porcorex

A good number of BDCs have fallen materially over the past year. While the bigger names like Ares Capital (ARCC) and Owl Rock Capital (ORCC) attract a lot of attention, I also see value in lesser followed names that also support a high yield.

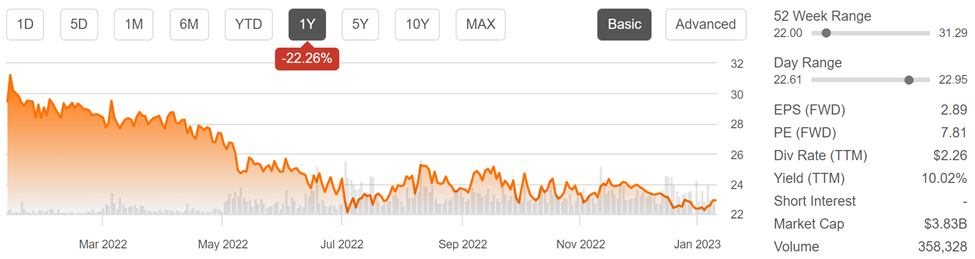

This brings me to Blackstone Secured Lending Fund (NYSE:BXSL), which, as seen below, has fallen by 22% over the past year and trades just a few percentage points above its 52-week low of $22. In this article, I highlight what makes BXSL a very appealing choice for high income investors at present.

BXSL Stock (Seeking Alpha)

Why BXSL?

Blackstone Secured Lending Fund is a BDC that’s managed by Blackstone (BX), one of the biggest asset managers in the world. This benefits BXSL in that it gains a strong network with market insights and deal flow that it would not otherwise have.

BX’s platform includes 516 credit professionals across 17 offices worldwide. Moreover, Blackstone has a long 15 year track record in direct lending with a defensive philosophy that’s resulted in just a 0.1% annual loss rate among its investment vehicles.

BXSL was launched four years ago, and recently passed its one-year anniversary as a public company. In a good move for BXSL’s shareholders, BX also charges a low base management fee of just 0.75% for BXSL’s initial 2 years, and 1% thereafter. This compares favorably to most other externally managed BDCs such as Ares Capital, which charges a 1.5% base fee.

At present, BXSL carries a well-diversified portfolio across 172 companies. It has zero assets on nonaccrual, and management maintains a safe investment profile, with 98% first lien senior secured loans.

Moreover, the portfolio companies carry on average a low loan to value ratio of just 47%. Each portfolio company’s borrowing represents on average just 1% of the portfolio total, and the borrower base is overall healthy, with just 1% with fair value marked below 90% of par.

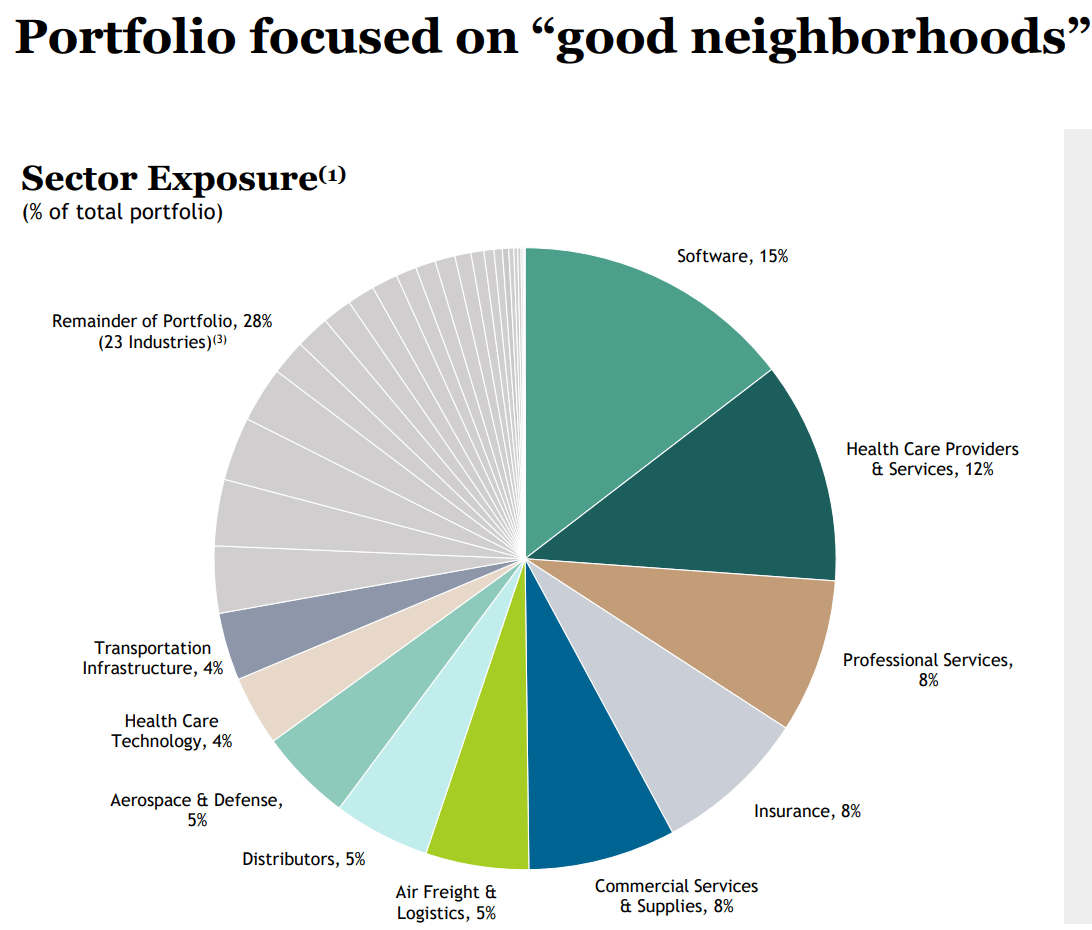

As shown below, defensive and growth industries such as software, healthcare, professional services, insurance, and commercial services and supplies make up half of BXSL’s portfolio.

BXSL Portfolio Mix (Investor Presentation)

Looking forward, BXSL is well-positioned for rising rates, with a 100% floating rate portfolio, while 58% of its debt is fixed rate. This enables BXSL to take advantage of a rising investment spread. While higher interest rates may put pressure on borrowers, BXSL’s borrowers are in overall good shape with interest coverage of 2.7x. Plus, BXSL’s investment style and structure is designed for challenging macroeconomic environments. This is supported by management’s comments during the last conference call, highlighting the low fee structure and share buybacks:

When we created BXSL and BCRED our non-traded BDC, we told investors that we would lead the market with best practices, including lowering our fees so we could build a more defensive portfolio that would protect capital in more challenging market conditions, yet still deliver attractive returns.

Despite macroeconomic headwinds on the horizon, we believe the outlook for BXSL shareholders is bright. Blackstone is highly focused on shareholder experience, we set our fees materially lower than the average public BDC, we’ve elected not to scrape fees for the manager. We have a performance look back mechanism and we just finished a $263 million buyback including repurchases after quarter end.

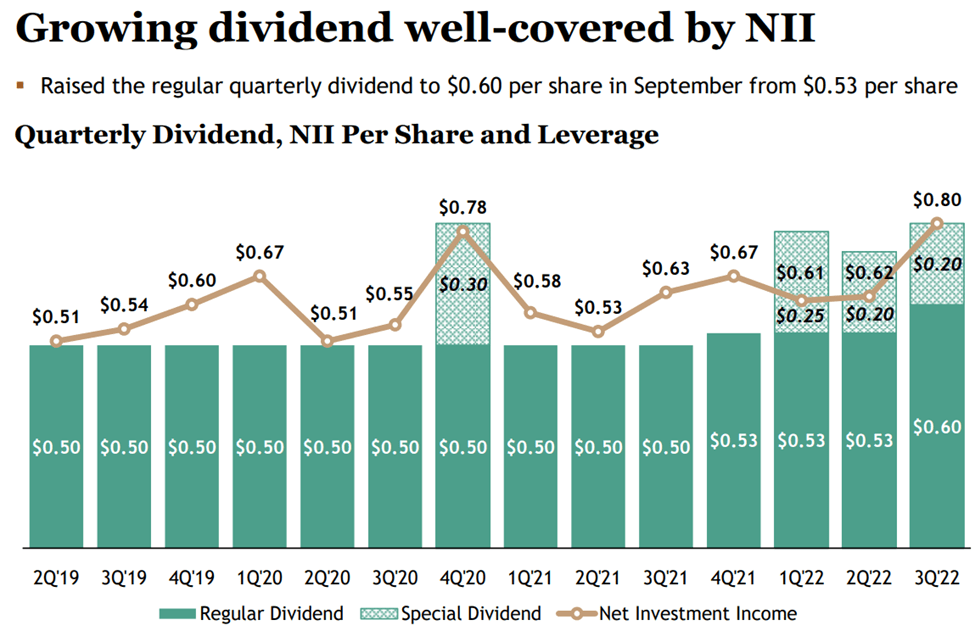

Meanwhile, BXSL carries a safe amount of leverage, with a debt to equity ratio of 1.33x, sitting well below the 2.0x statutory limit. It also raised its regular dividend by $0.07 to $0.60 and paid a special dividend of $0.20. As shown below, BXSL has maintained a covered regular dividend since 2019.

BXSL Dividend History (Investor Presentation)

Lastly, I see value in BXSL at the current price of $22.90, which equates to an 11% discount to NAV per share of $25.76. Given BXSL’s shareholder friendly structure and strong operating fundamentals, I believe it deserves to trade at least at NAV, which could result in a potential 21% total return including dividends. Additionally, analysts have a consensus Buy rating with an average price target of $26.22.

Investor Takeaway

BXSL is a well-run, externally managed BDC that carries an attractive fee structure and strong operating fundamentals. With its defensive portfolio and shareholder friendly structure, I believe it is well-positioned to generate attractive risk adjusted returns over the long term. At current levels, there appears to be good value in BXSL at an 11% discount to NAV per share, setting up investors for potentially rewarding long-term total returns.

Be the first to comment