We Are

Blackstone Secured Lending (NYSE:BXSL) is a well-managed business development firm that specializes in high-quality First Lien Senior Secured Loans.

Blackstone Secured Lending provides passive income investors with a dividend yield that is protected by net investment income, top-tier portfolio quality, and floating interest rate exposure that indicates portfolio income growth in a rising-rate environment.

In addition, the BDC’s 10.2% dividend yield is available at a discount to net asset value.

First-Lien Focused Investment Portfolio With Excellent Portfolio Quality

Blackstone Secured Lending is a First Lien-focused BDC backed by Blackstone, one of the world’s largest and most well-known alternative asset managers.

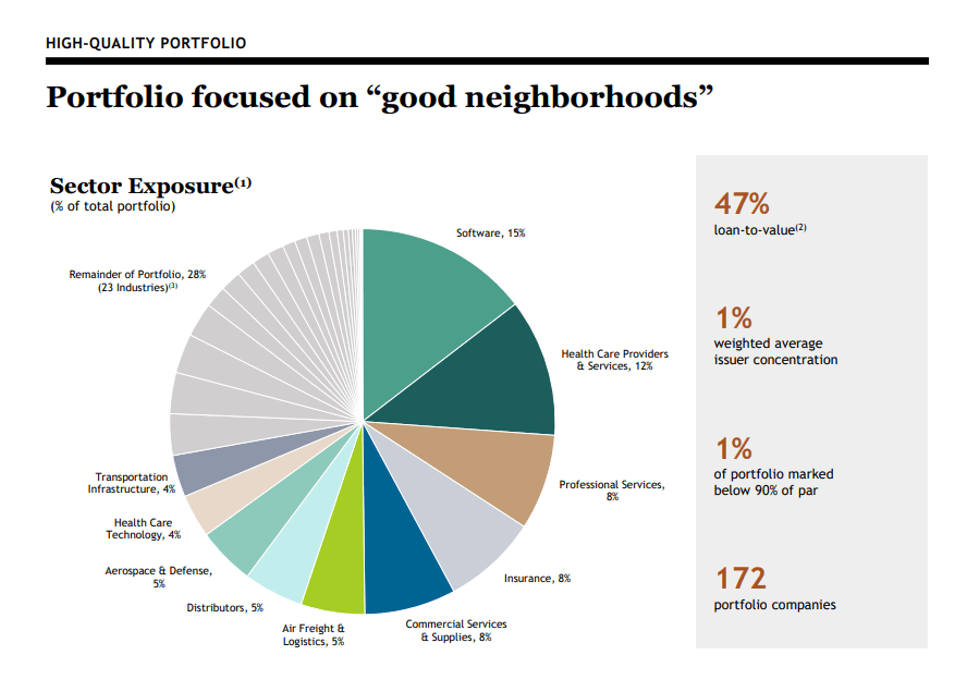

As of September 30, 2022, Blackstone Secured Lending had 172 portfolio companies with a total investment value of $9.7 billion. According to a portfolio breakdown, the BDC invested 97.9% in First Lien Senior Secured Debt, 0.7% in Second Lien Senior Secured Debt, and 1.4% in Equity.

As shown below, BXSL invests primarily in recession-resistant sectors such as software (15%), health care products/services (12%), professional services (8%), insurance (8%), and commercial services (8%). These industries promise stable cash flows and lower the risk of default.

Portfolio Overview (Blackstone Secured Lending)

One of the distinguishing characteristics of Blackstone Secured Lending is that the business development company had no non-accruals in its portfolio as of September 30, 2022, indicating that the portfolio was performing as expected.

The BDC’s impressive portfolio quality ranks it alongside Oaktree Specialty Lending Corporation (OCSL), which I regard as the gold standard in the BDC sector.

Floating Rate Exposure

The central bank is under pressure to raise interest rates as inflation reaches 40-year highs in 2022 and 2023, respectively, in my opinion. In a rising-rate environment, Blackstone Secured Lending’s floating-rate debt portfolio (99.9%) is expected to generate higher net interest income.

Based on interest rates in effect at the end of the September quarter, the business development company estimates that it could earn $0.10 per share more in net investment income per quarter than it did in 3Q-22.

Because the Fed is expected to raise interest rates further in 2023, Blackstone Secured Lending’s floating rate debt portfolio stands to profit, potentially leading to special dividend payments.

Estimated Quarterly NII (Blackstone Secured Lending)

Dividend Well Covered

In the last twelve months, Blackstone Secured Lending earned $2.69 per share in net investment income and $0.80 per share in 3Q-22. BXSL achieved a dividend pay-out ratio of 81% with a combined dividend pay-out of $2.19 per share, which is quite good for a business development company with a First Lien focus.

The pay-out ratio was 75% in 3Q-22, despite the fact that the BDC increased its dividend from $0.53 to $0.60 per share per quarter, a 13.2% increase QoQ.

Blackstone Secured Lending also pays special dividends to distribute excess portfolio income, but those payments are difficult to forecast and plan for, so I exclude them from my yield calculation.

Blackstone Secured Lending’s stock has a covered 10.2% dividend yield based on a quarterly dividend payment of $0.60 per share.

Dividend and NII (Blackstone Secured Lending)

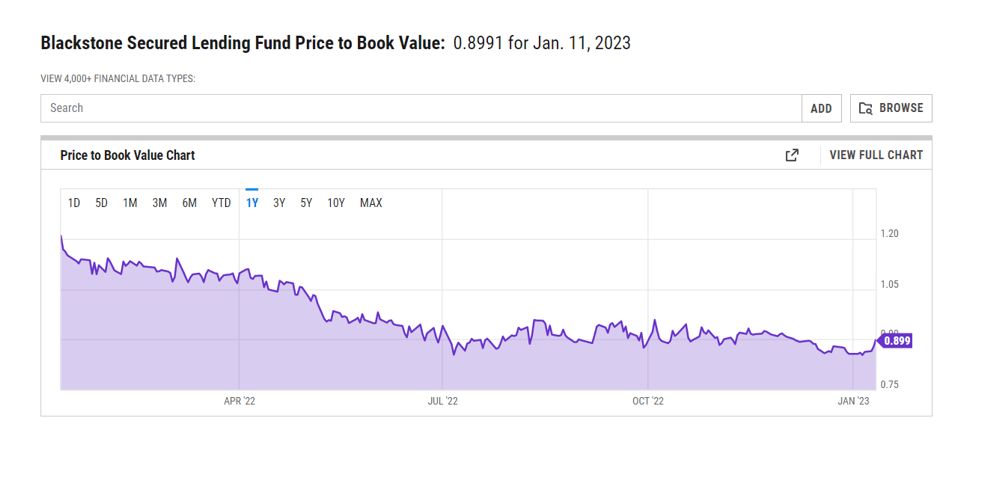

Discount To Net Asset Value Is Undeserved

Given that Blackstone Secured Lending has 0% non-accrual investments, I don’t think the business development company’s stock should be trading at a 10% discount to net asset value, but it is, and this presents an opportunity to purchase BXSL.

Oaktree Specialty Lending’s stock, for example, is currently trading at a 5% premium to net asset value, and Oaktree’s BDC has 0% of its investments in non-accrual status.

Furthermore, I believe Blackstone Secured Lending’s portfolio is safer than Oaktree’s because OSCL has 71% of its investments in First Liens versus 98% for BXSL.

Price To Book Value (YCharts)

Why Blackstone Secured Lending Could See A Lower Valuation

Non-accruals could change the game for Blackstone Secured Lending, but given the BDC’s strict focus on First Liens, I don’t see the portfolio quality deteriorating in the near term.

However, a deterioration in capital market health, combined with rising lending standards and rising defaults, could create headwinds for BXSL’s portfolio and net investment income growth.

The same is true for the central bank reversing the rate-hiking cycle, which could result in the BDC’s dividend coverage deteriorating.

My Conclusion

In my opinion, Blackstone Secured Lending is a high-quality business development firm in the truest sense of the term. The portfolio has no non-accruals and is primarily composed of highly rated First Lien debt instruments.

Blackstone Secured Lending also has significant floating rate exposure, which may help the BDC improve on its already solid dividend pay-out ratio.

When the 75-81% pay-out ratio is considered, the dividend appears to be on the rise, and investors may even see additional special dividend payments in 2023.

Based on portfolio quality and pay-out ratio, the stock does not deserve to be sold at a 10% discount to book value.

Be the first to comment