Diy13

Article Thesis

Business development companies (‘BDCs’) offer high income yields and could benefit from a rising interest rate environment as that makes their net interest margins expand. Blackstone Secured Lending Fund (NYSE:BXSL) is one of our favorite BDCs, as it combines low risks, a high yield, and strong management, while still trading at an undemanding valuation.

Company Overview

Business development companies are specialized financial corporations that offer financing solutions to small and medium-sized businesses. These businesses that receive financing through BDCs generally can’t access public debt markets directly, due to being too small to place corporate bonds etc.

The fact that they are dependent on specialized lenders when it comes to financing their operations and future business growth means that BDCs can demand above-average interest rates on their loans, oftentimes in the 10% range. That, in turn, makes BDCs quite profitable relative to the size of their portfolios.

Blackstone Secured Lending is a BDC that has been publicy-traded since 2021, when Blackstone (BX) took it public via an IPO. BXSL’s manager, Blackstone, is one of the largest alternative asset managers in the world, with around $1 trillion in assets under management. BXSL is thus run by a successful and reputable company, which is positive for BXSL’s shareholders — it’s unlikely that they will suffer from bad management decisions, as Blackstone won’t want to risk its strong brand by running BXSL solely for its own benefit.

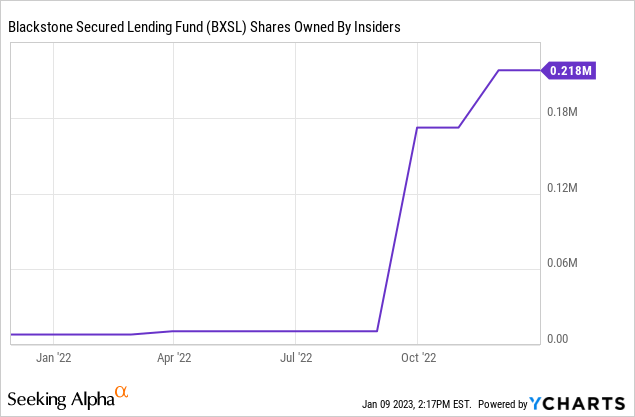

Alignment between insiders or management and shareholders is an important factor to consider. For now, insiders do not own a large stake in BXSL:

YCharts

220,000 shares equates to a little more than $5 million that insiders own in BXSL, versus a market capitalization of close to $4 billion. But importantly, the insider stake in BXSL has been growing, which is a positive sign. As insiders acquire more shares in Blackstone Secured Lending, alignment between managers and shareholders improves. On top of that, the insider buys could indicate that BXSL is trading at an attractive valuation — otherwise, those that know the company the most would likely not increase their allocation.

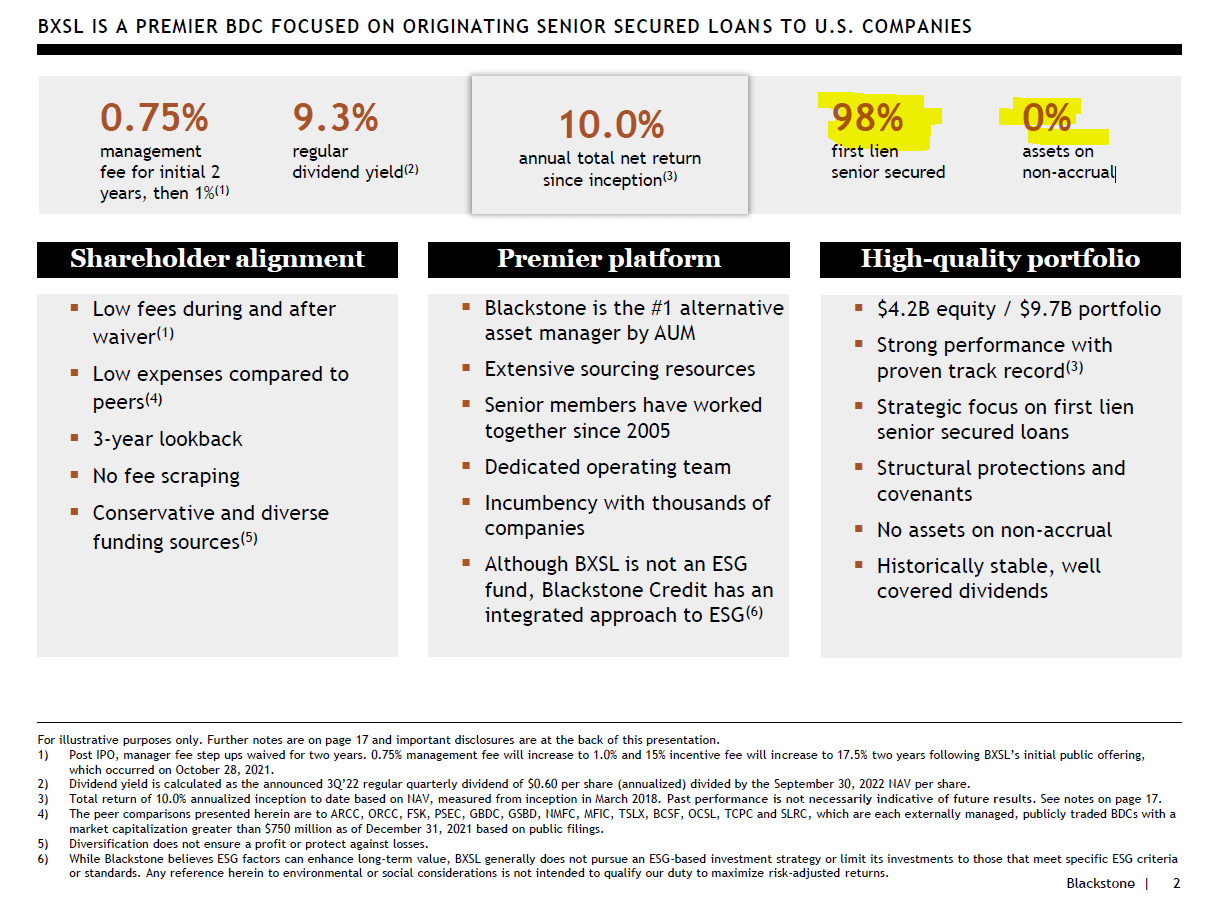

Blackstone Secured Lending is focused on low-risk loans:

BXSL presentation

98% of its assets consist of first lien senior secured loans, which can generally be described as low-risk relative to other loan investment, and especially versus equity investments. Not surprisingly, 0% of BXSL’s $10 billion in assets are on non-accrual, meaning the businesses BXSL has lent money to are up to date with their payments.

Blackstone Secured Lending also notes its low fees and shareholder-friendly policies. There is an initial 0.75% management fee that rises to 1% eventually, with a performance fee with a 6% hurdle rate on top of that. Relative to other BDCs, that makes for an attractively low level of expenses and — which has to be expected, as Blackstone isn’t a shady company, and since any questionable behavior on Blackstone’s side could hurt its brand name.

Blackstone controls or manages a couple of other BDCs as well, in total, those have around $70 billion of assets under management. Over a 15-year time frame, the annualized loss rate of Blackstone’s US Direct Lending operations is just 0.1%. The strong asset quality BXSL reports for now is thus not an outlier. Instead, it fits well with the strong asset performance that Blackstone has achieved over a long period of time in BXSL and in other lending vehicles. Proven management with a strong track record, even during difficult times, is a major positive for investors — especially for those that seek a buy-and-hold vehicle with below-average risks.

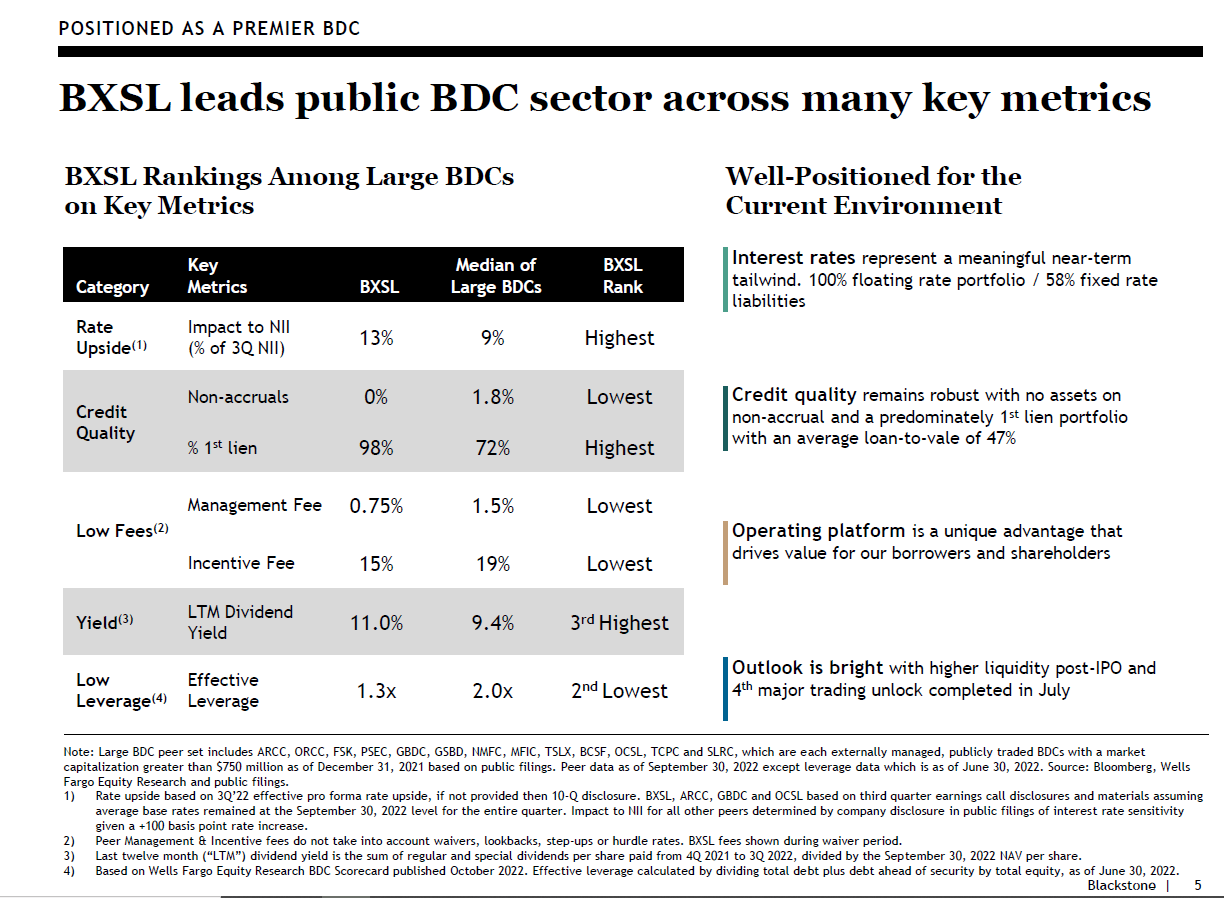

The above-average quality is also showcased by several other metrics:

BXSL presentation

Blackstone notes its strong credit quality and low expense ratio, as noted above, but also some other positives. In a rising rates environment, many BDCs see their net interest income climb. That is due to floating rate loans that will generate higher returns as interest rates increase. Most BDCs will benefit from that going forward, but Blackstone Secured Lending states that its exposure to this macro tailwind is more pronounced compared to all of its peers. Its net interest income climbs by 13%, versus a 9% average for its peer group of major business development companies.

This above-average positive impact on BXSL’s results can be explained by the fact that all of its portfolio consists of floating-rate loans, while the company has fixed the interest rates on the majority of its liabilities in the past. That was either luck or a prescient move by the company’s management team — I assume it was the latter. Management’s decision of locking in lowish rates on the money it owes while positioning the company for interest rate increase tailwinds on the asset side makes Blackstone Secured Lending a winner in the current environment, as the Fed forecasts that it will raise rates several more times this year.

Last but not least, Blackstone Secured Lending utilizes a below-average level of leverage, which reduces risks further. In combination with the first-lien debt focused portfolio, low (nonexistent) non-accruals, and a proven management team, the strong balance sheet makes Blackstone Secured Lending one of the most suitable sleep-well-at-night BDC picks thanks to its low-risk nature.

And yet, Blackstone Secured Lending still offers a highly attractive dividend to the BDC’s owners, which gets us to the next point.

A High Yield And Some Upside Potential

At current prices, BXSL’s dividend yield is 10.6%, based on the most recent dividend declaration of $0.60 for the third quarter. That’s above the peer group average, and it is also highly attractive in absolute terms.

Blackstone Secured Lending is forecasted to have earned $2.90 (we don’t know the final result yet, as Q4 results have not yet been published. That would make for a payout ratio of 83%, using a dividend level of $2.40 per year. While that is not a low payout ratio in absolute terms, it’s not high for a BDC, either. Considering BXSL’s low-risk nature and its strong credit quality, we believe that there is little risk of a dividend cut.

Even better, Blackstone Secured Lending is forecasted to see its earnings rise substantially this year. According to Seeking Alpha, the BDC is forecasted to earn around $3.50 this year, which makes for a payout ratio of just below 70% with the dividend standing at $2.40 per year. That is rather low for a BDC, thus a dividend increase during the current year would not be surprising, I believe — it’s not written in stone, however.

With Blackstone Secured Lending trading at just $23 per share, the $3.50 in profit that BXSL will earn this year, according to Wall Street analysts, translates into an earnings multiple of just 6.6. In other words, BXSL trades with an earnings yield of 15% today, which is pretty attractive.

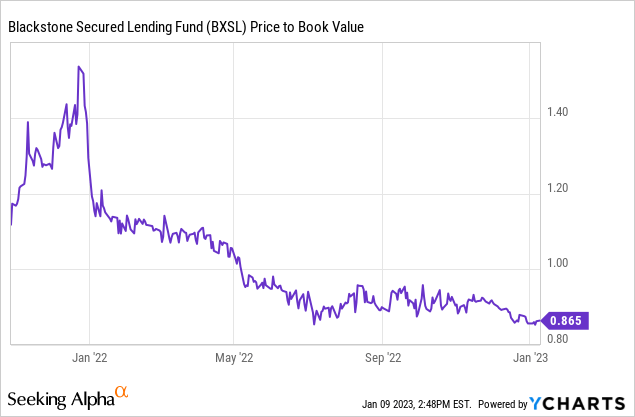

Another way to value BDCs is their book value:

YCharts

If BXSL were to trade at 1.1x book value five years from now, that would make for a 5% share price increase per year, even if BXSL were to not grow its book value at all over that time frame. Since the company does not pay out all of its earnings, which allows for some reinvestment, and since BXSL can buy back shares below book value, some book value per share growth would not be surprising. But the good news is that it wouldn’t be needed for BXSL to be a strong total return pick. Between a mid-single-digit share price growth rate and its 10%+ dividend yield, BXSL could generate mid-single digit returns even without any underlying business growth.

Takeaway

Blackstone Secured Lending is an underfollowed major BDC that has strong assets, great management, and that offers a compelling dividend yield that looks sufficiently safe. Shares also have some upside potential due to an undemanding valuation, which could translate to compelling longer-term returns for those that buy unloved BXSL at current prices.

Be the first to comment