Funtap

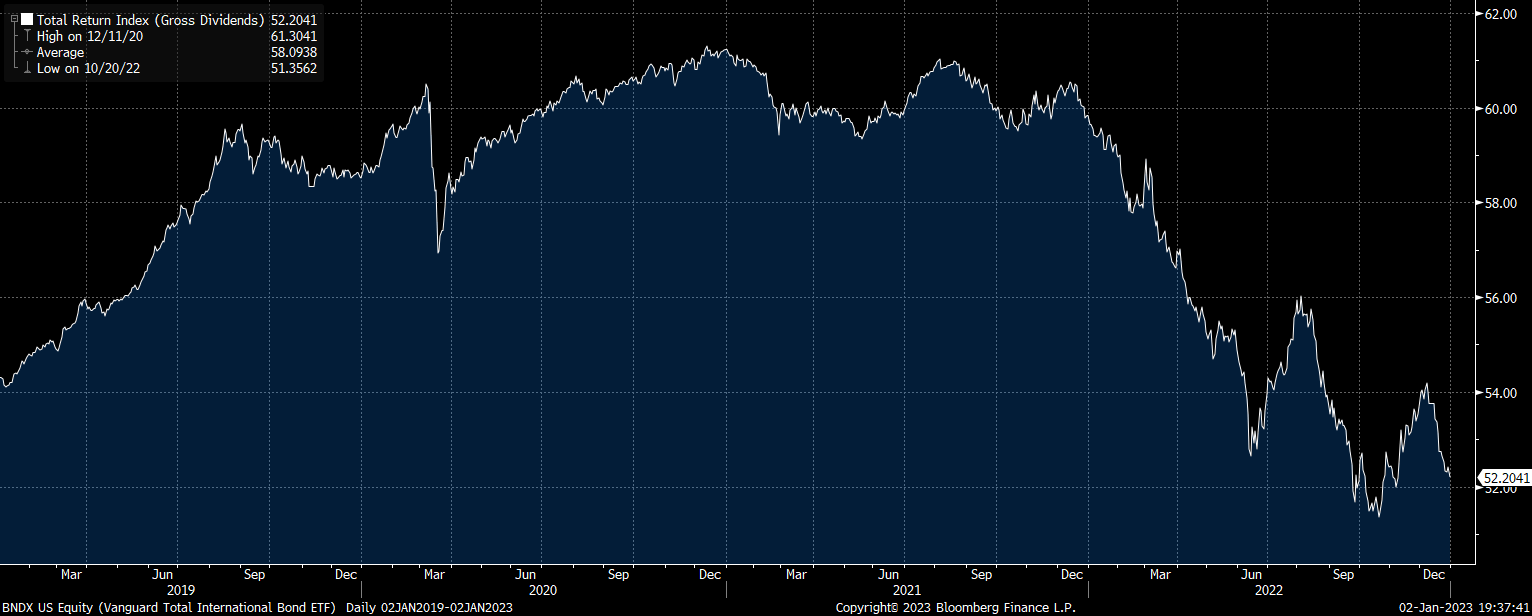

The Vanguard Total International Bond ETF (NASDAQ:BNDX) suffered heavy losses in 2022, declining by 12.5% in total return terms, which is significant for a high quality, relatively low duration bond fund. These losses are a direct consequence of the incredibly low yields on international developed market bonds that prevailed at the end of 2021. While the yield on the BNDX has risen significantly over the past year, it remains too low to justify a long position in the context of the inflation outlook. Even if yields fall over the coming years as central banks are forced to keep borrowing costs low amid elevated debt levels, this is likely to put upside pressure on inflation, further undermining long-term real returns.

BNDX Total Return (Bloomberg)

The BNDX ETF

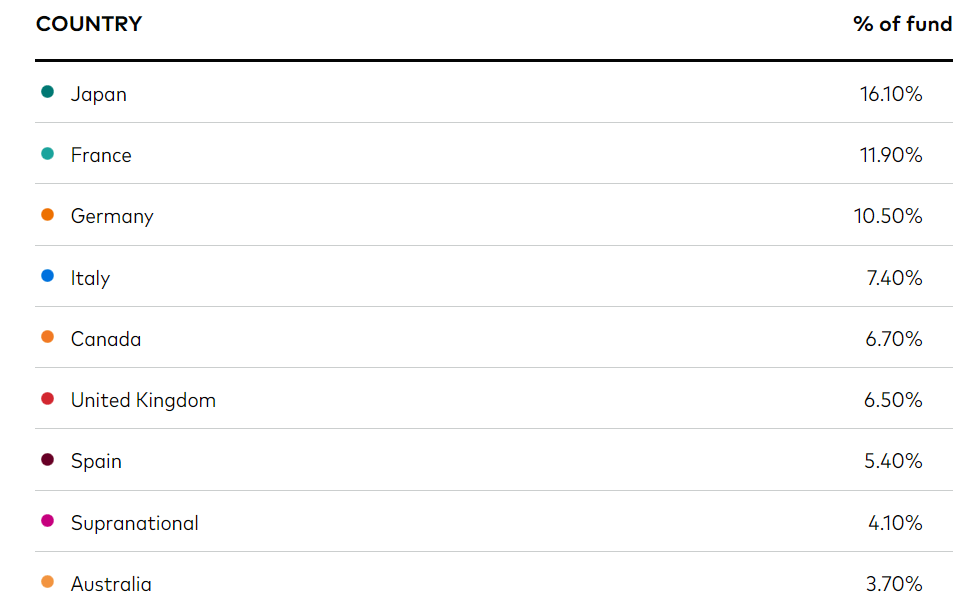

The BNDX seeks to track the performance of the Bloomberg Global Aggregate ex-USD Float Adjusted RIC Capped Index (USD Hedged) with an expense ratio of 0.07%. The current yield is 3.0%, although costs associated with currency hedging can have a meaningful impact on returns. The maturity of the fund is 9.0 years while the duration is 7.6 years. The fund is heavily exposed to Japan and Europe, with Japanese bonds making up 16% and European bonds making up 55% of total holdings. Emerging Market bonds make up just 6.5% of total holdings. As for credit quality, around half of the bonds are rated AAA or AA.

BNDX Holdings By Country (Vanguard.com)

Yields Are Now Reasonable, But Not Attractive

At 3.0%, the yield on the BNDX is reasonable, if not attractive. While I do not have exact data on where yields were a year ago, I suspect they were around 1%. Long-term inflation expectations are also down slightly over the past year, so as a USD-denominated bond fund, real return prospects have improved significantly over the past 12 months. Based on the 10-year U.S. breakeven inflation expectations rate of 2.3%, real returns on the BNDX are expected to average 0.7%, which compares to 1.8% on the Vanguard Total Bond Market ETF (BND), which is entirely focused on the U.S. market.

This 0.7% yield is also below par when compared against international stocks. The MSCI World ex-U.S. index offers a dividend yield of 3.4%, and as stocks are real assets in that their dividends tend to rise in line with inflation, the real yield on international bonds is clearly inferior.

A Renewed Focus On Monetary Stimulus Would Be Bitter Sweet For Bondholders

For investors in the BNDX to achieve real returns over the coming years that exceed those likely to be seen in U.S. bonds and international stocks, we would need to see yields fall materially from current levels. In order for this to occur we would likely need to see renewed global disinflationary pressures, or a shift in focus across European and Japanese monetary authorities towards suppressing bond yields despite still-elevated inflation.

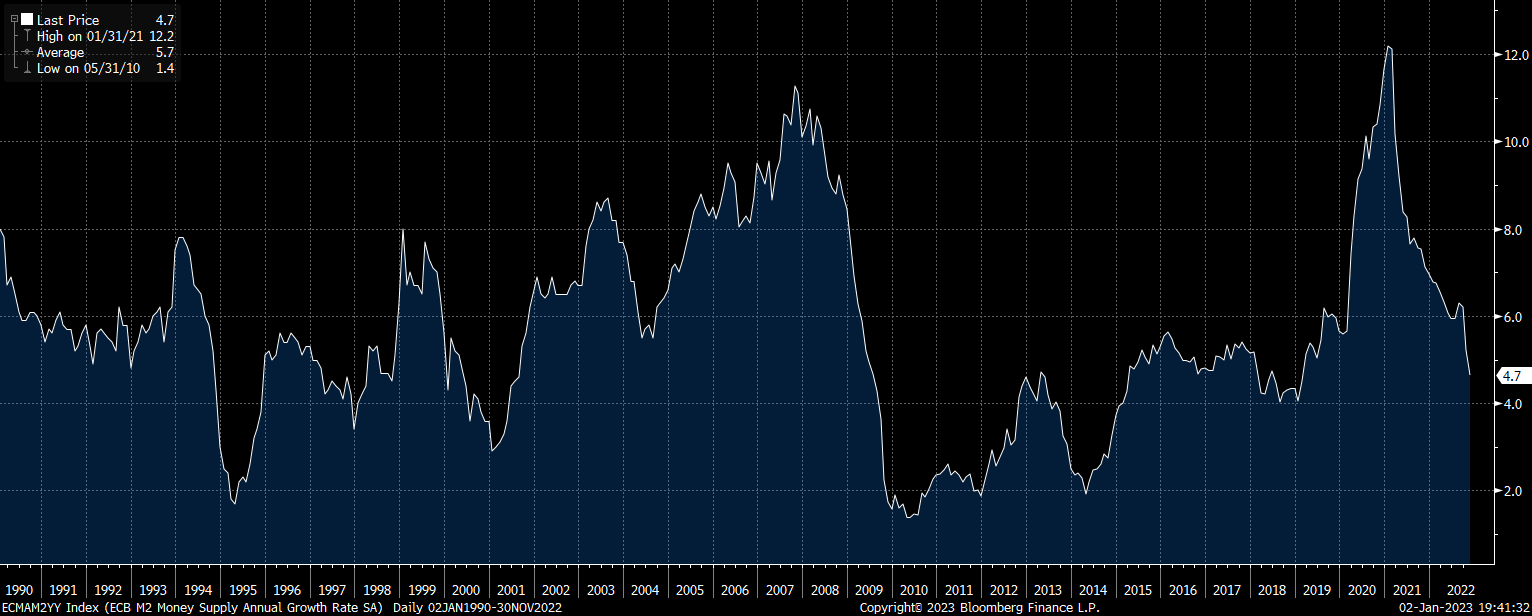

The prospect of renewed disinflationary pressures in Europe appears low. Unlike in the U.S., M2 money supply growth remains at 4.7%. Furthermore, while many investors are locked into the belief that weak real GDP growth is inherently disinflationary, this is not the case as I explained ‘Understanding The Real Drivers Of Inflation‘.

ECB M2 Money Supply Growth, % (ECB)

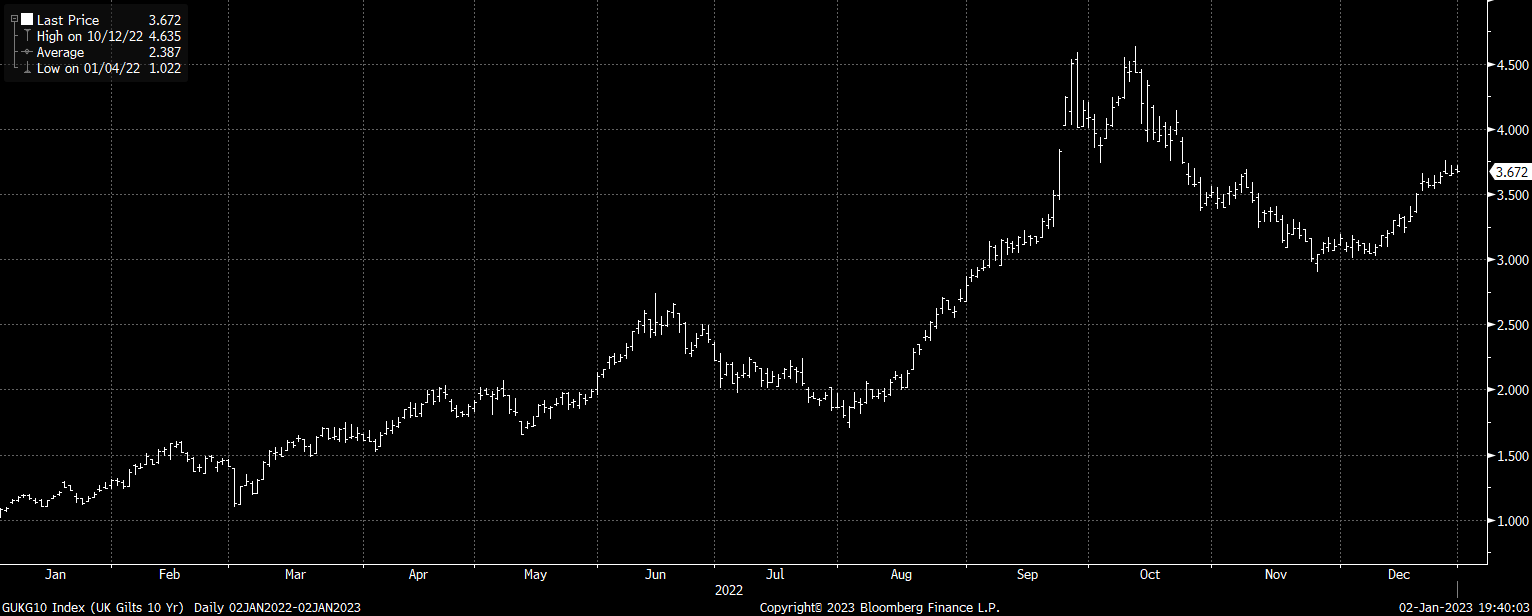

As for the potential for monetary authorities to abandon the inflation fight in favor of preventing rising bond yields from causing a debt crisis, there is certainly a case to be made. While the Bank of Japan appears to be moving in the opposite direction with its recent move to allow bond yields to move higher, we saw in the U.K. in September that bond market calm takes precedence over elevated inflation once the real economic impact of high yields begins to be felt.

U.K. 10-Year Bond Yield, % (Bloomberg)

That said, any shift towards increased bond buying across international markets would likely also raise long-term inflation. While falling bond yields would generate outsized returns for BNDX holders in the short term, these returns would merely come at the expense of lower future returns, particularly in terms due to higher inflation. In such a scenario, the BNDX should still be expected to lose out relative to U.S. bond and international stock indices.

Summary

After a sharp rise in yields over the past year, international bonds are not the terrible investment that they once were, and positive real yields are now expected over the long term. That said, returns are likely to be subpar compared to U.S. bonds and international stocks. While a policy shift in favor of supporting growth would likely generate positive near-term returns, the impact of higher inflation would cause more substantial underperformance over the long term.

Be the first to comment