and thus, their recent draw merely sees the full year net out to a massive build of $9.007b. When looking back at 2021, it also saw a sizeable build of $5.564b and thus, it means this sizeable build during 2022 was not merely recouping a draw from the previous year. Whilst positive, their very strong cash flow performance was not too surprising given the prevailing operating conditions and as always, their outlook for the year ahead is more important.

BP Fourth Quarter Of 2022 Results Presentation

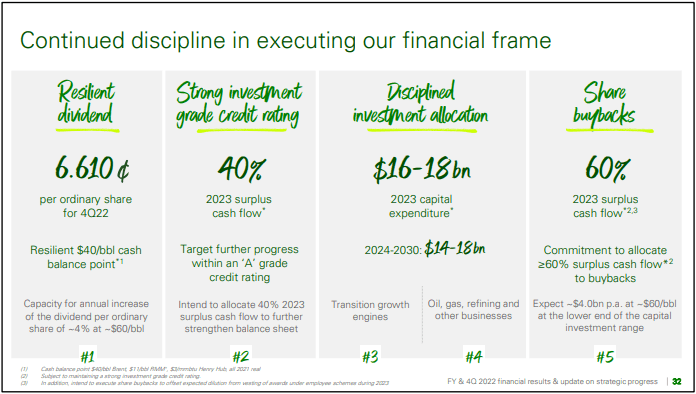

There are several parts to their guidance for 2023 and accompanying capital allocation strategy with the first being their dividends, which were increased by circa 10%, only half a year since they were already increased 10%. They also plan to keep capital expenditure reasonable at between $16b and $18b, thereby taking a middle-of-the-road approach between investing for the medium to long-term whilst also generating massive free cash flow for shareholders in the short-term.

Despite this positive backdrop, due to the inherent volatility of oil and gas prices, it is impossible to perfectly ascertain their operating cash flow and thus free cash flow. That said, the global energy shortage following the sanctions on Russia and the reopening of China should help support prices and avoid a severe downturn, despite the United States and other Western nations likely to see weak economic conditions.

After their surprise big dividend increase, their share price rallied circa 10% in the following days as of the time of writing because few things grab the attention of investors like higher dividends. Now that a $40 share price is almost afoot, it would leave investors wondering if there is more to come and perhaps, can their share price realistically each $50+.

In my eyes, the answer resides within the remainder of their guidance and capital allocation strategy for 2023. It can be seen they plan to divert 40% of their cash flow surplus, also known as free cash flow after dividend payments towards deleveraging, whilst the remaining 60% is returned to shareholders via share buybacks. Within their guidance for this latter part, they forecast these share buybacks to be circa $4b per annum when Brent oil is trading for merely $60 per barrel, which thereby implies a surplus cash flow of $6.67b. When 2022 ended, their ADR equivalent outstanding share count was 3,029,803,000, which means their ADR equivalent quarterly dividends of $0.3966 per share should cost $4.806b per annum.

Once combining these variables, it indicates massive free cash flow guidance for 2023 of circa $11.5b when Brent oil is trading at merely $60 per barrel and given their current market capitalization of approximately $115b, this sees a very high yield of circa 10% that offers very desirable value. To circle back to the $50 share price question, it would see their market capitalization at approximately $151b and thus by extension, it would still see a high free cash flow yield of circa 7.50% that still offers desirable value.

In theory, this should easily facilitate their share price climbing steadily to $50+ in the coming weeks and months but alas, I suspect one problem holding this back is the lack of surface-level appeal at such a share price. Whilst their moderate dividend yield of circa 4% on their present $38 share price can appeal to investors, a $50 share price would see this drop to only circa 3%, which does not carry much appeal for a company that is frequently sought as a source of income. This may sound downbeat but thankfully as subsequently discussed, this hidden value of their massive free cash flow can be unlocked progressively as they deleverage, which in turn creates scope to see their share price steadily climb towards $50+.

Author

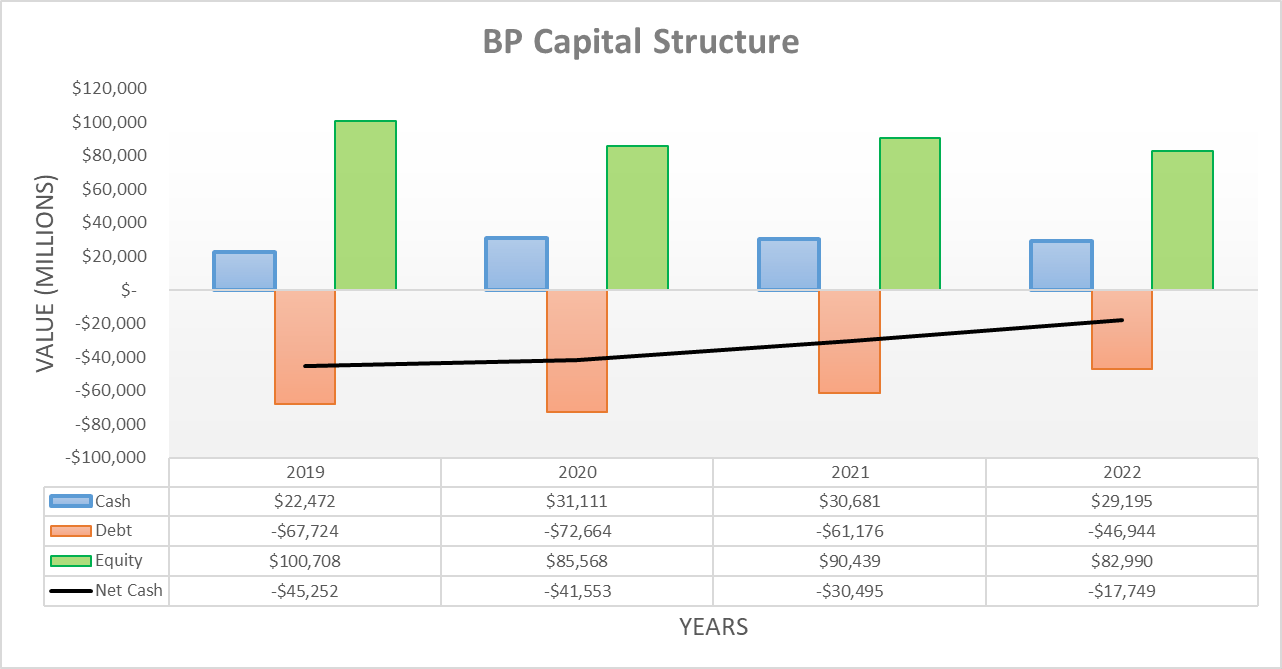

Since conducting the previous analysis, the second half of 2022 saw their net debt continue dropping even lower to now land at $17.749b, which is down almost exactly $2b since their previous level of $19.758b. If also including their leases as practiced by management, their net debt dropped to $21.422b versus its previous level of $22.816b across these same two points time. Whilst a less significant decrease, it nevertheless is impressive to see lower net debt considering this same period of time also saw a further $6.106b of share buybacks on top of their dividend payments of $2.228b.

Going forwards into 2023, they should slice away another few billion dollars of net debt given their aforementioned capital allocation strategy, especially if they can recover more latent cash from their working capital build during 2022. That said, the extent remains unpredictable because it depends upon inherently volatile oil and gas prices but at least the direction is quantifiable.

Author

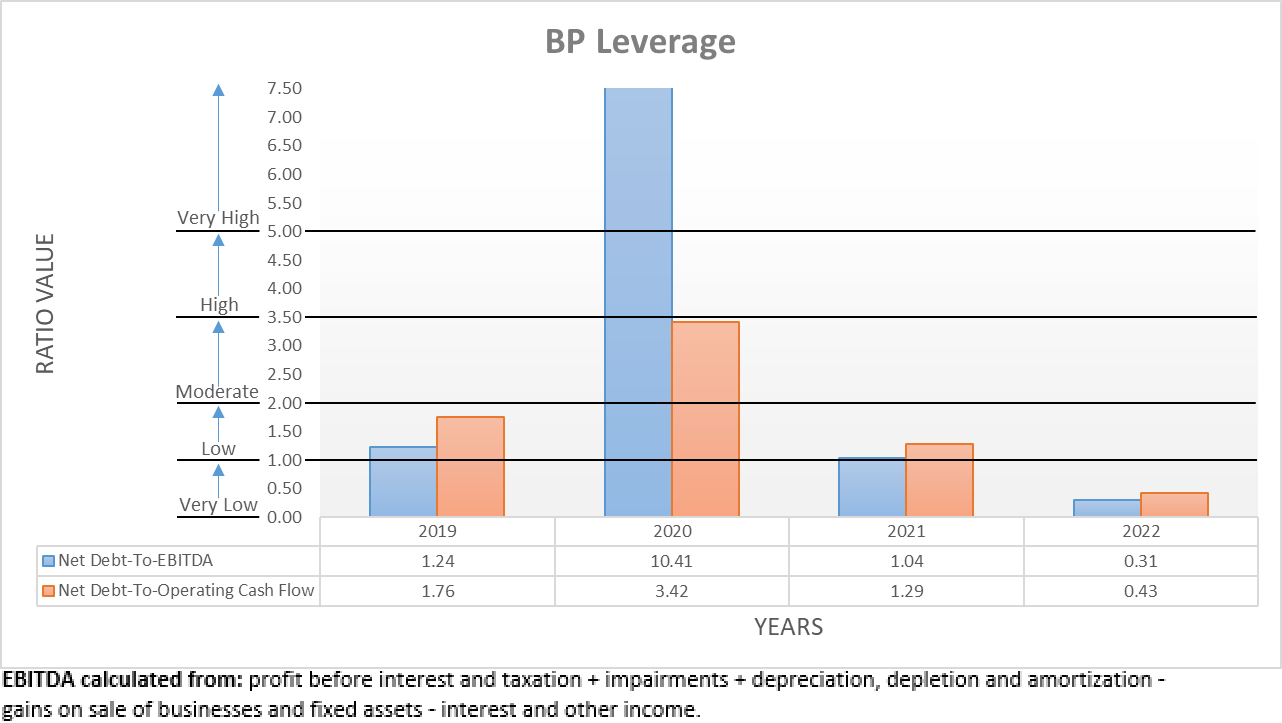

To absolutely zero surprise the second half of 2022 once again saw their leverage remaining within the very low territory, as both their respective net debt-to-EBITDA and net debt-to-operating cash flow of 0.31 and 0.43 remained beneath the applicable threshold of 1.00. These are almost identical to their previous respective results of 0.34 and 0.38 following the first half, as their lower net debt offset their slightly lower financial performance from oil and gas prices softening.

Thanks to their far lower net debt of $17.749b that is a mere fraction of the $45.252b at the end of 2019, this significantly lowers their downside risks should oil and gas prices plunge because it limits the extent their leverage can possibly increase, thereby limiting risks. Even more importantly, it also opens the door to unlock the hidden value of their massive free cash flow, as alluded to earlier. The lower their net debt goes, it lowers the requirement and thus the reward of deleveraging.

Whilst management is intent on deleveraging further in 2023, I expect this to progressively wane in the coming years and thus as a result, they begin increasing shareholder returns higher as a relative percentage of their free cash flow, which should help push their share price towards $50+. Even if these only come about via larger share buybacks, the additional buying support will help push their share price higher, plus create even more dividend growth due to the even lower outstanding share count. This second aspect would work in tandem with the first to help improve the aforementioned present lack of appeal at a $50 share price as they unlock the hidden value of their massive free cash flow.

This theory is all well and good but without action from management, it would be nothing more than a concept. Thankfully, their surprise big dividend increase shows a clear willingness to translate their lower outstanding share count into tangible rewards that appeal to shareholders, thereby making it much more likely to see their share price fulfill its potential.

Author

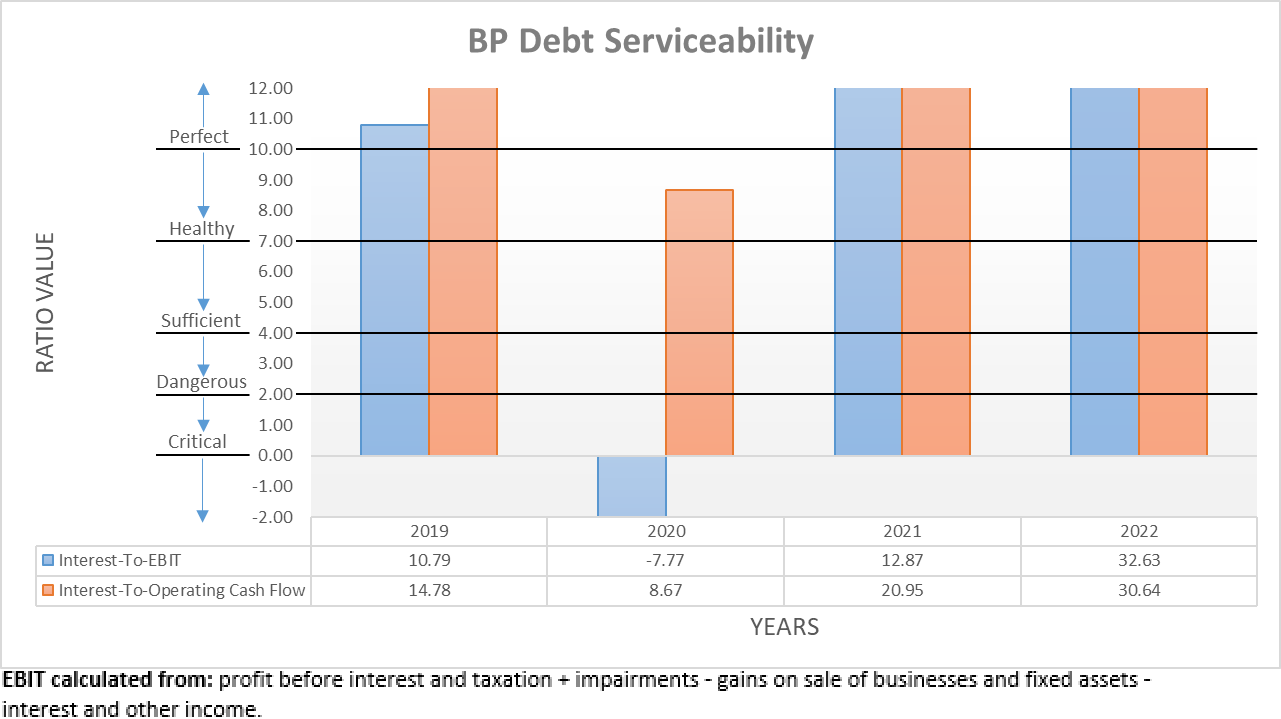

Even though the rapidly tightening monetary policy that dominated the news in 2022 proved a headwind, their booming financial performance and far lower net debt helped offset the pain. As a result, their interest coverage was once again perfect with results of 32.63 and 30.64 when compared against their EBIT and operating cash flow, respectively.

Once interest rates stabilize and possibly head lower, it should allow their far lower net debt to be translated into lower interest expense, thereby boosting their free cash flow and further helping their upside potential in the future, likely in 2024 and beyond. Throughout 2022 their interest expense was $1.336b and thus, it carries room to further enhance their already massive free cash flow in future years.

Author

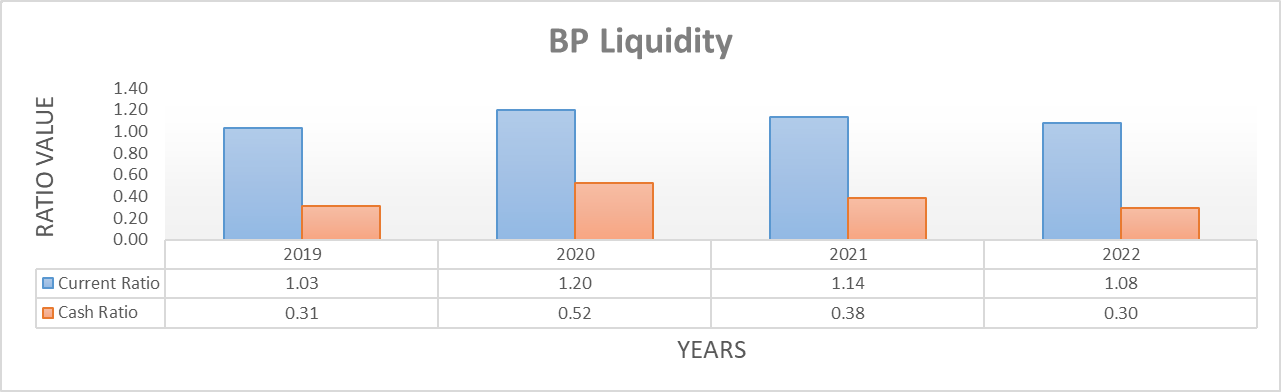

When it comes to their liquidity, it once again remains strong following the second half of 2022 with a current ratio of 1.08 accompanied by a cash ratio of 0.30. Similar to their leverage, these remain very close to their previous respective results of 1.12 and 0.31 following the first half. This does not necessarily help ensure their upside potential in the same manner as deleveraging, although it still ensures they can navigate anything in the future, which in turns helps reduce downside risks. Since they are a very large company with easy access to debt markets, there are no reasons to expect this to change nor to be worried about their future debt maturities, regardless of where monetary policy heads.

Conclusion

It is now quite easy to imagine their share price hitting $40 in the short-term, especially following the surge of enthusiasm for their shares after their surprise big dividend increase. More importantly, I now feel that we as shareholders are on the road to a $50+ share price as they generate massive free cash flow and management shows a clear willingness to unlock this value and boost the appeal of their shares with big dividend increases and as their net debt continues dropping, these should only get progressively better. Since their guidance assumes Brent oil prices of merely $60 per barrel, which is far less than current levels and what many analysts expect in the coming years, it creates a margin of safety and thus, I believe that maintaining my strong buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from BP’s Quarterly Reports, all calculated figures were performed by the author.

Be the first to comment